Trend Forecasting with Technical Analysis:

Unleashing the Hidden Power of Intermarket Analysis to Beat the Market (Excerpt from Chapter 4)

(Marketplace Books, 2000)

Written by: Louis B. Mendelsohn

Foreword by John Murphy

Moving Averages are Lagging Indicators

However, traditional moving averages have one very serious deficiency. They are a ‘lagging’ technical indicator. This means that moving averages, due to their mathematical construction (averaging prices over a number of prior periods) tend to lag behind the current market price. In fast moving markets, where the price is on the verge of rising or falling precipitously, this lag effect becomes very pronounced.

The shorter the length of a moving average, the more sensitive it will be to short-term price fluctuations. The longer the length of a moving average, the less sensitive it will be to abrupt price fluctuations. Therefore, short moving averages lag the market less than long moving averages, but are less effective than long moving averages at smoothing or filtering out the noise.

Trades based upon moving averages are often late to get into and out of the market compared to the point at which the market’s price actually makes a top or bottom and begins to move in the opposite direction.

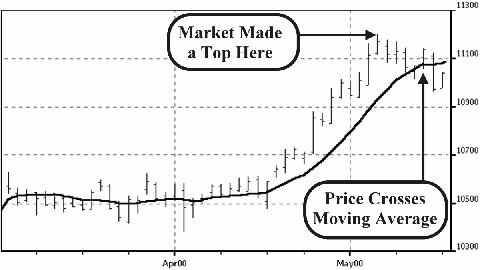

Figure 4-2 depicts a chart of daily prices of the U.S. Dollar Index compared to its 10-day simple moving average. Because of the steep price increase prior to the market making a top, the moving average actually continues to increase in value, even as the market begins to drop before cutting the moving average from above to below.

Depending on the price movement and the type and size of moving average used, this “response” delay can be financially devastating under extreme circumstances, such as waking up one morning and finding yourself on the wrong side of an abrupt trend reversal involving a lock-limit futures position.

The lag effect, which to date has been the Achilles’ heel of moving averages, has presented a challenge to technical analysts and traders for decades. Extensive research has been directed at finding ways to reduce the lag, while at the same time retaining the benefits of moving averages.

U.S. Dollar Index With its 10-day Simple Moving Average

To accomplish these two goals, numerous variations of moving averages have been devised. Each has its own mathematical construction, effectiveness at identifying the underlying trend of a market and ability to overcome the lag effect. The three most common types of moving averages relied upon by technical analysts and traders for decades are the simple, weighted and exponential moving averages.

A New Way to Forecast Moving Averages

The fact that despite their limitations moving averages continue to be widely used by traders is testimony that moving averages are recognized in the financial industry as an important quantitative trend identification tool. Yet, at the same time, the inherent lagging nature of moving averages continues to be a very serious shortcoming that has dogged technical analysts and traders for decades.

If this deficiency were somehow overcome, moving averages could rank as the most effective trend identification and forecasting technical indicator in financial market analysis.

Since traditional moving averages are computed using only past price data—the price for today, for yesterday, and so on—turning points in the moving averages will always lag behind turning points in the market.

For instance, to compute a 5-day simple moving average as of today’s close, today’s close plus the previous four days’ closes are used in the computation, as depicted previously in Figure 4-4 (see page 65). These prices are already known since they have all already occurred. The problem with this computation, from a practical trading standpoint, is that the moving average lags behind what is about to happen in the market tomorrow.

For a trader trying to anticipate what the market direction will be tomorrow, and determine entry and exit points for tomorrow’s trading, any lag, however small, may be financially ruinous in today’s highly volatile markets.

By comparison, a predicted 5-day simple moving average for two days in the future, based upon the most recent three days’ closing prices up through and including today’s close (which are known values), plus the next two days’ closing prices (which have not yet occurred) would have, by definition, no lag, if the exact closing prices for the next two trading days were known in advance.

Unfortunately, there is no such thing as 100% accuracy when it comes to forecasting market direction or prices for even one or two days in advance. No one will ever be able to predict the financial markets perfectly—not now, not in a hundred years. Through financial forecasting, though, mathematical expectations of the future can be formulated.

Needless to say, it is very challenging to predict the market direction of any financial market. The further out the time horizon, the less reliable the forecast. That’s why I have limited VantagePoint’s forecasts to four trading days, which is more than enough lead time to gain a tremendous trading advantage.

Trying to predict crude oil or the S&P 500 Index a month, six months or a year from now is impractical from a trading standpoint. This is due in part to the fact that market dynamics entail both randomness and unforeseen events that are, by definition, unpredictable. Plus, let’s face it, forecasting is not an exact science; there’s a lot of “art” involved.

I have successfully applied neural networks to intermarket data in order to forecast moving averages, turning them into a leading indicator that pinpoints expected changes in market trend direction with nearly 80% accuracy. This is in sharp contrast to using moving averages as a lagging indicator, as most traders still do, to determine where the trend has been.

If you are driving down an interstate highway at seventy miles per hour, you wouldn’t only look backwards through your rear window or over your shoulder. You need to look forward, out the front window at the road ahead, so you can anticipate possible dangers in order to prevent an accident from happening. It is the same with trading.

An enormous competitive advantage is realized by being able to anticipate future price action, even by just a day or two, so you can guide your trading decisions based upon your expectation of what is about to happen.

VantagePoint uses price, volume and open interest data on each target futures market and selected related markets as inputs into its neural networks. In this manner, its moving average forecasts are not based solely upon single-market price inputs.

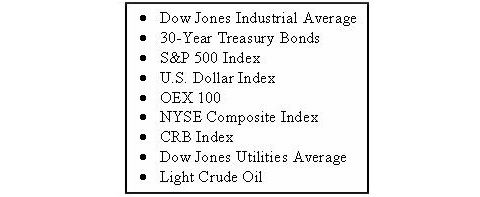

In the case of VantagePoint’s Nasdaq-100® program, for example, the raw inputs into the forecast of the moving averages include the daily open, high, low, close, volume and open interest for the Nasdaq-100 Index, plus nine related markets as shown in Figure 4-5.

Intermarket Data Used by VantagePoint’s Nasdaq 100 Program

Similarly, each other VantagePoint program has its own specific related markets, which provide input intermarket input data into its neural networks. Leading Indicators Give You a Competitive Edge

Since identifying the trend direction of a market is so critical to successful trading of that market, trend forecasting offers a substantial competitive advantage over traditional market lagging, trend-following strategies.

I have found predicted moving averages are most effective for trend forecasting when they are incorporated into other indicators which help identify not only the anticipated direction of the trend but also its strength from a momentum standpoint. This has been implemented within VantagePoint by comparing predicted moving averages for certain time periods in the future with today’s actual moving averages of the same length.

For instance, VantagePoint compares a predicted 10-day moving average for four days in the future with today’s actual 10-day moving average as of today’s close. It also forecasts other moving averages and makes similar comparisons, including that of a predicted 5-day moving average for two days in the future with today’s actual 5-day moving average as of today’s close.

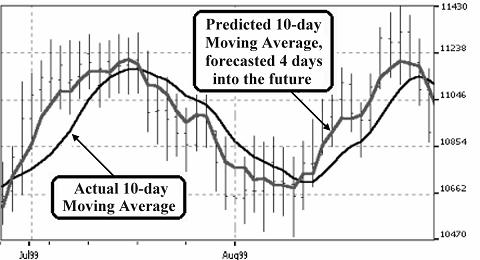

Dow Jones Industrial Average

Using A Predicted 10-day Moving Average Crossover Strategy

Figure 4-6 shows a crossover of the Predicted 10-day Moving Average and the Actual 10-day Moving Average for the Dow Jones Industrial Average. Notice that the Predicted Moving Average, because it is being forecasted for four days in advance does not lag behind the turns in the market, unlike the actual 10-day Moving Average.

This leading indicator within VantagePoint, involving the crossover of predicted moving averages with actual moving averages, which gives traders a forewarning that a change in market direction is imminent, will be discussed in more detail in the next chapter.