I was chatting recently with a group of traders, doing what traders always do when there is no chart in front of them and no bell about to ring. We were talking about the markets. The opening salvo of the conversation came fast and predictably: are you bullish or bearish? The room split almost perfectly down the middle, each side armed with strong opinions about where the market was headed next. When it came my turn, I said I was both bullish and bearish. That earned me a few sideways looks and more than one comment that I was sounding like a politician. But the truth is, in a market like this, being willing to hold two opposing views at the same time is not evasion. It is preparation.

Most traders want a single answer. Bullish or bearish. Preferably printed on a laminated card, color-coded, and handed out before the opening bell so no one must think too hard. Unfortunately, markets have never respected our desire for simple answers, especially late in the cycle when logic takes a long lunch and speculation orders dessert.

2026 is shaping up to be the kind of year where bulls can make money, bears can make money, and the people who buy everything because it has a ticker symbol can make memorable mistakes. Opportunity will exist, but only for those willing to be selective, disciplined, and guided by evidence rather than cocktail-party confidence.

The real danger is not volatility. Volatility is just the market doing what markets do. The real danger is indiscriminate exposure, the financial equivalent of eating everything at the buffet because you already paid for the plate.

Since 1990, the S&P 500 Index has told a very consistent story, even though the ride along the way has often felt anything but consistent.

First, the big picture. Roughly 8 out of every 10 years have been positive. That matters. It tells us that the long-term bias of the U.S. stock market is upward, even though the path is uneven and occasionally painful.

Across all the years in the dataset, the average annual return is about 12%. That number alone explains why equities remain such a powerful wealth-building tool over time. But averages hide important details, so let’s look under the hood.

The biggest up year in this period was 1995, when the market surged more than 37%. When the market goes up, it tends to go up decisively. In fact, the average gain in up years is roughly 19%, which tells us that strength, when it appears, usually persists.

On the downside, the worst year was 2008, when the market fell about 36%. Down years are fewer, but they can be sharp. The average loss in down years is about 15%. That asymmetry is important. Losses are less frequent than gains, but they demand respect when they occur.

Put it all together and the message is clear. Markets reward patience, discipline, and participation far more often than they punish it. This data supports what Warren Buffett has said for decades. Over time, it pays to be long the United States of America. Not because markets are easy, but because innovation, productivity, and growth have continued to assert themselves through wars, recessions, bubbles, and crises.

The lesson is not to ignore risk. The lesson is to understand it, manage it, and stay invested in a system that has historically rewarded those willing to play the long game.

In the late stages of a market cycle, rallies do not disappear. They become more selective. History shows that some of the strongest upside moves often occur when confidence is uneven and participation narrows. Risk-on behavior still exists, but it no longer lifts all boats. Capital becomes choosy, gravitating toward tight clusters of stocks, momentum-driven sectors, and speculative corners where returns appear fastest and most visible. This is where bullish opportunity survives, not in broad market optimism, but in concentrated leadership. For bulls, the mistake is assuming the entire market will rise together, as it may have earlier in the cycle. The more useful question now is simpler and more demanding. Where is money flowing today, not where it flowed last cycle.

When markets get late and tired, broad exposure stops being diversification and starts being a liability. This is where a strong index headline can hide a lot of damage underneath the surface. A handful of winners prop up the averages while most stocks quietly sink, stall, or go nowhere. If you are buying everything just because the index is up, you are not investing or trading. You are donating capital to stocks that institutions have already abandoned.

In 2026, bullish success will not come from owning more. It will come from owning better. That means knowing which stocks are actually outperforming, which sectors are attracting real money, and which names are lagging no matter how good the headlines sound. Relative strength matters. Sector discrimination matters. Cutting loose laggards matters, even when the market appears healthy on the surface.

Here is the rule that separates survivors from casualties. Outperforming the benchmark is not optional. It is survival.

The bear case in this cycle is less about an imminent collapse and more about a foundation that is quietly cracking. Economic stress rarely announces itself with sirens. It builds slowly, in rising debt loads, in job growth that decelerates at the margins, and in consumers who keep spending but do so with less resilience beneath the surface. None of these conditions are especially bullish over the long term, even if markets continue to climb in the short run.

This is why bears often look wrong late in the cycle. Not because their analysis is flawed, but because markets can remain buoyant long after the economic underpinnings begin to weaken. In these environments, the bear thesis is usually sound. The problem is timing. Being early can be indistinguishable from being wrong until it suddenly is not.

The key insight is one markets relearn every cycle. Bear markets are born during bull markets, not after them. The excesses that drive the final rally are the same forces that ultimately create the downturn.

Being bearish does not mean standing in front of the market with a stop sign and a strongly worded opinion. It does not mean shorting everything that moves and hoping gravity does the rest. Markets can keep going up longer than most balance sheets deserve and fighting that tape head-on is usually very expensive.

Where bearish opportunity shows up is at the margins. It appears first in companies that relied too heavily on leverage when money was easy, in stocks whose relative strength quietly rolls over even as indexes grind higher, and in sectors that institutions begin to exit long before headlines notice. These are not dramatic breakdowns at first. They are subtle failures to keep up.

This is what allows bears to participate without betting against the entire market. You are not calling the top. You are identifying where capital is already leaving. The discipline is simple and surprisingly hard to follow. Short weakness, not strength.

Volatility gets a bad reputation because it makes people feel nervous, and people hate feeling nervous when their money is involved. They would much prefer a calm, orderly market that goes up every day at a polite pace, like a well-behaved elevator. Unfortunately, markets are more like amusement park rides designed by people who hate you. Sharp turns, sudden drops, and the occasional moment where you wonder why you got on in the first place.

In 2026, volatility is not a warning sign. It is the operating system. Big swings are what you get when money is rotating, narratives are colliding, and confidence changes its mind every other week. Traders who demand smoothness will be disappointed. Traders who define risk, size positions sensibly, and accept uncertainty will find opportunity hiding in the chaos.

Let me explain.

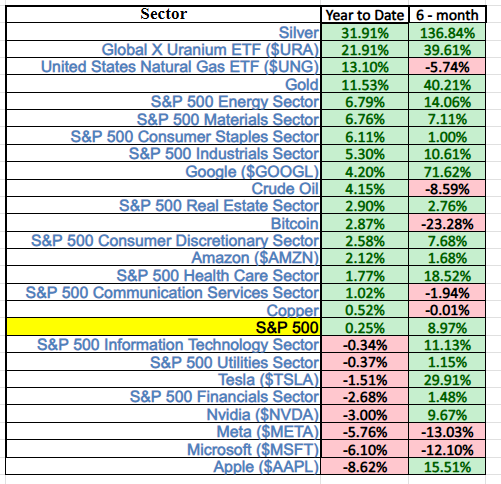

If you look at this performance grid without context, it feels like a bar fight. Red numbers. Green numbers. Tech bleeding in spots. Commodities screaming higher. Confusion everywhere. That is exactly how most traders get chopped up. They glance, react, and guess.

Now slow down and read the scoreboard.

At the top of the table, Silver is up over 31% year to date and a jaw-dropping 136% over six months. That is not noise. That is capital making a very loud decision. Uranium, gold, energy, materials, industrials. Same story. Different tickers. Money is rotating into real, tangible stuff with utility, scarcity, and pricing power.

Then your eye drops down to the so-called safety blanket. Big tech. The names everyone assumes will save them. Apple, Microsoft, Meta, Nvidia, Tesla. A mixed bag at best and outright damage at worst on a year-to-date basis. Some bounce over six months, sure, but the leadership is fractured. This is not a clean, unified bull move. This is dispersion.

And right there in the middle sits the S&P 500, barely positive year to date, quietly masking what is really happening underneath. This is how people get fooled. The index looks fine, so they assume everything inside it is fine. It is not.

This graphic is the market screaming one simple message. Broad exposure is lazy. Selectivity is mandatory.

When you apply context, the chaos disappears. The winners jump off the page. Real assets are leading. Cyclical strength is showing up where money flows when inflation, debt, and uncertainty matter. Meanwhile, large chunks of tech are no longer carrying the market the way they once did.

This is not a prediction. It is not a call. It is an observation. Capital is voting, and it is voting with size.

Here is the trap most traders fall into. They argue with this instead of acting on it. They defend laggards because of stories. They cling to yesterday’s leadership because it worked before. The market does not care. It never has.

This is how professionals separate signal from noise. Compare time frames. Compare assets. Measure relative strength. Follow the money instead of the narrative.

Do that, and the market stops feeling random. It starts feeling readable. And once it is readable, opportunity stops being scarce and starts being obvious.

Now let’s apply a contextual perspective to the following performance grid of all the stock market averages.

At first glance, the weekly and monthly numbers in this table tell a familiar story of market hesitation. Red ink in the near term invites the usual conclusions about fragility or fading momentum. But step back even slightly and the narrative shifts. Over six months and over the past year, the major U.S. equity benchmarks remain firmly positive, suggesting that short-term pullbacks are occurring within a broader advance rather than signaling a breakdown.

What becomes unmistakable with that context is leadership. The Russell 2000 Index, a proxy for small-cap stocks, is not just participating. It is outperforming. With the strongest gains across nearly every meaningful time frame, small caps are clearly attracting capital at a faster pace than their large-cap counterparts. That relative strength matters. It signals a change in risk appetite and a reallocation beneath the surface of the market that broad index headlines alone fail to capture.

Volatility rewards preparation. It exposes anyone who confuses conviction with courage. The goal is not to feel comfortable. The goal is to stay flexible, stay solvent, and let the market tell you what is working right now.

Liquidity is the quiet force that decides which trades work and which ones suddenly stop working. When liquidity is abundant, mistakes get forgiven. When it tightens, nothing is spared. Correlations rise, exits narrow, and assets that looked independent start moving together for all the wrong reasons.

This is where traders get caught leaning the wrong way. Positions that performed well late in the cycle can unwind quickly once liquidity is pulled back. Even assets that are considered defensive can experience sharp drawdowns when selling becomes indiscriminate and capital is forced to move. It is not about fundamentals in those moments. It is about access to cash.

That is why flexibility matters. Liquidity events do not give advance notice, and they do not care about narratives. Traders who survive them are the ones who respect risk, monitor conditions closely, and stay willing to change posture when the evidence shifts.

Opinions are cheap. Everyone has one, most of them are loud, and none of them move markets. Evidence, on the other hand, is stubborn, frequently inconvenient, and completely uninterested in how strongly you feel about your thesis. Markets have always preferred data to drama.

Evidence shows up in performance. Stocks that are outperforming are not doing so by accident. Sectors that attract capital are not winning popularity contests. Money leaves fingerprints, and those fingerprints show up in relative strength, trend persistence, and leadership that refuses to go away no matter how many experts declare it overvalued.

The trick is humility. When the evidence changes, you change with it. Clinging to an opinion after the market has rendered its verdict is not conviction. It is stubbornness with a brokerage account.

2026 is not going to reward blanket exposure or rigid viewpoints. This is a market that demands attention, patience, and the willingness to separate strength from weakness in real time. Bulls can succeed by staying aligned with leadership and respecting trend. Bears can succeed by targeting deterioration without fighting momentum.

The common thread is discrimination. Knowing what to own, what to avoid, and when to step aside matters more than having a strong opinion about the overall direction of the market. Broad labels like bullish or bearish miss the point entirely.

This environment does not punish uncertainty. It punishes carelessness. Traders who focus on evidence, manage risk, and stay flexible will find that 2026 offers plenty of opportunity, just not to everyone at the same time.

What 2026 ultimately demands is a shift in mindset. The traditional question of market direction misses the more consequential issue of market behavior. Capital is moving, but it is doing so unevenly, deliberately, and with far less forgiveness than in earlier phases of the cycle. That reality creates opportunity, but only for those willing to observe rather than embrace an egotistical perspective.

This is not a year for blanket exposure or ideological positioning. It is a year for attention to flow, leadership, and evidence as it develops. The investors and traders who succeed will be those who accept that markets can reward optimism and caution at the same time, often in different places and sometimes in the same week.

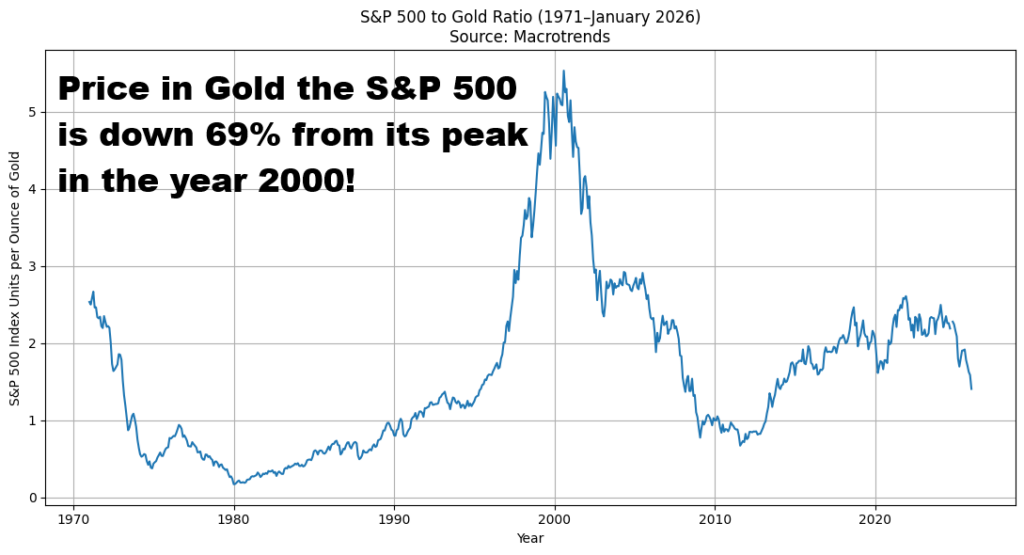

When people look at the stock market, most of the time they look at it through one lens only. Fiat dollars. And through that lens, the story looks fantastic. Since the year 2000, the S&P 500 Index is up roughly 650%. That sounds like prosperity. It sounds like progress. It sounds like success. And in many ways, it is. But context matters. The graphic you are looking at simply asks a different question. What happens when we stop pricing stocks in a currency that is steadily losing purchasing power and instead price them in something that has held its value over time, like gold?

Source: MacroTrends

When you do that, the picture changes dramatically. Priced in gold, the S&P 500 Index is down roughly 69% from its peak in the year 2000. That is not a prediction. It is not a warning. And it is certainly not an attempt to create doom, gloom, or fear. It is context. When you price any asset in a depreciating currency, it will almost always look wonderful over long periods of time. That is not a coincidence. That is arithmetic. It may also help explain why, just last year, the nation’s largest bank openly began promoting what it called “the debasement trade” to its customers. When currency loses value, hard assets, financial assets, and anything scarce tend to rise in nominal terms.

This context matters because debasement has not been subtle. It has been massive ever since we came off the gold standard. Understanding that keeps us grounded in facts and truth rather than headlines and narratives. But trading is not about nostalgia or moral judgments about money. It is about adaptation. In a world where debasement is the backdrop, we must be obsessed with one question above all others. Who is the fastest horse in the race right now? Because the only way to effectively deal with debasement is not to deny it, but to stay aligned with the assets that are outrunning it.

The discipline required is not bravado. It is restraint. Watch where money is going. Notice where it is quietly leaving. Adjust accordingly. In a market like this, that is not hedging your view. It is respecting reality.

The temptation in markets is always to simplify. Bullish or bearish. Risk on or risk off. In 2026, that instinct is more misleading than helpful. This is a market that is doing multiple things at once, rewarding precision and punishing generalization. There are real opportunities on both sides, but they are narrower, faster moving, and less forgiving than in earlier phases of the cycle.

What matters most is not the label you apply to your outlook, but how you respond to what the market is doing. Capital is signaling where it feels confident and where it feels uneasy. Strength is visible if you are willing to look for it. Weakness is equally visible if you are willing to acknowledge it. Ignoring either one is a choice, and not a profitable one.

The traders who navigate 2026 successfully will not be the loudest or the most certain. They will be the most attentive. They will follow evidence, manage risk, and accept that markets can be generous and cruel at the same time. In an environment like this, that balance is not indecision. It is the edge.

The real edge moving forward is not a hotter opinion, a louder prediction, or a better story about where the market should go. The edge is clarity. It is knowing what is happening beneath the surface and having the discipline to align with it. That is exactly where VantagePoint A.I. comes in. It removes guesswork and replaces it with objective, data driven insight. It does not care about headlines, narratives, or emotions. It measures what matters and shows you where strength and weakness are emerging before they become obvious to the crowd.

What this technology brings to the table is leverage of a different kind. Not financial leverage, but decision leverage. VantagePoint A.I. analyzes intermarket relationships, trend direction, and probability-based signals across multiple time frames, all at once. It does the heavy lifting that most traders try and fail to do manually. Instead of reacting late, you gain earlier awareness. Instead of chasing moves, you learn how to position alongside them. That is how consistency is built, not by working harder, but by working smarter.

Risk management is where most traders quietly lose, even when they are right on direction. The purpose of VantagePoint A.I. is to keep you on the right side of the right trend at the right time. When trends weaken, it shows you. When conditions improve, it shows you. That allows you to define risk, size positions intelligently, and avoid the costly mistake of overstaying trades that no longer deserve your capital.

If you want to see how this works in real time, you are invited to attend a free live online masterclass where you can watch VantagePoint A.I. in action. You will see how it identifies trends, filters noise and helps traders make better decisions without emotional interference. This is your opportunity to discover how letting A.I. do the heavy lifting can help you trade with greater confidence, discipline, and consistency.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.