This week’s ai stock spotlight is Lululemon Athletica ($LULU)

Let’s get something straight right up front. Lululemon Athletica does not sell pants. It sells identity. Pants are just the delivery system. And those pants cost more than your first bicycle, which is why investors have always paid attention. When a company can charge $128 for leggings and people line up like it’s a water shortage, that’s leverage.

Lululemon started in 1998 in Vancouver, Canada, back when yoga was still considered a niche hobby and not a full-blown personality. The headquarters are still in Vancouver, which explains the calm confidence and the subtle judgment of your posture. The company employs tens of thousands of people worldwide and operates hundreds of stores across North America, Asia, and Europe.

Leadership today looks less like a cult of personality and more like a professional retail operation. That matters. Retail kills amateurs quickly. Lululemon survived adolescence, grew up, and learned how to count inventory without breaking a sweat. Investors don’t cheer that. They quietly reward it with higher multiples.

Lululemon is a luxury operation that convinces rational adults to pay large for elastic pants and then posts enviable margins while doing it.

While growth slowed, Wall Street clutched its pearls, the stock took a beating, and now miracle of miracles it has remembered how to behave in public again.

The stock moves on earnings, guidance, China headlines, and any whisper about margins, as if analysts are checking the stitching for loose threads.

Traders don’t need perfection here. They just need management to commit the small miracle of being less disappointing than feared.

What Lululemon does is simple enough for any eighth grader. They design athletic and lifestyle apparel. They don’t own factories. They outsource manufacturing. Then they sell the product directly to customers through their own stores and website. That last part is the whole ballgame. Direct-to-consumer means no department store begging, no wholesale margin giveaway, and no clearance rack humiliation unless management screws up badly.

The products are mostly private-label branded goods. Translation: you can’t price-compare them easily, and that keeps margins high. Lululemon doesn’t compete on price. It competes on fit, fabric feel, durability, and the social signal that says, “I take my wellness seriously, even if I skip leg day.” Their strategy is to refresh products constantly, expand internationally, grow the men’s line, and keep the brand premium enough that discounts feel like personal insults.

Competition exists, but it’s uneven. Some competitors have scale but weaker margins. Others have buzz but no global footprint. Here’s how the landscape looks when you strip out the marketing fluff.

Nike is massive but slower. Adidas is still rehabbing its reputation. Under Armour is a reminder that branding mistakes linger. Alo and Vuori are real threats, especially with younger consumers, but neither has the global machine Lululemon runs. Lululemon sits in the sweet spot: big enough to matter, premium enough to price confidently.

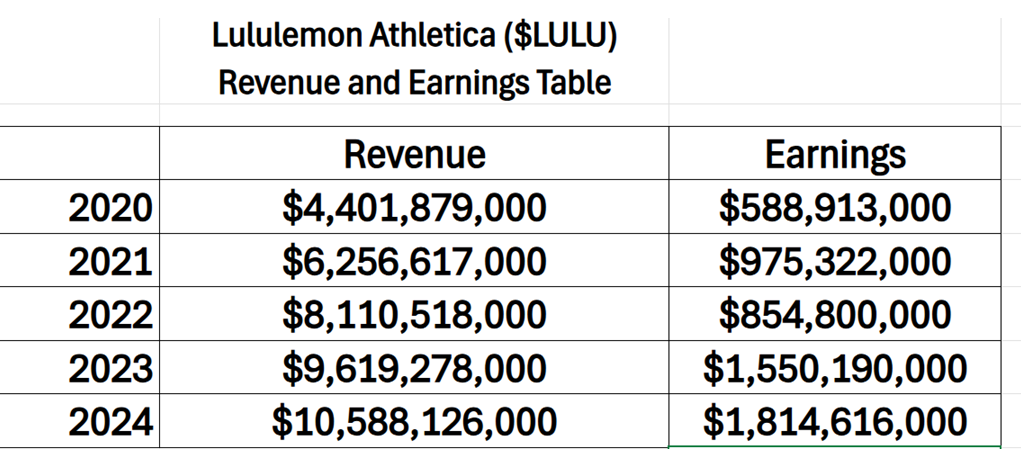

Now let’s talk money, because stories are cute, but earnings pay the rent. Lululemon’s revenue has continued to grow, though not at the hyper-speed investors got drunk on during the pandemic years. Gross margins remain north of 55 percent, which in retail is borderline offensive. Operating margins have compressed slightly as costs rose and international expansion continued, but they’re still strong compared to peers. Cash on hand is healthy. Debt exists, but it’s manageable and not threatening to eat the company alive.

Here’s the financial snapshot traders actually care about.

This is a balance sheet that lets management focus on growth, buybacks, and store expansion without begging bankers for mercy.

So why did the stock stumble? Because expectations got stupid. Growth slowed a bit. China headlines got messy. Guidance turned cautious. Wall Street reacted the way it always does when perfection takes a coffee break: it threw a tantrum. The stock sold off hard, valuations compressed, and suddenly Lululemon was no longer priced like a miracle but like a very good business with normal problems.

That reset is exactly why traders are paying attention again. The bar is lower now. Lululemon doesn’t need to surprise to the upside by a mile. It just needs to execute cleanly and sound confident while doing it.

The opportunities are clear. International growth, especially in China, remains underdeveloped relative to brand recognition. Men’s apparel continues to grow faster than the core women’s business, and men are loyal once they find something that fits. Accessories and footwear provide optional upside without threatening the core. And the direct-to-consumer model gives pricing power that protects margins when others start discounting.

Risks are equally straightforward. Fashion risk is real. Trends change faster than management decks. Competition is intensifying, especially online-first brands that understand TikTok better than Excel. China remains unpredictable. And because this is a premium brand, any hint of margin erosion gets punished immediately. This is not a stock that tolerates excuses.

Valuation is the quiet risk. Lululemon will never trade like a discount retailer. Investors expect excellence. When excellence shows up merely on time instead of early, the stock sulks. That’s the tax you pay for being good.

For traders, the verdict is simple. This is not a meme stock. It’s not a broken retailer. It’s a high-quality brand that stumbled, reset expectations, and is now trying to trend again. It rallies on clean earnings. It sells off on cautious language. It trends when momentum funds rediscover it. And it punishes anyone who ignores the calendar.

Lululemon remains a premium business with premium economics and a temporarily humbled stock price. That combination is often fertile ground for tradable moves. You don’t need to fall in love with the brand. You just need to watch earnings, respect the trend, and remember that when expectations get lighter, stocks don’t need miracles to move, they just need fewer disappointments.

The founding chief executive of Lululemon is Dennis “Chip” Wilson, and his reemergence around the company has revived a familiar — and powerful — market narrative. Founder returns tend to carry symbolic weight on Wall Street, signaling a possible reset to first principles after a period of operational drift. Wilson built Lululemon Athletica ($LULU) from a niche yoga concept into a premium global brand defined by pricing power, product obsession, and cultural distinctiveness. For investors, the allure isn’t nostalgia; it’s the belief that the original architect understands what made the model work, and what may need sharpening now.

That origin story is what animates traders. Markets often treat founders as a form of strategic optionality: the chance that clarity, discipline, and conviction return alongside the person who set them in motion. Wilson’s presence rekindles expectations of tighter product focus, less compromise on brand standards, and decisions guided by instinct as much as spreadsheets. Whether or not he formally retakes the helm, the narrative itself matters. It reframes recent challenges as correctable rather than structural and gives investors a reason to believe the next chapter could rhyme with the one that made the stock compelling in the first place.

In this weekly stock study, we will look at and analyze the following indicators and metrics as are our guidelines which dictate our behavior on a particular stock.

- Wall Street Analysts’ Price Forecasts

- 52-week high and low boundaries

- Best Case – Worst Case Analysis

- Vantagepoint A.I. Predictive Blue Line

- Neural Network Forecast

- Daily Range Forecast

- Intermarket Analysis

- Our trading suggestion

While we make our trading decisions based upon the ai forecasts we receive within the VantagePoint A.I. software we do consider the fundamentals to better understand the risk and reward profile of $LULU.

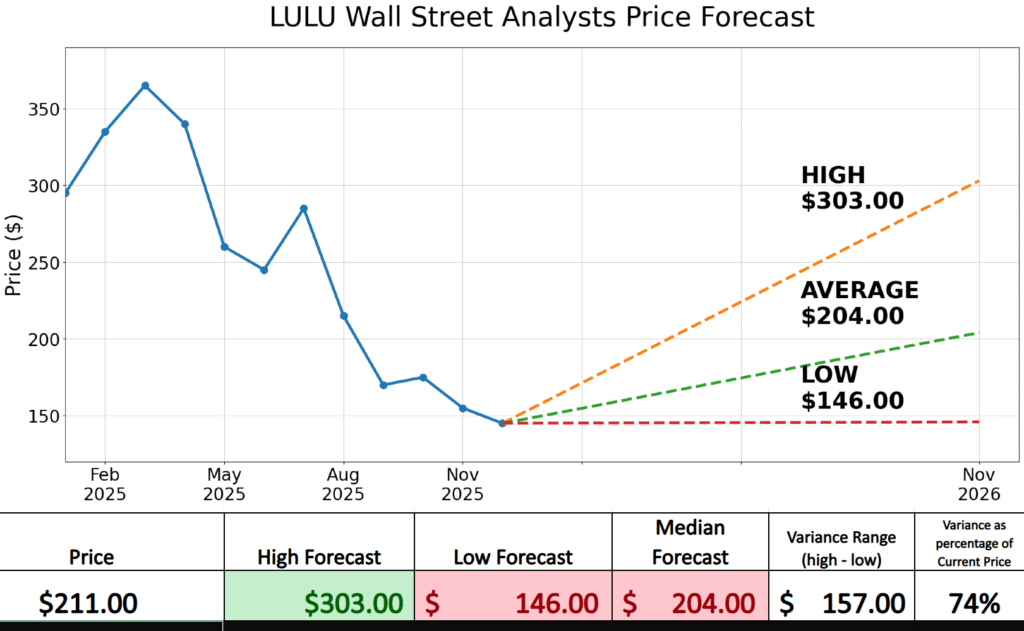

Wall Street Analysts Price Forecasts

What this chart captures is not conviction, but disagreement.

Based on 22 Wall Street analysts publishing 12-month price targets over the past three months, Lululemon Athletica sits at the center of an unusually wide forecast range. The average target is $204.00. The high-end view reaches $303.00. The low-end outlook falls to $146.00. That spread alone tells you most of what matters: analysts largely agree on the quality of the business, but not on how the next phase unfolds.

Start with the middle. The median forecast of $204.00 sits just below the current price, signaling hesitation rather than alarm. This is not a wholesale retreat from the stock. It’s a message that Lululemon must re-earn confidence after a period of slowing growth and tighter margins. The consensus reflects recalibration, not rejection.

Then there’s the upside case. The $303.00 high forecast assumes that margins hold, international growth — particularly in China — reaccelerates, and the brand’s pricing power remains intact despite intensifying competition. Analysts in this camp see recent weakness as cyclical, not structural, and believe the stock can reclaim its premium valuation if execution improves.

The $146.00 low forecast tells a different story. It reflects concern that demand normalizes, competition erodes differentiation, and the market permanently assigns Lululemon a lower multiple. This isn’t a collapse scenario. It’s a valuation reset argument, one that assumes excellence alone no longer guarantees premium pricing in a more cautious consumer environment.

What stands out most is the variance itself. A $157.00 spread between high and low forecasts, roughly 74% of the current share price, is striking for a company of this size. That dispersion signals uncertainty, not dysfunction. Wall Street is debating the direction of the story, not the viability of the business.

The takeaway is straightforward. When forecasts diverge this sharply, price action is driven less by averages and more by proof. Earnings, guidance, and execution will determine which narrative gains traction. This chart doesn’t predict where Lululemon will trade in a year. It maps the argument that will move the stock until then.

52 Week High and Low Boundaries

This 52-week chart of Lululemon Athletica tells a familiar market story, one that is less about fashion and more about psychology, expectations, and risk.

The two most important reference points on this chart are not indicators or moving averages. They are the boundaries. The 52-week high at $423.32 marks the point where optimism peaked. That level represents the market’s most aggressive view of Lululemon’s growth, margins, and brand momentum over the past year. When a stock is near its 52-week high, it signals confidence. Institutions are willing to pay up. Momentum traders are involved. Expectations are elevated. When price moves away from that level, it’s not just a technical retreat, it’s a reassessment of how much certainty investors are willing to assign to the story.

At the other end of the chart, the 52-week low at $159.25 defines the opposite extreme. That price marks the point where fear, disappointment, and uncertainty were fully priced in. It reflects the moment when the market collectively said, “We need proof.” For traders, this level matters because it represents exhaustion. Sellers who wanted out likely already left. Buyers stepping in near the 52-week low are not chasing narratives; they are betting on survival, stabilization, or mean reversion.

Together, these two boundaries form the stock’s annual trading range, and that range is more than just historical trivia. It is a real-world volatility benchmark. The distance between the high and the low shows how far the stock can travel when sentiment shifts. In Lululemon’s case, the range is wide, which tells you this is not a sleepy consumer staple. It’s a stock that reprices aggressively when expectations change. Traders use this range to size positions, set realistic targets, and manage risk. A move of $20 or $30 may feel dramatic day-to-day, but within a $260+ annual range, it’s context, not chaos.

As price moves back up from the lower boundary, the market is signaling something subtle but important. It’s not declaring victory. It’s testing whether the worst assumptions were too pessimistic. The 52-week range gives traders a map: where enthusiasm once lived, where fear took over, and how much movement history says is possible. In that sense, this chart is less about predicting the future and more about understanding the battlefield on which it will be fought.

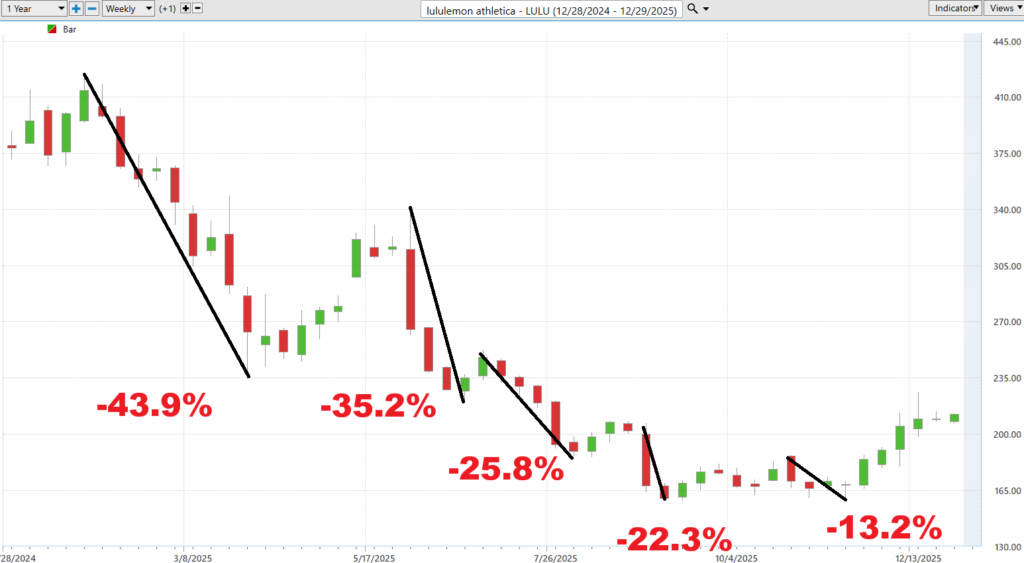

Best-Case/Worst-Case Scenario Analysis

If you really want to understand volatility, forget the fancy indicators and start with this: how far a stock can run without stopping, and how far it can fall without mercy. These charts show LULU’s largest uninterrupted rallies and declines, and they tell the truth faster than any formula ever will. A stock that can drop 40% without pausing is not “broken.” It’s volatile. And volatile stocks don’t whisper, they shout.

This workflow forces traders to understand what the expected and historic volatility means and puts real numbers on emotional pain and opportunity. Seeing a –43% decline or a +43% rally forces traders to confront what volatility means in dollars, not theory. It answers the only question that matters before you click buy: how much can this thing move against me before I’m forced to make a bad decision? The market doesn’t care about your feelings, but it will happily test them.

Here is the best-case analysis:

Followed by the worst-case analysis:

hat’s why traders do this before position sizing.

If you know the historical worst-case swings, you can size your trade, so a normal move doesn’t knock you out of the game. Volatility isn’t something to fear, it’s something to measure. And once you measure it this way, you stop guessing, stop overtrading, and start surviving long enough to let the odds work in your favor.

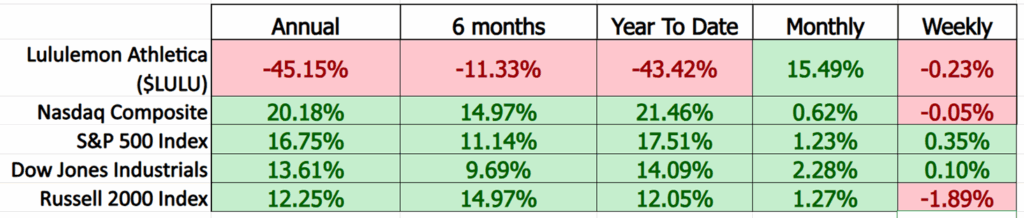

Next, we compare $LULU to the broader stock market averages:

This table is one of those uncomfortable mirrors traders don’t like to look into — but probably should. On an annual and year-to-date basis, Lululemon looks like it missed the party entirely. While the Nasdaq, S&P 500, Dow, and Russell 2000 were busy putting up respectable double-digit gains, LULU was doing the opposite — down sharply, and not in a subtle way. That’s underperformance, plain and simple, and it tells you institutions were voting with their feet.

But here’s where the story gets interesting. Zoom in. Monthly performance flips green. Suddenly $LULU is up over 15%, quietly outperforming everything else on the page. It tells you selling pressure may have run its course and buyers are starting to nibble again. Weekly numbers are flat, which is exactly what you want to see after a bounce, price catching its breath instead of giving it all back.

This is how leadership changes hands in the market. Big losses don’t disqualify a stock forever, they reset expectations. When something that badly lagged starts outperforming on shorter time frames, traders take notice. Not because the past suddenly looks better, but because the future might look different. This table doesn’t say “buy.” It says, “pay attention.” And in trading, that’s often where the real opportunities begin.

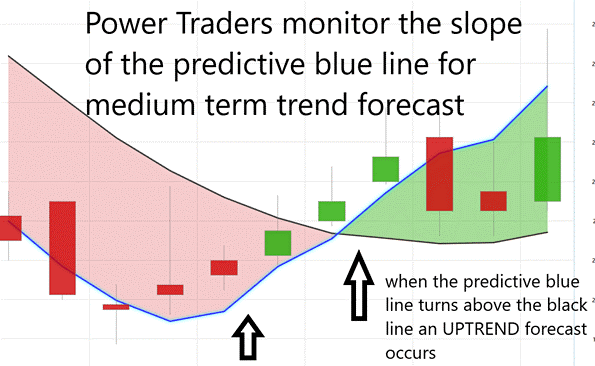

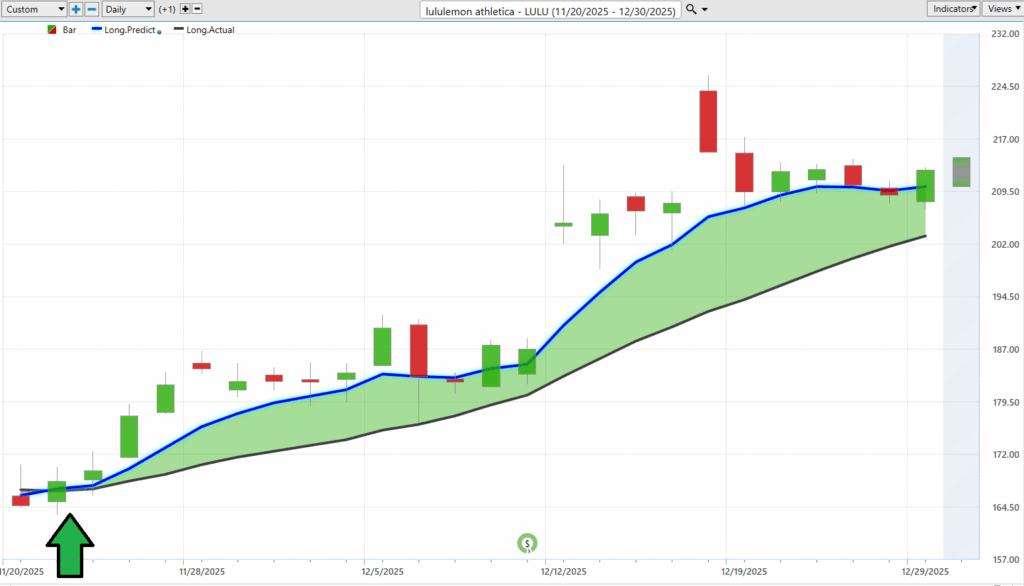

VantagePoint A.I. Predictive Blue Line

The Predictive Blue Line has one main job. Its primary job is to keep you from doing the one thing traders are best at — arguing with the market. The first rule is simple: pay attention to the slope. When the blue line turns up, it’s telling you the path of least resistance is higher. That doesn’t mean buy everything in sight. It means stop fighting the tape. A rising slope says momentum is shifting. A falling slope says risk is increasing. Most traders ignore this part and jump straight to conclusions. That’s how tuition gets paid.

A slope change is an early warning system. It’s the market clearing its throat before saying something important. When the slope flips from down to up, it tells you selling pressure is easing and accumulation may be starting. This is where traders stalk, not pounce. You reduce bearish exposure, tighten stops, and prepare. It’s a heads up, not a green light. Think of it as the weather forecast changing from storms to clouds. You don’t throw a beach party yet, but you stop boarding the windows.

The crossover is different. A crossover is confirmation. When price crosses above the Predictive Blue Line, the market isn’t hinting anymore — it’s declaring. That’s where trend traders act with more confidence because risk is now defined. Below the line, you’re defensive. Above it, you’re constructive. The key is understanding the sequence: slope change first, crossover second. Traders who respect that order stop guessing bottoms and start trading trends. And that, often, is the difference between surviving the market and becoming one of its cautionary tales.

VantagePoint A.I. Neural Index (Machine Learning)

A neural network for trading is a machine that studies the market the way an experienced trader would by remembering what happened before and recognizing when similar conditions begin to appear again. It evaluates price, trend, volatility, and time, then weighs those inputs based on historical outcomes. Instead of reacting emotionally to every red or green bar, the neural network asks a steadier question: given what has happened in comparable situations, what tends to follow?

The primary advantage is not prediction in the crystal ball sense. It is context. A neural network does not panic on bad news or become euphoric on good headlines. It measures probability by identifying repeating patterns that persist in markets even as the reasons behind them change. Because it continuously updates its calculations, it can recognize shifts in trend earlier than most traders who are anchored to opinions, narratives, or recent price action.

For traders, the benefit is discipline. Neural networks help define trend direction, identify higher probability trading windows, and reduce guesswork. They do not replace judgment. They refine it. Used correctly, they keep traders aligned with momentum, aware of risk, and out of the habit of fighting price. In markets that reward consistency and punish stubbornness, this approach is not an edge. It is a requirement.

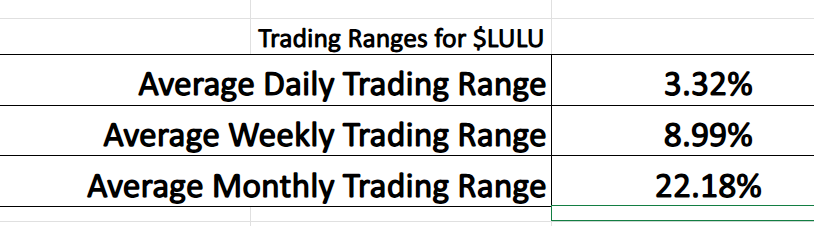

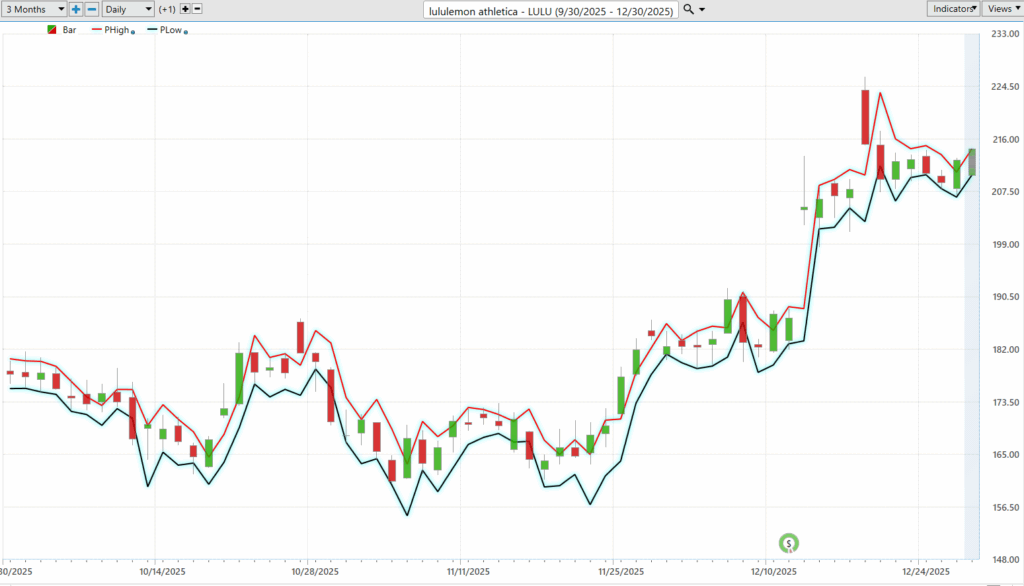

VantagePoint A.I. Daily Range Forecast

Every trader wakes up each morning asking the same two questions, whether they admit it or not: How far can this thing move today, and how much pain can I survive if I’m wrong?

The first graphic answers that question with uncomfortable honesty.

$LULU doesn’t tiptoe.

On average it moves over 3% in a single day, nearly 9% in a week, and more than 22% over a month. That’s not trivia. That’s the price of admission. Those numbers define the battlefield. If you don’t respect them, the market will teach you respect the expensive way.

The second graphic shows what those statistics look like in real time. The VantagePoint A.I. Daily Range Forecast isn’t guessing direction. It’s defining where opportunity and risk live today. The projected high and low bands act like guardrails, reminding traders that price rarely moves at random. It stretches, it pauses, it snaps back. When price pushes toward the upper boundary, opportunity starts giving way to risk. When it sinks toward the lower boundary, fear replaces logic and opportunity quietly shows up. This is how professionals stop chasing and start positioning.

Put the two together and the message is clear. Volatility is not something to fear. It’s something to measure. The VantagePoint A.I. Daily Range Forecast takes abstract movement and turns it into a practical framework traders can use every single day. It doesn’t promise certainty. It delivers context. And in a market that moves as fast as $LULU does, knowing where risk and opportunity live is not an advantage. It’s the difference between trading with intention and trading on hope.

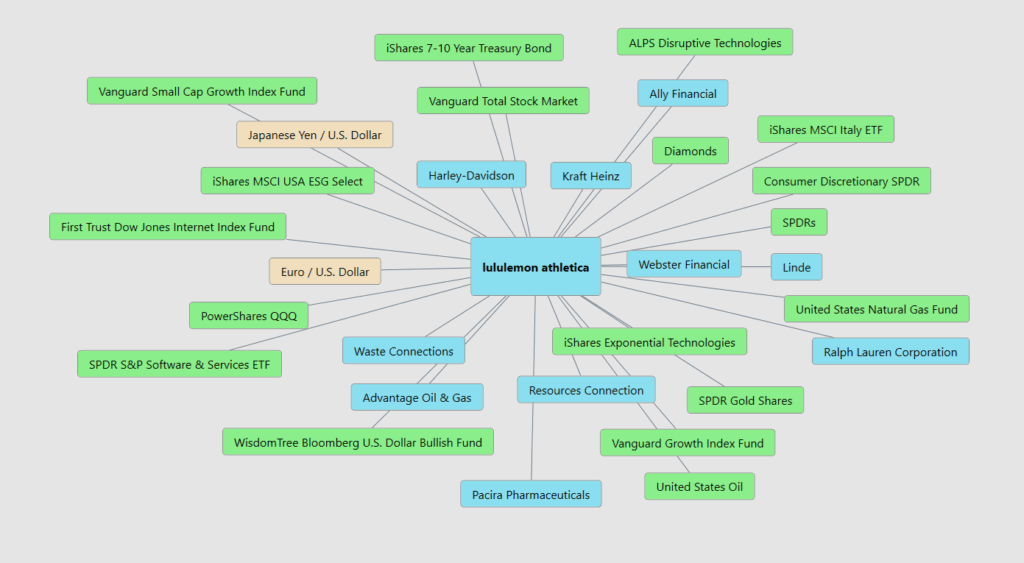

Intermarket Analysis

$LULU is sitting at the center of a web of forces that tug on it every single day. Bonds, stocks, currencies, commodities, sectors, and sentiment all run straight through this company whether management likes it or not. When Treasury bonds push higher and yields rise, that line running from interest rates to $LULU tightens. Higher borrowing costs don’t just slow housing and autos, they quietly siphon discretionary dollars away from premium yoga pants. That’s why the bond market matters. It’s the early warning system that tells you when consumers are about to start saying “maybe later” instead of “add to cart.”

Now follow the connections out into commodities and energy. Cotton, oil, and industrial inputs don’t show up on a Lululemon balance sheet as line items, but they show up in margins fast enough to make investors nervous. When oil spikes, synthetic fabrics get more expensive. When agricultural prices jump, natural fibers follow. That’s why those links to energy funds, resource plays, and even gold matter. They’re not academic. They’re telling you whether input costs are becoming a headwind or a tailwind. When commodities cool, $LULU breathes easier. When they surge, pricing power gets tested and margins start doing gymnastics.

Then there’s the currency layer, quietly sitting in the background like gravity. Lines running through the U.S. dollar, the euro, and the yen explain why international growth can look great one quarter and disappointing the next without anything changing on the ground. A strong dollar shrinks overseas profits when they come home. A weaker dollar does the opposite. With $LULU’s global footprint expanding, especially in Asia, currency trends stop being footnotes and start becoming drivers. The takeaway is simple. This chart reminds traders that $LULU doesn’t trade on leggings alone. It trades at the intersection of rates, resources, currencies, and risk appetite. Connect those dots early, and the stock makes a lot more sense. Ignore them, and you’ll spend the next cycle wondering why price moved when “nothing happened.”

Our Suggestion

Across the last two earnings calls, management’s tone has shifted from defensive to measured confidence, but not outright victory laps. On the earlier call, leadership acknowledged slowing growth in North America, heavier promotional activity across retail, and pressure on discretionary spending. Guidance was trimmed, language became cautious, and management focused heavily on execution, inventory discipline, and protecting margins rather than chasing growth at any cost. That call landed poorly with Wall Street. The message was essentially, “The brand is strong, but the consumer is wobbling,” which traders translated as, “Expect volatility.”

The most recent earnings call felt steadier. Management emphasized stabilization rather than acceleration. Inventories were cleaner, markdowns more controlled, and international growth, particularly in China, remained a bright spot. Margins were framed as resilient given the environment, not expanding, but holding. The messaging was tighter and more deliberate. Instead of explaining what went wrong, management spent more time explaining what they are doing now. That tonal shift matters. It doesn’t scream growth reacceleration, but it does suggest the worst-case narrative is losing traction.

Confidence, however, is still conditional. Management is not claiming they are back on a hypergrowth path. They are claiming discipline. Goals are being met operationally, but financial targets are now framed as ranges, not promises. This is a company prioritizing control over ambition, which Wall Street tends to respect after a reset. Traders hear this as, “Downside risk is better defined.”

The influence of founding CEO Dennis “Chip” Wilson has added an important psychological layer, even without a formal return to day-to-day leadership. His renewed visibility and involvement have shifted the conversation. Founders change tone simply by existing in the room. Wall Street interprets this as cultural gravity pulling the company back toward its roots: product obsession, margin discipline, and brand integrity. Management language has subtly reflected this, leaning more on first principles and less on macro excuses.

Wall Street’s feedback has followed suit. Analysts are no longer debating whether the brand is broken. The debate has moved to how fast growth can re-normalize and how much margin is structurally defendable. Price targets remain widely dispersed, which tells you conviction is still forming, but downgrades have slowed. Questions on calls have shifted from “What went wrong?” to “What would change your outlook?” That’s a meaningful transition.

The key takeaways from the last two earnings calls are straightforward. First, the reset is real and largely priced in. Second, management is executing better, even if growth remains uneven. Third, the founder’s presence has improved narrative clarity and confidence, even if it hasn’t magically fixed the macro environment. And finally, Wall Street is no longer panicking, but it is still watching closely. For traders, that’s often the zone where trends begin to form before headlines catch up.

Our suggestion is that you should place $LULU on your trading radar. The stock has rallied sharply off the 52-week lows.

It will provide numerous trading opportunities in the coming year.

Use VantagePoint A.I. Daily Range forecasts to isolate short-term trading opportunities.

It’s not magic.

It’s machine learning.

Disclaimer: THERE IS A HIGH DEGREE OF RISK INVOLVED IN TRADING. IT IS NOT PRUDENT OR ADVISABLE TO MAKE TRADING DECISIONS THAT ARE BEYOND YOUR FINANCIAL MEANS OR INVOLVE TRADING CAPITAL THAT YOU ARE NOT WILLING AND CAPABLE OF LOSING.

VANTAGEPOINT’S MARKETING CAMPAIGNS, OF ANY KIND, DO NOT CONSTITUTE TRADING ADVICE OR AN ENDORSEMENT OR RECOMMENDATION BY VANTAGEPOINT AI OR ANY ASSOCIATED AFFILIATES OF ANY TRADING METHODS, PROGRAMS, SYSTEMS OR ROUTINES. VANTAGEPOINT’S PERSONNEL ARE NOT LICENSED BROKERS OR ADVISORS AND DO NOT OFFER TRADING ADVICE.