The stock market does not climb a wall of certainty. If it did, every investor in America would already own three yachts, two senators, and a vacation home in Aspen. Markets do not rise because people feel safe. They rise because human beings are perpetually convinced civilization is one bad headline away from eating canned beans in a candlelit basement while listening to emergency radio broadcasts.

It climbs a wall of worry.

And Americans, in particular, have elevated worrying into a kind of Olympic sport. In the 1980s, we were convinced inflation would destroy the dollar, the Russians would vaporize Cleveland, and Japan would buy everything west of Nevada. In the early 2000s, the internet was supposedly a fraud, terrorism was going to permanently cripple capitalism, and every CEO in America appeared to be cooking the books with a blowtorch and a tequila hangover. In 2008, the global financial system looked like a raccoon held together with duct tape and unpaid mortgage applications. Today the fears are different, but the melody remains the same: artificial intelligence will take your job, the national debt will collapse the currency, geopolitical tensions will ignite the planet, and somewhere a man on YouTube is explaining why the entire banking system will implode next Tuesday around lunchtime.

Every generation believes its fears are uniquely catastrophic while dramatically underestimating capitalism’s almost supernatural ability to adapt, innovate, improvise, and occasionally sprint away from disaster.

That is the real lesson of the wall of worry.

The wall is never removed. Only renovated.

The fascinating thing is that investors always believe the current wall is finally too high. This time the deficits are too large. This time the technology is too disruptive. This time the war is too dangerous. This time the political system is too broken. And yet markets keep grinding higher over time, not because problems disappear, but because businesses adapt, technology evolves, productivity improves, governments panic and intervene, and capital relentlessly searches for opportunity like a pig hunting truffles.

The stock market is essentially a giant forward-looking discount machine trying to price both catastrophe and recovery at the exact same time. Which is why the headlines always sound terrible right before markets do something wildly inconvenient to the pessimists.

Of course there is another, more cynical explanation for why markets keep climbing the wall of worry, and it arrives wearing a tailored suit, carrying a PhD in economics, and standing next to something the Federal Reserve politely refers to as “liquidity facilities.” Ordinary people call it a printing press.

This is the part polite financial television usually avoids discussing because it sounds suspiciously like the sort of thing muttered by a man building a bunker out of canned soup and shortwave radios. But history is awkward that way. Over long periods of time, governments have displayed an almost irresistible temptation to solve debt problems, recession problems, banking problems, war problems, pension problems, and occasionally political problems by creating more currency units. Not because they are evil masterminds stroking white cats in underground volcanoes, but because printing money is politically easier than telling voters they cannot have twelve different government programs, three wars, subsidized mortgages, artificially low interest rates, and infinite economic growth simultaneously.

And once you understand that, an uncomfortable realization begins creeping across the room like a raccoon in a hotel hallway. Maybe asset prices are not only rising because capitalism adapts and innovates. Maybe they are also rising because the measuring stick itself keeps shrinking. If you continuously create more dollars, then stocks, real estate, gold, commodities, baseball cards, and occasionally ridiculous digital monkey pictures tend to rise in dollar terms over time. Not necessarily because the asset became infinitely more valuable, but because the currency measuring the asset quietly became less scarce.

Naturally, saying this out loud in respectable company is treated somewhere between impolite and mildly radioactive. The official narrative is that monetary authorities are simply “supporting stability,” “enhancing liquidity,” or “stimulating economic activity,” which sounds much better than saying, “We are manufacturing trillions of additional currency units because the alternative might involve riots and congressional hearings.”

Yet, history repeatedly shows governments debasing currencies during periods of excessive debt, war, or economic stress. Ancient Rome clipped coins. European monarchs diluted precious metals. Modern central banks use keyboards instead of melting pots, but the basic magic trick remains remarkably similar.

The fascinating part is that both perspectives can be true at the same time. Markets climb because human beings innovate, build businesses, improve productivity, and create real economic value. But markets may also climb because monetary authorities steadily increase the supply of currency chasing those assets. One explanation celebrates capitalism’s resilience. The other quietly questions the integrity of the measuring tape itself.

And perhaps that is the ultimate wall of worry for modern investors. Not simply whether stocks can rise, but whether the currency used to measure wealth is slowly melting like an ice cube left on the hood of a Buick in August.

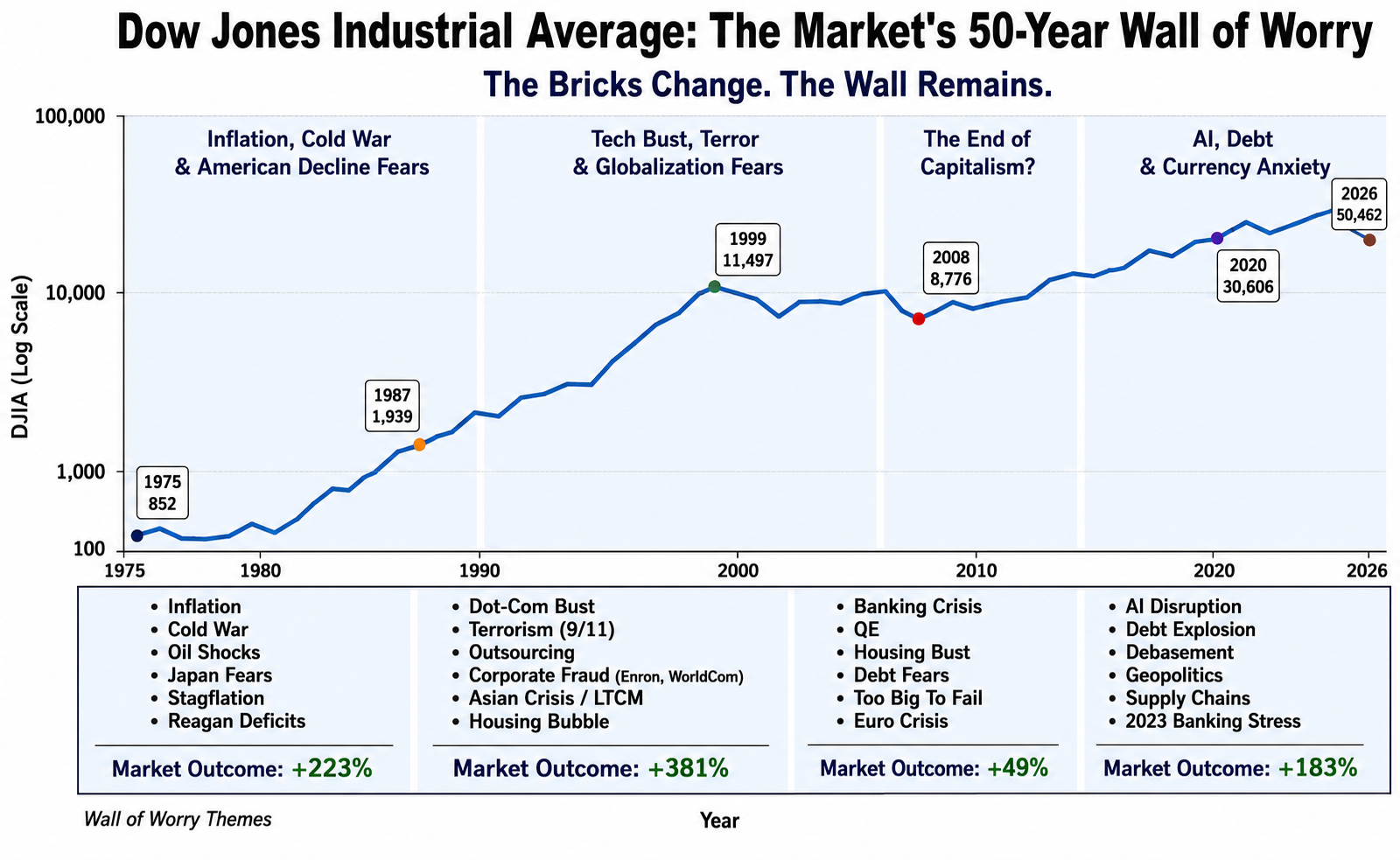

The 1980s: Inflation, Nuclear Fear, and America in Decline

The 1980s did not begin with optimism. They began with exhaustion. Inflation had ravaged the economy throughout the 1970s. Interest rates were painfully high. Mortgage rates pushed into the teens. Oil shocks had crushed consumer confidence. The Cold War dominated the headlines, and there was a very real fear that the United States and the Soviet Union could stumble into a nuclear confrontation at any moment. Americans were told Japan was buying everything, manufacturing everything better, and economically outperforming the United States at every turn. It genuinely felt to many people like America’s best days were behind it.

Then came Paul Volcker and the Federal Reserve. Interest rates were pushed aggressively higher to break inflation. It worked, but it came at a brutal cost. Recessions hit. Unemployment surged. Businesses struggled. Farmers protested. Markets became wildly volatile. And just when confidence started returning, the market crashed in 1987. On Black Monday the Dow Jones Industrial Average collapsed more than 22% in a single day. Investors thought the system itself might be breaking apart. Once again, the wall of worry looked too high to climb.

But something else was quietly happening underneath all the fear. Productivity was improving. Technology was advancing. Personal computers were beginning to spread into homes and offices. Capitalism was adapting the way it always does. Companies became leaner. Innovation accelerated. New industries emerged. And despite all the fear surrounding inflation, deficits, war, and economic decline, the market eventually launched into one of the most powerful long-term bull runs in modern history.

That is what makes the wall of worry so fascinating. The headlines in the moment always feel overwhelming. The fears always feel permanent. Yet markets have a tendency to look beyond current panic and focus on future opportunity. Investors in the 1980s saw inflation, nuclear tension, and economic decline. The market eventually saw productivity, innovation, and growth. Both existed at the same time. But one mattered more over the long run.

The Early 2000s: Dot-Com Collapse, Terrorism, and Corporate Fraud

The early 2000s felt like a financial bar fight after the lights came on.

The dot-com bubble had just exploded. Billions vanished. Tech stocks that had been treated like royalty got dragged into the alley and beaten with a shovel. Companies with no earnings, no business model, and occasionally no actual product disappeared almost overnight. Investors who thought they were geniuses in 1999 suddenly discovered they had been confusing a bull market with intelligence.

Then things got worse.

Enron blew up. WorldCom blew up. Corporate America suddenly looked less like a beacon of capitalism and more like a Vegas blackjack table run by guys named Vinny and “The Accountant.” Trust evaporated. Investors began wondering if any financial statement could be believed. And just as the market was trying to regain its footing, 9/11 happened. Fear consumed the country. Markets closed. Airlines collapsed. War followed. Afghanistan. Iraq. Terror alerts. Cable news pumping anxiety into living rooms 24 hours a day.

The wall of worry looked enormous.

People genuinely believed America was entering a long period of decline. Technology was considered toxic. The internet was supposedly over-hyped nonsense. Outsourcing fears exploded. China’s rise terrified manufacturers and workers alike. Every conversation seemed to end with someone saying, “Things are never going back to normal.”

But here is what the market quietly understood while the headlines screamed panic.

The internet was not dying.

It was growing up.

Underneath the wreckage, real companies were emerging. Amazon survived. Google arrived. Apple reinvented itself. Broadband expanded. Mobile computing exploded. The infrastructure built during the dot-com mania eventually became the foundation for an entirely new digital economy.

That is how the wall of worry works.

The public sees collapse.

The market looks for survivors.

The public focuses on pain.

Capital searches for opportunity.

And the same technology sector investors mocked, feared, and abandoned after the crash eventually became one of the greatest wealth-creation machines in financial history.

The Great Financial Crisis of 2008: The End of Capitalism?

The financial crisis of 2008 was not merely another recession or another painful bear market. For a brief and unsettling moment, it appeared the modern financial system itself might genuinely fracture under the weight of excessive leverage, opaque derivatives, reckless lending practices, and a dangerous assumption that housing prices could never decline nationally. Wall Street, Washington, central banks, hedge funds, and ordinary investors all discovered simultaneously that the intricate machinery underpinning global finance was far more fragile than anyone had imagined.

What made the period uniquely terrifying was the speed at which confidence evaporated. Bear Stearns collapsed. Lehman Brothers failed. AIG required a government rescue. Credit markets froze. Major financial institutions stopped trusting one another enough to lend overnight capital. The phrase “too big to fail” entered the mainstream vocabulary almost overnight. Television screens became dominated by images of traders staring blankly at collapsing markets while policymakers rushed between emergency meetings attempting to prevent a full-scale systemic panic. For many investors, this was no longer about stock prices. It was about whether ATMs would function, whether banks were solvent, and whether capitalism itself had reached a breaking point.

At the same time, the public mood turned deeply skeptical of both Wall Street and government institutions. Americans watched as taxpayers funded massive bailouts for financial firms that many believed had created the crisis in the first place. Unemployment surged. Foreclosures spread across the country. Retirement portfolios were devastated. And in Europe, a sovereign debt crisis soon emerged, raising fears that the instability could spread globally. The wall of worry was no longer theoretical. It was visceral, personal, and immediate.

Yet underneath the panic, policymakers responded with extraordinary force. The Federal Reserve slashed interest rates to historic lows. Quantitative easing entered the financial lexicon. Liquidity flooded the system. Governments coordinated rescue efforts on a scale rarely seen in modern history. Critics warned these policies would debase currencies, inflate asset bubbles, and encourage future risk-taking. Supporters argued they were necessary to prevent economic collapse. In many ways, both sides were correct.

What followed was one of the most remarkable market recoveries in history. Technology companies accelerated their dominance. Cheap capital fueled innovation, acquisitions, and financial engineering. Asset prices surged. Equities entered a bull market that would last more than a decade. Ironically, the very policies implemented to stabilize the financial system became a powerful driver of rising asset prices across stocks, real estate, and alternative assets.

That may be one of the most important lessons from the financial crisis and the wall of worry itself. Markets do not require perfect conditions to recover. They require adaptation, liquidity, and time. In 2008, investors saw the possible end of capitalism. The market eventually saw an entirely new cycle of monetary stimulus, technological acceleration, and capital formation. Both realities existed simultaneously. But once again, the market focused less on present fear and more on future possibilities.

Today’s Wall of Worry: AI, Debt, Currency Debasement, and Global Fragmentation

Today’s wall of worry may be the most complex and politically charged wall investors have faced in generations. Unlike previous eras where fear centered around one dominant crisis, modern investors are confronting multiple fault lines simultaneously. Massive sovereign debt. Persistent inflation. Artificial intelligence disrupting entire industries. Geopolitical instability stretching from the Middle East to Eastern Europe to the South China Sea. A fractured global supply chain. Political polarization. Declining trust in institutions. And perhaps most importantly, growing concern over the long-term stability of fiat currencies themselves.

At the center of this debate sits the modern central bank. Over the last two decades, monetary authorities around the world have repeatedly responded to economic slowdowns, financial crises, and systemic instability with aggressive liquidity injections and expanding money supply. Critics argue this has fundamentally altered markets by artificially inflating asset prices while steadily eroding purchasing power for ordinary citizens. Supporters insist these policies prevented depression-level economic collapse and stabilized the global financial system. Once again, both perspectives contain truth. But regardless of where one stands politically or economically, investors cannot ignore the reality that more currency units chasing a finite pool of assets has historically created upward pressure on stocks, real estate, commodities, and alternative assets.

At the same time, artificial intelligence has emerged as both an extraordinary opportunity and a major source of fear. Entire industries are now confronting the possibility of automation on a scale previously unimaginable. Investors are simultaneously excited by the productivity gains AI may create while fearing the disruption it may unleash across labor markets, corporate structures, and even national security. Semiconductors, data centers, cybersecurity, and advanced computing infrastructure have rapidly transformed from ordinary technology investments into strategic geopolitical assets. Modern warfare itself increasingly depends upon silicon, software, communications systems, surveillance platforms, and artificial intelligence. Capital has recognized this reality quickly, which helps explain why technology and semiconductor stocks have become major leadership groups despite widespread economic anxiety.

Meanwhile, the global economy itself appears to be fragmenting. The era of frictionless globalization is giving way to strategic reshoring, resource nationalism, tariff disputes, energy insecurity, and growing competition between major world powers. Investors are now forced to consider risks that previous generations rarely contemplated simultaneously: debt instability, currency debasement, supply chain vulnerability, cyber warfare, demographic decline, and geopolitical conflict. The sheer volume of uncertainty creates the impression that the system itself is becoming increasingly unstable.

And yet markets continue climbing.

That does not mean the fears are imaginary. Many of them are entirely legitimate. Debt levels are historically extreme. Monetary expansion has been extraordinary. Geopolitical tensions are real. Technological disruption is accelerating rapidly. But the market remains what it has always been: a forward-looking mechanism attempting to price both risk and adaptation simultaneously. While headlines focus on fear, capital continues searching for productivity, innovation, earnings growth, and strategic advantage.

That may be the defining characteristic of today’s wall of worry. Investors are no longer simply debating whether the economy can grow. They are debating whether the value of money itself is changing beneath their feet. They are questioning whether asset prices are rising because businesses are becoming more valuable, because currencies are becoming less scarce, or both. And perhaps most importantly, they are wrestling with the uncomfortable realization that modern markets may now depend as much upon monetary policy and liquidity creation as traditional economic fundamentals.

Still, history suggests the same lesson that appeared in the 1980s, the early 2000s, and the financial crisis. The fears change. The headlines evolve. The anxiety becomes more sophisticated. But capitalism continues adapting, technology continues advancing, and markets continue searching relentlessly for the next source of growth. The wall remains. Only the bricks are different.

The Media’s Role in Building the Wall

The media has always been one of the biggest bricklayers in the wall of worry. Fear sells. Panic gets attention. Calm and rational analysis usually does not. A headline that says, “Things are slowly improving and capitalism is adapting as usual” does not generate many clicks. But a headline screaming about economic collapse, war, banking panic, inflation, political chaos, or artificial intelligence destroying civilization by Thursday afternoon gets people glued to screens immediately.

Every era has its financial villains and apocalyptic forecasts. In the 1980s it was inflation and nuclear war. In the early 2000s it was terrorism and the collapse of technology. During the financial crisis it was the end of capitalism itself. Today it is debt, currency debasement, artificial intelligence, geopolitical conflict, and institutional distrust. The names change. The themes evolve. But the formula stays remarkably consistent. Convince people the world is becoming unmanageable and they will keep watching.

The important thing for investors to understand is that headlines are designed to capture emotion, not necessarily predict markets. Markets are forward-looking. The media is present-tense. That creates a major disconnect. By the time fear dominates the front page, markets are often already trying to determine what recovery, adaptation, or opportunity might look like six months or even several years down the road.

This does not mean the fears are fake. Many are legitimate. Inflation hurts people. Wars matter. Debt matters. Recessions matter. Technological disruption creates real winners and losers. But markets rarely wait for perfect clarity before moving higher. In fact, some of the strongest bull markets in history began when headlines looked terrible.

That is one of the strangest truths about investing. Bull markets are often born when reality turns out to be merely bad instead of catastrophic. The wall of worry only works because human beings naturally focus on danger first.

The Wall of Worry Creates New Winners

One of the great ironies of capitalism is that every major crisis eventually turns into somebody else’s bull market. Human beings panic. Markets reorganize. And somewhere, usually in a fluorescent-lit conference room filled with caffeine addicts and slideshows, somebody figures out how to monetize the fear.

Cold War anxiety helped fuel defense and aerospace booms. Inflation fears created massive runs in commodities, energy, and gold. The dot-com collapse wiped out armies of ridiculous internet companies with business models roughly equivalent to “losing money faster online,” but the wreckage eventually gave rise to Amazon, Google, and the modern digital economy. The financial crisis produced central-bank liquidity on a historic scale, which helped ignite one of the largest asset booms in history. Today, fear surrounding artificial intelligence, cybersecurity, supply chains, semiconductors, and geopolitical instability is pouring billions into entirely new industries.

This is how the wall of worry quietly becomes the incubator for the next generation of winners.

Every fear creates demand for a solution.

Afraid of war? Buy defense systems.

Afraid of inflation? Own hard assets.

Afraid of currency debasement? People run toward gold and Bitcoin.

Afraid artificial intelligence will reshape civilization? Capital floods into semiconductors, cloud computing, power infrastructure, and data centers fast enough to melt the wiring in lower Manhattan.

The public usually focuses on the danger itself. Markets focus on who profits from solving the danger.

Because while television panels are busy hyperventilating about catastrophe, capital is already sprinting around the economy searching for leverage, pricing power, productivity gains, and strategic advantage. Markets are not emotional support groups. They are giant capital allocation machines. They do not ask, “Is this frightening?” They ask, “Where will the money flow next?”

And that is why some of the biggest winners in market history emerge directly out of chaos and uncertainty. Fear forces governments to spend money. Fear accelerates innovation. Fear changes consumer behavior. Fear redirects investment capital. Entire industries are born because human beings become terrified of losing security, convenience, wealth, energy access, military superiority, or purchasing power.

In other words, the wall of worry does not merely obstruct bull markets.

Quite often, it builds them.

What Traders Can Learn from the Wall of Worry

The intelligent trader understands that markets are driven not by comfort, but expectation. By the time the news feels reassuring, the greatest opportunities are often gone. Markets anticipate. They discount the future long before the public fully recognizes what is happening. This is why bull markets so frequently begin in periods of deep pessimism and why major turning points often occur when confidence appears irreparably damaged.

The first lesson of the wall of worry is simple: headlines are not investment strategies. Fear is constant. Every generation produces persuasive arguments explaining why conditions are uniquely dangerous and why markets cannot possibly recover. Yet history repeatedly demonstrates that businesses adapt, industries evolve, productivity improves, and capital reorganizes itself toward opportunity. The successful trader learns to distinguish between emotional narratives and measurable market behavior.

The second lesson is that leadership matters more than opinion. In every cycle, certain sectors, industries, and companies begin attracting capital despite widespread uncertainty. This is rarely accidental. Markets leave clues. Relative strength, earnings growth, productivity gains, pricing power, technological leadership, and strategic relevance tend to reveal themselves long before consensus opinion changes. The disciplined investor studies where capital is flowing rather than becoming trapped in ideological debates about where it should flow.

It’s also important to recognize that markets are selective. Bull markets do not lift every company equally. Some businesses benefit enormously from inflation, technological change, monetary policy, geopolitical shifts, or changes in consumer behavior. Others struggle to adapt. The wall of worry itself often determines the next leadership group. Inflation fears may favor commodities and hard assets. Artificial intelligence may reward semiconductors and infrastructure providers. Currency debasement may strengthen interest in scarce assets. Fear reshapes capital allocation.

The final lesson may be the most valuable of all: uncertainty never disappears. Investors often delay action waiting for perfect clarity, stable conditions, and universal confidence. Those moments rarely exist. The market continuously operates in an environment of incomplete information, conflicting narratives, and shifting expectations. The most successful traders are not those who eliminate uncertainty. They are those who learn how to operate intelligently within it.

The wall of worry is not an obstacle unique to one generation. It is the permanent condition of investing and trading itself. Those who understand this gain an enormous advantage. While others become paralyzed by headlines, they focus on leadership, adaptability, capital flows, and opportunity. In the long run, that distinction can make all the difference.

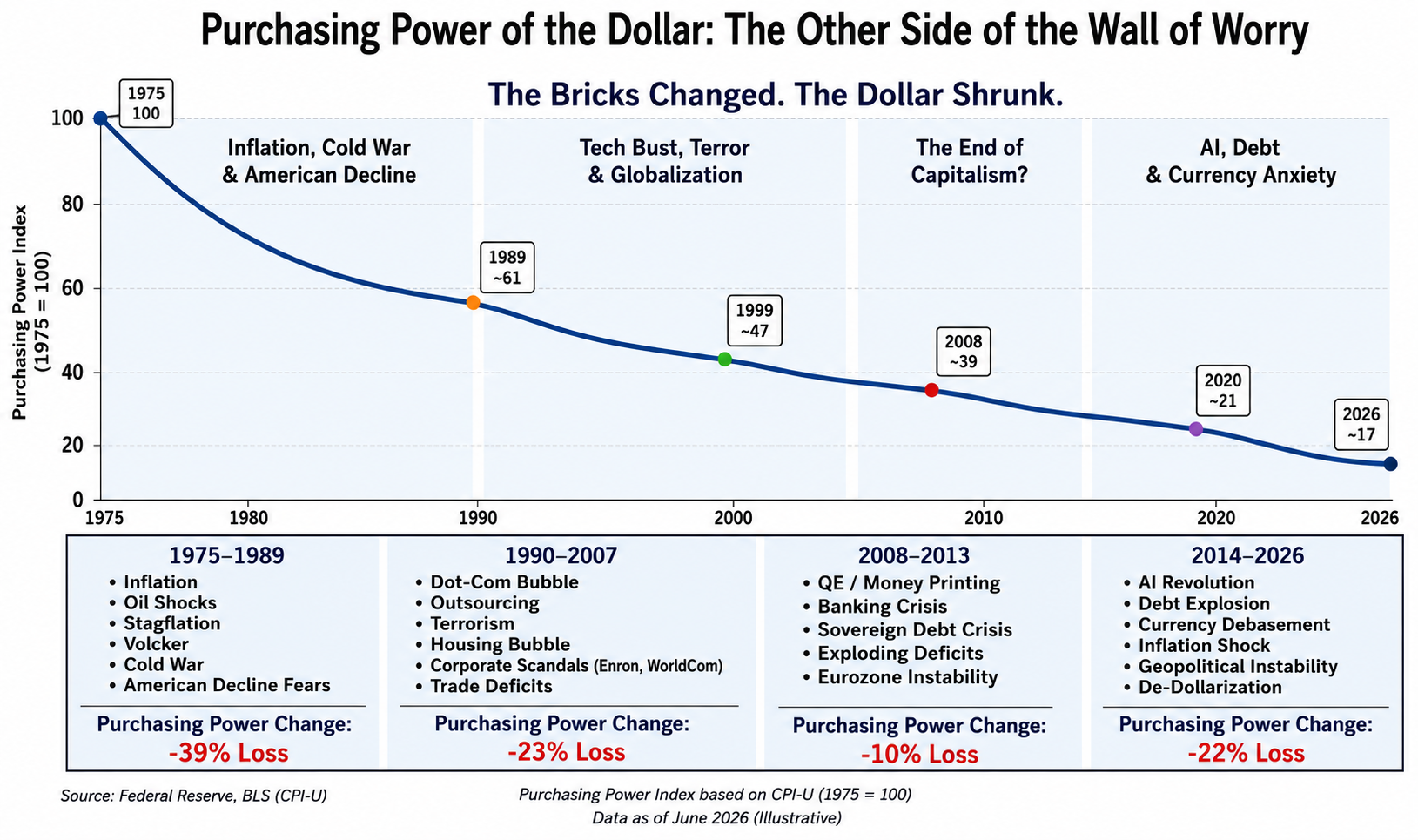

The graphic above tells a story most investors understand emotionally but rarely measure mathematically: the dollar in your pocket is not standing still. Since 1975, every era brought its own crisis, villains, and predictions of economic collapse. Inflation. Terrorism. Banking failures. Debt explosions. Yet through all of it, one force remained remarkably persistent: the purchasing power of the currency itself kept shrinking. What cost $100 in 1975 increasingly required far more dollars with each passing decade. The wall of worry changed shape. The arithmetic did not.

This is why intelligent investors must learn to think in two dimensions simultaneously. The first question is whether assets are rising. The second, and often more important question, is whether assets are rising faster than the currency is losing value. Wealth is not created merely by watching numbers go up. Wealth is created when purchasing power grows. The investor who ignores currency debasement risks celebrating nominal gains while quietly losing economic ground. Markets may climb walls of worry, but your measuring stick matters too.

Here’s something worth thinking about…

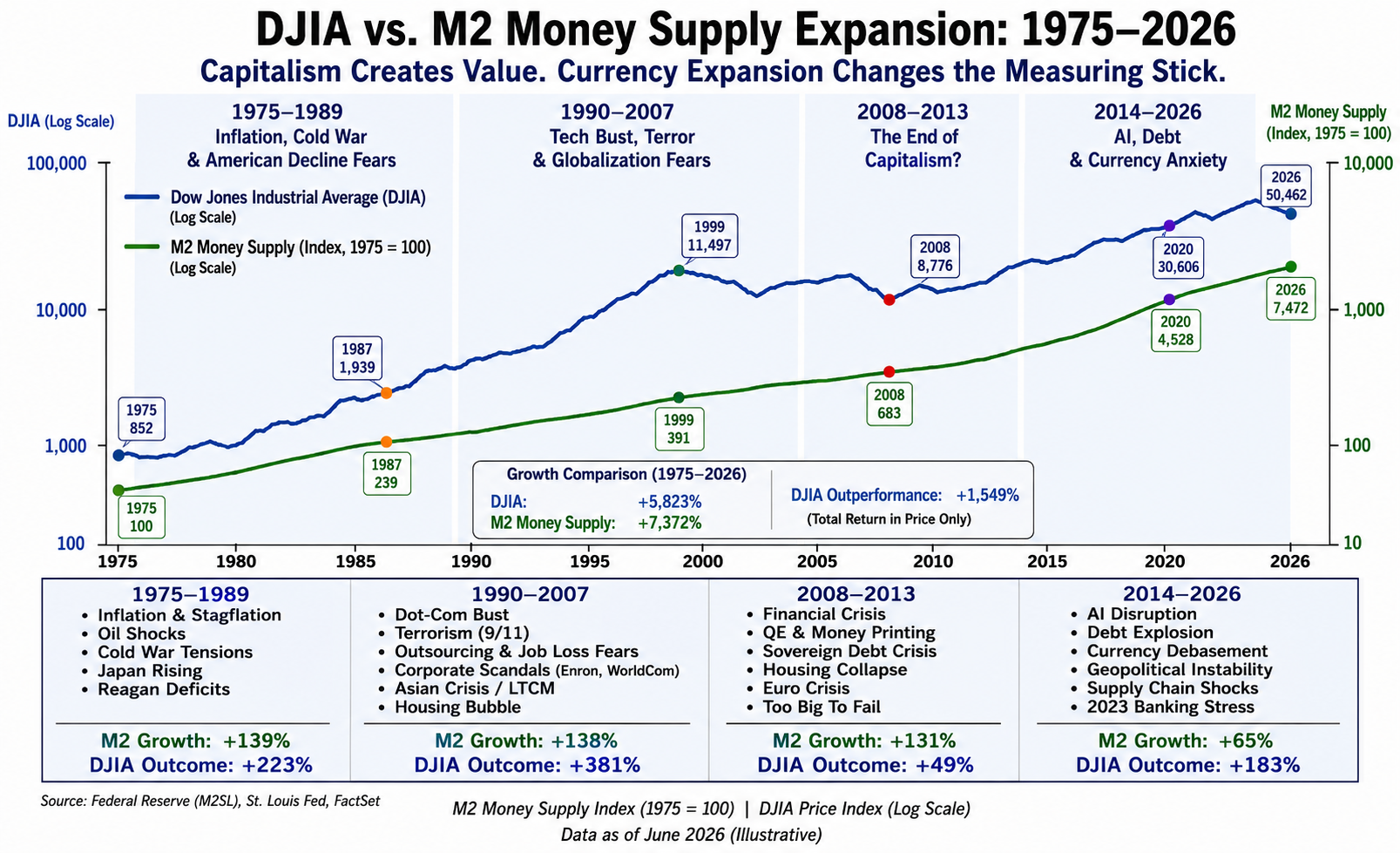

For nearly half a century, investors have lived through oil shocks, recessions, wars, terrorist attacks, financial crises, pandemics, and now the rise of artificial intelligence. Yet this chart suggests a more persistent force may have been operating beneath every headline: monetary expansion. Since 1975, the money supply has expanded dramatically, changing the denominator through which investors measure wealth creation. The result is a market that climbed a wall of worry while simultaneously climbing a mountain of liquidity. Capitalism undoubtedly creates value, but the measuring stick itself has been moving for decades.

What stands out is not simply that the market moved higher. It is how consistently periods of fear coincided with another round of monetary accommodation, debt expansion, or policy intervention. From stagflation to quantitative easing to today’s AI-driven enthusiasm, each era carried its own crisis narrative, yet both money supply growth and equity prices continued trending upward over long periods. The lesson is not that risk disappears. It is that modern markets increasingly force investors and traders to ask a different question: are asset prices rising because businesses are becoming more valuable, because currencies are buying less, or because both forces are occurring simultaneously?

Every generation gets its own version of the wall of worry.

Today? You get inflation, debt explosions, artificial intelligence, banking stress, geopolitical conflict, currency debasement, trillion-dollar deficits, ai data centers and markets moving faster than most people can think.

Different bricks. Same wall.

And while history suggests stock prices tend to rise over long periods as more dollars flood into the system, there is a catch nobody likes talking about:

The path keeps getting more violent.

Bigger swings.

Faster rotations.

Shorter cycles.

More false moves.

More noise.

Which means something very important…

Timing and market selection are not optional anymore.

They are everything.

The old “buy it and hope” strategy? It worked a lot better when markets moved at the speed of a horse and buggy. Today, billions of dollars can disappear or appear before lunch. One policy announcement. One headline. One algorithmic avalanche. And suddenly the market you thought you understood becomes something entirely different.

What you need now is not more opinions. Not more TV experts. Not another guy on social media screaming about the next hot stock. You need better tools. You need a framework built specifically for uncertainty, volatility, and speed. That is exactly why VantagePoint AI exists.

VantagePoint AI was built around one mission: keep traders on the right side of the right trend at the right time. Instead of waiting for yesterday’s indicators to confirm what already happened, VantagePoint AI looks forward. It analyzes intermarket relationships, predictive forecasting, neural networks, machine learning, and market probabilities to identify where strength may be building before it becomes obvious to everyone else. While most traders are driving by looking in the rearview mirror, VantagePoint AI is focused on forecasting what’s next.

Here’s the bottom line. The opportunities ahead could be enormous. But only for traders willing to adapt. Education comes first. Seeing these tools in action comes next. That is why I want to invite you to attend a FREE Live Online Masterclass where you can see how traders are using VantagePoint AI to navigate volatility, identify opportunity, and approach one of the most uncertain financial environments of our lifetime with greater confidence.

The investing textbooks most people learned from were written for a different world. Looking backward worked reasonably well when markets moved slowly. Today, backward-looking tools alone can leave traders reacting while smarter money is already repositioning.

This is why VantagePoint AI matters.

Because probabilities matter.

Accuracy matters.

Knowing where strength is building matters.

Knowing what markets to avoid matters.

And when volatility shows up, having tools that help keep you on the right side of the right trend at the right time becomes a serious advantage.

If you want to see how traders are using predictive artificial intelligence to cut through the noise, isolate opportunity, and navigate today’s market environment, join us for a free live online MasterClass and learn how to trade with VantagePoint AI.

Bring your favorite tickers.

Bring your toughest questions.

And see what happens when you stop reacting to markets and start preparing for them.

Look forward to seeing you there.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.