The A.I. stock spotlight this week is Century Aluminum ($CENX)

Century Aluminum isn’t just riding a commodity wave — it’s positioned at the center of an American industrial revival. This Chicago-based aluminum producer has transformed from a struggling operator shuttering capacity during weak pricing into a domestic manufacturing comeback story powered by tariff policy, tight aluminum inventories, and a strategic positioning that’s hard to replicate.

At its core, Century produces primary aluminum, the base metal that powers everything from aircraft manufacturing to electric vehicle components. But the real story isn’t just what they make, it’s where they make it and why that matters now. With production facilities in the United States and Iceland, bauxite mining operations in Jamaica, and a carbon anode facility in the Netherlands, Century controls critical stages of the aluminum supply chain at a time when reshoring manufacturing has become national policy.

The company operates smelters in Mt. Holly, South Carolina, and two Kentucky locations in Sebree and Hawesville. That domestic footprint suddenly became a competitive advantage when President Trump implemented 50% Section 232 tariffs on aluminum imports in 2025, making foreign aluminum significantly more expensive and domestic production substantially more profitable. Century responded immediately, announcing a $50 million investment to restart over 50,000 metric tons of idled production at Mt. Holly, bringing the plant from 75% to full capacity by June 2026 — a production level not seen since 2015.

Founded in 1995 and employing thousands across its global operations, Century has survived multiple commodity cycles, plant curtailments, and industry consolidation. What separates this moment from past rallies is structural: aluminum demand is being driven by electrification trends, lightweighting in transportation, and government-backed reshoring initiatives that aren’t going away with the next earnings cycle.

The aluminum business is brutally simple and impossibly complex. Simple because the product is a commodity — one ton of primary aluminum is fundamentally the same as another. Complex because profitability hinges on electricity costs, alumina prices, logistics, tariff policy, and global supply-demand dynamics that can shift dramatically quarter to quarter.

Century’s revenue model reflects this reality. When aluminum prices rise and production runs near capacity, margins expand quickly. When prices fall or energy costs spike, those same margins compress just as fast. The company has no pricing power in the traditional sense, it takes the market price for aluminum and competes on cost structure, capacity utilization, and operational discipline.

The recent restart at Mt. Holly illustrates how this works in practice. At 75% capacity, the plant was covering variable costs but leaving fixed costs underutilized. Bringing the facility to full production spreads those fixed costs across more tons of aluminum, improving per-unit economics even if aluminum prices stay flat. Add in the 50% tariff shield against foreign competition, and suddenly a marginal operation becomes highly profitable. That $50 million investment creates over 100 jobs averaging $100,000 in wages and generates an estimated $890 million in annual economic impact for South Carolina at full capacity.

Competition in primary aluminum is global and unforgiving. Century competes against massive international producers in China, Russia, and the Middle East, where energy costs are often subsidized and environmental regulations less stringent. Domestic competitors like Alcoa operate at similar scale but with different asset portfolios and strategies. The competitive advantage for Century right now isn’t superior technology or brand, it’s geography combined with policy protection.

Financially, Century has had a volatile few years, typical for commodity producers. The stock has surged approximately 85% over the past year, driven by tariff implementation, aluminum price strength, and the Mt. Holly restart announcement. Recent quarters showed mixed results: Q3 2025 earnings came in at $0.56 per share on an adjusted basis, beating expectations, though GAAP earnings of $0.15 per share declined sharply year-over-year. Revenue of $632.2 million slightly missed consensus but was up 17% from the prior year.

The balance sheet reflects the capital-intensive nature of the business. Century carries debt but has improved liquidity through recent financing, including a $400 million senior secured notes offering completed in July 2025. The company’s ability to fund the Mt. Holly restart and potentially bring the idled Hawesville smelter back online depends on sustained aluminum pricing and continued tariff protection.

Wall Street analysts currently rate the stock a consensus “Moderate Buy” with price targets averaging around $33, though forecasts range from $28 to $34 depending on assumptions about aluminum prices, production ramp timelines, and tariff durability. The stock currently trades in the mid-$30s with a market capitalization around $3.4 billion, giving it a mid-cap profile with high volatility and strong beta to industrial commodities.

The opportunities ahead for Century are clear and measurable. First, the Mt. Holly restart adds nearly 10% to U.S. domestic aluminum production by mid-2026, translating directly to revenue and margin expansion if pricing holds. Second, potential additional capacity restarts at Hawesville or investments in entirely new smelter capacity could further leverage the tariff-protected domestic market. Third, secular trends in electric vehicle production, defense manufacturing, and infrastructure spending all increase long-term aluminum demand, particularly for domestically sourced metal.

Management has been cautiously optimistic, crediting tariff policy for creating the conditions necessary to justify capital deployment. CEO Jesse Gary has emphasized the company’s readiness to “lead the resurgence of domestic primary aluminum,” signaling that Century views this as a multi-year opportunity rather than a short-term trade.

The risks are equally straightforward. Aluminum is a commodity, meaning price volatility is not an if but a when. A global economic slowdown, particularly in China, could pressure aluminum prices despite domestic tariffs. Energy costs remain a persistent risk — aluminum smelting is one of the most electricity-intensive industrial processes, and any spike in power prices hits margins immediately. Policy risk is significant: if tariffs are reduced, eliminated, or exempted for certain importers, Century’s competitive advantage erodes quickly.

Operationally, restarting idled capacity carries execution risk. Bringing a smelter from 75% to 100% capacity requires skilled labor, stable power supply, and operational precision. Delays, technical issues, or cost overruns could impact profitability. The company also faces potential headwinds from rising alumina costs, labor negotiations, and the ever-present risk of environmental or safety incidents at its facilities.

In this week’s stock study, we will look at and analyze the following indicators and metrics as they relate to $CENX:

- 52-week high and low boundaries

- VantagePoint A.I. Predictive Blue Line

- VantagePoint A.I. Intermarket Analysis

- Our Suggestion

While we make our trading decisions based upon the A.I. forecasts we receive within the VantagePoint A.I. software, we do consider the fundamentals to better understand the risk and reward profile of this asset.

52-Week High and Low Boundaries

When a stock breaks through its 52-week high, it’s a behavioral shift in how the market values that asset. Century Aluminum recently hit a new 52-week high around $37.45, a move that signals more than just momentum. It represents a fundamental repricing driven by the Mt. Holly restart announcement, sustained aluminum price strength, and the tariff protection that transformed Century’s operating environment.

The significance of this breakout becomes clearer when you look at where the stock has been. Just one year ago, CENX was trading in the low-to-mid teens, reflecting pessimism about aluminum pricing, concerns over energy costs, and uncertainty about the company’s ability to bring idled capacity back online profitably. The 85% gain over the past year is the market recognizing that Century’s earnings power has fundamentally improved.

What makes this 52-week high particularly notable is the catalyst behind it. Unlike momentum-driven breakouts that fade when the narrative shifts, Century’s advance is anchored in tangible operational changes: 50,000 metric tons of additional production coming online, $50 million in capital investment deployed, 100+ new high-wage jobs created, and a tariff structure that makes domestic aluminum production structurally more profitable.

The chart tells the story visually. After years of consolidation and volatility, the stock broke cleanly above prior resistance levels and has held those gains even through periods of broader market weakness. This price action suggests institutional accumulation — the kind of buying that happens when large capital allocators decide an asset’s risk/reward profile has materially improved.

For traders, the 52-week high creates a new reference point. Buyers who hesitated at $25 or $30 are now chasing into the $35+ range, and short sellers who bet against aluminum producers are being forced to cover. This dynamic can create sustained momentum as the market adjusts to a new valuation range. The question becomes whether the breakout leads to further upside or whether profit-taking and mean reversion reassert themselves.

Looking at the longer-term context, Century’s current price sits well above both its 50-day and 200-day moving averages, confirming that the trend is decisively bullish. However, commodity stocks rarely move in straight lines. Even within a strong uptrend, CENX has shown 5-7% daily volatility and monthly swings exceeding 25%. That volatility is a feature, it reflects the underlying commodity price movements, production updates, and tariff policy developments that drive the stock.

The key takeaway from the 52-week high is simple: the market is no longer pricing Century Aluminum as a struggling commodity producer hoping for better days. It’s pricing it as a company actively expanding production into a tariff-protected market with improving margins and visible earnings growth. Whether that repricing is complete or still underway will depend on execution, aluminum prices, and policy stability, but the direction is clear.

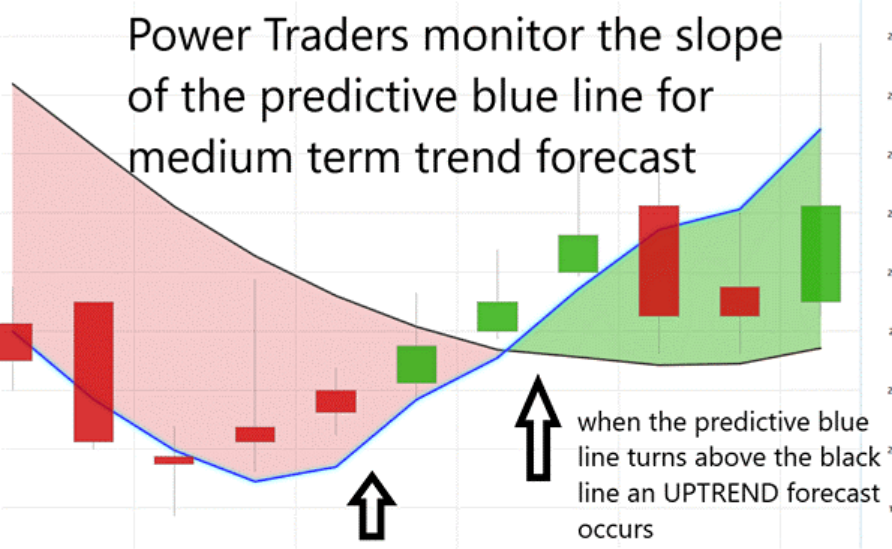

VantagePoint A.I. Predictive Blue Line

The first rule of the VantagePoint A.I. Predictive Blue Line is brutally simple: direction matters more than opinion. When the blue line is sloping upward, the market is telling you demand is gaining the upper hand. When it slopes downward, the opposite is true. Traders get into trouble when they argue with that slope instead of respecting it. You don’t predict the slope, you follow it. An upward slope is permission to think long. A downward slope is a warning to stand aside or think defensively. Everything else is commentary.

The second rule is confirmation, and it comes from the crossover. When the predictive blue line crosses above the black line, it’s the market saying momentum and trend are now aligned. When the blue line crosses below the black line, the message flips just as clearly. Risk is rising. The trend is weakening.

The final rule is discipline. The strongest trades happen when slope and crossover agree, the blue line rising and above the black line.

That’s when trends persist. If the slope flattens or the blue line slips back below the black line, the edge erodes, and capital preservation takes precedence. This is about being aligned.

VantagePoint A.I. Intermarket Analysis

Intermarket analysis is the recognition that no asset trades in isolation. Stocks, commodities, currencies, and bonds are interconnected, and understanding those relationships provides context that single-chart analysis misses entirely. For Century Aluminum, intermarket analysis is essential because the stock doesn’t move based on company-specific news alone — it moves based on aluminum prices, energy costs, currency fluctuations, and broader industrial commodity trends.

The relationship between $CENX and aluminum prices is direct and powerful. When the London Metal Exchange (LME) aluminum price rises, Century’s revenue per ton increases with no change in production costs, expanding margins immediately. When aluminum prices fall, the opposite occurs. This makes tracking aluminum futures essential for anyone trading CENX. Recent aluminum price strength, driven by low global inventories and supply disruptions, has been a tailwind for the stock.

Energy costs represent another critical intermarket relationship. Aluminum smelting requires massive amounts of electricity — it’s one of the most energy-intensive industrial processes in existence. Century’s production costs are therefore tied directly to natural gas and electricity prices. When energy prices spike, as they did during various periods in 2024 and 2025, Century’s margins compress even if aluminum prices stay flat. Conversely, stable or declining energy costs improve profitability without the company doing anything differently operationally.

Currency markets also play a role. While Century’s U.S. operations are dollar-denominated, its Icelandic facilities and global competitive dynamics mean exchange rates matter. A stronger U.S. dollar makes foreign aluminum relatively cheaper, increasing competitive pressure despite tariffs. A weaker dollar has the opposite effect, making U.S. production more competitive globally.

The intermarket map for CENX includes other industrial metals and mining stocks as well. Companies like Steel Dynamics, Alcoa, and other materials producers often move in tandem with Century, reflecting shared exposure to manufacturing activity, infrastructure spending, and commodity cycles. When these stocks strengthen together, it signals broad-based optimism about industrial demand. When they diverge, it highlights company-specific factors — like Century’s tariff advantage — that are driving relative performance.

Equity market breadth also matters. When the S&P 500, Nasdaq, and Russell 2000 are rising together, risk appetite is strong, and capital flows more freely into cyclical, volatile names like $CENX. When markets weaken or rotate defensively, commodity stocks tend to underperform regardless of their specific fundamentals. Century’s recent outperformance has occurred during a period of generally strong equity markets, which has amplified the stock’s gains.

Finally, tariff policy itself functions as an intermarket variable. Century’s competitive position is directly tied to the continuation of 50% Section 232 tariffs on aluminum imports. Any policy shift — whether tariff reductions, exemptions for certain countries, or broader trade negotiations — would impact CENX immediately. Monitoring trade policy developments, presidential statements, and Congressional activity around tariffs is as important as watching the stock chart itself.

The power of intermarket analysis for $CENX traders is that it provides early warning signals. If aluminum prices start weakening, energy costs are rising, and industrial metals stocks are rotating downward, those are yellow flags even if $CENX’s chart still looks strong. Conversely, if aluminum inventories are tightening, energy prices are stable, and peer stocks are breaking out, those are green lights for continued strength.

In short, Century Aluminum doesn’t trade in a vacuum. It trades at the intersection of commodity markets, energy markets, currency markets, and policy decisions. Traders who understand these relationships make better decisions, enter with better timing, and manage risk more effectively than those who focus solely on the stock chart.

Our Suggestion

Century Aluminum’s recent earnings and operational announcements paint a picture of a company in transition, and so far, the transition is working. The Q3 2025 earnings report showed adjusted EPS of $0.56, beating Wall Street’s $0.30 expectation by a wide margin. Revenue came in slightly below consensus at $632.2 million but was up 17% year-over-year, reflecting higher aluminum prices and improved capacity utilization. Management’s tone on the earnings call was measured but confident, emphasizing that the Mt. Holly restart is on track and that tariff protection has created a sustainable operating environment.

The biggest barriers to continued success are macro in nature: aluminum price volatility, energy cost fluctuations, and the ever-present risk that tariff policy shifts. Management has been clear that the restart and expansion plans depend on the tariff structure remaining in place. Any significant weakening of trade protections would force a reassessment of capacity plans and capital deployment.

Looking ahead, the next earnings call is expected in early 2026, when the company reports Q4 and full-year results. Analysts are forecasting continued earnings growth as the Mt. Holly restart progresses and aluminum pricing remains supportive. Current consensus estimates suggest 2026 EPS could reach $3.10, more than double 2025 levels, driven by higher production volumes and sustained margins.

For traders, Century Aluminum sits in an interesting position. The stock has already made a substantial move, up 85% over the past year, which means much of the “easy money” from the tariff announcement and initial restart news has been captured. However, if execution continues smoothly and aluminum prices hold, there’s further upside as the market prices in the full earnings power of a 100%-capacity Mt. Holly operation.

Put $CENX on your watchlist and monitor it closely. This is not a buy-and-forget position. It’s a trade that requires active management, attention to aluminum prices, energy costs, and tariff policy developments. The stock moves fast and moves far, which creates opportunity, but also risk.

Position sizing is critical here. CENX’s beta is high, volatility is significant, and the commodity exposure means swings of 5-10% in a session are entirely possible. Trade it with appropriate risk management. Use stops. And respect the fact that commodity stocks can reverse just as quickly as they advance.

The fundamental story is compelling: domestic aluminum production, tariff protection, capacity expansion, and secular demand growth from electrification and reshoring. The technical picture is strong: new 52-week highs, upward momentum, and institutional buying. But success in trading $CENX will come down to timing, discipline, the willingness to adjust when conditions change, and using VantagePoint A.I. in all your trade decisions.

It’s not magic.

It’s machine learning.

Disclaimer: THERE IS A HIGH DEGREE OF RISK INVOLVED IN TRADING. IT IS NOT PRUDENT OR ADVISABLE TO MAKE TRADING DECISIONS THAT ARE BEYOND YOUR FINANCIAL MEANS OR INVOLVE TRADING CAPITAL THAT YOU ARE NOT WILLING AND CAPABLE OF LOSING.

VANTAGEPOINT’S MARKETING CAMPAIGNS, OF ANY KIND, DO NOT CONSTITUTE TRADING ADVICE OR AN ENDORSEMENT OR RECOMMENDATION BY VANTAGEPOINT AI OR ANY ASSOCIATED AFFILIATES OF ANY TRADING METHODS, PROGRAMS, SYSTEMS OR ROUTINES. VANTAGEPOINT’S PERSONNEL ARE NOT LICENSED BROKERS OR ADVISORS AND DO NOT OFFER TRADING ADVICE.