Let’s not sugarcoat it. UnitedHealth (UNH) has been dragging a giant public relations problem behind it ever since its CEO was assassinated. You don’t just brush that off with a press release and a quarterly earnings call. The headlines alone could have sunk a weaker company.

But, despite the tragedy and the PR black eye, and despite the sector being the market’s punching bag all year, $UNH kept printing money. Quarter after quarter, revenue kept climbing. Earnings? DOWN but rock solid. While the narrative was dark, the numbers told a different story: this was still one of the most profitable machines in corporate America.

Enter Buffett. No fanfare, no hints dropped to CNBC, no “Buffett tracker” countdown. Just a quiet, $1.6 billion stake built while everyone else was chasing shiny objects in tech. And then — boom — the filing hits in mid-August. $UNH rips higher. Traders pile in. Investors nod like old sages.

One disclosure. Two reactions. But the bigger story? Buffett just planted his flag in the middle of a battlefield most investors were too scared to step foot on.

Buffett doesn’t trade stocks. He buys businesses. And not just any businesses — the kind that make money in their sleep, while you’re brushing your teeth, or while Congress is screwing something up. His rules of engagement are disarmingly simple:

- A proverbial moat you’d need the Army Corps of Engineers to cross.

- Cash flows steadier than a church collection plate.

- Market dominance so entrenched it makes medieval kings look like temp workers.

That’s why he married Coca-Cola decades ago, waltzed with American Express, and spooned with Apple. He doesn’t “flip” them — he sends them anniversary cards.

Now along comes UnitedHealth ($UNH) — a company whose business model is so sticky that customers can’t leave without risking bankruptcy, a nervous breakdown, or both. Recurring premiums? Check. Monopoly-sized scale? Check. A chokehold on healthcare so tight it makes you long for the good old days of leeches and bloodletting? Double check.

For Buffett, this isn’t about what $UNH does in Q3. He doesn’t care if the stock sneezes this quarter or hiccups the next. He’s staring at 2040, and in his crystal ball $UNH isn’t just eking along — it’s fatter, richer, and even more indispensable. That’s his long game. And he’s been playing it better than anyone since Monopoly was invented.

Healthcare was the market’s laggard — the worst-performing sector of the year, weighed down by political scrutiny, rising costs, and a drumbeat of bad press. It looked untouchable. Then came Buffett. His disclosure of a $1.6 billion stake in UnitedHealth worked like a defibrillator. “Clear!” — and suddenly, the sector shot up.

It isn’t the first time Buffett has played this role. Years ago, his bet on Apple redefined “old tech” as a growth story again. His purchase of Burlington Northern Santa Fe ($BNSF) reframed railroads as indispensable infrastructure, not relics. More recently, his investments in Occidental Petroleum cast oil in a new light — not just a cyclical trade, but a long-term cash generator.

The pattern is unmistakable. When Buffett declares something a “forever stock,” he doesn’t just make a purchase — he sets the tone for Wall Street. Analysts can issue upgrades and fund managers can rotate portfolios, but Buffett’s signal is different. It’s a vote of confidence that transforms sentiment faster than any research note ever could.

In 2024, Buffett did something that rattled even his most loyal followers: he moved aggressively to cash. While the market was setting new highs, he quietly concluded that valuations had reached what he once called “nosebleed levels.” For a man whose mantra is to buy forever, the decision to sit on the sidelines looked uncharacteristically cautious — even pessimistic.

It sparked debate across Wall Street. Was this prudence, a seasoned investor recognizing excess where others saw opportunity? Or was it a signal that one of the market’s greatest optimists no longer trusted the rally? After all, this was the same Buffett who in 2008 famously leaned in when fear was everywhere. To see him step back in 2024 — while the S&P surged — was, at minimum, unsettling.

Critics accused him of being out of step with a new era of liquidity-driven markets. Supporters countered that the sheer volume of buybacks and speculative fervor demanded exactly this kind of restraint. Either way, the move was controversial because it went against his own legend: the investor who preaches forever suddenly seemed willing to wait.

But the episode underscored something essential about Buffett’s playbook. “Forever” doesn’t mean blind. It means disciplined. And in his mind, the discipline of holding cash was as much an investment decision as buying Apple or UnitedHealth.

Buffett’s philosophy is simple: buy stocks you can hold forever. His lens isn’t next quarter or even next year — it’s decades. That’s why a $1.6 billion stake in UnitedHealth matters. It signals that, despite political headwinds and messy headlines, he sees a durable business model with cash flows strong enough to outlast the cycle.

Most traders, by contrast, don’t see ahead decades. They see Friday. The moment Buffett’s position became public, the stock jumped, and so did short-term bets across the healthcare sector. For them, the play wasn’t about durability — it was about capturing a window of momentum before the trade ran out of steam.

Both approaches can be right. But the distinction underscores Buffett’s unique influence: his credibility doesn’t just move a stock; it validates an entire sector. In a year when healthcare was left behind, his “forever” vote of confidence sparked a wave of FOMO — traders chasing the immediate upside, investors recalibrating for the long term.

Healthcare is ugly. Let’s be honest. It’s political. It’s riddled with lawsuits, endless government red tape, drug price outrage, and yes — the assassination of a CEO that turned into a global PR nightmare. The headlines are toxic. The optics are a disaster.

But Warren Buffett doesn’t buy headlines. He buys cash flows. And in the middle of all the noise, UnitedHealth keeps doing what it has always done — printing money. This is the fortress business he craves: premiums paid like clockwork, margins insulated by scale, and a customer base that can’t just “shop around” for alternatives.

While the public sees scandal and outrage, Buffett sees durability. He sees a sector that — no matter how messy, no matter how political — is simply too essential to fail. And when it comes to building wealth, that’s the kind of cash flow that outlasts every storm.

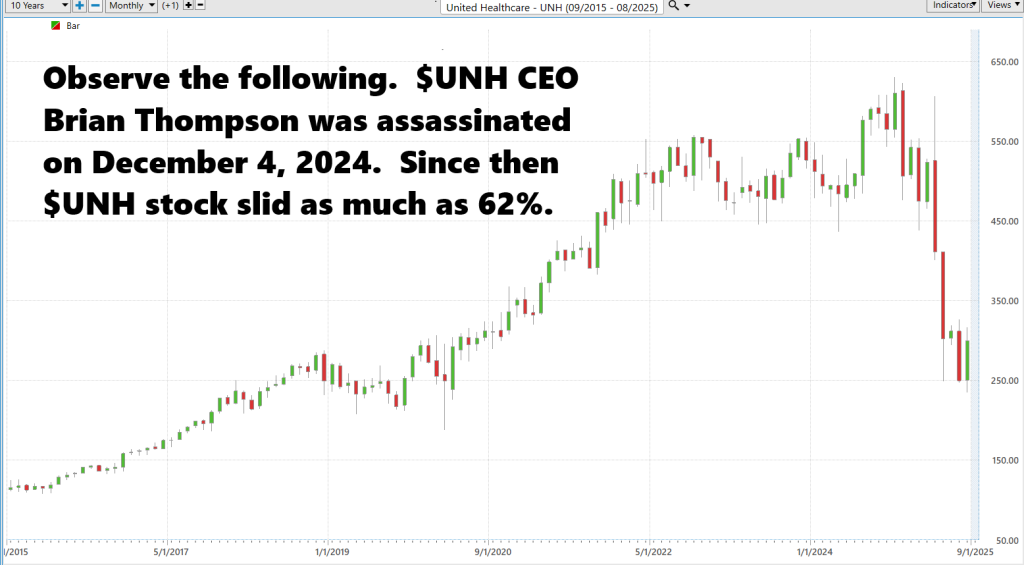

The collapse in UnitedHealth’s stock price since the assassination of CEO Brian Thompson tells a brutal story. Once one of the most reliable performers in the S&P 500, $UNH has cratered by as much as 62% since December 4, 2024. The chart makes clear what the market already knows: leadership shocks, combined with fears about profitability, have stripped the company of its defensive premium. Investors who once viewed UnitedHealth as a fortress stock suddenly treated it as radioactive, a dog in Wall Street’s kennel. In moments like these, the market doesn’t just punish — it overcorrects, wiping away decades of compounding with ruthless speed.

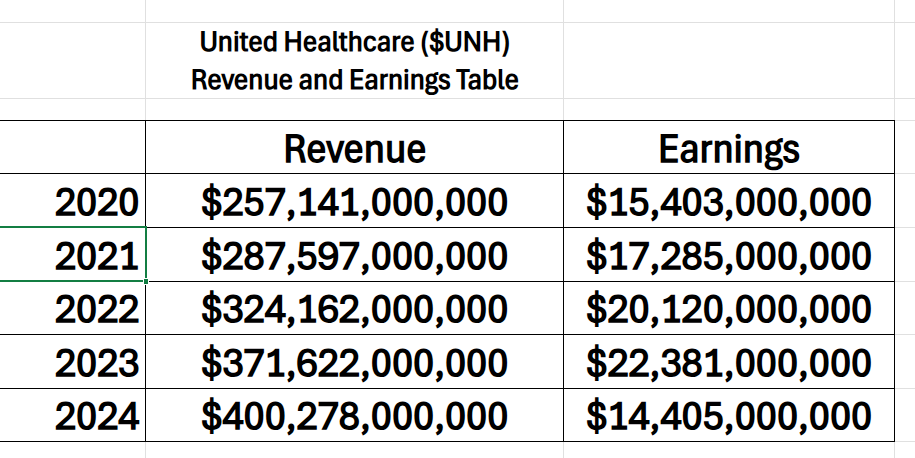

But look closer at the fundamentals, and a different picture emerges. Revenues have soared to record highs — topping $400 billion in 2024 — yet earnings have collapsed, sliding from more than $22 billion in 2023 to just $14.4 billion. On the surface, that looks like a margin crisis. Beneath it, though, is precisely the type of dislocation Warren Buffett has built a career exploiting. Cash flow, not quarter-to-quarter earnings, is the lifeblood of a business. And when a company with UnitedHealth’s scale and entrenched market position gets marked down to dog status, that’s when contrarians take notice. For Buffett, this isn’t a tragedy in numbers — it’s an invitation.

In the mid-1960s, American Express was engulfed in what became known as the Salad Oil Scandal. A company had faked massive amounts of soybean oil inventory, leaving AmEx with enormous losses. The scandal sent the stock tumbling, and many investors fled, convinced the brand’s reputation had been permanently damaged. Warren Buffett, however, saw something different. He recognized that the American Express name still carried enormous trust with consumers and businesses, and that its competitive position in payments remained secure. He invested heavily. What looked like a broken company to most turned into one of Buffett’s most enduring winners. Today, AmEx remains a cornerstone Berkshire holding, generating billions in value and proving the power of buying into a strong brand during a crisis.

Buffett’s Coca-Cola investment came in the aftermath of the 1987 stock market crash. Markets were reeling, and Coca-Cola’s shares had been knocked down. But Buffett saw beyond the temporary turbulence. He recognized the timeless appeal of Coke’s brand and the global distribution network that guaranteed consistent demand. In 1988, Berkshire poured over $1 billion into Coca-Cola, the largest investment in its history at the time. Buffett wasn’t chasing growth or technology — he was buying into a brand with unrivaled global recognition and predictable cash flows. More than three decades later, Coca-Cola continues to pay Berkshire over $700 million annually in dividends, a reminder that Buffett’s strategy of buying forever businesses can produce income streams that compound over generations.

Buffett’s relationship with Geico stretches across decades. He first purchased shares in 1951 as a young investor, drawn to the company’s direct-to-consumer model and low-cost structure. Decades later, when Geico faced challenges in the 1990s, Buffett returned with conviction. In 1996, Berkshire acquired the remaining shares of Geico for $2.3 billion. For Buffett, the appeal was obvious: an insurance model that was efficient, scalable, and sticky with customers. What others saw as a struggling company, he viewed as a long-term cash generator with unmatched competitive advantages. Geico has since become one of Berkshire’s crown jewels, providing steady underwriting profits and reinforcing the foundation of Berkshire’s insurance empire.

By 2016, Apple was already a tech giant, but skepticism was everywhere. Concerns about slowing iPhone sales weighed on the stock, and many investors feared its best days were behind it. Buffett, however, saw something different. He understood Apple’s ecosystem, customer loyalty, and brand dominance were the kind of moat he prized. Berkshire invested nearly $1 billion in 2016 and kept adding aggressively. At its peak, Berkshire owned more than 5% of Apple, worth over $160 billion. Beyond the massive capital gains, Apple also provided Berkshire with billions in annual dividends. It has since become Berkshire’s single largest holding — a rare tech investment that Buffett embraced because, in his words, it was “more of a consumer products company than a tech company.”

One Buffett filing doesn’t just move a stock — it moves the entire conversation. When Berkshire revealed its $1.6 billion stake in UnitedHealth, it wasn’t just $UNH that got a sugar rush. Suddenly, Humana, Cigna, Anthem, and even the lumbering $XLV healthcare ETF started looking like the belle of the ball. Wall Street, which had been treating the healthcare sector like a contagious disease, suddenly wanted a dance.

That’s Buffett’s real superpower. He doesn’t just buy businesses — he rewrites the narrative.

Think of it like a rising tide after Buffett drops anchor. The water level doesn’t just lift his ship — it lifts every boat in the harbor, including the leaky dinghies. Traders call it a sympathy play. Investors call it validation. Either way, when Buffett sneezes, whole sectors catch a bull market.

Here’s the thing about Warren Buffett: when everyone else is running for the exits, he’s the guy walking in with a shopping bag and a grin. Healthcare? It’s been radioactive all year. Politicians are swinging at drug prices, lawsuits are flying, and investors wouldn’t touch the sector with a ten-foot cattle prod. Perfect. That’s exactly when Buffett shows up with $1.6 billion for UnitedHealthCare.

Remember 2008, when Wall Street was on fire and Goldman Sachs was circling the drain? Buffett cut a deal, walked away with fat dividends and warrants, and everyone else kicked themselves for being too scared. Or look at his move into Occidental Petroleum when oil was bouncing around like a drunk at last call. People thought fossil fuels were dead. Buffett thought otherwise — and now he’s sitting on a cash machine. Even with airlines, which he swore off forever, he still had the guts to buy them when nobody else would.

This is Buffett’s edge: he doesn’t care about headlines, panic, or herd behavior. His “forever” mindset gives him the steel stomach to buy when everyone else is puking stocks into the gutter. That’s not luck. That’s discipline. That’s how you turn crises into fortunes.

Here’s the secret most investors and traders never learn until it’s too late: you can win at either game, but you can’t play both at once. Buffett’s moves aren’t about next week’s earnings call. They’re about the next generation’s economy. And Charlie Munger, in his usual dry brilliance, reminded us: “The big money is not in the buying and selling, but in the waiting.”

That’s the essence of investing — patience harnessed to durable cash flows. Buffett looks for businesses so bulletproof that time itself becomes his ally. He doesn’t care about the noise, the headlines, or the day-to-day swings. He’s building wealth the way cathedrals were built — brick by brick, meant to last for centuries.

But traders? They thrive on speed. They make their living in the space between today’s panic and tomorrow’s relief. They need catalysts, charts, and momentum, not moats and dividends. Both approaches can work beautifully. Yet disaster comes when you mix them. Sell a forever stock just because it didn’t move this week, and you’ve robbed yourself of compounding. Hold a trade because you fell in love with it, and you’ll ride it straight into the ground.

So, the choice is simple, but critical: decide which game you’re playing. As Munger put it, “It’s not supposed to be easy. Anyone who finds it easy is stupid.” If you’re an investor, marry forever stocks. If you’re a trader, chase momentum with discipline. But don’t get caught in the muddled middle. That’s where portfolios — and dreams — go to die.

At the end of the day, Warren Buffett and Charlie Munger weren’t just building Berkshire Hathaway — they were teaching a masterclass in discipline. Buffett once quipped, “The stock market is designed to transfer money from the active to the patient.” That’s the whole ball game right there.

You’ve just seen how Warren Buffett builds his fortune — not on speculation, not on hot tips, not on hype. He builds it on certainty. On cash flows he can count on. On “forever stocks” that compound quietly while the world chases shiny objects.

But here’s the question every serious trader and investor must ask themselves today:

👉 How do you find your own “forever” opportunities in a market that moves faster than Buffett ever imagined?

The answer is simple: you borrow his principles… and you turbocharge them with the one advantage Buffett never had — artificial intelligence Because A.I. doesn’t sleep. It doesn’t get distracted. It doesn’t fall in love with a stock. It scans thousands of assets across dozens of sectors in minutes, spotlighting the strongest trends and the hidden leaders — the very same way Buffett hunts for moats and cash flow. Only now, you can do it in real time.

That’s why I’m personally inviting you to join me for a very special “Learn How to Trade with A.I.” MasterClass.

In this online session, you’ll discover:

- How to spot “Buffett-style” forever stocks early — the ones with unstoppable trends and fortress fundamentals.

- How to identify entry and exit points with precision, so you’re not waiting decades to see profits compound.

- How to remove guesswork and gut feelings from trading — letting A.I. do the heavy lifting so you can focus on execution.

- How to thrive in any market, bull or bear, by following predictive analytics that show you where the real money is flowing.

Think of it this way: Buffett gave us the principles. A.I. gives us the playbook. Put them together, and you get a repeatable, reliable way to trade with confidence in today’s chaotic markets.

But you need to see it in action.

Reserve your seat now for the FREE “Learn How to Trade with A.I.” MasterClass.

It just might be the turning point in your trading journey — the moment you stop guessing… and start commanding the markets with the same calm conviction that has made Buffett one of the richest men alive. You can also learn more about how VantagePoint called the $UNH trend before the Buffet news by clicking here.

The difference between chasing the market and commanding it… can be just one decision away.

It’s not magic.

It’s machine learning.

Let’s Be Careful Out There!

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.