The Federal Reserve isn’t going to tell us what comes next anymore? No roadmap. No carefully crafted hints about future rate cuts. No clues about future rate hikes. No forecasts designed to help Wall Street prepare for what’s around the corner.

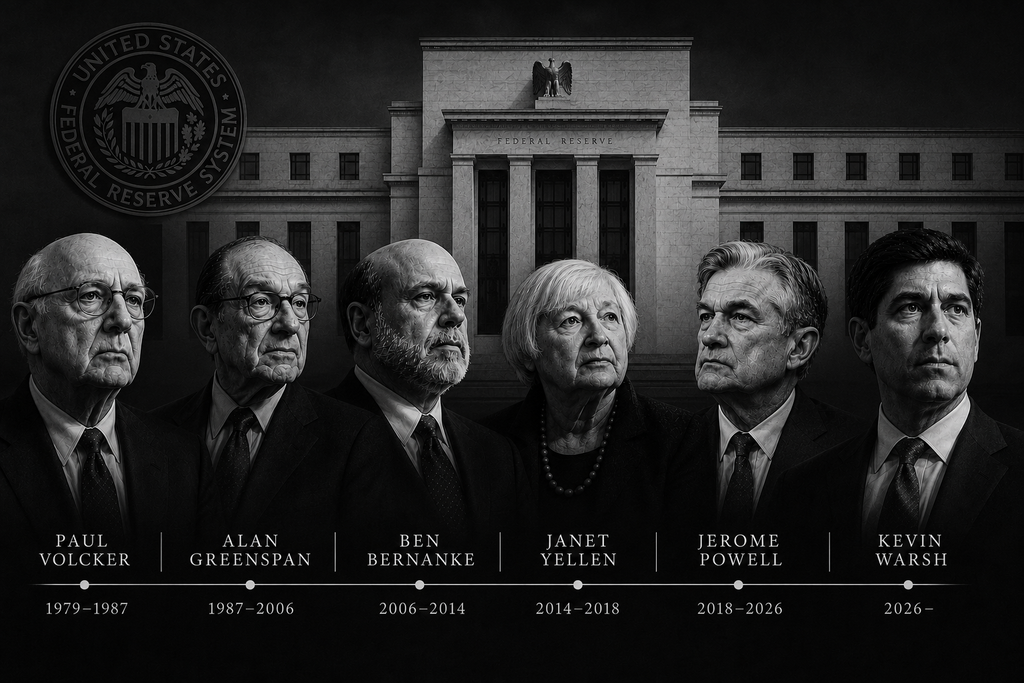

That’s exactly what new Federal Reserve Chairman Kevin Warsh signaled in his first press conference. And it may prove to be one of the most important shifts in Federal Reserve policy in decades. For years, investors have grown accustomed to hearing from the Fed. Markets hung on every word. Every statement was dissected.

The answer may be hidden in a lesson from the past. This past week, former Federal Reserve Chairman Alan Greenspan passed away at the age of 100. Greenspan led the Federal Reserve from 1987 through 2006 and became one of the most influential central bankers in modern history. During his nearly two-decade tenure, investors developed a belief that would permanently change how markets viewed risk.

That belief became known as the Greenspan Put. The concept was simple. Whenever markets experienced enough pain, investors believed the Federal Reserve would eventually step in with lower interest rates, additional liquidity, or other forms of support designed to stabilize the financial system. Whether that perception was entirely fair is still debated. What matters is that investors believed it.

Over time, that belief evolved into something larger. The Greenspan Put became the Bernanke Put. Then the Yellen Put. Then the Powell Put. Generations of investors grew accustomed to the idea that the Federal Reserve would not only manage monetary policy but also help cushion the impact of severe market declines.

In many ways, that expectation became just as powerful as the Fed’s actual policies. Which brings us back to Kevin Warsh. At the very moment the financial world is reflecting on the legacy of Alan Greenspan and the era he helped create, the new Chairman appears to be moving in a very different direction. Less guidance. Less forecasting. Less intervention through communication. More uncertainty. More responsibility. More emphasis on what markets are actually doing rather than what policymakers are saying. And that changes the game for investors.

Because while most people focus on stock picking, professional investors spend enormous amounts of time trying to understand the environment those stocks are operating in. The Federal Reserve remains one of the biggest influences on that environment. Interest rates matter. Liquidity matters. Credit conditions matter.

The cost of money influences nearly every financial asset on the planet. Which leaves investors facing an uncomfortable question. If the Fed stops telling us where it’s going, how do we figure it out for ourselves? How do we know whether interest rates are likely headed higher or lower? How do we know if liquidity is being added to the financial system or quietly removed?

How do we know whether conditions are becoming more favorable or less favorable for stocks? Those are important questions. But they may have a surprisingly simple answer. Markets leave clues. In fact, understanding a silent Fed may actually be easier than trying to decode thousands of carefully chosen words from a press conference. Because money leaves footprints. It moves. It rotates. It seeks opportunity. And if we know where to look, we can often learn more from the behavior of financial markets than we can from the speeches of policymakers.

The real question is no longer what the Fed says. The real question is what the market is telling us. And that is where our story begins.

For most of its history, the Federal Reserve did not spend much time explaining itself. Policymakers made decisions, adjusted interest rates when necessary, and largely allowed markets to interpret the consequences on their own. Investors focused on economic data, corporate earnings, business conditions, and market behavior. The Fed certainly mattered, but it was not the center of every financial conversation.

That began to change gradually during the 1990s and accelerated dramatically after the Financial Crisis of 2008. Policymakers became increasingly concerned that market expectations themselves could influence economic outcomes. If households, businesses, and investors believed rates would remain low, they might borrow, spend, invest, and hire more aggressively. Communication evolved from a supporting tool into a policy tool.

The result was the rise of what became known as forward guidance. Rather than simply announcing what it had done, the Federal Reserve increasingly told markets what it expected to do next. Investors were no longer evaluating only the current decision. They were evaluating a roadmap of future decisions that might unfold months or even years into the future.

One of the clearest examples occurred in August 2011. With interest rates already near zero, the Federal Reserve announced that it expected rates to remain exceptionally low for an extended period. Later, those timeframes were extended further. The policy itself did not immediately change, but expectations changed dramatically.

That distinction proved enormously important. Long-term interest rates are not determined solely by where rates stand today. They are influenced by where investors believe rates, inflation, and economic growth will be in the future. By shaping expectations, the Federal Reserve discovered it could influence financial conditions long before making an actual policy move.

Markets quickly learned the lesson. Every statement became an object of scrutiny. Investors searched for clues in individual words, sentence structures, and even punctuation. Entire teams of economists, strategists, and reporters were devoted to interpreting subtle changes in Federal Reserve language. The phenomenon reached new heights during the tenure of Jerome Powell. Press conferences became major market events. Investors dissected every answer, every phrase, and every shift in tone. The Federal Reserve was no longer simply setting monetary policy. It was actively shaping the narrative surrounding monetary policy.

In many respects, the strategy worked. Financial conditions often responded before rates changed. Markets became more predictable. Volatility sometimes declined. Policymakers gained another mechanism for influencing economic behavior without immediately adjusting interest rates.

Yet every policy creates unintended consequences. As communication became more detailed, investors became increasingly dependent upon it. Market participants devoted more attention to interpreting the Federal Reserve’s intentions than observing what markets themselves were communicating. Guidance became a source of comfort, and comfort gradually became an expectation.

Over time, investors learned to trade anticipated policy rather than observable reality. Instead of asking where capital was flowing, they asked what the Federal Reserve might say next. Instead of focusing on market leadership, they focused on future guidance. Instead of studying evidence, they studied forecasts.

This shift altered the relationship between investors and the Federal Reserve. What began as an effort to improve transparency evolved into something much larger. The Federal Reserve became Wall Street’s narrator, explaining not only where policy stood today but where it might be headed tomorrow.

That dependency matters because dependence changes behavior. The more investors relied on guidance, the more difficult it became to imagine markets functioning without it. Which helps explain why Kevin Warsh’s decision to communicate less has attracted so much attention.

For nearly two decades, investors became accustomed to having a narrator explain the story as it unfolded. Now, for the first time in a generation, that narrator appears to be stepping away from the microphone.

There is an old saying that if you feed a stray cat long enough, it eventually becomes your cat. Something similar happened to investors over the past three decades. Markets experienced a series of increasingly memorable encounters with the Federal Reserve. Every time conditions became painful enough, policymakers arrived carrying lower rates, fresh liquidity, emergency lending facilities, or some other financial version of relief.

At first, investors were grateful. Then they became comfortable. Eventually, they became expectant. By the time we reached the pandemic, many investors no longer viewed Federal Reserve intervention as an extraordinary event. They viewed it as standard operating procedure.

That change in thinking may be one of the most important developments in modern financial history. Think about it from the perspective of a trader. Imagine a casino where every losing streak eventually triggers a rebate from management. Would gamblers take bigger risks? Of course they would.

Would they place larger bets? Absolutely. Would they become more confident than the situation actually justified? Without question. Human beings respond to incentives, and markets are no different. When the consequences of risk appear smaller, people naturally become willing to take more of it. Over time, investors learned that periods of severe market stress were often followed by some form of policy response. Sometimes it came through interest-rate cuts. Sometimes through quantitative easing. Sometimes through emergency lending programs. The mechanism changed, but the lesson remained the same.

The Federal Reserve was paying attention. The term “Fed Put” eventually entered the financial vocabulary. The concept borrowed its name from put options, which gain value when markets decline. Investors began behaving as though the Federal Reserve itself had written an enormous insurance policy beneath asset prices.

If losses became large enough, policymakers would eventually step in to help stabilize conditions. Whether that belief was entirely accurate is almost beside the point. The important fact is that millions of investors acted as though it were. And behavior drives markets.

The result was one of the most remarkable shifts in investor psychology ever observed. Risk began to look safer. Leverage became more attractive. Speculation became easier to justify. Valuations expanded as investors became increasingly comfortable paying higher prices for future earnings. To be fair, many of the Federal Reserve’s interventions occurred during genuine crises. Policymakers were attempting to preserve financial stability, not encourage speculation. But markets rarely focus on intentions. Markets focus on outcomes. And the outcome was clear. A generation of investors came to believe that severe market declines would eventually attract a policy response. That belief became self-reinforcing. Investors bought dips because previous dips had been rescued. Institutions added risk because previous crises had been stabilized.

The longer the pattern continued, the stronger the expectation became. Then something interesting happened. Markets stopped focusing primarily on economic reality and began focusing on the reaction function of the Federal Reserve. Instead of asking, “What is this asset worth?” investors increasingly asked, “What will the Fed do if this falls?”

That is a very different question.

One seeks value.

The other seeks protection.

And once enough people start seeking protection, the character of a market begins to change. Risk becomes something to be managed by policymakers rather than by investors themselves.

Which brings us back to Kevin Warsh. A quieter Federal Reserve may represent more than a communications strategy. It may represent an attempt to restore something markets have not experienced in quite some time: uncertainty. That word tends to make investors uncomfortable, but uncertainty serves an important purpose.

Uncertainty forces participants to evaluate risk honestly. It forces prices to reflect reality rather than expectations of rescue. It forces traders to focus on evidence instead of assumptions. For years, many investors looked to the Federal Reserve for reassurance.

Kevin Warsh appears to be asking markets to find their own confidence. Whether investors welcome that change remains to be seen. But one thing is already clear. The era of constant guidance and perpetual reassurance may be giving way to something very different.

And that makes the next question particularly important. If the Federal Reserve is stepping away from certainty, why would its Chairman refuse to provide a forecast of his own?

One of the most useful mental models in investing is surprisingly simple: never confuse confidence with knowledge. Human beings do this constantly. Someone speaks confidently, and we assume they know what they are talking about. Someone makes a forecast with conviction, and we assume the forecast is reliable. Someone occupies a position of authority, and we assume they possess information unavailable to everyone else. Unfortunately, none of those assumptions are necessarily true. The future remains stubbornly difficult to predict. That reality brings us to one of the most curious decisions Kevin Warsh made during his first Federal Reserve meeting.

He declined to submit a dot plot. For those unfamiliar, the dot plot is the Federal Reserve’s quarterly forecast of where individual policymakers believe interest rates are headed over the coming years. Each policymaker submits a projection, and those projections are then published for investors to study. The theory sounds reasonable enough. Gather the views of the people closest to monetary policy and provide investors with a glimpse into the future. The problem is that forecasting the future has a terrible track record, particularly among economists. This is not a criticism. It is simply reality. Economies are complex systems, financial markets are complex systems, and human behavior itself is a complex system.

The interaction of millions of consumers, businesses, investors, governments, and institutions creates a level of complexity that exceeds anyone’s forecasting ability. Yet markets often treat forecasts as if they were facts. Think about what has occurred over the last decade alone. Economists missed inflation, missed the speed of inflation, and missed the persistence of inflation.

They missed recessions. They missed recoveries. They missed interest-rate paths. None of this is unusual because forecasting errors are normal. The future contains information that has not happened yet.

Charlie Munger frequently warned about this tendency. He understood that intelligent people are particularly vulnerable to creating elaborate stories about the future. The more sophisticated the story becomes, the easier it is to mistake speculation for certainty. Markets reward humility far more often than they reward overconfidence.

Which is why Warsh’s blank dot plot is so interesting. Most observers interpreted it as a refusal to communicate. Perhaps it was something else entirely. Perhaps it was an admission that no individual, regardless of title, can reliably forecast where interest rates, inflation, economic growth, employment, geopolitical risks, technological disruption, consumer behavior, fiscal policy, and financial markets will intersect several years from now.

That is not weakness. That is intellectual honesty. Investors often demand certainty from policymakers, but certainty is frequently unavailable. When certainty is unavailable, pretending otherwise becomes dangerous.

A bad forecast can be worse than no forecast at all. It can encourage leverage. It can encourage complacency. It can encourage investors to position themselves around a future that never arrives.

Good investors understand this intuitively. They operate in probabilities. They manage risk. They adapt when conditions change. Most importantly, they remain willing to admit when they are wrong.

Markets punish certainty more often than they punish caution. This may be the deeper message behind Warsh’s decision. Instead of offering another collection of educated guesses, he may be signaling that investors should spend less time focusing on forecasts and more time focusing on evidence.

Because evidence is observable. Evidence is measurable. Evidence is occurring right now. Price is evidence. Volume is evidence. Relative strength is evidence. Capital flows are evidence.

The market, on the other hand, is revealing what is happening today. That distinction may become increasingly important in the years ahead. Fortunately, markets leave clues everywhere. The challenge is learning where to look.

Before we discuss where money may be flowing next, it helps to understand one of the simplest ways to measure the market’s confidence in the financial environment. Most investors look at the S&P 500 Index in isolation. The index rises. The index falls. Conclusions are drawn. But viewed alone, the S&P 500 tells us very little about investor preferences.

What matters is not simply whether stocks are rising or falling. What matters is whether stocks are attracting capital relative to other major asset classes competing for the same investment dollars. After all, every investment decision involves a comparison. A portfolio manager buying stocks is simultaneously deciding not to buy something else. That “something else” often includes gold, silver, Bitcoin, and crude oil.

Each of these assets tends to represent a different set of economic expectations. Gold often reflects a desire for stability, purchasing-power preservation, or protection against financial uncertainty. Silver frequently combines monetary concerns with industrial demand expectations. Bitcoin is increasingly viewed as a speculative growth asset and, by some investors, a hedge against currency debasement. Crude oil serves as a proxy for economic activity, industrial demand, and inflationary pressures throughout the global economy.

By comparing the performance of the S&P 500 against each of these assets over identical periods, we gain a clearer picture of where capital is actually flowing. The calculation itself is straightforward. If the S&P 500 rises 12% while gold rises 8%, stocks are outperforming gold by 4 percentage points. If Bitcoin rises 20% while the S&P 500 gains 12%, Bitcoin is outperforming stocks by 8 percentage points. The comparison is repeated across each major asset class and across multiple time horizons.

The objective is not to determine which market is rising. The objective is to determine which market is winning the competition for capital. That distinction is critical. Markets do not operate in a vacuum. Investors constantly allocate and reallocate capital among competing opportunities.

Pension funds, hedge funds, institutions, sovereign wealth funds, family offices, and individual investors are all making variations of the same decision every day: Where can my capital earn the highest risk-adjusted return? The answers to those decisions leave footprints. When stocks consistently outperform gold, silver, and other defensive assets, investors are generally expressing confidence in economic growth, corporate earnings, and risk-taking behavior. When gold and silver begin outperforming stocks, investors may be signaling increased concern about inflation, financial stability, or future growth.

When Bitcoin dramatically outperforms both stocks and precious metals, it often reflects an increased appetite for speculation, innovation, and future-oriented themes. And when crude oil begins attracting capital relative to financial assets, investors may be anticipating stronger economic activity, rising inflationary pressures, or tightening energy supplies. Viewed together, these relationships provide something extraordinarily valuable. They provide context. Not opinions, forecasts, or economic predictions, but evidence.

Evidence of where investors are choosing to deploy capital today. Because money has a remarkable habit of revealing what investors truly believe long before economists, policymakers, and financial commentators explain why they believed it. In a world where the Federal Reserve may be saying less, understanding where money is moving may become more important than ever. If forecasts become less useful, the flow of capital becomes increasingly valuable. It offers investors a real-time report card on confidence, fear, growth expectations, inflation concerns, and risk appetite.

Each asset represents a different economic narrative. When crude oil outperforms everything else, investors are often betting on stronger global demand, persistent inflation, supply constraints, or geopolitical tensions that could keep energy prices elevated. When Bitcoin becomes the strongest performer, it usually reflects a surge in speculative appetite, abundant liquidity, optimism toward innovation, and a willingness to embrace higher risk. When gold rises to the top of the leaderboard, investors are typically seeking safety, preserving purchasing power, and preparing for uncertainty surrounding inflation, currencies, or financial stability. And when the S&P 500 leads, investors are expressing confidence in corporate earnings, economic growth, and America’s ability to generate profitable businesses.

This matrix reveals something far more important than which market is up or down. It reveals where the world’s capital is choosing to live.

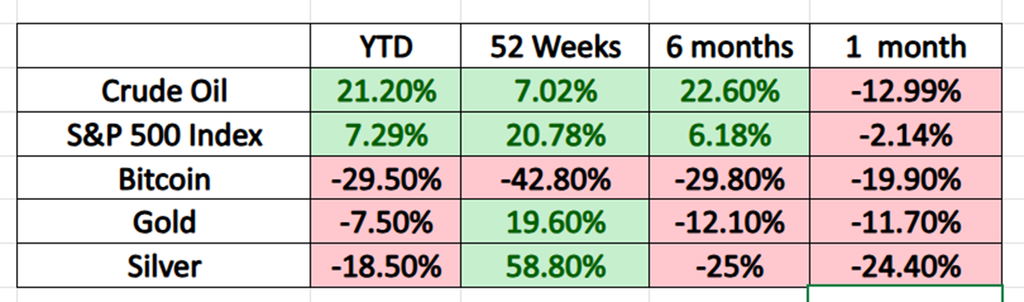

Today’s matrix paints a fascinating picture. Crude oil is the clear leader, suggesting that investors continue to price in resilient economic activity, lingering inflationary pressures, or heightened geopolitical risk. The S&P 500 remains remarkably resilient, evidence that confidence in corporate America has not disappeared despite a more challenging environment. Bitcoin, however, has become the weakest major asset across every measured period, signaling a meaningful retreat from speculative capital as investors demand stronger fundamentals and more immediate cash flows. Even more telling is the one-month column, where weakness has spread across nearly every asset class. That suggests investors are becoming more selective rather than simply moving from one market to another. In other words, this is no longer a market driven by easy money. It is becoming a market driven by discernment, where capital is rewarding evidence over enthusiasm and fundamentals over speculation.

The market is constantly voting. Every allocation decision casts a ballot. Every trade reveals a preference. Every dollar committed to one asset is a dollar not committed somewhere else. By observing those decisions objectively, investors gain insight into what market participants actually believe rather than what they claim to believe.

And that may prove to be one of the most important lessons of a quieter Federal Reserve. When policymakers speak less, the behavior of capital speaks louder. The clues are there every day. The challenge is learning how to read them.

For the better part of two decades, investors have spent an extraordinary amount of time listening. Listening to speeches. Listening to press conferences. Listening to forecasts. Listening to Federal Reserve officials explain what they might do next. The majority of the time the opinions that were provided were horribly wrong and misguided.

Kevin Warsh’s message appears straightforward: stop listening so much and start watching. Because the truth is that money moves before narratives do. Long before economists explain a trend, long before reporters identify a theme, and long before policymakers acknowledge a shift, capital begins moving. Those movements leave footprints.

The challenge for investors is learning how to recognize them. One of the clearest places to start is relative performance. Not whether an asset is rising, but whether it is outperforming. Those are very different things.

A stock can rise and still be a poor investment if better opportunities exist elsewhere. Likewise, an entire sector can appear healthy while quietly losing the competition for capital. Professional money managers understand this instinctively. They are not trying to identify what is good. They are trying to identify what is best.

Capital naturally gravitates toward leadership. That is why relative strength remains one of the most powerful concepts in investing. The strongest assets tend to attract additional capital. The weakest assets tend to lose it. Success often attracts more success, while failure frequently attracts more failure.

This principle becomes especially important when examining the relationship between stocks, precious metals, cryptocurrencies, and commodities. These markets compete with one another every day for investment dollars. If the S&P 500 is outperforming gold, silver, and other defensive assets, investors are expressing confidence in growth, earnings, and risk-taking. If gold and silver begin outperforming stocks, investors may be becoming more defensive.

If Bitcoin begins dramatically outperforming nearly everything else, investors may be embracing speculation, innovation, and future-oriented themes. Every relationship tells a story. The story is not what investors are saying. The story is what investors are doing. And money is far more difficult to fake than words.

This is why comparing the performance of major asset classes can be so revealing. Stocks, gold, silver, Bitcoin, and crude oil each represent different expectations about growth, inflation, risk, and opportunity. When one asset consistently outperforms the others, it is often attracting a disproportionate share of available capital. Those flows tell us where conviction is building.

Consider what is happening today. One of the largest capital-allocation events in modern financial history is unfolding in plain sight: SpaceX. The company immediately entered the ranks of the world’s largest and most valuable enterprises. Investors around the globe want exposure. The excitement is understandable, and the opportunities may be enormous.

But there is a mathematical reality that cannot be ignored. A dollar cannot be in two places at the same time. Every dollar committed to SpaceX must come from somewhere. Perhaps it comes from an existing stock portfolio. Perhaps it comes from bonds, gold, Bitcoin, cash, or margin.

The source matters because when enough dollars move in one direction, they inevitably leave another. This is why successful traders spend so much time studying capital flows. The winners and losers are often revealed long before the headlines catch up. When institutional money begins rotating aggressively into a sector, that sector tends to outperform. When institutions begin exiting a market, weakness often appears long before the explanation arrives.

This process is happening every day. Technology versus financials. Growth versus value. Stocks versus commodities. Bitcoin versus gold. Risk assets versus defensive assets. The competition never stops, and neither does the information.

In many ways, markets function like a giant voting machine. Every transaction represents a choice. Every allocation reveals a preference. Every dollar cast is a vote for one opportunity and against another. Collectively, those votes tell us where confidence resides and, more importantly, where confidence is growing.

This is precisely why traders should pay close attention to leadership. New 52-week highs. New 10-year highs. Sectors consistently outperforming broad market benchmarks. Asset classes attracting capital across multiple time frames. These are not random observations. They are evidence.

The beauty of this approach is its simplicity. It does not require predicting the next Federal Reserve meeting. It does not require forecasting inflation six months from now. It does not require guessing what a Chairman may say during a future press conference. It requires observing where money is flowing today.

That information is available to everyone willing to look. In fact, it may become even more valuable in a world where the Federal Reserve communicates less frequently. Because when policymakers become quieter, market behavior becomes more important. And market behavior has always communicated something important.

The strongest opportunities are usually found where capital is arriving. The greatest risks are often found where capital is quietly departing. The Federal Reserve may be speaking less. The market, however, continues talking every single day.

The question is whether investors are listening to the right voice.

For most of financial history, investors operated without a safety net. Markets rose. Markets fell. Companies succeeded. Companies failed. Investors made money, and investors lost money. The process was often messy, occasionally painful, and frequently humbling, but it served an important purpose: it allowed markets to determine value.

Over the last several decades, however, something changed. As Federal Reserve communication expanded and intervention became more common during periods of financial stress, many investors grew accustomed to a different environment. It was an environment with more guidance, more forecasts, more reassurance, and more visibility into the thinking of policymakers. Whether intentional or not, those developments reduced uncertainty.

While uncertainty is uncomfortable, it serves an important economic function. Uncertainty forces discipline. Uncertainty forces risk assessment. Uncertainty forces investors to think independently. When uncertainty declines, something else often declines with it: respect for risk.

This is one reason periods of easy money and abundant liquidity frequently coincide with speculation. Investors become increasingly comfortable assuming that favorable conditions will continue indefinitely. Valuations expand. Leverage increases. Risk-taking becomes easier to justify. Then reality eventually intervenes.

It always does.

The market has a remarkable way of reminding participants that uncertainty never truly disappears. It merely hides for a while. Kevin Warsh’s approach may represent an acknowledgment of that reality. By speaking less, forecasting less, and guiding less, the Federal Reserve may be shifting responsibility back to investors.

That may sound unsettling. In many respects, it should. Successful investing has never been about finding certainty. It has always been about managing uncertainty better than others. The best investors understand this intuitively.

Warren Buffett has often remarked that he has no idea what interest rates, economic growth, elections, or market sentiment will look like next year. What he does understand is value, probabilities, incentives, and risk. Charlie Munger spent decades warning investors about overconfidence, prediction, and the dangers of believing they understood a future that had not yet arrived.

Both Munger and Buffett built their success by adapting.

That distinction becomes particularly important in the environment that may lie ahead. A market with less guidance may become a market with greater dispersion. Some assets will thrive. Others will struggle. Some sectors will attract enormous pools of capital, while others may be left behind.

The gap between winners and losers may widen. For traders, that creates both risk and opportunity. Risk because uncertainty tends to increase volatility. Opportunity because volatility often creates mispricing. And mispricing creates opportunity for disciplined investors who remain focused on evidence rather than emotion.

The irony is that many investors fear uncertainty precisely because they misunderstand its role. Uncertainty is not a flaw in markets. It is a feature. Without uncertainty there would be little opportunity. If everyone knew exactly what interest rates, inflation, earnings, economic growth, and asset prices would be twelve months from now, investing would become little more than bookkeeping.

The opportunity exists because the future remains unknown. That is what creates risk. It is also what creates reward. Perhaps that is the larger lesson behind Kevin Warsh’s decision. The Federal Reserve cannot eliminate uncertainty.

The dot plot cannot eliminate uncertainty. Forward guidance cannot eliminate uncertainty. At best, they can create the appearance of certainty. The market eventually discovers the difference. And that discovery process is what economists call price discovery.

Every day millions of investors express opinions with real money. Those opinions compete against one another. Some prove correct. Others prove costly. The resulting prices become a reflection of collective judgment. The process is imperfect, often emotional, and occasionally irrational.

Yet over time it remains remarkably effective.

The market finds its way.

Which may explain why periods of great uncertainty have often produced extraordinary opportunities for disciplined investors. Not because uncertainty disappeared, but because uncertainty was properly priced. As the Federal Reserve becomes quieter, investors may find themselves relying less on official forecasts and more on market evidence.

That is not necessarily a step backward. It may be a return to the way successful investing has always worked. Less prediction. More observation. Less certainty. More discipline. Less faith in forecasts and more respect for evidence.

And perhaps, in the long run, a healthier market as a result.

The passing of Alan Greenspan marks more than the end of a remarkable life. It may also symbolize the closing of an important chapter in Federal Reserve history. Greenspan helped shape an era in which investors increasingly looked to central bankers for reassurance. Over time, that reassurance evolved into the Greenspan Put, the Bernanke Put, the Yellen Put, and ultimately the Powell Put.

Along the way, financial markets became accustomed to guidance, forecasts, intervention, and the belief that policymakers would help cushion the impact of severe market disruptions. Kevin Warsh appears to be moving in a different direction. His first actions as Chairman suggest a Federal Reserve that intends to speak less, forecast less, and rely less on managing investor expectations. Whether that approach proves successful remains to be seen.

What is already clear, however, is that investors will need to adapt. For years, many market participants spent enormous amounts of energy trying to anticipate what the Federal Reserve would say next. The challenge now may be learning to focus on something more important: what the market itself is saying. Because markets communicate every day.

They communicate through prices, trends, relative strength, and capital flows. They communicate through the ongoing competition between stocks, bonds, gold, silver, Bitcoin, crude oil, and every other asset class competing for investment dollars. Those signals often reveal changing conditions long before policymakers acknowledge them. They often reveal those changes long before headlines explain them.

The most successful traders understand this. They do not begin with predictions. They do not begin with opinions. They do not begin with headlines. They begin with evidence.

They study where capital is flowing. They identify leadership. They measure relative performance. They focus their attention on assets attracting participation rather than those losing it. That discipline may become even more valuable in the years ahead.

A quieter Federal Reserve does not mean investors have less information. It simply means the information may come from a different source. Not from a press conference. Not from a dot plot. Not from a carefully worded statement.

Instead, the information comes from the market itself.

At Vantagepoint AI, this principle sits at the heart of everything we do. Rather than attempting to predict what policymakers might say tomorrow, we focus on forecasting where money is moving tomorrow. Our tools are designed to help traders predict emerging trends, measure relative strength, monitor intermarket relationships, and uncover opportunities that may not yet be obvious to the broader market.

Because in every market environment, one truth remains unchanged. Money leaves footprints. The Federal Reserve may have stopped talking. The market never did.

The Federal Reserve may choose to speak less in the years ahead, but that does not leave investors with less information. It simply changes where the best information comes from. Instead of listening for clues in carefully scripted press conferences, successful traders will increasingly look to the market itself. Capital flows, relative strength, intermarket relationships, historical precedent, probabilities, and risk have always been the market’s true language. The challenge has never been finding information. The challenge has always been knowing how to interpret it correctly.

The truth is that this type of analysis is extraordinarily time-consuming. Done properly, it requires comparing today’s market with similar periods throughout history, measuring how thousands of markets behaved under comparable conditions, evaluating probabilities rather than opinions, and constantly reassessing risk as new information becomes available. Until recently, this kind of work required teams of highly trained analysts and weeks of research. Today, advances in artificial intelligence and computing power allow VantagePoint AI to perform much of that analysis in minutes, transforming an overwhelming amount of market data into practical artificial intelligence data that traders can actually use.

At its core, intelligent investing has never been about predicting the future with certainty. It has always been about recognizing when the probabilities are shifting in your favor and, just as importantly, recognizing when they are not. That simple distinction often separates consistently successful traders from those who spend years chasing headlines, emotions, and yesterday’s news. Which group do you belong to? More importantly, how are you doing this year compared to the S&P 500 Index? Are you outperforming the market, or has the market quietly been outperforming you?

If you’d like to see how professional traders use artificial intelligence to forecast emerging trends, measure market leadership, monitor capital flows, and manage risk before the crowd catches on, I invite you to join us for a free Learn How to Trade with VantagePoint AI live online masterclass. You’ll discover how today’s most advanced forecasting technology helps traders analyze the markets with a speed and depth that would have seemed impossible only a few years ago. More importantly, you’ll see how objective, probability-based trading analysis can help you make better decisions in a world where the Federal Reserve may be saying less, but the markets continue speaking every single day.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.