Warren Buffett didn’t just master the markets — he reshaped the way generations of investors think about money, time, and value. Over the course of nearly six decades, he transformed Berkshire Hathaway from a struggling textile firm into one of the most valuable and respected conglomerates in the world, not by chasing trends or timing the market, but by articulating and executing a philosophy that prioritized quality, discipline, and patience. To many, he wasn’t just the “Oracle of Omaha” — he was the embodiment of rational optimism in a world often ruled by short-term panic and speculative fervor.

Now, as Buffett signals his retirement from active leadership, the financial world is experiencing something akin to a tectonic shift. The man who once said his favorite holding period was “forever” is finally stepping back — and in doing so, he leaves behind more than just a mountain of returns. He leaves a framework for long-term thinking that remains radically underappreciated in today’s algorithmic, adrenaline-fueled market. His legacy is not simply in what he bought, but in how he thought. And for investors and traders alike, the lessons in temperament, trust, and time are more relevant now than ever.

Buffett turned a dusty textile company into a financial freight train with a mind-melting return of over 5,500,000% since the mid-1960s. Yeah, you read that right. Five million. Five hundred thousand. Percent.

If you had the stones to drop $1,000 into Berkshire Hathaway back when Buffett took the reins, you’d be sitting on more than $55 million today. Not a typo. No meme stock, no NFT, no crypto rocket ride has come remotely close to that kind of long-term compounding firepower.

So how did he do it?

Not with hype. Not with leverage. Not with luck. Buffett built that empire on a slow, steady, and ruthlessly disciplined strategy: Buy great businesses. Run them better. Hold them forever. He didn’t chase fads — he bought Coca-Cola when people were panicking, Apple when most “value” guys were still clutching their fax machines, and railroads when no one gave a hoot.

Here’s the lesson every trader, investor, and market junkie needs to tattoo on their brain: Fortunes are made by buying quality while everyone else panics. Buffett didn’t just create money — he created a masterclass in focus, patience, and staying power.

Benjamin Graham, Warren Buffett’s mentor at Columbia, is known as the father of value investing. His core philosophy was simple but rigorous: buy stocks trading for less than their intrinsic value, especially those selling below their net asset value. He focused heavily on financial statements, balance sheet strength, and a “margin of safety” — the idea that buying cheap gave investors a cushion against mistakes or market downturns.

Graham’s approach was mechanical and defensive. He looked for “cigar butt” stocks — companies that might be on their last puff but still had a little value left. If a company was worth $10 and trading at $5, Graham was interested, regardless of the company’s future prospects.

Buffett started as a Graham disciple, but over time, he evolved. He realized that buying cheap companies was not enough — you also had to buy great companies with strong brands, predictable earnings, and competitive advantages (what he calls “moats”). He famously said, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Similarities:

- Both prioritize intrinsic value over market noise.

- Both demand a margin of safety in every investment.

- Both reject speculation in favor of rational, data-driven analysis.

Differences:

- Graham focused on price and balance sheets; Buffett focuses on quality and long-term business economics.

- Graham bought cheap stocks; Buffett buys great businesses.

- Graham was happy to sell when a stock hit its fair value; Buffett prefers to hold forever if the business remains strong.

Buffett took Graham’s defensive playbook and turned it into an offensive powerhouse by adding one key ingredient: quality.

Let’s break down the four cornerstone principles of Warren Buffett’s investing philosophy—starting with the concept he popularized more than anyone else: the durable moat.

Durable Moat: The First Line of Defense

Buffett isn’t just buying stocks — he’s buying fortresses. A “durable moat” is what protects a business from competition. It could be brand loyalty (like Coca-Cola), network effects (like American Express), high switching costs (like Apple), or regulatory barriers (like Moody’s). The key is that the company has something sustainable that keeps others from eating its lunch.

Buffett doesn’t want to know how a company will do next quarter—he wants to know that 10 years from now, it’s still the dominant player in its space. A strong moat means pricing power, customer retention, and long-term cash flow. Without it, even a great product can become irrelevant fast.

Capable, Trustworthy Management

Buffett has always been clear: he invests in people just as much as in businesses. He looks for leaders who are rational capital allocators, honest about mistakes, and skilled at running operations efficiently.

He famously avoids meddling. Once Berkshire buys a company, he trusts management to run it. But they have to earn that trust. He admired Roberto Goizueta at Coca-Cola, Tim Cook at Apple, and Ajit Jain within Berkshire itself — not because they dazzled markets, but because they made smart, durable decisions that maximized long-term value.

Consistent Profitability

Buffett wants companies with predictable, reliable earnings. Flashy growth means nothing if profits are erratic. His favorite businesses generate steady cash flows across economic cycles — think See’s Candies, which sells more chocolate in good times and bad, or BNSF Railway, which moves freight whether markets are soaring or sinking.

These businesses often have high returns on equity, low capital requirements, and long operating histories. The ability to compound capital at a high rate without constant reinvestment is what turns good companies into Buffett companies.

A Fair Price

Buffett isn’t a bargain-bin investor anymore — he’s a value realist. He’s willing to pay a fair price for a wonderful business, because time and compounding will do the rest. Overpaying can kill returns. But underpaying for junk is even worse.

He calculates intrinsic value based on future cash flows and buys only when the market gives him a margin of safety. If it doesn’t, he waits. That discipline is why he passed on thousands of companies and still built Berkshire into a $900+ billion powerhouse.

In short: Buffett’s principles aren’t flashy — but they’re forged in logic, discipline, and decades of data. Traders chase what’s hot. Buffett chases what lasts. That’s the difference.

There are shelves full of books about the Oracle of Omaha. Slick covers. Fancy titles. Endless praise. And sure, they’re entertaining, you’ll get some folksy quotes, a few anecdotes about Cherry Coke and bridge games, and maybe a warm fuzzy about compound interest. But let me tell you where the real education is: not in the stories, but in the stocks.

You want a world-class financial education? Don’t read about Buffett — reverse engineer the guy. Strip down his portfolio. Take apart every position. Ask yourself why he bought it, how long he’s held it, what it earns, and what “moat” it’s hiding behind. This isn’t theory. This is the playbook of a man who turned $1 into over $500,000 since 1965. And the best part? You don’t need an MBA or a seat at the Berkshire table to get started. Everything you need is sitting in his top ten holdings, which I’m about to lay out for you — clean, clear, and ready to study like your future depends on it. Because if you’re serious about building wealth, it does.

As of December 31, 2024, Berkshire Hathaway’s top 10 equity holdings, based on publicly available data, are as follows:

- Apple Inc. (AAPL) – Approximately 28.1% of the portfolio. Berkshire began acquiring Apple shares in 2016, recognizing its strong brand and customer loyalty.

- American Express Co. (AXP) – Around 16.8% of the portfolio. Buffett has held this position since 1964, valuing its durable competitive advantage and consistent earnings.

- Bank of America Corp. (BAC) – Approximately 11.2% of the portfolio. Berkshire started investing in BAC in 2011, attracted by its extensive banking operations and potential for growth.

- The Coca-Cola Company (KO) – Roughly 9.3% of the portfolio. Buffett began purchasing Coca-Cola shares in 1988, impressed by its global brand recognition and steady cash flows.

- Chevron Corp. (CVX) – About 6.4% of the portfolio. Berkshire’s investment in Chevron reflects confidence in the energy sector and the company’s dividend yield.

- Moody’s Corporation (MCO) – Approximately 4.4% of the portfolio. Buffett appreciates Moody’s dominant position in credit ratings and its consistent profitability.

- Occidental Petroleum Corp. (OXY) – Around 3.3% of the portfolio. Berkshire has increased its stake in Occidental, viewing it as a strategic play in the energy sector.

- The Kraft Heinz Company (KHC) – About 3.2% of the portfolio. Berkshire’s involvement dates to the merger of Kraft and Heinz, emphasizing long-term value in consumer staples.

- U.S. Bancorp (USB) – Approximately 2.5% of the portfolio. Buffett values its conservative banking practices and strong regional presence.

- DaVita Inc. (DVA) – Around 1.9% of the portfolio. Berkshire’s investment in DaVita highlights interest in the healthcare sector, particularly in dialysis services.

These holdings reflect Buffett’s investment philosophy of acquiring companies with strong fundamentals, competitive advantages, and reliable earnings.

Here’s Warren Buffett’s Timeless Investment Checklist, crafted in a way that traders and long-term investors can apply immediately. Think of this as your “Buffett Filter” for finding quality companies worth holding — or at least paying attention to when they show relative strength.

Warren Buffett’s Investment Checklist

1. Is the business easy to understand?

- Can I explain what it does in one sentence?

- Do I understand how it makes money?

- Is the business model predictable?

Example: Coca-Cola sells drinks. You get it. Simple businesses are harder to disrupt.

2. Does the company have a durable competitive advantage (a “moat”)?

- Does it have brand loyalty, patents, pricing power, or scale?

- Are customers likely to stay for years?

- Can competitors copy it easily?

Example: Apple’s ecosystem locks users in—hardware + software + services.

3. Is the company consistently profitable?

- Has it shown strong earnings over multiple years?

- Are margins stable or improving?

- Are earnings real—not based on accounting gimmicks?

Example: Moody’s produces consistent high-margin profits from credit ratings.

4. Is it run by capable and trustworthy management?

- Do they treat shareholders well?

- Are they transparent and rational in capital allocation?

- Would Buffett want to partner with them in private business?

Buffett’s Rule: “You can’t do a good deal with a bad person.”

5. Does it generate strong return on equity (ROE) without excessive debt?

- Is it earning a high return on shareholders’ money?

- Can it grow without borrowing too much?

Buffett loves businesses with high ROE and low debt.

6. Is there strong and growing free cash flow?

- After all expenses, does the business produce excess cash?

- Is that cash reinvested wisely or returned to shareholders?

Cash is king—Buffett wants businesses that produce it predictably.

7. Is the stock trading at a fair (or better) price?

- Am I getting more value than I’m paying for?

- What’s the intrinsic value vs. current price?

Buffett isn’t obsessed with the cheapest stock — he wants quality at a fair price.

8. Would I be happy owning this company for 10+ years?

- Could I ignore the market and still be confident in holding this?

- Would I feel fine if the stock market shut down tomorrow?

This is Buffett’s “forever test.”

Let’s apply this Check list to a handful of Buffett’s top investments.

Coca-Cola ($KO)

Warren Buffett’s 1988 move to load up on Coca-Cola wasn’t some casual bet on sugar water — it was a calculated, long-term punch right in the face of Wall Street’s obsession with complexity. While most investors were still nursing their wounds from the ‘87 crash, Buffett dropped $1 billion on a business everyone thought was boring. But that’s the point. Coca-Cola wasn’t just a drink; it was a global addiction wrapped in red and white. Buffett saw what others missed: a brand so powerful it could raise prices during recessions, a distribution network that blanketed the planet, and a product that billions consume daily without even thinking about it. And best of all, it was throwing off consistent, predictable cash like clockwork — without needing to dump billions into capital upgrades. The return on equity was sky high, the need for reinvestment was low, and the moat? Unbreakable.

He also trusted the guy at the helm — Roberto Goizueta, a CEO who understood scale, marketing dominance, and how to squeeze every ounce of value out of a global empire. Buffett knew he was buying a machine that could run itself while sending him checks for decades. And the icing on the cake? The stock was undervalued because the market was still shaking from Black Monday. While the herd was panicking, Buffett was backing up the truck on a business he could understand with his eyes closed. This wasn’t just a smart trade. It was Buffett’s entire philosophy — brand power, cash flow, trustworthy management, and a fair price — all wrapped up in a red can.

Here are the specifics on Buffett’s Coca Cola Investment in 1988 which has become a legendary case study of his strategic philosophy:

Purchase Details

- Year Purchased: 1988 (continued buying through early 1989)

- Total Investment: $1.02 billion

- Number of Shares Purchased: 23.35 million shares

- Average Purchase Price: Approximately $43.81 per share (pre-split)

Stock Splits Since 1988

Coca-Cola ($KO) has split its stock two times since Buffett’s purchase:

- May 1, 1990 – 2-for-1 split

- August 13, 2012 – 2-for-1 split

Effective total split factor: 4-for-1 So Buffett’s 23.35 million shares became 93.4 million shares after both splits.

Dividend Details in 1988

- Dividend per share (1988): $0.40 annually

- Based on his cost basis of ~$43.81/share, Buffett’s initial dividend yield was around 0.9%.

But here’s the magic of long-term investing and quality compounding:

Dividend on Cost Today

- 2024 Dividend: $1.94 per share (annually)

- His original shares now pay $1.94 x 4 = $7.76 per original share (adjusted for splits).

- On his cost basis of $43.81, that’s a dividend yield on cost of ~17.7% annually.

Total Return Since 1988

Let’s break it down:

Capital Appreciation

- Adjusted share price (post-splits) as of May 2025: ~$61/share

- His cost basis (adjusted): $10.95/share

- Capital gain multiple: ~$61 ÷ $10.95 = ~5.57x

Dividends Collected Over 36 Years

- Cumulative dividends per share since 1988: ~$25 (split-adjusted)

- Total dividends on 93.4 million shares: Over $2.3 billion in cash payouts

Total Return Estimate

- Berkshire’s initial $1.02 billion investment is now worth about $5.7 billion in stock alone.

- Add over $2.3 billion in dividends.

- Total return exceeds $8 billion, or a return of nearly 700%, excluding reinvestment.

Buffett turned a “low-yielding” soda stock into a cash-generating empire, proving that buying high-quality, durable brands — even at what looks like a full price — can deliver staggering long-term returns.

American Express ($AXP)

Buffett began investing in American Express ($AXP) in the 1960’s and added to his position in 1994. His investment became one of his longest-held and most profitable positions. Like Coca-Cola, Buffett’s investment in American Express showcases his playbook: buy durable, high-quality businesses with strong brands, loyal customers, and wide moats — and hold them forever.

Purchase Details Major Purchase: 1994

Total Investment: $1.29 billion

Shares Acquired: 151.6 million

Average Cost Basis: Around $8.50 per share (adjusted for splits and dividends)

Note: The 1994 stake is the core of Berkshire’s current holding.

Since Purchase American Express has not split its stock since the 1994 purchase. This makes the math simpler compared to Coca-Cola.

Dividend Details in 1994 Dividend per share (1994): ~$0.44 annually

Initial yield: Based on a cost of $8.50, Buffett’s dividend yield was about 5.2%

Dividend on Cost Today (2025) 2024 Dividend per Share: $2.40 annually

On his original cost basis of $8.50, Buffett now earns a 28.2% dividend yield on cost.

That means every 3.5 years, Buffett earns back his entire investment in dividends alone.

Total Return Since 1994 Capital Appreciation Current Share Price (May 2025): ~$230

Capital Gain Multiple: $230 ÷ $8.50 = ~27x

Dividends Collected Cumulative dividends per share since 1994: Estimated at $32–$35 per share

On 151.6 million shares: Over $5 billion in cumulative dividends received by Berkshire.

Total Value Today Market value of shares: ~$230 × 151.6 million = ~$34.9 billion

Total gain (including dividends): ~$40 billion

Original investment: $1.29 billion

Total return: ~3,000% or 30x

Buffett Bought American Express Because of its Powerful Brand & Loyal Customer Base AmEx was and remains a premium financial services brand. Buffett liked its prestige, customer loyalty, and differentiated model.

Every time someone swipes an AmEx card, the company earns a cut of the transaction — a perfect Buffett-style “toll booth” investment.

Strong Returns on Capital AmEx consistently generated high ROE (Return on Equity) without needing large amounts of physical capital.

Pricing Power and Moat Its moat came from brand, customer relationships, partnerships with airlines and hotels, and unique data on spending habits.

Management Trust Buffett valued the consistent leadership and culture of financial conservatism.

Buffett’s Own Words In his 2008 shareholder letter, Buffett wrote:

“We can afford to look foolish as long as we don’t feel foolish. And with American Express, we feel very smart.”

Takeaway for Traders: Buffett didn’t buy American Express because it was “hot” or had a new tech breakthrough. He bought it because it was predictable, powerful, and profitable — and he was willing to sit still while the cash rolled in. That’s what quality investing looks like.

Apple Computer ($AAPL)

Warren Buffett’s investment in Apple is more than a case study in late-cycle brilliance — it’s a moment that redefined how we think about value in the modern era. For decades, Buffett avoided technology stocks, famously saying he didn’t understand the pace of innovation well enough to make a reliable long-term bet. He sat out the meteoric rise of Microsoft, the network effect of Google, and the disruption of Amazon. But in 2016, Buffett broke his own precedent — and in doing so, engineered one of the greatest trades of his career.

It began quietly. In the first quarter of 2016, Berkshire Hathaway started buying Apple shares. Initially, the purchases were made by Buffett’s portfolio managers, Todd Combs and Ted Weschler. But as the numbers — and the business case — came into sharper focus, Buffett stepped in and made Apple his own. Over the next two years, Berkshire amassed a $36 billion position in what Buffett would later call “probably the best business I know in the world.” That $36 billion stake, purchased at an average cost of roughly $36 a share (split-adjusted), would eventually swell to more than $150 billion in value, not including dividends. At its height, Apple made up nearly half of Berkshire’s entire equity portfolio.

Critics argued Buffett was late to the tech party. And technically, they were right. But what they missed was the nuance: Buffett didn’t buy Apple because it was a hot technology stock. He bought it because it had become a consumer product juggernaut, wrapped in an ecosystem of brand loyalty, repeat sales, and customer lock-in. The iPhone wasn’t just a gadget — it was a gateway into a recurring revenue model, where users paid not just once but year after year, without even thinking about it. Buffett recognized that Apple’s blend of pricing power, simplicity, and capital discipline made it behave more like a branded consumer goods company than a traditional tech firm.

Tim Cook’s leadership played a key role in Buffett’s comfort. While Steve Jobs was the iconoclast, Cook was the executor — the operator who turned Apple into a capital-return machine. Under his stewardship, Apple embarked on an aggressive buyback program and initiated a dividend policy that gave Berkshire exactly what it loves most: rising ownership without having to lift a finger. Buffett wasn’t chasing innovation. He was buying predictability, scale, and trust — on terms he could understand.

In the end, what looked like a late arrival turned out to be one of Buffett’s most iconic moves. It wasn’t flashy, but it was profound. And it underscored something essential about his philosophy: the discipline to wait, the conviction to act, and the wisdom to know when something complex has become simple enough to trust. That’s not a contradiction. That’s Warren Buffett at his best.

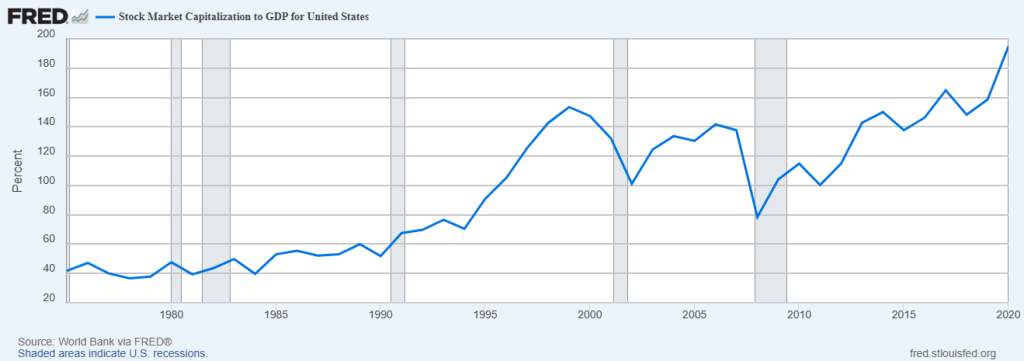

Warren Buffett has never been just a stock picker. He is, in many ways, one of the great system thinkers of modern finance — a man who didn’t just play the game but helped define its rules. Among his lesser-sung but no less important contributions is what’s now called the “Buffett Indicator”: a simple but potent ratio that compares the total market capitalization of U.S. stocks to the country’s gross domestic product. In Buffett’s view, when the value of the stock market far exceeds the size of the real economy, it’s a red flag — a signal that euphoria may be outrunning fundamentals. For years, the indicator has flashed red, and for years, critics argued that Buffett was stuck in a bygone era of valuation discipline.

The Buffett Indicator charted by The St. Louis Federal Reserve

Six months ago, as markets floated higher on the back of artificial intelligence mania and the promise of a soft landing, Buffett did what he’s always done when the math stopped working — he moved to the sidelines. In an environment saturated with liquidity and optimism, he quietly built a $153 billion position in U.S. Treasury bills — short-term government debt that pays little but protects principal. Predictably, the move was panned. Pundits accused him of being out of touch. Talking heads on financial news networks openly questioned whether the Oracle had lost his edge. But then came the drawdown — sharply rising volatility, earnings misses, and renewed fears around sticky inflation and debt refinancing. And just like that, Buffett looked prescient again.

The lesson is familiar, but it bears repeating: Buffett is not in the business of prediction — he’s in the business of preparation. He doesn’t try to time the exact top or bottom. He watches the relationship between prices and intrinsic value with a discipline few can match. When things get stretched, he doesn’t hedge — he waits. In an era of speed, Buffett’s greatest asset may be his willingness to be still. While others chase momentum, he studies balance sheets. While others debate rate cuts, he reads cash flows. And while others dismiss the Buffett Indicator as outdated, the man who made it famous quietly builds dry powder — just in time to use it when the panic begins.

Let me share with you a truth about investing and trading. In a market flooded with noise, speculation, and thousands of tickers vying for attention, the data tells a sobering story — almost none of them actually matter. Strip away the marketing, the memes, and the momentum trades, and what you’re left with is this: just 15% of all U.S. public companies manage to outperform the S&P 500. Fewer still — only 12% — offer the kind of real liquidity that institutional investors need to move in and out without distorting the price.

Dig a little deeper and the picture gets narrower. Just 8% of all listed companies even have an Options market. For traders looking to hedge, speculate, or build sophisticated strategies, that’s a striking limitation. But the most jarring statistic of all? Roughly 96% of all publicly traded U.S. companies underperform short-term U.S. Treasury bills. That’s right — risk-free government paper beats nearly everything. The brutal reality: nearly all of the stock market’s long-term wealth creation comes from just 4% of companies. That small elite — companies with enduring business models, competitive moats, and scale — are the real engines of equity returns. Everyone else is just noise.

Here’s the raw truth, no sugarcoating: Most of the market is junk. Not “kind of underwhelming.” Not “worth a look.” Junk. You’ve got thousands of tickers clogging your screen like cholesterol in an overworked heart — and 96% of them can’t even beat a T-bill. That’s the most boring, zero-risk asset on the planet. And yet? It’s outperforming nearly everything with a ticker symbol and a story to sell.

Here’s where the game changes — and why VantagePoint’s artificial intelligence isn’t just helpful in today’s market, it’s essential. A.I. doesn’t care about hype. It doesn’t get emotional, it doesn’t fall in love with a brand, and it doesn’t follow CNBC hot takes. A.I. scans the entire market, every sector, every timeframe — and it finds that elite 4%. The small handful of trends that actually matter, the ones that create wealth while the rest of the market eats dust.

You want to survive in this volatile, manipulated, headline-driven macro mess? You need a tool that doesn’t flinch. You need software that filters out the noise and identifies real strength, real quality, and real opportunity before the herd catches on. This is not about throwing darts. It’s about putting a sniper scope on the 4% that move the needle — and leaving the rest to the amateurs.

The next bull market isn’t going to be won by guts or guesses. It’s going to be won by precision. That’s what A.I. brings to the table. You’ve got the entire market at your fingertips — but only if you’re smart enough to know where to focus and what to ignore.

Let’s call out a majority of the market for what it is: currency debasement, dressed up in a cheap suit and paraded around as economic strategy. The dollar’s getting weaker — not by accident, but by design. And while the talking heads on TV call it “stimulus” or “policy,” you and I know what it really means: your money buys less, your savings shrink, and everything from eggs to auto insurance hits like a gut punch.

Now here’s the question that keeps grinding in your brain: If the government’s goal is to silently siphon value out of your wallet… where do you put your money?

That’s where Buffett’s thesis hits like a hammer. You don’t chase momentum. You don’t buy hype. You own quality — real, cash-flowing, dominant businesses with the pricing power to laugh in the face of inflation. Buffett didn’t build his empire by guessing interest rates or playing currency wars. He did it by identifying companies that could raise prices, protect margins, and keep compounding when the rest of the world was on fire. That’s how you escape the trap. That’s how you build wealth when everyone else is bleeding it.

So yeah, the dollar’s being drained. But that doesn’t mean you have to be. The game is rigged for those who don’t know what to look for. Buffett showed you the way. VantagePoint will help you down the path. The next move is yours.

Let’s be honest: in a world where the dollar gets weaker by design and inflation eats away at your buying power like termites in a rotten floorboard, the real question is this — do you have a way to find trades and investments that actually keep you ahead of the game?

Buffett built his fortune by sticking to one timeless principle: buy quality. Own assets that have pricing power, real earnings, and the ability to grow stronger even when the economy weakens. But finding those gems today — when markets are a daily warzone of noise, fake signals, and emotional landmines — isn’t easy. It’s not about being brave or bold. It’s about being precise. That’s where VantagePoint’s artificial intelligence trading software comes in. Not to replace your instincts, but to sharpen them. This isn’t guesswork or gut feeling — it’s data. Real-time, predictive, pattern-driven insights that strip out the noise and zero in on what works.

With VantagePoint’s A.I., you’re not throwing darts — you’re deploying strategy. It’s like having Buffett’s discipline and patience, turbocharged by 21st-century tech. A.I. doesn’t panic when the market dips. It doesn’t get greedy at the top. It watches, learns, and points you toward high-probability setups based on intermarket relationships and statistical probability — not hype. This is how smart traders separate themselves from the crowd.

If you’re ready to stop reacting and start making moves with clarity and confidence, it’s time to see what trading with A.I. really means. Learn how to spot quality trends like Buffett — and trade it with the speed and certainty of a machine.

This is your chance to learn from the experts, see A.I. in action, and understand how you can apply it to achieve consistent trading success.

Hit up the link, sign up for the A.I. trading masterclass, and jump into the future of A.I.-driven trading.

Let’s Be Careful Out There!

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.