Sometimes you hear a news story that totally rocks your world, and you spend an inordinate amount of time trying to make sense of it. Last week I read the third largest bank in the United States, Wells Fargo, with $1.7 trillion in assets was shuttering all personal lines of credit with its customers.

This story is quite puzzling for many reasons. At its core, the entire purpose of the banking industry is to boost loan growth. When one of the largest banking institutions, with over 70 million customers, purposely curtails loan growth, by closing all existing lines of credit, I think it is worth pondering and trying to understand why.

The Wells Fargo revolving credit lines, typically let users borrow $3,000 to $100,000, were a viable way for customers to consolidate higher-interest credit card debt, pay for home renovations or avoid overdraft fees on linked Wells Fargo checking accounts.

Wells Fargo Customers credit scores may be adversely affected by this move, which is how most in the media interpret this inconvenience. I tend to look at it much more organically.

Imagine a lumber distributor stopping its selling of certain wood products?

Or a steel manufacturer no longer selling steel beams used for construction?

Or ponder why your grocer might suddenly stop selling meat. The first question you could ask is, did he have a vegan conversion? Or is there a problem with the meat?

When the Federal Reserve manipulates Interest Rates and bypasses the free market process of price discovery, the unintended consequence is our previous definitions of risk are no longer functional. This results in massive price distortions as markets try to understand what is occurring.

The most important definition in finance is how you define risk.

When this definition is unclear, chaos can easily prevail in the markets.

Today RISK has never been more prevalent. The challenge, dear reader, is how can you eliminate risk at all when the Fed has pushed interest rates to zero in the hopes of increasing economic growth?

Imagine you are trying to help a widow or orphan save their nest egg and are not interested in taking any risk. In the past, what any fiduciary would do is invest in money market funds, treasury bills or treasury bonds. These staples of the financial markets were the islands where individuals could remove themselves from risk. They might only earn 2% or 3% yield on their investment. Since inflation was less than that yield, these widows and orphans would protect the purchasing power of their savings.

Not anymore. Today it is impossible.

Since the Fed has pushed interest rates down to close to ZERO and last month’s Consumer Price Index number was 5.4%, anybody who has their money parked in these short-term treasury assets will experience a greater than negative 4% real rate of return every year.

In other words, the best that you could do for a widow and orphan today is guarantee them that they would lose 4% per year on their savings.

This problem compounds for banks, as depositors do not want to lose money on their deposits, so they only keep a minimal amount in the banking account. Since depositors are keeping less money in the bank, the bank has less money to invest in productive loans.

It is a horrible, vicious cycle.

What makes this action on the part of Wells Fargo so confusing is that Wells Fargo is literally returning the funds to the Fed that it borrowed from the Federal Reserve.

Last year, Wells Fargo halted all new home equity lines of credit. Months later, the bank also withdrew from a large segment of the auto lending business.

Stop and think about that. Particularly since housing prices are up over 15% year over year and many used car prices are up over 30% in the same time frame.

Why would a top lender in those markets stop lending?

That is a real head scratcher until I saw this headline:

While not privy to the goings on at the board meetings of the large banking institutions, my take on this is that Wells Fargo and J.P. Morgan are thinking that it is much riskier to loan funds now.

They are analyzing their loan portfolios and have concluded that risk outweighs return in the personal credit sector. You may disagree with their decision. However, keep in mind these institutions were central to the 2008 Great Financial Crisis, what is it that is stopping them from lending now?

Is it possible that they too are being squeezed by the low interest rate environment? Might they require a higher yield and return on investment to compensate for what they perceive to be a greater chance of default on the part of the borrower?

What is clear is that both J.P Morgan and Wells Fargo perceive that there is greater counterparty risk in the financial system now.

What is worthy of every investor and trader’s attention is to ponder the potential consequences of what occurs when a bank curtails lending.

If people couldn’t borrow, do you think the housing prices would continue moving higher? The totality of economics is the puzzle of supply and demand reaching an equilibrium. When the Fed manipulates the cost of money it distorts the definition of risk, and even the largest financial institutions are forced to wrestle with how they can safely navigate the landscape.

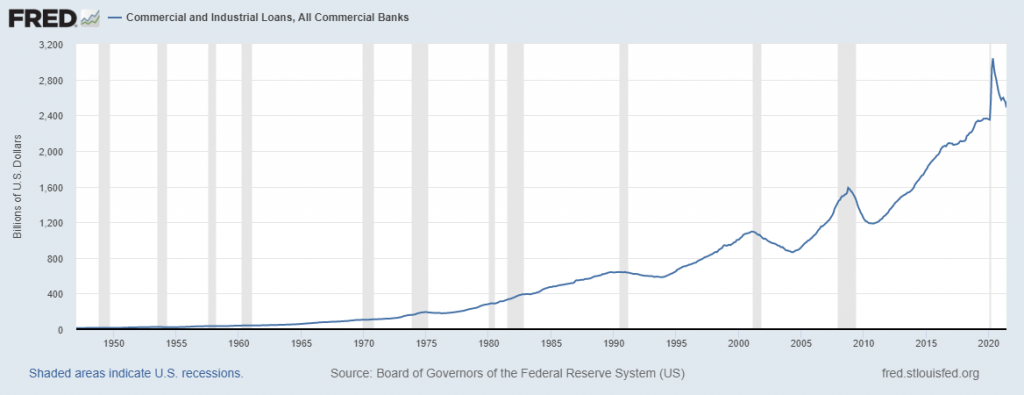

Here is a chart published by the St. Louis Federal Reserve of all Commercial and Industrial Loans at all Commercial Banks going back to 1950. You can see how loan activity has exploded exponentially initially since we came off the Gold Standard in 1971. Since the 2008 Financial Crisis Commercial Loans have gone up 150%. The shaded areas are recessions in the economy.

Observe how since the pandemic began the rise of loan activity has been almost straight up.

Before the Great Financial Crisis in 2008, Commercial loan activity contracted by 23%!

What is concerning to Fed Watchers is that since last Summer Commercial Loan activity has contracted 19%! That is the steepest decline since the Great Financial Crisis.

Could this be what is spooking the banks?

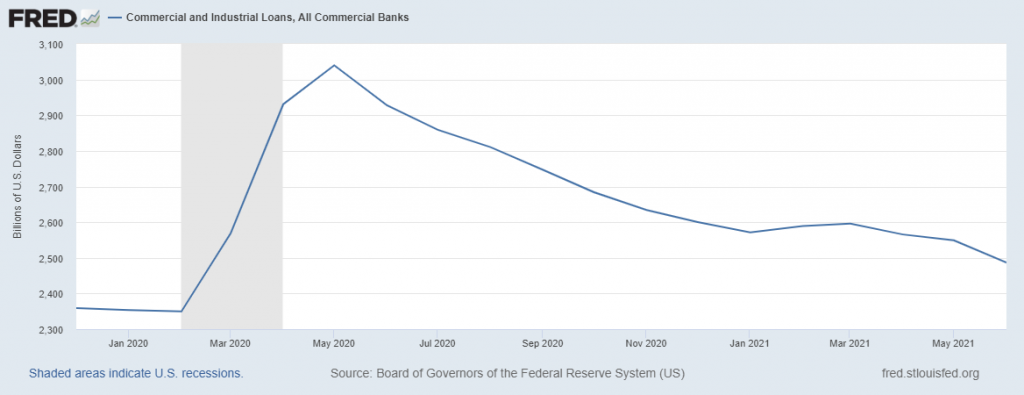

Here is a closeup of Commercial Loan activity of the past year.

Money and credit are what drives the economy.

Why is this of concern?

We live in a credit-based world. If lending does not occur, then neither does commerce and the potential consequences could be severe.

Why is this important?

If banks are struggling to define risk, you can rest assured that spells huge volatility in the financial markets for their customers.

When the largest banks in the country curtail personal loans accompanied by massive commercial loan contraction, my question is where is the money going to come from to drive price higher?

I would challenge you to pay very close attention to next month’s Consumer Price Index and Producer Price Index Reports If those numbers are elevated my expectation is that Commercial bank lending will contract further.

That could be disastrous.

It could also be wonderful.

That is, if you are on the right side of the market.

That is why I would urge you, regardless of your opinion, to pay very close attention to the artificial intelligence forecasts.

I love the bearish side of the market. The old Wall Street adage that bull markets take the stairs, but bear markets take the elevator is very true. I have a very bearish opinion on the stock market. But what may surprise you is that I do not let my fundamental analysis get in the way of what I do in the market.

The artificial intelligence guides my trading decisions 100%.

When my opinion, coincides with the A.I., I embrace the certainty of my conviction and position myself accordingly.

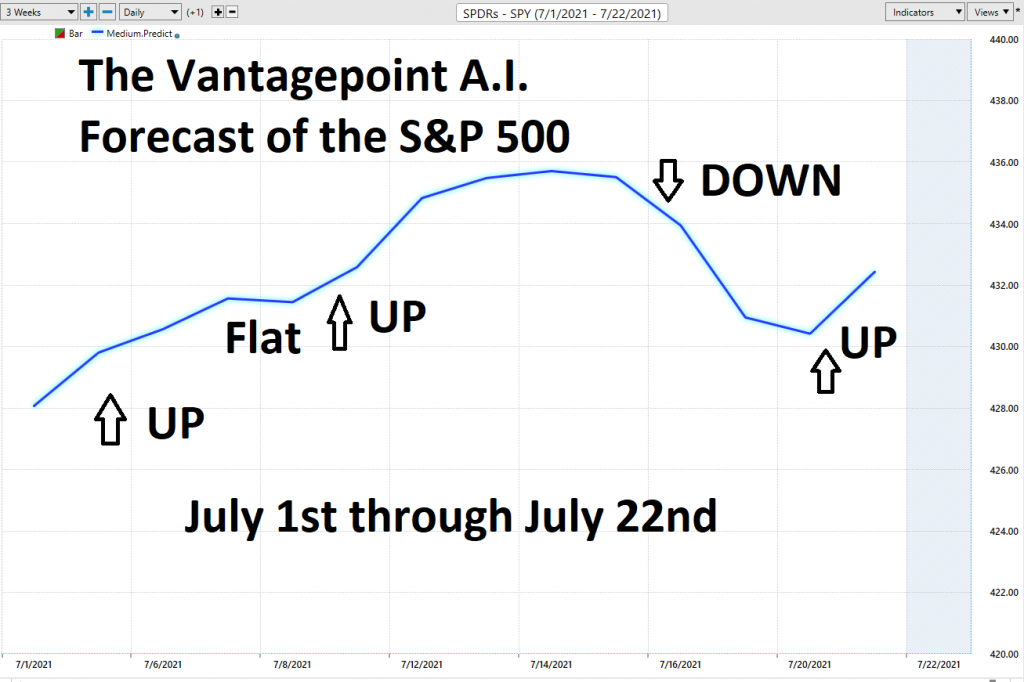

Down below is what the artificial intelligence forecast looks like in the S&P 500 over the past three weeks.

The key to the VantagePoint analysis is the predictive blue line. The slope and general direction of the blue line determines the medium forecast for the market.

To understand and appreciate how powerful this indicator is, we’ll remove the daily price bars on the chart.

- The slope of the predictive blue line determines the short-term trend. On the following graphic, you would want to look for opportunities to buy when the slope of the blue line is going up.

- When the slope of the blue line is going sideways you would be anticipating sideways prices.

- Likewise, when the slope of the blue line is going down you would be anticipating lower prices.

Trading with artificial intelligence is the best way to minimize risk by having statistical certainty that you are on the right side of the right market at the right time.

How good are you at making decisions?

What has your performance been this year?

What’s Your Best Chance to Make Money in The Financial Markets Today?

The Answer A.I. Offers Will Surprise You. Intrigued?

You too can start finding the best trend at the right time regardless of your experience.

After all, A.I. has beaten humans at Poker, Chess, Checkers, Jeopardy and Go. Why should trading be any different?

Intrigued? Visit with us and check out the A.I. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.