Imagine traveling back in time and asking four billionaire investors about two upcoming IPOs. The first company sells lumber, plywood, and power tools. The second helps college students share photos online. Neither sounds particularly revolutionary. Yet those companies would eventually become Home Depot and Meta; two of the greatest wealth-creating businesses in modern history.

The market has a habit of describing transformational companies by their smallest visible feature. Before Home Depot became Home Depot, it was viewed as a hardware retailer. Before Facebook became Meta, it was viewed as a social media website for college students. Investors who focused only on what these companies were often missed what they were becoming. The biggest fortunes were made by those who recognized the larger opportunity hiding beneath the surface.

Today, many investors describe SpaceX as “just a rocket company.” That may be like describing Home Depot as a lumber yard or Meta as a photo-sharing app. The company’s ambitions extend far beyond launches, touching communications, defense, transportation, satellite internet, and potentially the future of human expansion beyond Earth. Whether those ambitions translate into shareholder returns remains to be seen, but the comparison is worth considering.

When SpaceX comes public, it has become one of the most anticipated IPOs in Wall Street history. Investors will debate the valuation. Analysts will dissect the growth prospects. Financial media will focus on Elon Musk and the spectacle surrounding the offering. Yet the more interesting question may not be whether SpaceX is a good company, but how great investors would evaluate the opportunity.

That is why, in this article, we will do a hypothetical exercise, a potential SpaceX IPO through the eyes of four legendary billionaire investors: Warren Buffett, Paul Tudor Jones, Ray Dalio, and Michael Burry. Not because billionaires are infallible, and certainly not because they always agree. Rather, they became billionaires through an intense commitment to discipline, process, rational decision-making, and calculated risk-taking. Their success came from asking better questions than the crowd and viewing opportunities through unique lenses.

Each of these investors would likely study the same company and reach a very different conclusion. Buffett would focus on economic moats and cash flows. Jones would focus on momentum and capital flows. Dalio would analyze long-term economic and geopolitical cycles, while Burry would search for hidden risks and flawed assumptions. By understanding how each investor thinks, traders can gain valuable insight into how world-class decision-makers and capital allocators approach one of the most anticipated IPOs of our time.

Investors have an unfortunate habit of believing that every exciting IPO will become the next Amazon and every disappointing IPO will become the next Pets.com. Wall Street loves certainty almost as much as it loves charging fees, and both are generally in short supply. The reality is that many of the greatest wealth-creating companies in history looked surprisingly ordinary when they first came public. Meanwhile, some of the most celebrated IPOs arrived with fireworks, confetti, and enough hype to launch a small nation into orbit, only to spend years disappointing shareholders.

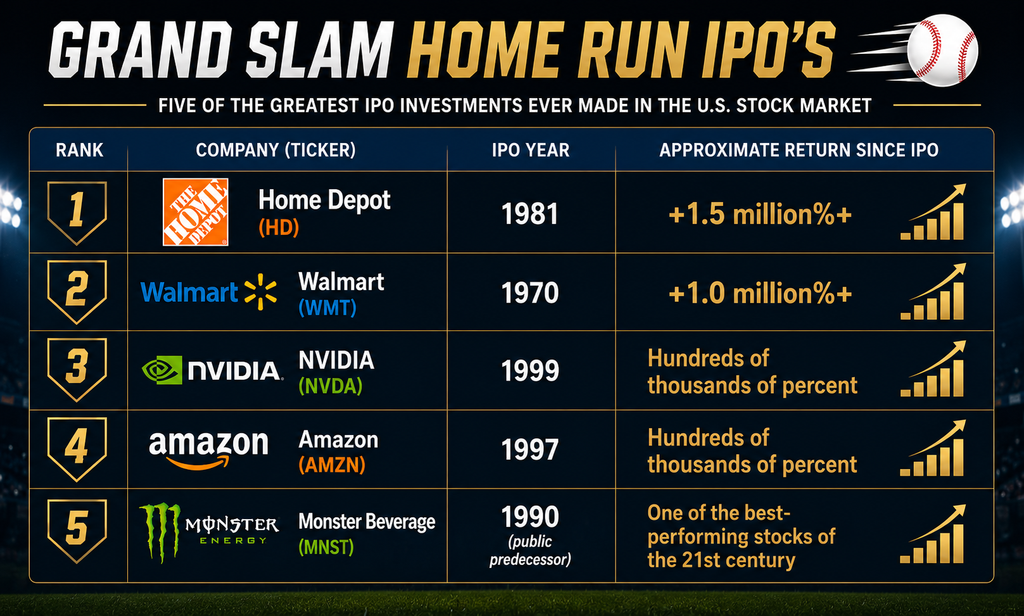

Consider the IPO Hall of Fame. Home Depot sold lumber, power tools, and enough plywood to build a subdivision. Walmart specialized in selling tube socks, fishing tackle, and discounted lawn furniture. NVIDIA made computer chips for gamers, Amazon sold books over the internet, and Monster Beverage sold caffeinated sugar water in oversized cans. None of these businesses sounded like obvious candidates to create hundreds of billions, and in some cases trillions, of dollars in shareholder wealth.

At the time, these companies did not look like legends. They looked like retailers, beverage companies, and niche technology firms. Their greatness only became obvious after years of execution, growth, and relentless expansion. Investors often imagine that extraordinary opportunities arrive wearing a neon sign that says “Future Trillion Dollar Company.” More often they arrive disguised as something far less exciting.

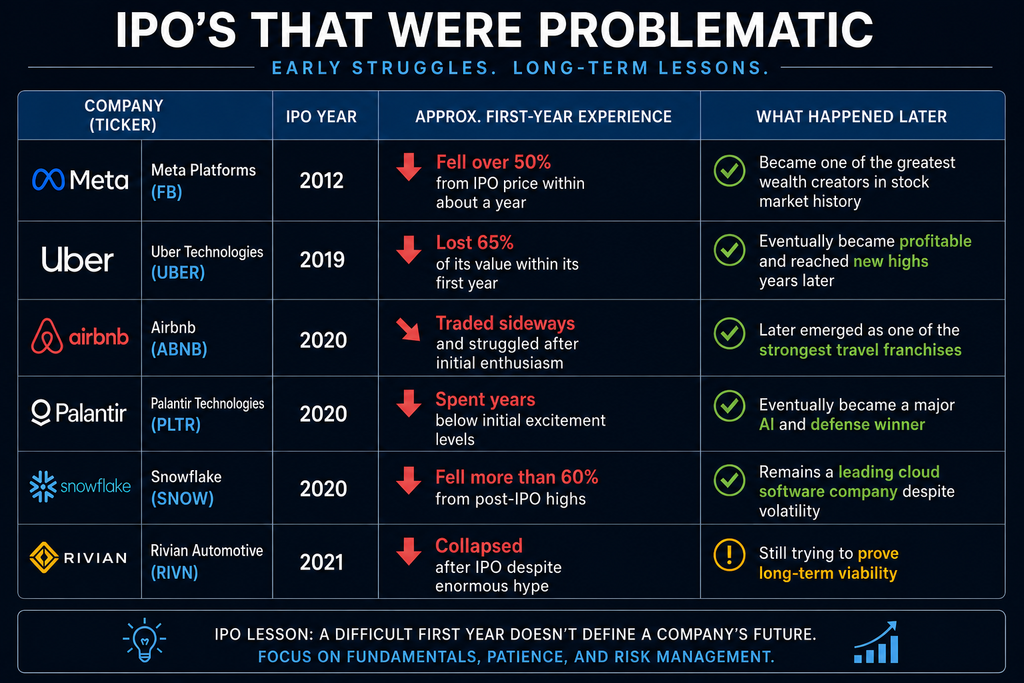

Then there is the IPO Hall of Shame, or perhaps more accurately, the IPO Hall of Temporary Embarrassment. Meta lost more than half its value after coming public and became a favorite target of financial commentators who confidently explained why the company was doomed. Uber lost roughly 65% of its value in its first year, Airbnb struggled after the initial excitement faded, and Palantir spent years testing the patience of even its most devoted shareholders. Snowflake collapsed more than 60% from its highs, while Rivian transformed from Wall Street’s electric vehicle darling into a case study in excessive optimism.

The fascinating thing is that several of these so-called failures eventually became remarkable businesses. Meta became one of the greatest wealth creators in market history. Uber found profitability. Airbnb emerged as a dominant force in travel. Even Palantir eventually rewarded investors who survived the turbulence. The lesson is that a great company and a great stock are not always the same thing, particularly during the first few years after an IPO.

Which brings us to SpaceX, as the company comes public, investors will almost certainly treat it as either the next great opportunity or the next great bubble. Financial television will feature endless debates. Social media will be filled with experts who discovered aerospace engineering approximately thirty minutes earlier. Every price move will be analyzed as proof that somebody’s prediction was correct.

The most useful question is not whether SpaceX will be a successful company. The most useful question is whether it will follow the path of Home Depot, Amazon, and NVIDIA, or whether it will endure the painful post-IPO growing pains experienced by Meta, Uber, and Palantir. History suggests the answer may be both. Some of the greatest investments ever made spent their early years looking like mistakes.

That possibility is exactly why it is worth examining how Buffett, Jones, Dalio, and Burry might evaluate the opportunity. Because while most investors will be asking whether SpaceX is going up tomorrow, billionaires tend to ask a far more important question: what are the odds that this becomes one of the great wealth-creating businesses of the next twenty years?

Every generation gets one company that seems impossible to value.

For Baby Boomers, it was Home Depot.

For Millennials, it was Meta.

For today’s investors, it may be SpaceX.

Home Depot didn’t just sell tools. It reinvented retail.

Meta didn’t just connect friends. It rewired global communication.

SpaceX isn’t trying to build a better rocket.

It’s attempting to build the transportation and communications backbone for the next century.

That distinction could make all the difference.

Wall Street is staring at the SpaceX IPO the way a Labrador retriever stares at a dropped steak. Tongue hanging out. Eyes locked in. Convinced destiny has delivered dinner. And who can blame them? This isn’t some sleepy utility company raising capital to replace power lines. This is SpaceX. Rockets. Satellites. Mars. Elon Musk. The closest thing modern capitalism has to a superhero franchise that happens to launch payloads into orbit.

The excitement is understandable. The problem is that excitement isn’t analysis. What makes the SpaceX IPO so fascinating is something my friends and I talk about constantly. There are zero data points and millions of opinions. Everyone has a guess. Everyone has a target price. Everyone has a story. Almost nobody has actual evidence.

Think about what you don’t know. You don’t know how institutions will position themselves once trading begins. You don’t know how much volatility will show up in the first few weeks. You don’t know how aggressively early investors want liquidity. You don’t know how much stock insiders will ultimately be allowed to sell. You don’t know what future earnings growth will look like as a public company. You don’t know whether Wall Street’s expectations are too high, too low, or completely detached from reality.

Then there are the lockup provisions. Most investors never read them. Smart investors obsess over them. Lockups prevent founders, executives, employees, and early investors from immediately selling shares after the IPO. The reason is obvious. If everyone heads for the exits on Day One, gravity tends to make a dramatic reappearance. Yet until those provisions are fully understood, nobody really knows how much potential selling pressure could be waiting in the shadows.

Everybody is talking about how high SpaceX might go. Almost nobody is asking what happens after everybody gets what they wanted. A company valued somewhere around two trillion dollars may soon enter public markets. The public sees an opportunity to buy the future. The insiders see an opportunity to monetize the past. Those are very different investment objectives.

An enormous amount of paper wealth is preparing to become spendable wealth. The moment liquidity arrives, human nature arrives with it. Venture capitalists suddenly become interested in beachfront property. Early employees discover that twenty years in front of a laptop should probably result in a larger boat. Founders who spent decades living on cold pizza begin comparing private aviation options. Nobody has to sell everything. They only have to sell enough.

Enough to diversify. Enough to exercise options. Enough to buy the yacht. Enough to create selling pressure that wasn’t there yesterday. Enough to remind late-arriving investors that whenever someone is buying a dream, someone else may be selling one. That’s not cynicism. That’s how markets work.

The crowd will watch headlines. Smart money will watch liquidity. The crowd will celebrate every new all-time high. Smart money will be reading lockup agreements, monitoring secondary offerings, and tracking who is quietly converting stock certificates into cash. Because markets, like politics, are rarely about what people say. They’re about what people do when large sums of money are involved.

History has a funny way of humbling investors who believe a great company automatically guarantees a great stock. Many of the best businesses in history delivered disappointing IPO experiences. Some struggled for months. Some struggled for years. A great company and a great investment are not the same thing. The difference is price.

Amazon spent years going nowhere while critics mocked the business. Meta stumbled badly after its IPO. Numerous technology darlings have delivered painful early experiences before eventually rewarding patient investors. The lesson isn’t that great companies fail. The lesson is that the market often takes time to discover what something is truly worth.

That’s why Warren Buffett’s observation matters more than ever: “Price is what you pay. Value is what you get.” The value of SpaceX will not be determined on opening day. It won’tbe determined during the first week. It may not be determined for many months. Yet millions of investors are already speaking about its future value with astonishing certainty.

What fascinates me isn’t SpaceX itself. SpaceX will probably be an amazing company. What fascinates me is watching millions of opinions masquerade as data points. Every forecast sounds scientific. Every valuation model sounds authoritative. Every television expert suddenly becomes a prophet. Yet nobody possesses the one thing traders should care about most: actual trading data.

Let me be clear. I’m not telling you to participate in the SpaceX IPO. I’m not telling you to avoid it. These articles are never financial advice. I’m telling you that, at this moment, there are far more opinions than facts. In the absence of meaningful trading data, there are only a few things we know with certainty.

Elon Musk is going to get paid. The early investors are going to get paid. The underwriting syndicate is going to get paid. Beyond that, everything else is speculation wrapped inside slide presentations, television interviews, and social media certainty.

Traders should remember an important lesson from market history. You did not have to buy Walmart on the day it went public in 1970 to eventually make a fortune. You did not have to buy Home Depot in its first week of trading to participate in one of the greatest wealth-creation stories in American business. There was plenty of opportunity after the data proved the story.

The market doesn’t hand out trophies for being first. It rewards investors who identify durable trends and stay with them. That’s a completely different game. The objective isn’t to win the race to buy. The objective is to make money.

At VantagePoint AI, we’re in the market forecasting and data business. Our goal isn’t to predict what a stock might do out of thin air. Our goal is to help traders stay on the right side of the right trend at the right time once the market begins revealing its intentions. We focus on the data instead of narratives, global analysis instead of the fishbowl, price action instead of press releases, and market reality instead of market mythology.

When SpaceX finally begins trading, we’ll be watching closely. We’ll be watching the data. Because sooner or later every great story becomes a chart, and every chart eventually reveals the truth.

The first year of Facebook’s IPO was not the triumphant coronation that Wall Street had imagined. It was something far more instructive. The stock arrived in May 2012 at the much-publicized $38 offering price, carrying a valuation north of $100 billion and the weight of Silicon Valley’s biggest expectations. Then reality intervened. Within months, investors who believed they were buying the future watched the shares lose more than half their value, bottoming near $18 as doubts swirled about mobile monetization, growth, and whether the world’s largest social network could ever justify its extraordinary price tag. Yet the most remarkable feature of this chart is not the collapse, it is the recovery. By the summer of 2013, Facebook had clawed its way back above the IPO price, proving a lesson that markets teach repeatedly but investors rarely learn: the public offering is often the beginning of the story, not the end, not the verdict. The first year of Facebook trading was a masterclass in the difference between a great stock and a great company. For those willing to look beyond the headlines, it was also an early glimpse of one of the most successful business franchises ever built.

Uber’s 2019 IPO arrived with enormous fanfare, only to see investors quickly sour on mounting losses, regulatory uncertainty, and concerns about the path to profitability. The company’s eventual turnaround served as a reminder that Wall Street often rewards execution over narratives, as Uber evolved from a cash-burning disruptor into a profitable platform business.

Palantir’s public debut generated enormous enthusiasm among investors captivated by its unique role at the intersection of data analytics, government intelligence, and national security. Yet years of uneven performance tested shareholder patience before the company’s growing relevance in artificial intelligence and defense spending reignited investor interest.

When SpaceX comes public, much of Television commentators will debate price targets. Social media influencers will calculate how quickly the stock can double. Retail investors will worry about missing the next great opportunity. Warren Buffett, however, would likely start somewhere else entirely…

For decades, Buffett has approached investing with a deceptively simple framework. Before asking how much money he can make, he asks how much money he can lose. Before becoming excited about a company, he wants to understand the business. Before considering the upside, he studies the downside. It is a discipline that sounds almost boring in an era dominated by hype, but it has helped transform Berkshire Hathaway into one of the greatest wealth-creation vehicles in history.

If Buffett were evaluating a SpaceX IPO, he would not begin by asking whether rockets represent the future. He would ask whether the company possesses a durable competitive advantage. Does SpaceX have a moat that competitors cannot easily cross? Does it generate recurring cash flows through businesses like Starlink? Can management continue allocating capital effectively as the company grows? Most importantly, what price provides an adequate margin of safety?

These questions may not generate viral social media posts, but they get to the heart of what separates investing from speculation. Buffett understands that even extraordinary businesses can become poor investments when purchased at extraordinary prices. History is littered with examples of investors who correctly identified a great company but paid so much for it that their returns were mediocre.

For traders, this lesson is particularly important because position sizing is often overshadowed by stock selection. Investors spend countless hours searching for the next Home Depot, Amazon, or NVIDIA. Far fewer spend time determining how much capital should be committed to the opportunity. Yet the size of a position frequently has a greater impact on long-term performance than the stock itself.

The temptation surrounding a SpaceX IPO will be obvious. The company has a visionary founder, a dominant market position, and a story that captures the imagination. Those characteristics can create tremendous opportunity. They can also create excessive enthusiasm. Buffett’s approach serves as a useful reminder that successful investing is not about maximizing excitement. It is about balancing opportunity against risk.

That is why Buffett’s most famous investing principle remains so relevant today: “The first rule of investing is don’t lose money.” The quote is often repeated but rarely appreciated. Buffett understands that preserving capital creates flexibility. Flexibility creates opportunity. And opportunity is what ultimately produces extraordinary returns.

The lesson for traders is straightforward. Before asking how high SpaceX might go, ask how much capital deserves to be allocated to the opportunity. Excitement is not a strategy. Discipline is. Buffett’s fortune was built not by predicting every outcome correctly, but by consistently placing capital where the odds were favorable and the risks were manageable.

If Warren Buffett begins by asking whether a business is worth owning, Paul Tudor Jones begins by asking whether the market agrees. That may sound simplistic, but it reflects one of the most important lessons in trading. Markets are voting machines every day and weighing machines over time. Jones understands that price is not merely a number. Price is information.

When SpaceX comes public, there will be no shortage of opinions. Elon Musk will have an opinion. Wall Street analysts will have opinions. Financial television will have opinions twenty-four hours a day. Social media will produce enough opinions to power a small city. The challenge for traders is that opinions are abundant, free, and frequently wrong.

Jones built his fortune by focusing on something much more important: performance. He wants to know where money is flowing. Is the stock outperforming the S&P 500? Is it outperforming its peers? Are institutions accumulating shares? Is relative strength improving? Is momentum accelerating? These are the questions that capture his attention because they reveal what investors are doing rather than what they are saying.

This distinction matters because markets have a way of exposing the difference between a compelling story and a winning investment. History is full of companies that sounded revolutionary but never rewarded shareholders. History is also full of companies that looked ordinary on the surface yet quietly delivered extraordinary returns. The scoreboard ultimately settles every debate.

Imagine SpaceX rallies 100% after its IPO. Most investors would celebrate the story. Jones would study the buying pressure. Imagine the stock doubles and then continues outperforming the broader market for months. That would tell him something important. Capital is voting with conviction. The market is sending a signal that deserves attention.

Now imagine the opposite scenario. SpaceX debuts to enormous fanfare, dominates headlines, and becomes the most discussed stock in America. Six months later, however, it is underperforming the S&P 500, lagging its peers, and struggling to attract institutional demand. Jones would not care how exciting the story sounds. He would care that the market is delivering a very different verdict.

For traders, this may be the most practical lesson in the entire article. The most important opinion about SpaceX will not come from Elon Musk. It will not come from Wall Street analysts. It will not come from financial journalists or social media influencers. It will come from the stock itself.

That philosophy aligns perfectly with a simple truth that many traders overlook. Strong stocks tend to outperform before the crowd fully understands why. Money flows toward strength long before the headlines explain it. The traders who learn to follow performance instead of predictions often find themselves on the right side of the market at the right time.

Paul Tudor Jones understands something that every successful trader eventually discovers. The market is under no obligation to agree with your opinion. Your job is not to tell the market what should happen. Your job is to listen carefully to what the market is already saying and position yourself accordingly.

One of the easiest mistakes investors make is confusing a company with its product. Investors thought Amazon sold books. They thought Meta connected friends. They thought NVIDIA made graphics cards for video gamers. In each case, the market initially focused on what the company did rather than the larger economic system it was quietly becoming part of.

That distinction would almost certainly capture Ray Dalio’s attention if SpaceX came public. Dalio has spent his career studying systems, cycles, and the forces that shape economies over decades. He would not begin by asking how many rockets SpaceX launched last quarter. He would begin by asking a far more consequential question: What problem does SpaceX solve that the world cannot afford to ignore?

The answer extends far beyond rockets. SpaceX sits at the intersection of communications, national security, defense spending, artificial intelligence, satellite infrastructure, and global connectivity. Starlink alone is reshaping how governments, businesses, and consumers access information. The company’s launch capabilities are increasingly becoming part of the strategic infrastructure of the United States and its allies.

Viewed through that lens, SpaceX starts to look less like a technology company and more like a platform. Investors often talk about platforms because they create powerful network effects and long runways for growth. Railroads were platforms. The interstate highway system was a platform. The internet became a platform. The question Dalio would likely ask is whether SpaceX is building the next layer of global infrastructure.

This matters because some of the largest wealth-creating opportunities in history emerged when multiple trends converged at the same time. Home Depot benefited from demographic growth, suburban expansion, and homeownership. Amazon rode the rise of e-commerce, cloud computing, and digital payments. NVIDIA found itself at the center of gaming, data centers, artificial intelligence, and autonomous systems. The biggest winners often succeed because they are connected to several powerful forces simultaneously.

SpaceX appears to occupy a similar position. Governments want secure communications. Militaries want resilient satellite networks. Businesses want global connectivity. Artificial intelligence requires ever-expanding infrastructure. Meanwhile, geopolitical competition between the United States and China continues to intensify. Each trend creates demand for capabilities that SpaceX already possesses.

For traders, the lesson is simple. Great opportunities often reveal themselves long before they appear in earnings estimates. They emerge when a company finds itself aligned with powerful forces that are likely to persist for years. Price action matters. Relative strength matters. But understanding the larger trend can help explain why certain companies continue outperforming long after the crowd believes the move is over.

Dalio often reminds investors that understanding the machine is more important than predicting the next headline. If SpaceX eventually becomes one of the defining companies of the next generation, it may not be because it launches rockets more efficiently than its competitors. It may be because it occupies a critical position within several of the most important economic, technological, and geopolitical trends of the twenty-first century.

That is the type of question Ray Dalio would be asking. Not whether SpaceX can go higher next quarter. Whether the company is becoming indispensable to the future.

Let’s get something out of the way.

When SpaceX comes public, there won’t be a shortage of cheerleaders.

Wall Street will love it. Financial television will obsess over it. Social media will crown it the greatest investment opportunity since Amazon. Every commentator with a microphone will explain why the future belongs to rockets, satellites, Mars colonies, and whatever Elon Musk tweeted five minutes ago.

And that’s exactly when Michael Burry starts getting nervous.

Burry has built a career doing something most investors hate: looking for reasons why the crowd might be wrong. While everyone else is admiring the shiny new sports car, he’s underneath it checking for loose bolts. While the market is celebrating, he’s asking uncomfortable questions. While investors are dreaming about becoming rich, he’s trying to figure out what could cause them to lose money.

That mindset made him famous during the housing bubble. While nearly everyone on Wall Street was convinced housing prices could only go up, Burry sat alone in a room studying mortgage documents and discovering things nobody else wanted to see. He wasn’t looking for confirmation. He was looking for contradictions.

Burry’s first question won’t be, “How high can this stock go?”

His first question will be, “What assumptions are already baked into the price?”

That question matters because great companies and great investments are not the same thing.

A company can be extraordinary. But a stock can still be terrible.

Investors learned this lesson with Meta. They learned it with Uber. They learned it with Snowflake. In every case, the business survived. In some cases, the business thrived. But investors who paid too much discovered that being right about the company is not enough.

You also have to be right about the price.

Burry would likely ask questions that few investors want to consider.

What if growth slows?

What if competition emerges?

What if government contracts become less profitable?

What if Starlink’s economics fail to match investor expectations?

What if the valuation already assumes twenty years of success?

None of these questions make for exciting television. Nobody gets invited onto a podcast to discuss reasonable expectations. The crowd wants optimism. The crowd wants certainty. The crowd wants a simple story.

Markets rarely work that way.

For traders, this may be the most valuable lesson of all. The biggest risks are usually the ones nobody is discussing. The greatest danger often appears when everyone agrees. Whenever an investment seems universally loved, it is worth asking what could possibly go wrong.

That doesn’t mean SpaceX will fail. Far from it.

Burry might ultimately conclude that SpaceX is one of the most important companies in the world. But before he commits a single dollar, he will search relentlessly for the flaw. And that’s the lesson.

The goal is to become impossible to surprise.

Because when everyone else is looking at the opportunity, the smartest investors are often looking for the risk.

And sometimes, that difference is worth billions.

What makes the exercise of examining SpaceX through the eyes of Warren Buffett, Paul Tudor Jones, Ray Dalio, and Michael Burry so valuable is not that it provides an answer. It doesn’t. In fact, there is a very good chance that all four investors would arrive at different conclusions. Buffett might focus on the moat. Jones might focus on the momentum. Dalio might focus on the macroeconomic implications, while Burry searches relentlessly for hidden risks.

Yet beneath those differences lies a common thread. None of these investors became billionaires by chasing headlines or reacting to the latest narrative. They built extraordinary fortunes by following disciplined processes, managing risk, allocating capital intelligently, and remaining willing to change their minds when the facts changed. Their success was rooted in process.

History offers a useful reminder. Home Depot did not look like one of the greatest investments of all time when it came public. Amazon looked like an online bookstore. Meta was dismissed by many investors after losing more than half its value following its IPO. Uber spent years proving that a great company and a great stock are not always the same thing. In each case, the market’s first verdict turned out to be incomplete.

That may ultimately be the most important lesson for traders. The biggest opportunities rarely arrive with universal agreement. They rarely look obvious in real time. More often, they emerge through uncertainty, skepticism, volatility, and a long process of proving themselves to the market. The companies that eventually reshape industries are often misunderstood before they are understood.

Whether SpaceX becomes the next Home Depot, the next Amazon, or simply another fascinating chapter in Wall Street history remains to be seen. But traders would be wise to remember that the market’s first opinion is often its least informed one. The real opportunity is not in knowing the answer before everyone else. It is asking better questions than everyone else while the story is still being written.

As we have explored throughout this article, Warren Buffett, Paul Tudor Jones, Ray Dalio, and Michael Burry would almost certainly arrive at different conclusions about a SpaceX IPO. Yet all four investors share a common trait: they understand that successful trading is not about certainty. It is about defining, measuring, and managing opportunity and risk better than the rest of the crowd.

That philosophy lies at the heart of everything we do at VantagePoint AI. Markets are constantly changing. New opportunities emerge. New risks appear. Trends strengthen, weaken, and sometimes reverse with remarkable speed. Our objective is not to predict every headline or every market-moving event. Our objective is to help traders stay on the right side of the right trend at the right time.

When SpaceX goes public, we will be watching closely. Like every market we track, we will collect the data, monitor the price action, evaluate the intermarket relationships, and test our predictive models. We do not add markets to the VantagePoint AI forecasting database simply because they are popular or because investors are excited about them. We add them when our artificial intelligence has demonstrated a proven ability to forecast future price direction with a minimum accuracy threshold of 70%. Until then, we will continue to track and evaluate the opportunity with the same discipline that guides every decision we make.

That discipline has never been more important than it is today. Traders have spent much of this year navigating a market environment characterized by uncertainty, volatility, rapidly shifting narratives, and powerful crosscurrents between sectors, asset classes, and global markets.

VantagePoint AI was specifically designed for environments like these. By analyzing thousands of intermarket relationships every day, our artificial intelligence helps traders identify emerging opportunities, anticipate trend changes, recognize relative strength, improve market timing, and make decisions based on data rather than emotion.

The truth is that the future belongs to traders who can adapt faster than the crowd. VantagePoint’s artificial intelligence trading software offers a powerful advantage by helping traders see what traditional analysis often misses. If you would like to see exactly how VantagePoint AI identifies opportunities, measures risk, and helps traders stay aligned with the strongest trends in the marketplace, we invite you to attend a Free Live Online Masterclass. You will see the technology in action, learn how professional traders are using AI in today’s markets, and discover how VantagePoint AI can help you make more confident trading decisions in any market environment.

Let’s Be Careful Out There!

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.