Nineteen days into a war filled with missiles, drones, and enough expensive hardware to make a Pentagon accountant weep, the most dangerous weapon turned out to be a sentence.

Iran suggested that oil tankers could pass through the Strait of Hormuz again, provided the cargo is paid for in Chinese yuan instead of U.S. dollars.

Four words that landed harder than any missile strike, because they were aimed at something far more fragile than ships or soldiers.

They were aimed at money.

Paid for in yuan.

For decades, the system has been simple. Oil trades in dollars. The world needs dollars. The United States sits at the center of that flow. Now, in the middle of a war, a country controlling the most important oil choke point on earth is offering access on different terms.

That is not a military maneuver.

That is a change to the rules.

Let’s strip this down.

The Strait of Hormuz is a narrow stretch of water between Iran and Oman, about 33 kilometers wide at its tightest point. Through it flows roughly 20 million barrels of oil per day, nearly one-fifth of global supply.

Oil does not reroute easily. It moves through fixed infrastructure, and when one of the main arteries tightens, the system reacts immediately. Alternatives exist, but they are limited. Pipelines cannot replace the volume. Storage buys time, not solutions.

So, when uncertainty enters the equation, markets do what they always do.

They price risk, not reality.

If Hormuz becomes unstable, oil does not drift higher. It moves fast. And because oil sits underneath transportation, manufacturing, and food production, that move ripples across the entire economy.

Control of Hormuz is about price.

To understand why this matters, you must go back to 1971.

That was the year President Richard Nixon ended the dollar’s convertibility into gold. The old system disappeared overnight. What replaced it was something more subtle and, ultimately, more powerful.

In 1974, the United States reached an agreement with Saudi Arabia. Oil would be priced in U.S. dollars, and in return, the United States would provide security guarantees. Over time, the rest of OPEC followed.

That decision rewired global finance.

Every country that needed oil now needed dollars first. Those dollars were then recycled into U.S. Treasuries, helping finance American deficits at scale. Energy demand supported the dollar. The dollar supported U.S. borrowing. That borrowing supported both domestic spending and global influence.

It was not just a system.

It was a feedback loop.

And for 50 years, it held.

We have seen attempts to challenge this before.

Iraq tried shifting oil pricing away from dollars. Libya explored a gold-backed alternative. Venezuela moved toward non-dollar trade. Each effort failed for the same reason.

They were alone.

What makes this moment different is not the idea. It is the alignment.

Iran controls a critical choke point. China, the world’s second-largest economy, has spent years building infrastructure for yuan-based energy trade. And this is happening during a real supply disruption, not a theoretical debate.

That combination changes behavior.

If you are an energy importer, you are not making a philosophical decision. You are making a practical one. You need oil. If oil flows in yuan, you adapt.

This is how structural shifts happen.

Not with announcements.

With transactions.

Currencies do not collapse all at once.

They weaken at the margins.

The real risk is not that the U.S. dollar disappears. It is that the world discovers it has alternatives. One shipment settles in yuan. Then another. Then a pattern forms.

And once a pattern becomes repeatable, markets do not debate it.

They price it.

Fast.

The question is what happens when global demand for dollars becomes less automatic.

Because even a small change in demand can have large consequences.

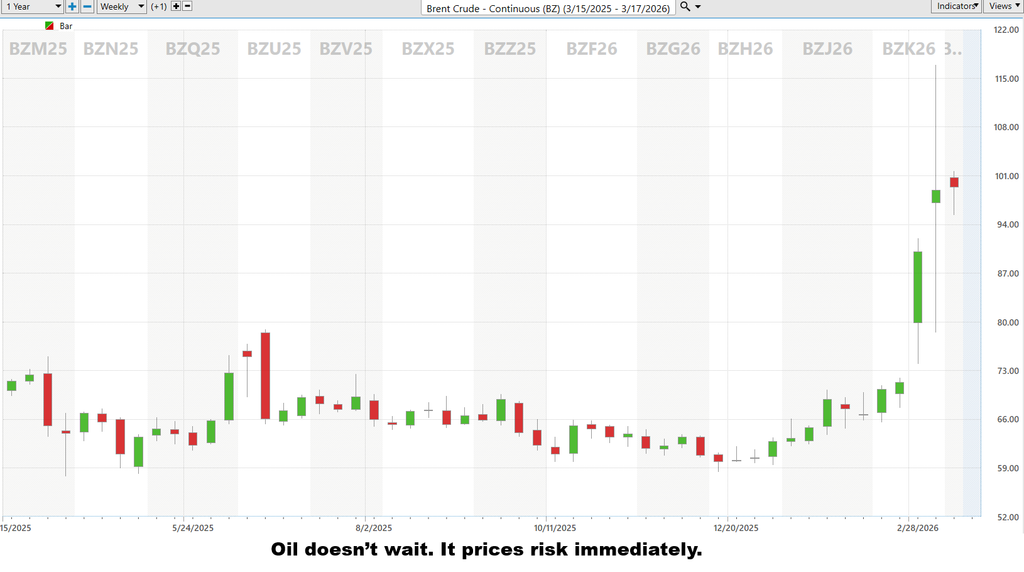

If you want to see this process in real time, start with oil.

Oil is always the first to react because it cannot wait. It reflects fear, logistics, and supply risk immediately. When uncertainty rises in Hormuz, traders act.

Insurance costs rise. Shipping behavior changes. Supply becomes uncertain not just because of production, but because of risk tolerance. That is when prices accelerate.

Brent crude moves. WTI follows. Energy equities respond.

Oil is not just another market.

It is the signal.

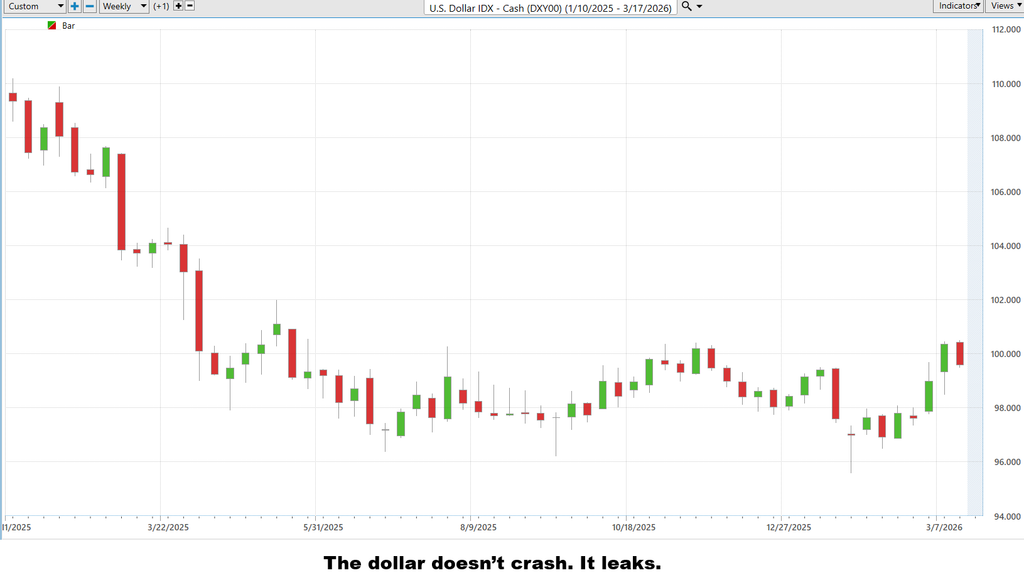

After oil, watch the U.S. dollar.

Oil reflects supply. The dollar reflects trust.

For decades, global demand for dollars has been embedded in energy markets. But if even a portion of that trade shifts to another currency, the flow changes. Countries hold fewer dollars. Reserve strategies evolve. Treasury demand adjusts.

This is erosion. And markets price erosion long before it becomes obvious.

The U.S. Dollar Index (DXY) does not need to break down dramatically. It only needs to lose its structural tailwind.

That is what traders watch next.

When confidence begins to shift, capital looks for something it cannot be diluted.

That is where Gold comes in.

Gold does not move quickly, but it moves with purpose. It represents stability when systems feel uncertain. Central banks understand this, which is why they return to it when pressure builds.

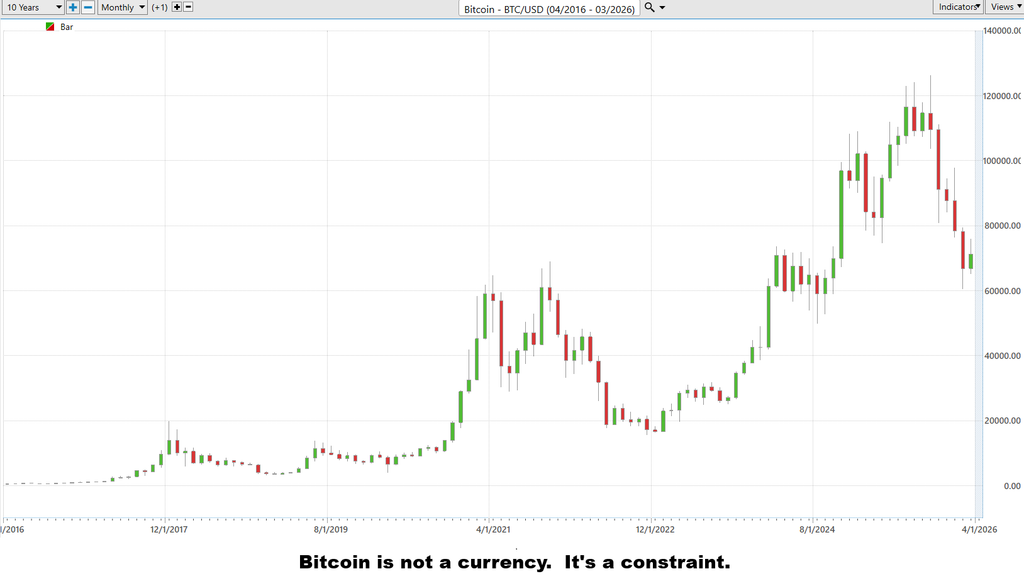

Then there is Bitcoin.

Different behavior. Same core appeal.

It cannot be printed.

In a world where currencies are being questioned and financial systems are evolving, that constraint matters. Investors do not need to agree on philosophy. They only need to recognize scarcity.

So, capital is reallocated. Some flows into Gold. Some into Bitcoin.

Not because investors change beliefs.

Because they change priorities.

What is unfolding here is not a single market event.

It is a coordinated shift.

Energy prices move higher. The dollar faces pressure at the margin. Hard assets begin to attract capital. These are not isolated reactions. They are connected signals.

This is how macro cycles begin.

And when these signals align, markets reprice.

For traders, this is where opportunity exists.

But only for those paying attention early.

The real risk here is not that one oil shock suddenly turns the United States into some historical museum exhibit of bad monetary policy. We are not waking up tomorrow pushing wheelbarrows of cash to buy a sandwich. The numbers do not support that kind of drama.

As of early 2026, CPI is running in the mid-twos, which is about as exciting as a government spreadsheet can get. But oil is not a polite, well-behaved inflation problem. Oil is the economic equivalent of spilling coffee on the entire operating system. It hits transportation, food, manufacturing, and household budgets all at once, and it does it without asking permission from economists.

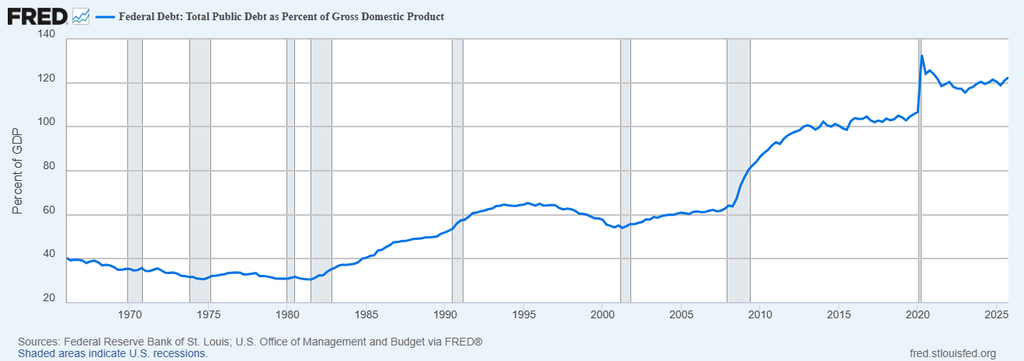

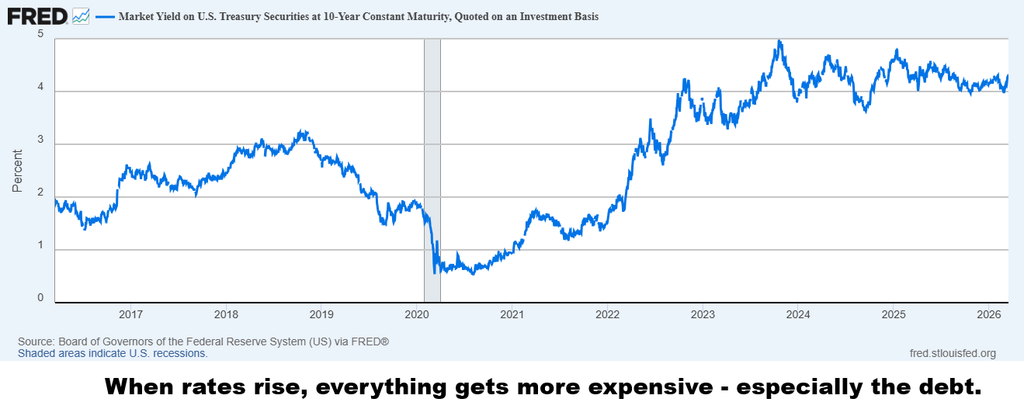

Now layer that on top of a government that already spends like a teenager with a new credit card. The Congressional Budget Office is projecting a deficit pushing $1.9 trillion, with debt sitting around 121% of GDP and climbing. Interest payments are no longer a footnote. They are becoming one of the main events. Which means the United States is not just running a large balance sheet. It is running a large balance sheet at interest rates that matter again. And when rates matter, small changes stop being small.

This is where things get uncomfortable. The U.S. just surpassed $39 trillion in cumulative debt. If foreign buyers decide they are a little less enthusiastic about loading up on U.S. Treasuries, the system must adjust. Either yields rise to attract new buyers, or someone else steps in to keep the show running. And by “someone else,” we mean the same institution that has a long and well-documented history of stepping in when things get awkward. The data does not show foreigners running for the exits yet. But markets do not need panic to get interesting. They just need hesitation.

So now imagine the setup. Oil prices are rising. Inflation stops behaving. Deficits are large. Treasury issuance is heavy. And the market starts asking, politely at first, whether it really wants to absorb all that Treasury supply at current prices. This is usually the moment when policymakers rediscover their favorite tool. It hums. It whirs. It occasionally goes “brrrrrr” in the background while everyone pretends this is a sophisticated form of economic management.

The issue is what the decision signals. When monetary policy starts leaning in to support fiscal reality, investors notice. They may not protest loudly, but they adjust quietly. The Federal Reserve’s balance sheet is still enormous by historical standards and expanding it again during an oil-driven inflation scare does not scream “we are firmly in control.” It suggests the priorities may be shifting.

That is how confidence changes, in a series of small realizations. Maybe you demand a little more yield to hold long-term debt. Maybe you diversify reserves. Maybe you stop assuming the dollar automatically solves everything. None of this requires panic. It just requires a slightly different set of assumptions.

Of course, there is another option. Let rates rise and defend the currency the old-fashioned way. That sounds responsible right up until you remember that higher rates make everything more expensive for everyone, including the government itself. Interest costs rise. Refinancing becomes painful. Housing slows. Credit tightens. Asset prices wobble. In other words, you fix one problem by creating several new ones.

And that is the trap. The more debt you have, the fewer good choices you get. You can lean into higher rates and stress the system, or you can lean into accommodation and gently remind everyone that the currency supply is, shall we say, flexible.

So no, this is not a hyperinflation story. It is something far more modern and far more familiar. An oil shock feeds inflation. Inflation complicates policy. Deficits expand. Treasury supply increases. And policymakers are left to choose between higher yields or a little more help from the printing press.

For traders, that is not a doomsday script. It is a roadmap.

Because when oil is rising, policy is constrained, and the monetary spigot starts making noise again, markets do not sit still.

They adjust.

Markets tend to ask the loud questions.

Is the U.S. dollar collapsing?

That is the wrong question.

The better question is quieter.

What happens if the world needs fewer dollars?

Not zero. Just less.

Because that is how systems evolve. First comes the workaround. Then repetition. Then normalization. By the time it feels obvious, it is already priced in.

In this article, we have explored a series of scenarios. Some are plausible. Some are already unfolding. Others will prove incorrect. That is the nature of markets. They are not governed by certainty, but by probability. And even the most intelligent analysis, when filtered through human emotion, is prone to error.

This is precisely why VantagePoint artificial intelligence trading software has become indispensable.

The modern market is no longer a place where instinct alone can compete. It is a battlefield of data, speed, and pattern recognition. Millions of variables move simultaneously. Correlations form and break in real time. And by the time a human trader “feels” confident, the opportunity is often gone.

VantagePoint A.I. does not feel. It does not hesitate. It does not rationalize a bad position or fall in love with a narrative. It observes. It calculates. It adapts. And it does so continuously, without fatigue, bias, or distraction.

In a world where we have just outlined multiple possible futures, some of which will be right and some wrong, the advantage belongs to the system that can measure probability most accurately.

Now consider this.

If you ignore what the market is telling you, you are not merely late to the trade. You are late to the truth. Because the market is already making its decision about where capital flows next.

And at this moment, it is voting with remarkable clarity.

The question is not whether the market is moving.

The question is whether you are aligned where it’s moving ahead of everyone else.

Are you navigating today’s markets with predictive tools… or with opinions?

Are your decisions based on measurable probabilities… or on headlines, noise, emotions, and instinct?

Consider the possibility of a trading partner that does not tire, does not panic, and does not second-guess itself at the worst possible moment. Patented artificial intelligence trading software that processes vast amounts of market data, identifies patterns invisible to the human eye, and presents you with a forward-looking view of market direction.

This is not theory.

It is happening now.

There is an opportunity to observe this for yourself.

A live, online learn to trade with VantagePoint A.I. masterclass where you can discover how artificial intelligence analyzes markets in real time. Not through promises or predictions, but through demonstration. You will see how trends are identified earlier, how positions are managed with discipline, and how risk is controlled with precision.

No theatrics. No exaggeration.

Just the mechanics of how modern traders are gaining an edge.

The truth is simple.

Machines have already surpassed human performance in environments defined by probability, timing, and pattern recognition. The markets are no different. The question is not whether this shift is happening.

It is whether you choose to participate in it.

You can continue trading the way most people do. Or you can explore a more intelligent approach.

The choice is yours. Reserve your seat.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.