Unintended Consequences: The Pension Crisis, How We Got Here and What’s Next?

In late March 2020, the Federal Reserve Bank announced broad policy initiatives geared to support the economy. Among these measures were near-zero short-term interest rates, unlimited large-scale purchases of U.S. Treasury securities and mortgage-backed securities designed to stabilize the markets for consumer debt, corporate, and municipal bonds, and commercial paper.

As stated in its March 23 press release, the Federal Reserve intends these actions to “support smooth market functioning and effective transmission of monetary policy to broader financial conditions.”

On the surface, this policy sounds quite benevolent until you come to realize that for the last 30+ years the Fed has been trying to use lower interest rates to spur on economic growth with very limited success. Currently we create $7 in new debt to create $1 in New GDP. Furthermore, the most important metric in Capitalism is the cost of money (interest rates) which today the Fed has deemed to be near zero. There are huge consequences to manipulating the cost of money to zero. Specifically, this will result in a pension crisis that will make everything we have experienced so far, pale in comparison.

Pensions date back more than 100 years, to a time when most people didn’t live long enough to collect them. Nowadays Americans take living comfortably to 80 and beyond to be a given. Longevity in and of itself is wonderful, but it does have a few downsides—like a gradually declining pension system.

Note that we are talking here about a specific kind of pension: defined benefit plans. They are usually sponsored by state and local governments, labor unions, and a number of private businesses. Many sponsors haven’t set aside the funds needed to pay the benefits they’ve promised to current and future retirees. They can delay the inevitable for a long time but not forever. And “forever” is just around the corner. The numbers are large enough to make this a problem for everyone. The underfunded pensions could also be one of the triggers to the unprecedented credit crisis.

A report from Citigroup estimates governments around the world are short $78 trillion to pay their pension liabilities. This is about eleven times larger than the stimulus outlays we have seen so far with the COVID-19 lockdowns in the United States.

How could this occur?

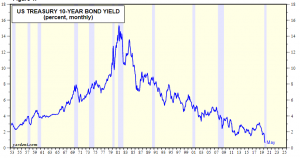

Look at the chart below –

Over the last 40 years interest rates have been falling precipitously. Since the 1987 stock market crash, lower interest rates were the remedy that the Federal Reserve always went to in their playbook, to spur on further economic growth. The mandate from the Federal Reserve Board of governors has always been lower interest rates and more stimulus.

In a defined benefit pension plan, employers set aside funds for their employees retirement. Traditionally these funds were not to be speculated with. Instead they were only to be invested in AAA Bonds which guarantee a very low risk of default! When the pension plans were created the actuaries felt it was safe to assume that they could realistically return 7% to Pensioners. They would do this by investing in high quality government bonds to ensure the quality of the principal that was invested.

But have you looked at what Bonds are yielding today? Less than 1%. Those low-interest rates that were used to spur on economic growth have simultaneously eroded the retirement plans for millions of workers. How? Well, let’s look at it this way – At a 1% yield you need to have a million dollars in bonds to create $10,000 in cash flow benefits. If you are expecting $50,000 a year in cash flow benefits, that would be the equivalent of $5 million in bonds to create the same type of cash flow.

The very economic activity that the Federal Reserve was trying to create has ended up hurting citizens and savers on Main Street the most.

The end result is these pension programs are massively underfunded because they have only been able to grow their principal by whatever the US Bond market is yielding, which is inadequate for the pension plan to remain solvent.

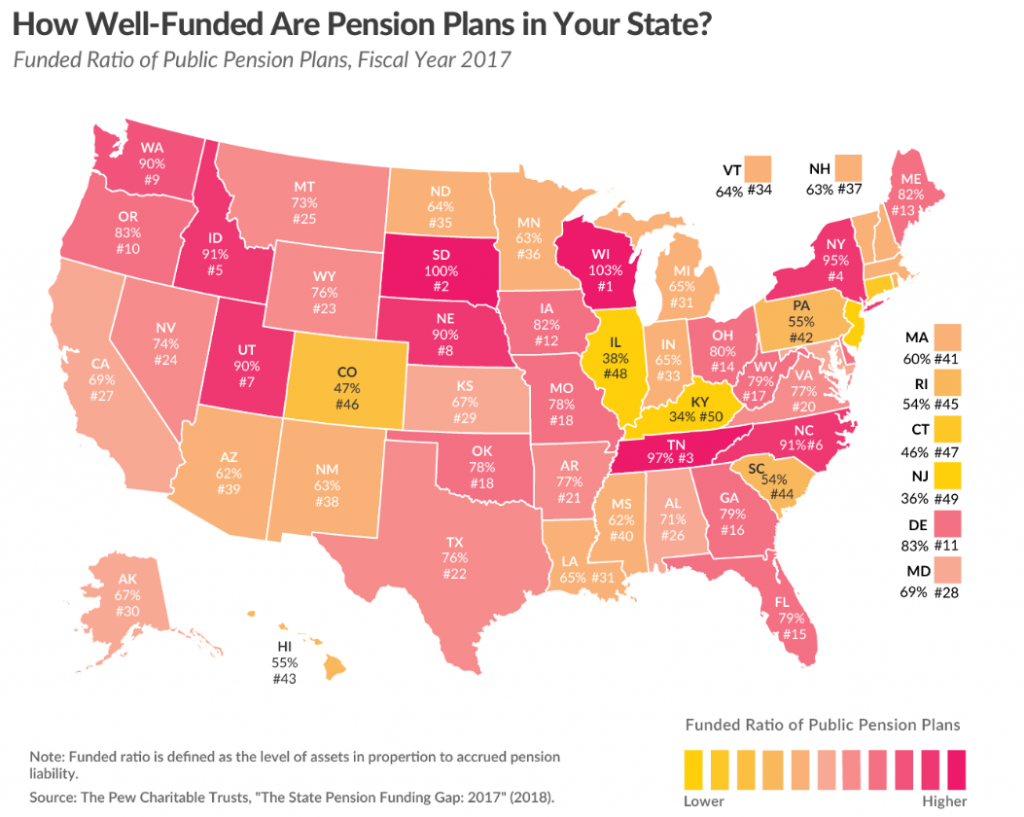

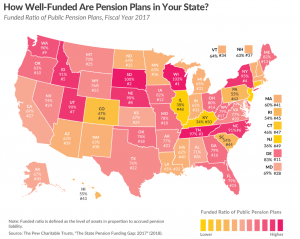

The chart below, created by Pew Charitable Trusts, shows the nature of the problem by showing what percentage of $1 each state has available to meet their pension obligations. Note that Kentucky for example, only has 34 cents on the dollar and is ranked at the bottom of all States. Wisconsin on the other hand is overfunded, and actually has $1.03 on hand to meet their $1.00 of obligations.

Chances are if you are a boomer this is old news to you. Most boomers discovered that after the 2008 Financial crisis that investing in bonds which offered very low returns was not going to allow them to reach their retirement goals.

The heartbreaking issue of this crisis is that we are looking at a social contract between a government and its citizens. The effect that this will have on our social fabric and discourse would be hazardously toxic. Think about the challenges of many of these State and local governments will face in the coming months as they try to collect taxes and the effects of the economic lockdown are more fully encompassed.

- In May 2020, 8.8% of all mortgages are in forbearance. This means that they are not making payments but have been granted a temporary exemption by banks from doing so.

- 4.7 million Americans cannot pay their mortgages right now. That is 1.5 million more than during the peak of the Great Financial Crisis in 2009.

- Almost 46 million Americans are out of work since early March. This is larger than the entire population of Canada.

It doesn’t require very much imagination to assume that these State and local governments are going to be facing massive tax delinquencies in the next twelve months.

What does this mean to you as an investor and trader?

My opinion is these pension funds are slowly being untethered from their commitment to only investing in credit instruments. Many of them have been blowing the whistle for many years that they can’t hit their 7% objectives, which is what is required to remain solvent when bonds are only yielding 1%. In other words, they have to chase yield.

Chasing yield is what creates massive volatility in the markets. Put yourself in the shoes of pension managers from the State of Kentucky. You have 34 cents to meet $1.00 worth of obligations. The only way you can recover that gap is by chasing yield in the stock market. I believe this has occurred in the FANG stocks already (Facebook, Apple, Netflix and Google). Kentucky would need 6 years of 20% returns to be fully funded! I am not advising that this should occur. Instead I am suggesting that it has probably already started.

Many of these pension funds are prohibited from trading and speculating in stocks by their charters. However, I think over the past two months one of the major factors that contributed to the shortest bear market in history is the reality that these huge pension funds have to chase yield when the Federal Reserve is maintaining a near-zero interest rate policy.

This is the Unintended Consequence of what appears to be a benevolent near zero interest rate policy.

The primary other consequence of this policy will be huge volatility in the financial markets. The rules and valuation methods of yesteryear will no longer be valuable in determining where you should commit your assets and energy for the greatest return.

This is where artificial intelligence and intermarket analysis will prove to be priceless for traders.

Since the 1980’s, when traders had a myopic focus, only looking at each market’s own price dynamics in isolation, Louis Mendelsohn, VantagePoint’s founder, began to recognize the dynamic interconnections occurring between related global markets and integrated them into his computerized trading strategies, fostering a technical analysis revolution.

VantagePoint A.I., first released in 1991, applied neural network pattern recognition to intermarket analysis to make highly accurate market forecasts based on intermarket correlations.

It is humanly impossible for a trader to calculate these complicated intermarket correlations. The only way to grasp the significance of their effects is through the application of sophisticated mathematical processes known as neural networks which have been developed and refined since 1991 in VantagePoint.

The essence of this process lies in understanding that every market is intertwined amongst other key drivers. Once you discover what the key drivers of an asset are, artificial intelligence and machine learning are capable of delivering forecasts one to three days in advance with up to 87.4% accuracy.

VantagePoint uses neural networks to identify which global markets have the most influence on a target market, then produces a set of intermarket data to generate predictive technical indicators that give you short-term price and trend forecasts. VantagePoint is able to make these incredibly accurate market forecasts because of Mr. Mendelsohn’s two patented technologies that have helped traders like you transform their trading and change their lives.

Look at the following chart now of the S&P 500 Index over the last few months and ask yourself if you could’ve made some profits for yourself based upon the artificial intelligence forecasts on the chart?

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it and then focuses on other paths to find a solution. This is the Feedback Loop that is responsible for building the fortunes of every successful trader I know.

Artificial Intelligence applies mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

That should get you pretty excited because it is a game-changer.

This is the winning combination.

Intrigued?

Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.