RIPPLE EFFECT LOOMS LARGE IN FX MARKETS

By Louis B. Mendelsohn

Today, it is imperative to include an intermarket perspective in FX analysis.

If they had not realized it before, this summer’s market turmoil that started in the United States and quickly spread elsewhere drove home an important message to foreign currency traders worldwide: The financial markets are globally intertwined and should not be considered in isolation from one another.

Now, even novice traders know that a development affecting one market or financial sector is likely to spill over and have repercussions in other markets because no market, particularly the forex market (which is at the center of global commerce), exists by itself today.

But a serious disconnect still prevails between the reality of how the markets interact and the technical analysis’s emphasis on looking internally at one market at a time. Technical analysis, in this regard, has failed to keep pace, for the most part, with the globalization of financial markets.

Changes that began in the 1980s with the proliferation of personal computers and global telecommunications—which accelerated in the 1990s with the growth of the Internet and gained momentum in this decade with the cross-border consolidation of financial exchanges worldwide—have hastened the interconnectedness of global financial markets. Now traders need to pay serious attention to what’s happening in other markets, even those seemingly unrelated to the markets they trade.

Still, too many individual traders, particularly newcomers just learning the ABCs of technical analysis and the mechanics of forex trading, rely solely on single-market technical analysis strategies that have been around, in one form or another, since the 1970s, which is when I first started in this industry. This narrow approach to technical analysis predates the emergence of market globalization. As a result, I believe a large percentage of these traders fail in their trading endeavors and end up losing their trading capital after a brief stint in the markets.

Admittedly, a trader still needs to analyze the past price behavior of each individual market that he or she trades. If for no other reason, doing so continues to be worthwhile to identify the double tops, broken trendlines or moving average crossovers that other traders are observing, because such single-market indicators are part of the mass psychology that helps drive price action. But that narrow focus does not go far enough any longer.

It became increasingly clear to me in the mid-1980s, as the global economy was beginning to take shape, that intermarket analysis would become essential to traders who wanted to get an early reading on price direction in a target market before it became apparent to the masses. Since then, I have advocated in articles, books and television interviews that traders incorporate intermarket analysis into their trading strategies. Now at this juncture, I think it is fair to say that it is imperative to include an intermarket perspective in a trader’s analysis, given the mature state of today’s globally interconnected markets.

A Golden Oldie

Intermarket analysis has a long history in the equity, agricultural commodity and currency markets. Equity traders for years have compared returns between small- and large caps, one market sector versus another, a sector against a broad market index, one stock against another, international versus domestic stocks, etc. Fund managers talk about diversification and asset allocation as they try to achieve superior portfolio performance. Whether they are speculating for profits or arbitraging to take advantage of temporary price discrepancies, intermarket analysis in this sense has been part of equity trading for a long time.

Likewise, commodity traders have practiced intermarket analysis for decades. Farmers have been involved in it, although they may not have thought of what they do in those terms. When farmers calculate what to plant in fields where they have several crop choices—between corn and soybeans, for example—they typically consider current or anticipated prices of each crop, the size of the yield they can expect from each and the cost of production in making their decisions. Farmers do not look at one market in isolation but know that what they decide for one crop will likely have a bearing on the price of the other, keeping the price ratio between the two crops somewhat in line on a historical basis.

Currency traders and bankers have also performed intermarket analysis while trading currency spreads (involving a long position in one currency and a short position in another) long before the term “forex pairs” became popular among individual traders.

The Domino Effect

The commodity markets, such as crude oil and gold, have a tremendous effect on other financial markets—including U.S. Treasury notes and bonds, which, in turn, have a powerful impact on the global equity markets. They subsequently affect the U.S. dollar and forex markets, which then further influence prices of commodities.

This domino effect, when set off by what might appear to be a seemingly isolated or relatively small triggering event at the onset, can ripple through global financial markets in a circular, cause-and-effect, dynamic process that seems to take on a life of its own. Underlying this process are inflationary expectations, changes and differentials in interest rates and credit risk in different countries, corporate earnings growth rates, stock prices, and forex fluctuations—not to mention hurricanes and terrorist attacks—to name just a few of the potential triggering mechanisms that can set this process in motion.

Today, one can hardly name a market that is not affected by related markets or does not influence others in turn. That’s because “hot money” on a global basis—in what seems like nanoseconds—can now migrate to those markets promising higher returns. This is especially true in the foreign exchange market where a participant is always trading one currency against another. This search for returns is evident in the establishing and unraveling of so-called carry trades in recent years, as sophisticated traders and hedge funds borrowed money in low-interest-rate countries, such as Japan, and invested these funds in instruments in countries with higher interest rates, including New Zealand and Australia.

This dynamic has already played itself out a number of times since the 1987 crash, including the 1997 Asian currency crisis, the 1998 Long Term Capital Management debacle and the crisis following the 2001 terrorist attack on the United States. Each occurrence underscored the far-reaching implications regarding the fragile stability of the global financial system, itself, amid the ever-present prospect of a worldwide financial meltdown.

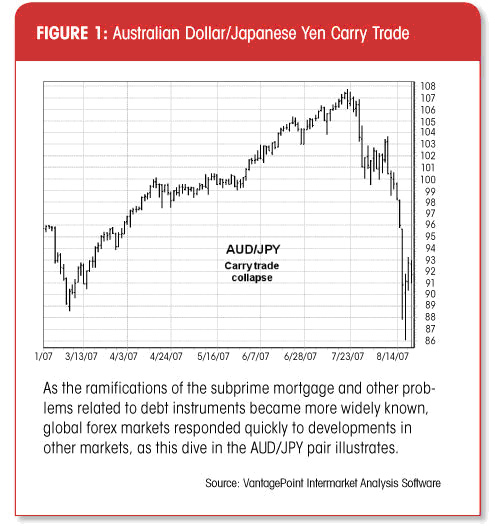

The most recent episode that began this past summer demonstrated how problems in the U.S. subprime credit markets spilled over into international hedge funds and banks, sending stock prices tumbling in July. Traders unwound their carry trades, buying the Japanese yen and selling the higher interest rate currencies to raise cash to provide liquidity for their funds. Once started, the move fed on itself, affecting numerous global markets including forex. Within a span of less than a month, the Japanese yen went from a “weak” currency to 14-year highs against the U.S. dollar, and the Austrailian dollar/yen pair plunged from above 107 yen to 86 yen (see Figure 1), illustrating the enormous trading opportunities in the forex market beyond pairs tied to the U.S. dollar.

The recent crisis in the U.S. credit markets and the subsequent fallout affecting highly leveraged funds illustrates again the extent to which the global financial markets are interconnected. Within hours, the reverberations from Bear Stearns and other hedge fund implosions tied to debt instruments had spread to banks and other financial institutions around the globe, prompting central banks in the United States, Japan, Europe and elsewhere to inject funds into their own economies to provide liquidity in the hope of preventing the financial contagion from spreading farther and becoming even more severe.

As is often the case, traders’ flight to quality in a financial crisis lifted U.S. Treasuries and the U.S. dollar, which again steered away (at least temporarily) from the edge of collapse as some pundits have been prognosticating for some time. Whether the Fed and other central bank actions alleviated the crisis this go-around or just put it off a while is still uncertain at this time.

The answer depends on whether any other “ticking time bombs” still lurk in the U.S. mortgage market or elsewhere. But the key point for FX traders from all of this is that they need to pay attention to what’s going on beyond the forex market and be on the lookout for a spark that could ignite elsewhere, and then flame reactions across the globe that inevitably affect the currency market.

Taking the Next Step

Recognizing that the financial markets are interdependent is necessary but by no means sufficient to be successful as a forex trader. To turn this awareness into trading profits, one has to be able to quantify these market interrelationships and then apply that information to actual trading situations in a way that improves performance. This challenge has been the focus of my research for the past 20 years, as I have sought ways to analyze how global markets influence each other, quantify their interconnectedness and develop predictive technical indicators and methods by which traders can apply this information.

For instance, if a trader wants to judge the value of the euro versus the U.S. dollar (EUR/USD), he or she not only has to look at euro data but also at numerous related markets to see how they influence the EUR/USD pair. This includes other currency pairs, as you might expect, but also U.S. Treasury notes and bonds, as well as other markets that, at first glance, may not seem to have much of an influence.

Often the correlation between other markets and the dollar is inverse, especially for markets such as gold or oil that are priced in U.S. dollars in international trade. When the value of the U.S. dollar declines, foreign currencies naturally rise by varying degrees, and prices for gold, oil and many other commodities usually do too.

As the value of the U.S. dollar weakened several years ago, the Organization of Petroleum Exporting Countries began pricing some of their crude oil exports in euros to make up for losses from the cheaper dollar. When the U.S. Dollar Index sagged again last summer to its 2004 lows, around 80, there was more talk from Russia about pricing its oil in euros, and several countries announced plans to shift some of their currency reserves from the dollar into other currencies. Traders in many markets, not just forex, need to keep an eye on whether the dollar can maintain its reserve currency status, as well as consider the implications if the dollar’s role diminishes in global financial markets.

In the future, another major challenge for FX traders will involve China’s response to U.S. pressure to revalue the Chinese yuan. Any movement will likely continue to be slow and calculated to preclude any severe disruptions to Chinese and world markets, but this is a development that currency traders and others need to monitor for the potential jolt it could have on numerous global financial markets, particularly forex. It’s unlikely that a trader will know when and how any adjustments might unfold, but intermarket analysis can provide some early clues for those markets he or she trades.

Analytical Challenge

As 2007’s market turmoil highlighted, many traders still ignore intermarket analysis altogether or fail to implement it in a meaningful way as part of their trading plans. At best, traders too often rely upon simplistic ways to compare markets. The complexity of the dynamics between markets, which I call market synergy, and how they influence each other suggests that just comparing price charts of two currencies and looking at the spread difference or a ratio between their prices (to measure the degree to which they move in relation to one another) is simply no longer adequate in today’s global trading environment.

This approach is too limited because it does not take into account the influence exerted by other currencies or other related markets. Additionally, such correlation studies fail to address the leads and lags that exist in the global economy as they affect market dynamics. In today’s global markets, particularly the forex market, traders must include in their analysis (to one degree or another) even seemingly distant markets.

Introducing Intermarket Data

Intermarket analysis provides a more comprehensive set of data points for analysis than simply looking at an individual market’s past prices. Through the use of an artificial intelligence tool known as neural networks, which I first started working with in the late 1980s, both single-market data from a target market, such as one of the forex pairs, and intermarket data from dozens of related markets are used as inputs into the neural networks. Once the networks have been properly designed, trained and tested, they can be used in real-time trading with current data updated each day to generate short-term forecasts for the target market.

Knowing that it would be futile to attempt to make accurate long-term forecasts (just like it is impossible to do with weather forecasts), the neural networks are designed to make predictions for just a day or two into the future. Of course, even for this short timeframe, it is folly to expect 100 percent accurate forecasts. That’s not only unrealistic, it’s downright impossible due to inherent randomness in the markets and unforeseen events that affect them.

No ‘Holy Grail’

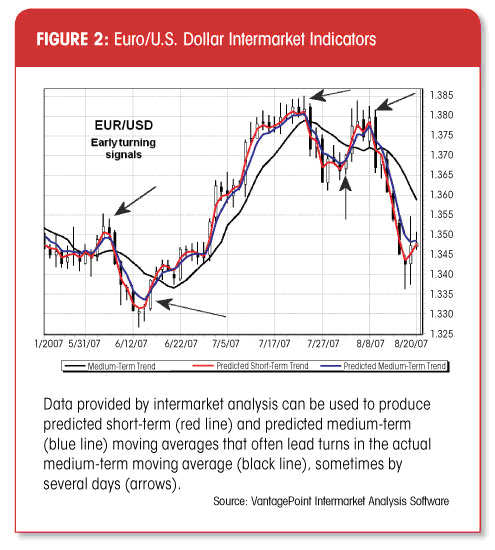

The good news is that all a trader really needs to tilt the odds in his or her favor are reasonably consistent and accurate short-term forecasts. With powerful analytical tools such as neural networks that use intermarket data from related forex and other global markets, popular technical indicators that include moving averages and moving average convergence divergence, among others, can be transformed from single-market lagging indicators into intermarket-based leading indicators (see Figure 2).

With predictive information available to traders through use of leading indicators, traders will have the added confidence and self-discipline to adhere to trading strategies, which can enable them to pull the trigger at the right time without self-doubt or hesitation. In the fast-paced forex market, this can be the difference between success and failure.

About the Author

Louis B. Mendelsohn is president and chief executive officer of Market Technologies, a trading software development firm founded in 1979, that specializes in the use of intermarket analysis and predicted moving averages to forecast short-term trend direction. His firm’s software, VantagePoint Intermarket Analysis Trading Software, predicts market trends with nearly 80% accuracy for interest rates, stock indexes, currencies, energies, metals, grains, meats, softs, and stocks covering a total of over 600 financial futures and commodities markets. Market Technologies’ website is www.vantagepointsoftware.com and the phone numbers are 813-973-0496 or 800-732-5407