The American retirement system has become a high-stakes game of roulette — and for millions, the ball is landing on zero.

Imagine saving for decades, doing everything right — contributing to your pension, trusting the system, and expecting a dignified retirement. But when the time comes, there’s not enough money. That, my friend, is a pension crisis. It’s what happens when governments, corporations, and even unions, promise retirement benefits… but fail to fully fund them.

Now here’s where it gets urgent — for you, the trader, the investor, the wealth builder. Because this isn’t some distant headline or abstract economic theory. This is a financial time bomb ticking underneath your portfolio.

A pension crisis unfolds when the inputs (contributions) are too small, the middle (investment returns) are mismanaged or mandated into low-yield government debt, and the outputs (retiree benefits) are too generous or politically untouchable. The result? Underfunded liabilities. Cities cut services. States raise taxes. Companies freeze pensions or dump them on the government’s lap.

And this ripples through the market. While attention often focuses on contribution levels and benefit payouts, the most significant and overlooked problem is how the pension funds are managed — or mismanaged — once the money is in the system.

Traders need to understand: when pensions crumble, it forces huge institutional investors — pension funds managing trillions — to chase yield in riskier assets. That’s part of the reason we’ve seen wild volatility, inflated asset bubbles, and crushing market corrections. It distorts natural price discovery. It warps interest rates. And worst of all — it can obliterate the very assets you’re counting on to fund your own retirement.

So yes, the pension crisis matters. Not just for retirees. But for anyone trying to build wealth in a system that’s quietly breaking beneath their feet.

If you want your portfolio to outlive you, you must understand the battlefield. Because in this war between promises and reality — the informed investor wins.

In the late 20th century, a subtle but powerful narrative began to take hold across corporate America — one that would fundamentally reshape the retirement landscape and, in turn, the financial security of millions. Investment bankers, consultants, and financial engineers sold executives a simple proposition: shed your pension obligations, and your stock price will rise. It was a compelling pitch, especially in an era when shareholder primacy had become dogma. Defined benefit pensions were seen not as a promise to workers, but as a liability dragging down earnings-per-share.

Wall Street’s financial elite framed the decision in terms CEOs understood — pensions were “balance sheet baggage.” Replace them with defined contribution plans like the 401(k), and not only do you remove long-term obligations, but you also get a short-term boost in valuation. The market applauded. Analysts rewarded the cuts. And within a generation, the responsibility for retirement was no longer a shared burden — it had become entirely individual.

As corporate America moved en masse away from traditional pensions, Wall Street didn’t just support the shift — it monetized it. A vast ecosystem of market-based retirement products took over: 401(k)s, IRAs, mutual funds, target-date funds, and annuities. On paper, these vehicles gave individuals “choice” and “control.” In reality, they tethered the future of millions of Americans to the unpredictable whims of global markets.

What wasn’t advertised was the machinery underneath. Hidden fees quietly eroded returns. Layer upon layer of fund-of-fund structures and active management took a cut before savers saw a dime. Complexity became a feature, not a bug. For the average worker, trying to decipher their retirement plan’s prospectus was like reading a foreign language. The more confusing it became, the more profitable it was for the institutions behind it.

And then came the inevitable: crashes. In 2008, millions watched their life savings vaporize as markets plunged. Again in 2020, the pandemic sent portfolios into freefall. Boom-and-bust cycles weren’t a bug in the system — they were the system. Market timing, volatility, and speculation became central variables in determining whether someone could retire or not. Risk wasn’t managed — it was outsourced to the public.

Meanwhile, the financial industry fought tooth and nail against reforms. Efforts to implement a fiduciary rule — requiring retirement advisors to act in their clients’ best interest — were met with aggressive lobbying. Billions were spent to ensure that financial professionals could continue to profit without accountability. In other words, while Americans took on all the risk, Wall Street made sure it kept all the reward.

It wasn’t just a shift in structure — it was a shift in philosophy. Retirement was no longer a guaranteed outcome. It became a wager — one with high stakes, rigged odds, and no bailout for the losers.

Let’s talk about Washington’s role in this mess — and folks, it’s a disgrace. The retirement crisis didn’t just happen, it was built, brick by brick, by decades of deregulation, inaction, and outright misdirection. Our elected officials, Republican and Democrat alike, have stood by as the foundation of retirement security crumbled beneath working Americans. They had plenty of opportunities to act — and instead, they punted.

Take Social Security. It’s the bedrock of retirement for millions of Americans, yet Congress has refused to modernize its funding structure. The trust fund is set to run dry in less than a decade, and all they’ve done is kick the can down the road, scared stiff of political blowback. Meanwhile, inflation eats away at fixed incomes and COLA adjustments barely keep pace with reality. The silence from Capitol Hill is deafening.

Oversight? Forget about it. Retirement advisors and plan managers operate in a murky world where conflicts of interest are too common and accountability is too rare. Washington had a shot at real reform with the fiduciary rule — to make sure advisors act in your best interest — but Wall Street lobbyists swooped in and gutted it. So now, retirees are left navigating a rigged system where bad advice can cost them their future.

And then there’s the tax code — a rigged game that rewards the wealthy and punishes the middle class. Retirement contributions are capped. Income thresholds for deductions are skewed. And the real estate tycoons and hedge fund managers? They ride off into the sunset with loopholes the average worker can’t even spell. Even recent attempts at reform, like the SECURE Act, offered more bark than bite. They helped but they didn’t fix the core problem: a broken system that rewards capital over labor.

Now here’s the real kicker: perpetual currency debasement — Washington’s favorite silent tax — hits pensions like a wrecking ball. As the Fed prints trillions to fund endless deficits, the value of each dollar drops. For public pensions, which are often tied to fixed return assumptions, that means real purchasing power evaporates. And private sector pensions? The assets they hold become less valuable relative to future obligations. In short, inflation steals from savers and retirees to patch over government mismanagement. It’s theft by another name, and the people paying the price are the ones who played by the rules.

Washington didn’t just fail retirees. They sold them out. And unless we force a course correction, the next chapter in this story won’t be a correction, it’ll be a collapse.

We’ve allowed retirement security to be reshaped by forces that prioritize short-term profit over long-term stability, gambling with the futures of everyday workers who played by the rules. The old guarantees are gone. In their place, we’ve constructed a fragile apparatus of market dependency, individual risk, and political inertia — and called it a plan.

But roulette tables are not built for the player to win. They’re built for the house.

If we continue this path — ignoring underfunded pensions, deferring Social Security reform, and tolerating a system that demands 8% returns from 4.5% instruments — the consequences won’t just be personal. They’ll be national. We are staring down the barrel of a slow-moving economic and social catastrophe. Many alternative investments are not regularly marked to market, allowing pension funds to carry inflated asset values and delay the recognition of losses — creating a dangerous illusion of solvency.

It’s time for policymakers to step away from the political theater and act with urgency and clarity. The choices we make now will determine whether the next generation retires with dignity or despair.

Here’s the fact that should keep us all up at night: According to Vanguard, the median 401(k) balance for Americans aged 65 and older is just $87,725. That’s not a retirement plan — that’s a four-year buffer against poverty.

We’re not out of time yet. But the wheel is spinning — and the longer we wait, the harder it will be to beat the odds.

Here’s the ugly truth no one in polite financial circles wants to say out loud: the core problem facing pensions is the same one stalking every investor and trader in America today — saving money in an age of currency debasement is a sucker’s game. It’s like trying to fill a leaky bucket in a downpour. You can save every day, skip the lattes, budget like a monk — and still fall behind.

Why? Because the dollars you’re saving are rotting while you sleep. That’s what happens when the government treats the money supply like an endless buffet. They print, borrow, and spend with zero accountability — and your purchasing power? It shrinks like cotton in a hot wash. This isn’t theory, it’s math. Real-world inflation plus currency debasement equals one thing: your savings lose value — fast.

Now, people who do save, who do show discipline, are punished for it? Safe investments? CDs, savings accounts, treasury bonds? They don’t even come close to keeping pace with the real inflation rate. So, what’s left? Risk. Volatile markets. Stocks that swing like a drunken prize fighter. Bitcoin and Crypto. Real estate bubbles. It’s all a forced march into uncertainty, just to break even.

And pensions? They’re in the same twisted game. They’ve got to hit 7-8% annual returns just to survive. But how the hell do you hit those numbers when treasuries — the so-called “safe” investments they’re mandated to buy — are barely yielding 4.5%? They’re trapped. If they play it safe, they die slowly. If they chase risk, one bad year can wipe them out.

Let’s not sugarcoat this. The system is broken by design. The rules have been rigged so now you must gamble just to stand still. It’s not about personal responsibility or prudent planning anymore. It’s about surviving a financial system that punishes savers, rewards debtors, and grinds the disciplined into dust. Until we fix the money, we can’t fix retirement. Period.

Let’s be clear: the pension crisis we’re witnessing today isn’t the result of a single misstep. It’s a slow-moving, multifaceted disaster decades in the making — a perfect storm of underfunded contributions, questionable asset management, and a political system more inclined to kick the can down the road than confront hard fiscal truths. And yes, there’s enough blame to go around — from Washington policymakers and Wall Street product pushers to pension boards making multibillion-dollar decisions with the sophistication of a high school bake sale.

At its core, the solvency of a pension plan hinges on three deceptively simple elements: how much money goes in, how well it’s managed while it’s there, and how much goes out. But the devil — and the crisis — is in the details. For decades, much of the public debate has centered around contribution rates and benefit obligations. Are governments and corporations putting enough into these funds? Are retirees asking for too much on the back end?

But remarkably little attention is paid to the middle act — the actual management of these assets. And here’s where things go off the rails.

Source: Amazon.com

If you’ve read Who Stole My Pension?, co-authored by Edward “Ted” Siedle and Robert Kiyosaki, the thesis is painfully straightforward: losing 1% to 2% annually in fees and underperformance might not sound catastrophic — until you extend that over 30 years. Compound it, and suddenly you’re looking at a fund that winds up with half the money it should have.

That’s not misfortune. That’s mismanagement on a generational scale.

Part of the problem is structural. Pension boards — often populated by well-intentioned but financially inexperienced public servants like firefighters, teachers, or city officials — are tasked with allocating hundreds of millions, sometimes billions, of dollars. These folks are heroes in their professions, but they aren’t trained to navigate complex derivatives, illiquid private equity structures, or opaque hedge fund vehicles.

And Wall Street knows it.

To the banks and asset managers, pensions represent “dumb money” — slow-moving, captive capital pools that can be quietly steered into fee-heavy, complexity-laden investment vehicles. What begins as a pursuit of higher returns in a low-rate world often ends in an alphabet soup of alternative assets: stadium funding deals, venture capital funds with no transparency, and crypto plays dressed up as sophisticated arbitrage strategies.

What’s more, there’s a regulatory irony at play. Many public pension plans are required to own long-dated Treasury instruments for “safety,” but in today’s rate environment, those instruments often yield less than the actuarial return targets — typically 7% to 8% — that pension funds must hit to stay solvent. That delta — the difference between what pensions need and what these “safe” assets produce — drives the reach for yield and opens the door to Wall Street’s fee machines.

In other words, Washington mandates safety. Wall Street profits from risk. And pensioners are left to spin the wheel.

The real tragedy? No one notices until the checks stop coming.

At the heart of the problem is this brutal truth: the U.S. retirement system has quietly shifted all the risk from employers and the government to everyday workers — without giving them the tools to succeed. For decades, Americans could count on a trifecta: a steady pension from work, reliable Social Security, and a bit of personal savings. Today? That three-legged stool is down to one wobbly leg: the 401(k) — a glorified savings account tied to the chaos of Wall Street, where most people don’t have the financial training, income stability, or investment confidence to navigate.

Here’s the gut punch: the average 401(k) balance for people near retirement age is around $100,000. That might sound decent until you do the math. Spread over 20-30 years of retirement, it barely covers the basics — especially when you factor in inflation, medical costs, and long-term care. And that’s if you’re lucky enough to have a 401(k) at all. Millions of Americans don’t.

This isn’t a failure of individual discipline. It’s a failure of design. We’ve built a retirement system that depends on flawless execution by millions of people juggling debt, stagnant wages, volatile markets, and rising costs — and then we blame them when it collapses. That’s not a system. That’s a setup.

What happened? Corporate America found a way to dump responsibility, shifting from defined benefit pensions to defined contribution plans like the 401(k). Sounds harmless, right? But make no mistake, this was a calculated move to transfer risk from the boardroom to the break room. No longer would companies have to guarantee retirement income. Now, employees were on their own, tossed into the shark-infested waters of the stock market.

And let’s be clear: this wasn’t done to empower workers. It was about cutting costs and boosting quarterly earnings. Companies slashed pension liabilities from their balance sheets and replaced them with a “do-it-yourself” retirement model that looks good on paper but fails millions in reality.

The result? Workers now bear the full burden of market volatility, interest rate swings, and even how long they’ll live. That’s right — if you live too long, that’s your problem. If the market crashes the year you retire? Also your problem. It’s a high-stakes game, and most Americans were never given the rulebook.

So, while Wall Street lines its pockets managing these accounts and Washington sits on its hands, the American worker is left holding the bag. We went from retirement security to retirement roulette — fast. And unless we fix it, the next generation is heading for a crisis of historic proportions.

Here’s something nobody at your local country club or retirement seminar is gonna say out loud — most pension programs are run by well-meaning bureaucrats who couldn’t spot a toxic asset if it bit ‘em on the butt. These are folks with master’s degrees in public administration, not finance. They’re managing billions with spreadsheets, consultants, and a whole lotta blind faith. And Wall Street? They smell that naivety like blood in the water.

What happens? Whenever the boys on Wall Street have a stinking, radioactive deal they can’t unload on anyone with half a brain… they call the pension funds. Junk bonds, overleveraged real estate projects, shady structured products that even the people who built them don’t fully understand — it all gets quietly shoveled into the pension portfolio. Believe it or not, pension funds today are looking at investing in Crypto assets to fund long term retirements. I am a huge believer in Bitcoin, and some Crypto, but for the uneducated, Crypto as a market is far too volatile and risky for pensions. But if you dress it up with a PowerPoint, slap a fake AAA rating on it, and boom — problem solved.

Why pensions? Because it’s the perfect dumping ground. There’s no immediate blowback. No angry shareholders. No public outrage. These funds are playing the long game — so nobody notices when that toxic trash starts festering. They bury the time bomb deep in a vault and hope nobody opens the box until long after they’ve retired on their fat government pensions and speaking fees.

And the real punchline? The victims won’t find out for 30 years. By then, the damage is done. The retirees who trusted the system wake up one day and find that the “secure future” they were promised is a steaming pile of broken promises and IOUs. But the suits who made the deals? They’re long gone — richer, unaccountable, and already onto the next scam.

This isn’t an accident. It’s a business model. And even when someone brave enough does blow the whistle — lays out the fraud, exposes the cooked books, proves the fees are highway robbery — nothing happens. Nada. Zip. The SEC shrugs. The DOJ hits snooze. State AGs look the other way while cashing campaign checks from the same suits looting the pension vaults. It’s a rigged game. Accountability? Doesn’t exist. The message is loud and clear: go ahead, fleece the system — just don’t get caught being too obvious. And if you do? No worries. No one’s coming for you.

The suits in D.C. and the financial wizards on Wall Street want you to believe that if you just “max out your 401(k)” and “invest for the long run,” you’ll be golden. Bull. The game changed decades ago, and no one told the players. Pensions are a dying breed, Social Security is limping toward insolvency, and the so-called safety net? It’s made of fishing line and wishful thinking.

What we’re dealing with isn’t just a savings problem — it’s a systemic failure of leadership, policy, and trust. Washington sold you a dream and Wall Street sold you a product. And when it all collapses, guess who’s left holding the bag? That’s right. The average worker who did everything they were told, only to find out the finish line was moved while they weren’t looking.

These public pension funds are filled with taxpayer dollars — your money — and yet when you ask where it’s invested, how it’s performing, or what it’s costing, you get stonewalled. Why? Because some Wall Street lawyer stuffed a “trade secret” clause into the fine print. That’s right — the people managing billions in public funds hide behind the same legal tactics Coca-Cola uses to protect its recipe. Except this recipe is a cocktail of risk, leverage, and high-octane fees — shaken, not disclosed.

We’re talking about a perfect storm: the death of guaranteed pensions, wages that haven’t kept up with inflation, a cost of living that’s skyrocketed, and a stock market retirement model that depends on timing, luck, and blind faith. And somehow, if it doesn’t work out, it’s your fault for not budgeting better? Give me a break.

Here’s the deal. This isn’t just about dollars and cents. It’s about dignity. It’s about whether the people who built this country get to retire in peace or end up bagging groceries at 78. And if we keep spinning this roulette wheel, we already know how it ends — with the house winning and the retirees broke. Let’s stop pretending the system’s fine. It’s not. It’s rigged — and it’s time we called it what it is.

Inflation isn’t just some temporary “transitory” annoyance like the talking heads keep claiming — it’s a wrecking ball. And it’s smashing through everything we thought was stable, starting with your retirement. The dollar’s getting weaker by the day, not because of some invisible hand of the market, but because the geniuses in Washington keep printing it like it’s Monopoly money. That’s currency debasement, folks — and it’s the silent killer of financial planning.

Here’s the setup: pension funds across the country are in a full-blown panic. You know what they’re legally allowed to invest in? Treasury instruments. And guess what those are yielding? Around 4.5% on a good day. That’s like trying to fill a leaking bucket with an eyedropper. These funds are bleeding, and the gap is only getting wider. So, what do they do? Stretch for yield, gamble with riskier assets, and pray the market doesn’t collapse again — because if it does, the whole system implodes.

And while Wall Street plays roulette with your retirement and Washington keeps firing up the printing press, they’ve sold you a nice little fairy tale called “personal responsibility.”

You’ve heard the pitch: just save more, invest smart, and everything will work out. That myth is the financial version of a con job. It’s like telling someone to win a drag race in a beat-up station wagon with no gas in the tank. Wages haven’t kept up with inflation in decades. Healthcare costs are through the roof. And every time you think you’re getting ahead, another economic shock knocks you flat.

But that’s not even the worst part. They’ve turned retirement into a DIY project. Behavioral finance tells us that most people aren’t wired to manage long-term investments — not because they’re dumb, but because they’re human. Emotions, fear, greed, confusion — the market feeds on all of it. Yet somehow, you’re supposed to navigate this chaos, read charts, manage risk, and plan 30 years out while juggling a mortgage and raising a family?

And don’t get me started on retirement calculators — those shiny little tools that spit out how much you “should” save each month to retire in comfort. They might as well come with a laugh track. They don’t account for recessions, layoffs, medical emergencies, or real-life curveballs. They sell an illusion of control in a system that’s anything but.

Here’s the truth they won’t say on CNBC: you didn’t fail the system — the system failed you. And until we stop blaming workers for structural sabotage, we’re going to keep watching Americans retire broke, exhausted, and betrayed.

The pension crisis in the United States is not a distant threat — it is a multi-trillion-dollar liability hiding in plain sight, and the numbers are staggering.

According to Pew and other nonpartisan analysts, state and local pension systems are underfunded by an estimated $1.5 to $4 trillion, depending on the assumptions you use for future returns. These aren’t abstract figures. These are legally binding promises — contractual obligations — made to millions of teachers, firefighters, police officers, and public workers across all 50 states.

What makes this particularly urgent is that these shortfalls are not theoretical or negotiable. They are real debts owed to real people who have upheld their end of the bargain. And as investment returns continue to fall short of optimistic targets, and inflation eats away at the real value of assets, the gap only widens. State budgets — already strained — cannot absorb these costs without massive tax increases, severe cuts to services, or, more likely, help from the only entity large enough to step in: the federal government.

And that’s where the problem intensifies for everyone — not just public employees. Because when the shortfall becomes unbearable — and it will — the bailout will come from the one institution with an unlimited checkbook: the Federal Reserve. But that money doesn’t come free. It comes from the printing press, in the form of new dollars entering the system.

This is crucial to understand. Bailing out pensions with newly printed money will further dilute the purchasing power of every dollar in your pocket. It is, in effect, a hidden tax — paid not through legislation, but through inflation. And as monetary debasement accelerates, volatility across the financial markets intensifies. Bonds become harder to price. Equities whipsaw. Capital flows into harder assets. Market confidence erodes.

So, yes, the pension crisis is about public workers. But more than that, it’s about the fragility of the broader financial system — and what happens when trillions in unfunded promises collide with a fiscal and monetary regime already stretched to the brink. Ignoring it won’t make it go away. But confronting it may be the only way to prevent the next great financial rupture.

Chasing yield is one of the most dangerous spots you can be in financially. It’s not investing. It’s desperation dressed up in a necktie. Imagine a day trader with maxed-out credit cards, no cash, and rent due in three days. He doesn’t have the luxury of patience or risk management — he’s gotta make money today, or he’s toast. That’s exactly what chasing yield feels like. It turns long-term investors into gamblers, turns risk into necessity, and turns markets into minefields.

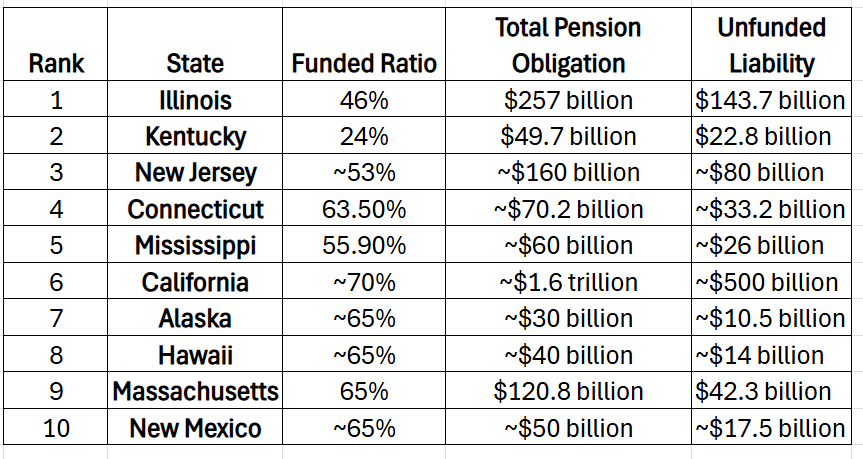

Now, picture this: you’re a pension manager in Kentucky. You’ve got 24 cents for every dollar you owe retirees. That’s not underfunded — that’s flat-out broke. And yet, those retirees expect to get paid. So, what do you do? You roll the dice. You chase yield. You dive headfirst into the stock market — not because it’s smart, not because it’s safe — but because you don’t have a choice. You start piling into high-growth tech, hoping the next six years will deliver 20% annual returns just to break even.

And let’s be honest — I believe that’s exactly what’s already happened. FANG stocks didn’t go parabolic on retail investors alone. Institutions — including pension funds — got squeezed into the trade. They needed growth, and big tech was the only place offering even the illusion of it. The result? Massive inflows, inflated valuations, and a stock market so top-heavy it’s starting to look like a Jenga tower at happy hour.

Let me be crystal clear: I’m not saying this is a strategy anyone should follow. I’m saying it’s already in motion. The Kentucky pension fund is just one canary in a very big, very shaky coal mine. And if we keep chasing yield in a market built on hopium and stimulus fumes, it’s not just pensions that will crash — it’s confidence in the entire system. Chasing yield is a ticking time bomb. And when hope becomes the plan, it’s time to rewrite the playbook.

On the flip side…

Imagine having a trading partner that never sleeps, never forgets, and learns from every mistake — not just its own, but everyone else’s too. That’s the power of VantagePoint’s artificial intelligence. While the average investor is scanning headlines or reacting emotionally to market moves, A.I. is running a systematic, unbiased process — sifting through mountains of intermarket data, identifying patterns, and making probability-based forecasts grounded in real market relationships. It doesn’t guess. It knows what’s worked, what hasn’t, and what the next high-probability move looks like. That’s not speculation — that’s strategy.

The real edge? Mistake prevention. Great traders aren’t just good at making money — they’re elite at avoiding losses. A.I. applies this principle 24/7, constantly adapting to changing market conditions, flagging landmines in advance, and course-correcting in real time. No human can do that — not with the consistency and speed required in today’s volatile markets. That’s why traders using VantagePoint Artificial Intelligence software consistently find themselves on the right side of the right trend at the right time. It’s not about being perfect. It’s about being positioned.

Artificial intelligence works because of one key principle: the feedback loop. It learns what doesn’t work, remembers it, and evolves — every day, every tick, every trade. That loop, refined and repeated, is the very foundation of every fortune made in the markets. It’s the difference between reacting and anticipating. Between missing a move and riding the wave. When you combine this relentless process with the right data, the right timing, and the right tools, what you get is something rare in trading — an unfair advantage.

This is the winning combination. Less risk, more reward, and clarity when others are confused. That should get you excited — because it is a game-changer. Intrigued?

Visit with us and check out the A.I. at our Next Live Training.

Discover why artificial intelligence isn’t just the future — it’s the secret weapon professional traders rely on today.

It’s not magic. It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.