[fusion_builder_container hundred_percent=”no” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” overlay_color=”” video_preview_image=”” border_color=”” border_style=”solid” padding_top=”” padding_bottom=”” padding_left=”” padding_right=”” type=”legacy”][fusion_builder_row][fusion_builder_column type=”1_1″ layout=”1_1″ background_position=”left top” background_color=”” border_color=”” border_style=”solid” border_position=”all” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” center_content=”no” last=”true” min_height=”” hover_type=”none” link=”” first=”true” border_sizes_top=”” border_sizes_bottom=”” border_sizes_left=”” border_sizes_right=”” type=”1_1″][fusion_text]

No Upside. All Downside. How Is This Good Economic Policy?

The Federal Reserve Chairman, Jerome Powell, hosted an online press conference last week and answered questions from financial journalists around the world. The press conference came on the heels of a speech he made in Jackson Hole, Wyoming a few weeks earlier.

The key theme of the Fed’s new policy is to push interest rates down to zero while simultaneously targeting a slightly higher than 2% inflation rate.

Often when you hear about Fed policy there is a lot of “grey” which is subject to interpretation. The challenge with this policy was how black and white it was, and how few seem to comprehend it.

Personally, I waited and waited for a journalist to ask the only three questions which mattered. Instead, there was a lot of verbose chatter about technical economic terms and the journalists seemed to strive to sound ‘intelligent’ over probing.

Before I share with you those three key questions, what would you ask Fed Chairman Jerome Powell if you had the opportunity to do so?

The policy paper read as follows:

The Federal Reserve expects to keep interest rates near zero until at least 2023 to help reinvigorate the coronavirus-stricken economy, the central bank announced Wednesday in opting to leave rates unchanged. The widely expected decision to stand pat on interest rates is in line with the Fed’s recent policy shift. “Many find it counterintuitive that the Fed would want to push up inflation,” Powell said in prepared remarks. “However, inflation that is persistently too low can pose serious risks to the economy.”

One of the key principles of investing and good economic policy is a principle called the “Real Rate of Return.” This idea is the bedrock of basic investment analysis. It’s calculated by taking the yield of an asset and subtracting the projected inflation. So, if the policy paper was accurate, the yield on a 10 Year Treasury Bond was ZERO, and inflation was at 2%, that means that the real rate of return for investing in any American Treasury instrument, moving forward, was negative 2%. Billions of dollars mature every week from past Treasury activity. They usually just roll over their commitments to another U.S. Treasury bond at least 10 years into the future. One question I had is very simple. Who is going to buy any American credit obligation when your net return is best case is negative 2% per year? How does anyone get convinced that a “guaranteed loss of money” is a good idea for them to pursue? How in the world is this good economic policy?

Someone in the Financial Media has to ask this most basic fundamental question.

As far as I am concerned “Is this good economic policy” is the most important question of all regarding the Fed controlling American interest rate. For the last 30 years the only organization purchasing Japanese debt is the Japanese Central bank for the same financial reasons. During this time frame Japan, the third largest economy in the world, behind the U.S. and China has languished economically.

I have written at great length about the unintended consequences of such policy and how toxic and damaging it is for Central Planners to control interest rates. It always sounds very altruistic and noble but the long term effects of such policies are very destructive. Every public pension program that has been created has its solvency threatened if they cannot yield at least 7%. These pension programs have created social contracts with millions of retirees. All of these local, state and federal employees are now put at greater risk. How does a pension program which is specifically chartered to invest in the safety of government credit return 7% when the Fed Chairman is guaranteeing that the best case investment return on American credit is negative .58%? How is this good government policy?

As of this writing, the 30 Year Treasury Bond is yielding 1.42%. Subtract your average 2% inflation target from that yield and you end up with a negative -.58%.

How is this guaranteed loss good for anyone?

As the financial media neglected to ask this question, I kept thinking about every economic textbook I’ve read or class I ever sat through and how what was occurring proved how dismal of a science economics truly was. Directly related to the real rate of return, the cornerstone of all valuation models in finance is what is referred to as the “risk free financial rate.” This benchmark is incorporated as the foundational metric for all of finance. Every cash flow, business valuation and options pricing model in existence bases all of its calculations from what is the rate of return someone could earn, if they did the least possible and had zero risk. In practice, however, a truly risk-free rate does not exist because even the safest investments carry a very small amount of risk. Thus, the interest rate on a three-month U.S Treasury is often used as the risk-free rate for U.S.-based investors. The 3 Month Treasury Bill Rate is at 0.10%. If I earn .10% on my t-bill over 90 days, and subtract my .5% for inflation adjusted quarterly, I come up with a negative risk free rate of minus -.4%. Excuse me, Mr. Fed Chairman, you’re telling me I will lose .4% every 90 days.

And that is the best-case scenario for short government debt?

Where is the upside?

I lose 4/10 of 1% every 90 days if I participate and place my money in U.S. T-bills, assuming the Fed can hit their 2% inflation target. If I don’t participate, and place my money underneath my mattress, I lose 5/10th’s of 1%. Once again, no upside. All downside. How is this good economic policy?

Directly related to this question is the issue of retirement. How do you retire in this environment?

What every individual wants to accomplish in their life is to be able to save their money and then retire when they have done the effective economic planning for their future. Retirement planning at its essence has always been about buying cash flow. Traditionally this has been done by purchasing U.S. government bonds. Only a decade ago a retiree would scrape together their life savings and if they wanted $50,000 a year in income, they would buy one million dollars of U.S. government bonds at 5%. Today that 10 year government bond is yielding 6/10ths of 1%. So you invest one million dollars with the U.S. Treasury and today you get $6,000 a year? And then lose $20,000 in purchasing power to inflation.

Where is the upside? Since this new “visionary” Fed policy is in place till 2023, hasn’t the Fed literally outlawed retirement until then?

Please do the math for yourself and see what you come up with. Whether the Federal Reserve realizes this or not, we’re talking about trillions of dollars that will now chase yield in other asset classes. Unless they’re convinced losing 2% per year is in their best interest.

Watching this Federal Reserve press conference certain made me understand what drives markets. The only other question worth asking then is, where is all of this money that would traditionally roll over into Treasury Bonds going to go? There are only three choices.

- Stocks

- Precious Metals

- Bitcoin

We’re talking about trillions of dollars that will be moved amongst these three categories in the coming years as people try to retain the purchasing power of their assets and stay out of U.S. Treasuries.

Economists and the talking heads in the financial media love to talk about the Consumer Price Index as the boogeyman metric of inflation. This is the greatest of all distractions because the CPI bears no resemblance to day to day living which every individual encounters in their finances. The Consumer Price Index is literally a cherry picked basket of goods and services that is designed to communicate what the government wants you to see. Instead inflation is very nuanced based upon the type of goods or services that you are looking to acquire.

There are four or five different classifications of goods and services which consumers are most familiar with in terms of dealing with a loss of purchasing power.

Category 1 – Deflationary goods – These are all the goods like software, electronics, apps, microchips, processors, computer equipment, video, music. Items like generic goods and commodities. These are goods which have been de-materialized and sold on the internet. Often these are goods produced by a robot. They are highly deflationary and fall in price every year as it costs less and less to produce them.

Category 2 – Standard goods – branded consumables, traditional government services. These are generic goods which traditionally go up in price by roughly 1% to 2% per year.

Category 3 – These are luxury products, scarce products, elite education, elite medical services. These items have been going up in price by roughly 6% to 7% every year for the last 30 years. Price an Ivy League Education today and you are looking at $70,000 per year. In 1990 that same education only cost $10,000. The compound rate of inflationary growth has been roughly 7% a year. Gold fits into this category as it has been growing at roughly 6% per year.

Category Four – These are inflationary assets which have been growing between 8% and 24% per year over the last 10 years. They include Bonds (Credit), Stocks, Scarce Art, Luxury Real Estate. If you own them, you have done extremely well in terms of protecting your purchasing power.

Category Five – These are scarcest of all assets. Anyone want to hazard a guess as to what the best performing asset class of all time has been?

The answer is Bitcoin.

Bitcoin is the least understood of all major investments. It is only 11 years old. But in that time frame it has become the 6th largest currency in the world.

88% of all bitcoin have already been mined and it will take another 140 years for the remaining 12% of bitcoin to be created. This is the hardest money in the history of money. Where huge financial uncertainty exists, bitcoin flourishes.

It is the only currency in the world that has a fixed limited supply that cannot change. There will only ever be 21 million bitcoin and 18.5 million have already been created.

Bitcoin is:

Decentralized – it does not have a specific location.

Borderless – without boundaries or restrictions.

Trustless – verification occurs through consensus of all computers on the network, not through a central authority, middleman, personality or political figure.

Value Transfer Network – it transfers value between any two parties anywhere in the world without the permission or interference of any other authority. The amount of time it takes depends on how busy the network is. It can take as long as a day for a transaction to clear and as little as a few seconds.

Currency – a system of money.

Is it possible that the Federal Reserve, and their current negative yield policy is the best and boldest marketing and advertising campaign for Bitcoin?

If you have bonds maturing anywhere between now and 2023 where are you going to place those funds? That is the decision that trillions of bond dollars will have to decide moving forward. This YIELD CHASE will be the driving force behind stocks, gold and bitcoin for the next three years.

The largest hedge fund manager in the world is Ray Dalio of Bridgewater Associates. Mr. Dalio has proclaimed in his speeches that “cash is trash.” If the Fed has decided that their best monetary policy is to debase the U.S. Dollar it would be prudent for you to think about how you position yourself in the markets for the next few years.

I contend that a very large percentage of these bond funds will find their way into bitcoin. As long as Treasury yields are guaranteed negative, the yield chase is almost certain. The greatest threat to bitcoins ascendancy is good government policy. According to Fed Chairman Jerome Powell, we will not see a change in policy till the end of 2023.

So what’s a trader to do?

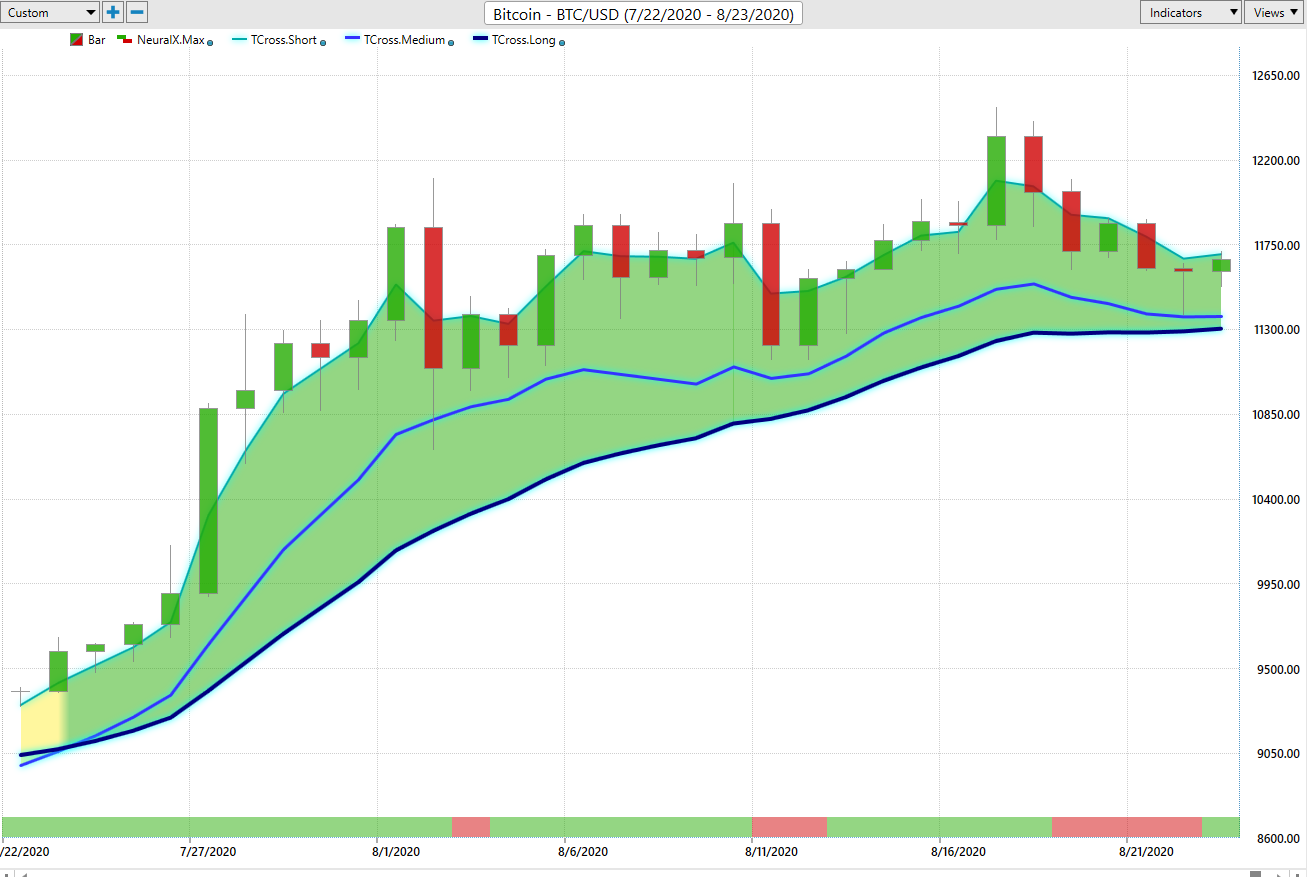

What all traders and investors want is an accurate, proven solution that alerts you when a high probability trend is unfolding. The Vantagepoint A.I. forecasts have proven to be up to 87.4% accurate in determining the trend three days in advance.

Here is a recent chart of Bitcoin with the Vantagepoint a.i. forecast.

What allows for such an accurate forecast? The Vantagepoint software creates these forecasts every day based upon its proprietary Intermarket analysis of what the most 32 statistically correlated stocks, commodities, forex, and other cryptocurrencies have been doing to drive the Bitcoin price.

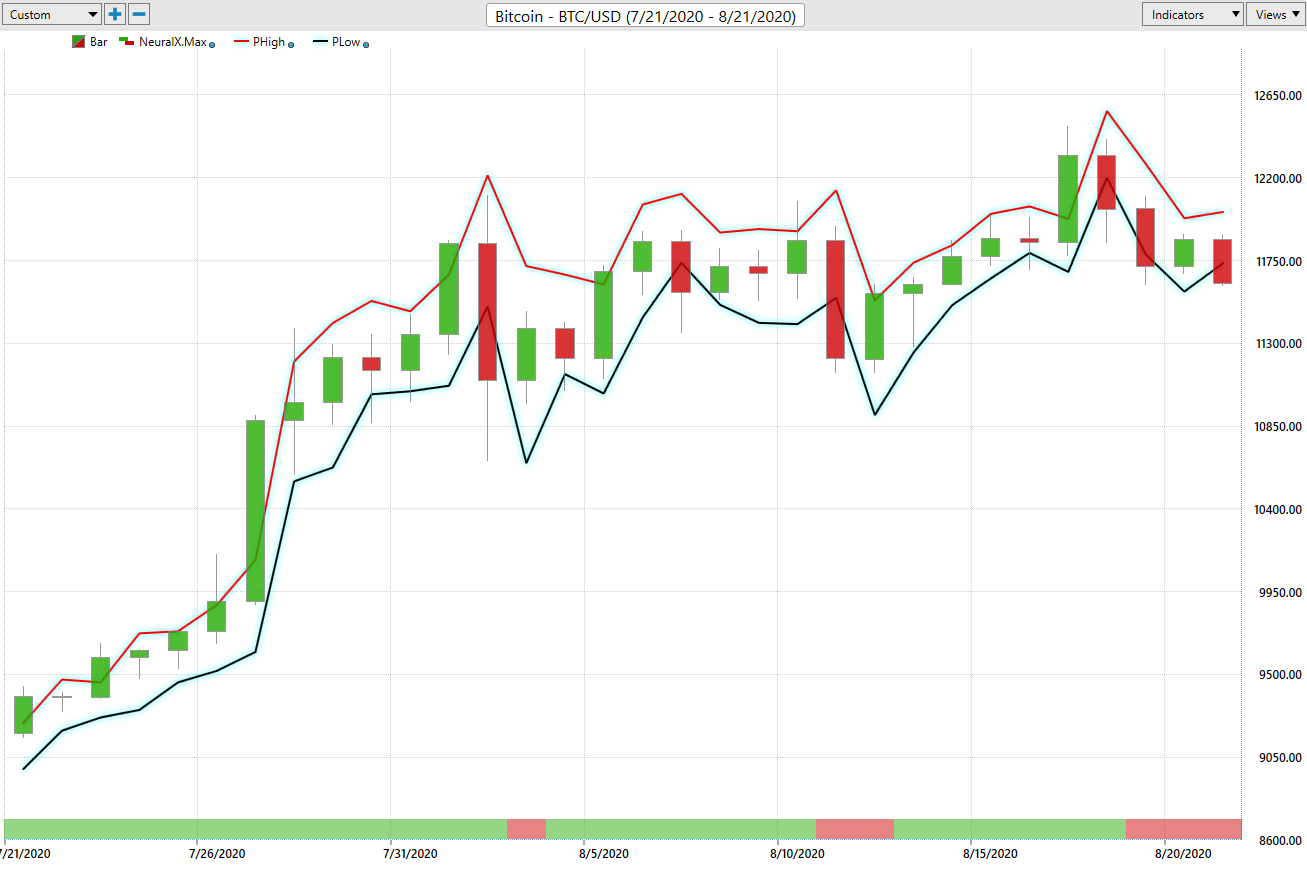

Below is the daily price range forecast from late July till September. I think you’ll understand why swing traders love this as a short term trading solution.

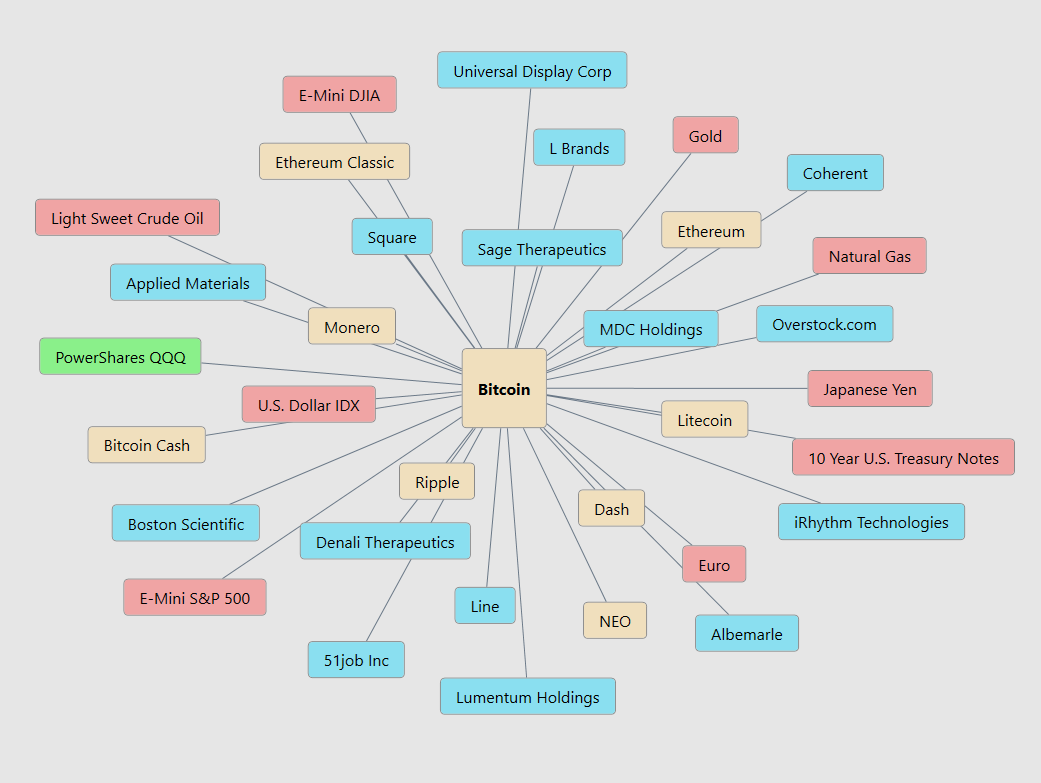

Here is a current snapshot of the Intermarket correlations for Bitcoin:

What’s Your Best Chance To Make Money In The Financial Markets Today?

The Answer A.I. Offers Will Surprise You. Intrigued?

Visit With US and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]