Imagine you’ve been playing Monopoly with your family for years, except it’s not a board game, it’s your actual life. Your dad still owns Boardwalk and Park Place because he bought them in the ’80s when they were cheap. Your mom’s got the Railroads locked up because she inherited them. And every time you pass “Go,” you’re still collecting $200 — only now it barely covers groceries for the week and gas to get to work.

Meanwhile, the banker — think of him as the Federal Reserve with a mustache — keeps sliding extra stacks of cash to your parents under the table. “Liquidity,” they call it. To you, it looks a lot like cheating. You’re left praying you don’t land on one of their hotels because rent equals three months of your salary.

That, friends, is wealth inequality.

It’s not abstract, it’s not some graph in the Wall Street Journal — it’s watching your parents’ property values soar while you can’t even afford Baltic Avenue. It’s the long arc of finance bending, not toward justice, but toward the same people who already had the good seats at the table.

Money runs our lives from cradle to grave. The minute you’re born, somebody’s already calculating whether you’ll be delivered at the Ritz-Carlton of hospitals or the Motel 6 of maternity wards. And when you check out of this world, the undertaker wants cash up front. In between, money decides where you live, what you eat, how many choices you get to make, and whether you drive a Lexus or ride the bus with a guy who thinks deodorant is government mind control.

And yet, for all that, most Americans wander around blissfully clueless about just how lopsided the wealth in this country really is. Ask the average person what wealth inequality looks like, and you’ll get a blank stare — like you just asked them to explain quantum physics using sock puppets.

This isn’t some dry, academic snooze-fest about “economic theory.” Nope. In this article, we’re going straight for the jugular. We’re going to rip open the whole ugly truth about wealth inequality — where it comes from, who’s behind it, and why it keeps getting worse

no matter how hard you work. Spoiler alert: it’s not bad luck, and it’s not your fault. It’s baked into the system.

We’ll pull back the curtain on how the Fed and government policy have hardwired inequality into the economy. We’ll show how every new dollar created doesn’t float down to you and me — it funnels straight into the hands of those already at the top. And we’ll expose the dirty little secret that wealth inequality isn’t just about the rich having more toys. It’s about inflationary currency debasement — the silent tax that steals your purchasing power while they smile on TV and call it “stability.”

By the time we’re done, you’ll see exactly how the game is rigged… and why if you don’t start playing smarter, you’ll be eaten alive by the same machine that’s been grinding down the middle class for decades.

Wealth is all the stuff you own that has value — money, houses, land, businesses, stocks, and even assets like art or gold.

Wealth inequality means that some people have way more of this stuff than others. Imagine if 10 kids were in a room and one kid had 95 candy bars, while the other nine kids had to share and fight over the remaining five candy bars between them. That’s wealth inequality.

Wealth inequality is a slow-motion mugging, conducted in broad daylight, with the thieves wearing $3,000 suits and calling it innovation. Once upon a time, you could trade a summer job for tuition, one paycheck for a mortgage, and a union card for dignity. Now you trade three side hustles for panic attacks, and your landlord charges you $1,900 – $3,000 for landing on his square.

The system works beautifully — for the people who designed it. They get castles with elevators. We get DoorDash. They get stock buybacks and offshore accounts. We get toothy productivity gurus, and the existential privilege of mistaking burnout for ambition. Capitalism, in theory, is a fair game. In practice, it’s still Monopoly – where you showed up late, all the properties are gone, and late in the game you discover that the guys winning big are playing with counterfeit money.

Our elites like to call this meritocracy. The “merit” seems to be having the right parents.

Economists and politicians understand something very simple, and very important: the greatest power in the world is the power to control the money supply. If you can decide

how much money there is, you can create almost any illusion you want. You can make people feel richer, or poorer, or convince them that growth is happening, even when it isn’t.

Take currency debasement. It’s the oldest trick in the book, and it’s directly tied to wealth inequality. When the currency loses value, anything denominated in that currency — stocks, houses, art, bitcoin, gold, whatever — goes up in price. But here’s the catch: the thing didn’t necessarily get more valuable. It just takes more dollars to buy it, because the dollar itself is worth less.

The illusion is that wealth is being created. Your home price doubled! Your stock portfolio is up! Politicians can point to charts and brag about prosperity. But in reality, the denominator is shrinking, not the numerator growing. For people who already own assets, this system works beautifully: their wealth compounds as money is debased. For people who don’t, it’s brutal: their wages lag behind inflation, and they watch from the sidelines as the asset-owning class pulls further ahead. That’s how currency debasement quietly translates into wealth inequality — it props up those at the top while making it harder for everyone else to catch up.

Most people don’t really understand inflation. Which is fine, because most people also don’t really understand money, or wealth, or the strange ways those things overlap. Charlie Munger once said that if you want to understand why a company works (or doesn’t), you should look at the incentives. My own theory about wealth inequality is just that: the incentives are bad.

Our political and economic leaders are rewarded not for protecting the currency, but for mismanaging it. That’s not an opinion, it’s a statistic. Over the past 112 years, the U.S. dollar has lost about 98% of its purchasing power. That’s… a horrible batting average for the central bank. But here’s the magic trick: every time the Treasury and the Federal Reserve debase the currency, everything priced in that currency — houses, stocks, cars, bananas — goes up in price.

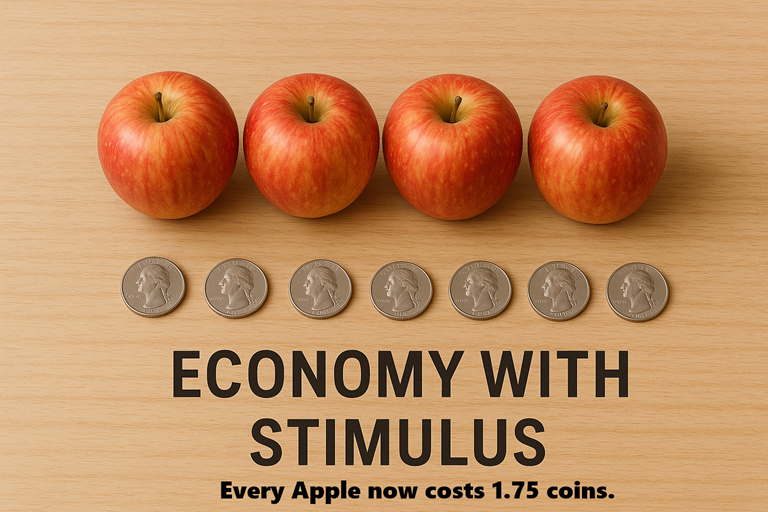

Imagine the world boiled down to four apples and four coins. Simple. One apple costs one coin. No economists, no central bankers, no talking heads on CNBC — just apples and coins. Even a kid in kindergarten could understand this economy.

Now, in a healthy world, the apple farmer does what humans are supposed to do: he figures out how to grow more apples cheaper. Irrigation, better seeds, maybe even a robot scarecrow with A.I. laser eyes, whatever it takes to boost yield. Result? More apples for the same four coins. You win, I win, everyone gets pie for dessert. In fact, in the dream scenario, one coin gets you two apples. That’s the miracle of productivity and stability rolled into one shiny Granny Smith.

But no. That’s not how the real-world works. Enter government. Our trusted officials show up at the orchard with three extra coins they printed out of thin air. Did they bring more apples? Of course not. That would require effort. So now we’ve got seven coins chasing the same four apples. Gradually, an apple costs 1.75 coins. Congratulations — you’ve just experienced inflation without the fun part of actually getting more apples.

And here’s the kicker: we’ve been trained like Pavlov’s dogs to believe falling prices are some sort of economic apocalypse. Cheaper apples? Horrors! So instead of embracing abundance, we stick with what we’re actually good at: debasing currency. Make the money smaller, blur the math, and keep the peasants happy with shiny new “Fruit ETFs” as hedges against the inflation. All so the grift can keep rolling until the orchard is bare.4

So we get this odd illusion: even though the economy is being mismanaged, it looks like wealth is being created. Your house is worth more! Your stocks are up! Your 401(k) statement looks great! Except what’s really happening is that the denominator—the dollar—is shrinking. It sounds insane, but it’s the system.

You might think the little graphics of apples and coins are too simplistic — like economics for kindergarten. But that’s the point. Currency debasement isn’t complicated. It’s stupidly simple and stupidly destructive. All I’m trying to show is how this shell game works when you’re trying to measure economic value.

Your stocks and bonds? They react to government “stimulus” the same way those apples did in the pictures: they get a bigger price tag, not because they’re worth more, but because the money used to price them is worth less. It’s a cheap magic trick — an illusion of prosperity. Washington waves its hands, Wall Street claps, and Main Street wonders why everything costs more.

Look at just this year: the dollar is down 11%, the broad stock market averages are up 10–12%. Do you think that’s a coincidence? Or is it simply the math of measuring things in a unit that keeps melting?

The same pattern shows up everywhere — homes, stocks, art, collectibles. All the things we’re told are “going up in value.” Since 2000, even gold — which used to be money — has outperformed both the Nasdaq and the S&P 500. Think about that. The world’s most successful, best-managed companies, applauded daily by Wall Street and financial media, have been beaten by a lump of metal pulled out of the ground.

And yet every night on CNBC, rising asset prices are celebrated as proof of “wealth creation.” Houses at record highs. Stocks at record highs. Art auctions breaking records. But ask yourself: how is it possible that what used to be money has outperformed the crown jewels of modern capitalism?

The answer is painfully obvious. It isn’t that these assets are magically more valuable. It’s that the measuring stick — the dollar — is deteriorating. This is not wealth creation. It’s currency debasement dressed up as prosperity.

Want to question this reality? Just change the measuring stick. Stop pricing assets in dollars, and start pricing them in gold or Bitcoin. Do that, and the three-card monte routine our politicians have been running becomes obvious.

Take this example: in the 1960s, a top-of-the-line Oldsmobile cost about 25 ounces of gold — or $875. Fast-forward to today. That same Oldsmobile will still set you back about 25 ounces of gold. But in dollar terms? Roughly $90,000.

Did the car suddenly become some priceless collectible? Of course not. The car didn’t change. What changed was the currency. The dollar deteriorated, and the illusion created was that “wealth” had been built because the price tag ballooned. In reality, it’s the same car — just measured with a ruler that keeps shrinking.

In economics, we like to pretend we have neat, objective tools to tell progress from regress. GDP, CPI, unemployment rates — all dressed up in charts and formulas. Our authorities insist these are reliable measures of economic “health.”

But let me pose a simpler set of questions: How do you actually judge the health of a country or its currency? How do you measure whether an economy is truly creating wealth, or just playing shell games?

My perspective is painfully basic. If politicians can debase the currency, they will. That’s the one rule you can count on. And once they do, they’ll point to the ripple effects as proof of their brilliance. Your house quadruples in price? They’ll tell you that’s prosperity. Stocks surge when the dollar melts? They’ll call it growth.

But what’s really happening is sleight of hand. They weaken the measuring stick — the dollar — then celebrate when everything measured against it looks bigger. It’s the same pile of wood, but they’ve shrunk the ruler.

And here’s the madness: we’ve been living with this for generations in the United States. Every time the dollar falls, policymakers claim they’ve discovered the recipe for wealth creation. In reality, they’ve just found a new way to disguise wealth transfer. The illusion is progress; the reality is regress.

Let me explain.

The Trump administration made it clear: they want a weaker dollar and rock-bottom interest rates. If they could get away with it, they’d love negative rates — you know, the kind of upside-down lunacy where you pay the bank to hold your money.

And here’s what that means: prices are going to rip higher. Substantially. Don’t kid yourself. It’s the same scam as the apple/coin graphics above — you think you’re richer because the price tag is bigger, but all that’s really happening is the dollar in your pocket is shrinking.

That’s not a healthy economy. Call it “stimulus,” call it “modern monetary policy,” call it “winning” if you want — it’s still sick. And here’s the kicker: the people who own assets love it. Their wealth soars. The folks scraping by on wages? They get crushed. That’s how you end up with a society split right down the middle. The rich vault higher, the rest sink lower.

Bottom line: this game of cheap money and weaker dollars doesn’t fix the system. It breaks it further. And every time it happens, the wealth gap yawns wider.

The first thing any serious investor must recognize today is the reality of currency debasement and its link to widening wealth inequality. The dollar is not a fixed measure of value — it has been eroding steadily for over a century, and the pace has only accelerated. That forces everyone, from policymakers to households, to rethink how they navigate a currency that is perpetually shrinking. If you fail to understand this dynamic, you risk mistaking illusions of prosperity for real growth.

So, the question becomes: how do you operate in this environment? The choices are stark. You can rely on wages and savings accounts that consistently underperform inflation, or you can build strategies that actively account for the currency’s deterioration. This isn’t just an academic exercise. It’s the difference between compounding wealth or watching your purchasing power evaporate. And for traders, that means using every tool available to stay ahead of markets that no longer follow traditional rules.

And here’s where it gets weird — and kind of funny, in the dark way economics is funny. If the dollar keeps shrinking, then trading in dollars is like playing a board game where the rules keep changing mid-turn. So you need something that adapts faster than you can, which is why A.I. makes sense. The purpose of trading with A.I. isn’t magic. It’s just math at scale: helping you stay on the right side of the right trade at the right time. It’s like having a calculator in a world where everyone else is still doing long division on a napkin.

What traders truly want — what you crave every single day — is certainty. A repeatable, reliable way to stay aligned with the winning side of the market. And that’s precisely what A.I. delivers. It doesn’t tire, it doesn’t blink, and it doesn’t get fooled by the propaganda or headlines that constantly lead ordinary investors astray. In a world where our currency is deliberately weakened and inequality keeps climbing, A.I. is the rare advantage that allows you to fight back. It is, in every sense, the secret weapon to safeguard and multiply your wealth.

Look, you’re not crazy. The money is. This shell game of printing, spinning, and pretending it’s all fine has been going on forever — and it’s not stopping. Your job is simple: don’t fall for it. Don’t swallow the propaganda. Don’t cling to “traditional” thinking that hasn’t worked in decades. Use the tools that actually give you an edge, like A.I., to stay one step ahead. Because the truth is brutal: if you keep playing by the old rules, you’ll keep losing. The only objective is survival — and survival means owning the trend, not getting steamrolled by it.

Every trader faces the same uphill battle…

How do you silence the noise — the avalanche of charts, headlines, predictions, and talking heads — and make clear, confident, profitable decisions day after day?

The sobering truth? Most don’t.

Markets are more volatile than ever. The rules keep changing. And the old playbook — the one built on blind faith in “buy and hold” — is dead and buried.

Here’s what the savviest traders already understand:

We are no longer in the market of five years ago. We’ve entered a Brave New Financial World — engineered by artificial interest rates, reckless monetary experiments, and a level of uncertainty we’ve never seen before.

When central banks shoved rates into negative territory, they didn’t solve a problem. They detonated a time bomb. And now, with the Federal Reserve signaling no rate cuts through 2025, the tremors are only getting stronger. Volatility isn’t “coming back.” It’s preparing to explode.

So, what’s the smart trader’s move?

You adapt. You evolve. You upgrade your tools.

That’s where Artificial Intelligence enters the picture.

Not as a toy. Not as a luxury. But as a trader’s new necessity.

Today’s A.I. trading systems don’t drown you in data — they filter it. They cut through the chaos, uncover the probabilities that matter, and put you on the right side of the right trend at the right time.

This is no longer the domain of billion-dollar hedge funds. Right now, Main Street traders are harnessing A.I. to achieve institutional-grade precision.

Smaller accounts, bigger wins. Lower stress, higher certainty.

And here’s why it matters to you… if you’ve watched your hard-earned savings get tossed around by headlines and algorithms… then it’s time to take back control.

That’s what this free, live online training is about.

It’s not magic.

It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.