If you asked a thousand traders where Wall Street finds its next big winner, most would point toward a research report, an earnings forecast, a television interview, or perhaps a rumor whispered over an expensive steak dinner in Manhattan.

They would be wrong.

The biggest pools of capital in the world do not begin their search for opportunity with stories. They begin with performance.

Before an institution commits millions or billions of dollars to a stock, it asks a simple question:

“Is money already flowing into this asset?”

This may be the most important lesson an individual trader can learn.

Most traders spend their time searching for what is cheap, unpopular, or undiscovered. Institutions spend their time searching for what is working. They look for assets outperforming the market, outperforming their sector, making new highs, attracting capital, and demonstrating leadership. They understand a simple truth that many traders never fully appreciate:

Money leaves footprints.

Those footprints appear in relative strength, trend persistence, and performance leadership long before they appear in headlines.

Ironically, while institutions possess enormous resources, they also operate with enormous constraints. Their size often prevents them from acting quickly, investing in smaller opportunities, or changing direction rapidly. In many respects, the individual trader possesses advantages that some of the world’s largest money managers would gladly trade for.

The purpose of this article is to pull back the curtain on how institutional investors identify opportunity, what independent traders can learn from their process, and why understanding the behavior of institutional money could also improve your own decision-making.

Because in the stock market, success comes from recognizing where the money is already going.

When we talk about “institutions,” we’re not referring to some secret society meeting beneath the New York Stock Exchange by candlelight. We’re talking about the professional money managers who control enormous pools of capital: hedge funds, mutual funds, pension funds, insurance companies, sovereign wealth funds, endowments, and asset managers. They differ in their objectives, regulations, and investment styles, but they all share one common challenge: they have an astonishing amount of money to put to work. A retail trader may be deciding what to do with $10,000, $100,000, or even $1 million. An institution may need to deploy $500 million before lunch and another $500 million before dinner. That changes everything. It affects what they can buy, how quickly they can buy it, and even how they think about opportunity. While their strategies may differ, they are all engaged in the same relentless pursuit: finding places where capital can be allocated with the highest probability of producing attractive returns.

Institutional investors certainly have advantages. They have research departments, economists, analysts, consultants, lawyers, compliance officers, risk managers, conference rooms, subcommittees, and committees to oversee the subcommittees. In many cases they have enough bureaucracy to invade a small country. What it isn’t is nimble.

The public often confuses size with intelligence. A pension fund managing $100 billion sounds impressive until you realize it has the turning radius of an aircraft carrier. If a retail trader decides to buy 500 shares of a promising company, the trade can be completed before the trader finishes a cup of coffee. If a large institution wants to build a meaningful position, it may require weeks of planning, execution, and paperwork. By the time everyone signs off on the trade, the opportunity may have already moved on.

This is one of Wall Street’s best-kept secrets: size creates constraints. The very scale that gives institutions influence often robs them of flexibility. They cannot simply buy whatever they want. They must buy assets large enough to absorb hundreds of millions or even billions of dollars. Many of the market’s most exciting opportunities are simply too small for them to touch.

The individual trader has something many institutions desperately wish they had: agility. The ability to act quickly, adapt quickly, and focus on opportunities too small to attract Wall Street’s attention.

The purpose of this article is not to convince you that institutions are foolish. Far from it. Institutions have developed sophisticated methods for identifying opportunity, managing risk, and allocating capital. Traders can learn a great deal from their process. The goal is to understand how the professionals think, adopt what works, and then combine those lessons with the advantages that only an individual trader possesses.

Because the smartest traders don’t try to become institutions.

They learn to think like institutions while trading like individuals.

If you have spent any amount of time around Wall Street, you’ve probably noticed that the public has a romantic notion about how investment decisions are made. They imagine a room full of brilliant analysts pouring over spreadsheets, earnings estimates, economic forecasts, and industry reports, eventually emerging with a stock recommendation handed down from Mount Sinai.

The reality is far less glamorous.

The first thing institutions do is eliminate.

Imagine standing in front of a grocery store with 10,000 items on the shelves. You cannot possibly study every product. You need a process that quickly separates what deserves your attention from what doesn’t. Institutional investors face the same problem. The stock market contains thousands of publicly traded companies. No portfolio manager has the time, resources, or patience to investigate each one individually.

So they begin with a series of filters.

The first filter is usually performance. Before anyone studies a balance sheet or listens to a conference call, they want to know which stocks are already outperforming. Not outperforming because somebody on television likes them. Outperforming because money is actively flowing into them.

Wall Street likes to pretend it operates on grand theories, elegant economic models, and enough PowerPoint presentations to deforest a medium-sized country. In reality, the smartest institutions begin with a far simpler question: where is the money already being made? Before they worry about forecasts, valuations, or whatever explanation happens to be fashionable this week, they look at the scoreboard. Who are the biggest winners? Who are the biggest losers? Which sectors are attracting capital, and which ones are being abandoned like last year’s exercise equipment? Only after they identify the winners do they ask why. And even then, they treat the answer with suspicion. On Wall Street, “why” is usually just a story invented after the fact to explain what has already happened. The money is real. The performance is measurable. The explanation is often little more than a temporary working theory waiting to be replaced by the next one.

The next question becomes relative performance. Is the stock outperforming the S&P 500? Is it outperforming its sector? Is it outperforming its direct competitors? If a stock cannot beat its benchmark, it rarely earns a place on an institutional watchlist. Why spend time studying a laggard when leadership is already revealing itself elsewhere?

Once a stock passes those initial screens, institutions begin looking for confirmation. Revenue growth. Earnings growth. Expanding profit margins. Improving guidance. Strong balance sheets. These factors matter, but they are rarely the starting point. They are supporting evidence. Think of them as witnesses corroborating what price has already suggested.

This is where many traders get themselves into trouble. They start with the story and hope performance follows. Institutions typically do the opposite. They start with performance and then investigate the story. One approach asks, “What should be working?” The other asks, “What is actually working?” Those are very different questions.

As the screening process continues, the list becomes smaller and smaller. Thousands of stocks become hundreds. Hundreds become dozens. Dozens become a focused group of candidates worthy of deeper investigation. By the time a stock reaches this stage, it has already survived multiple rounds of scrutiny.

This process is illustrated in the graphic below. Notice what is absent from the funnel. There are no television appearances. No social media trends. No predictions about where a stock might trade five years from now. The process is remarkably practical.

The lesson for traders is straightforward. If the largest and most successful money managers in the world begin with performance, perhaps we should too. Instead of asking which stock has the most exciting story, a better question may be:

“Which stock is already proving itself in the marketplace?”

Because long before a stock becomes a Wall Street darling, it usually becomes a performance leader.

If institutional investors have a secret weapon, it isn’t superior intelligence. It isn’t a faster computer. It isn’t access to some mysterious information hidden from the rest of the market. Their edge is often much simpler than people imagine.

It’s relative strength.

Relative strength is simply a measurement of performance compared to something else. It answers a critically important question: compared to what? A stock may be up 15% this year, which sounds impressive until you discover the S&P 500 is up 25%. Conversely, a stock may be down 5%, but if its competitors are down 20%, it may actually be demonstrating leadership. Context changes everything.

This is one of the reasons institutions spend so much time measuring performance against benchmarks. They aren’t looking for stocks that are merely going up. They are looking for stocks that are going up faster than the alternatives.

Relative strength reveals where investors are choosing to place their trades. Think about it this way. Imagine two marathon runners approaching the finish line. Both are moving forward. Both are making progress. But one runner is steadily pulling away from the field. Which one deserves your attention?

In the financial markets, relative strength helps identify the runner separating from the pack. This is why institutional investors constantly compare stocks to the S&P 500, sector ETFs, industry groups, and direct competitors. They are searching for evidence that demand is stronger than average and that capital is flowing toward leadership rather than mediocrity.

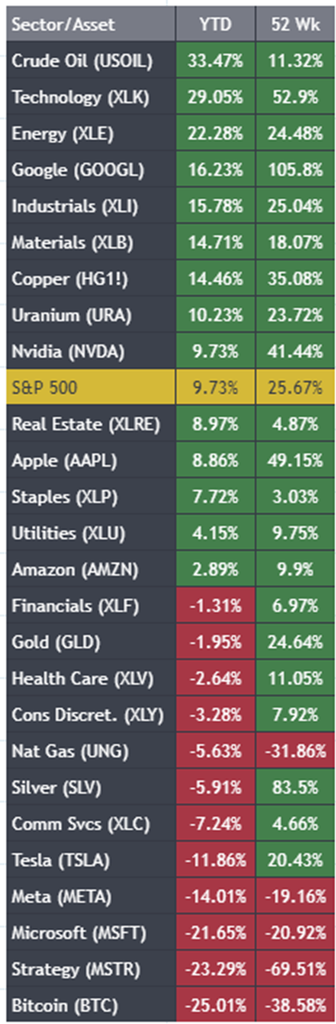

Institutional investors rarely begin by asking why. They begin by asking a far more practical question: who is winning and who is losing? The guide above provides a clear snapshot of which sectors, assets, and individual securities are outperforming the S&P 500 on both a year-to-date and 52-week basis. That alignment matters because institutional capital is naturally drawn toward demonstrated leadership. When an asset is outperforming across multiple time frames, it suggests that buyers are consistently willing to commit capital, reinforcing the trend and attracting even greater participation. In many respects, the market functions as a giant voting machine, and those assets receiving the strongest and most persistent votes tend to capture the majority of institutional attention, research coverage, and investment dollars.

A stock outperforming its peers is often telling you something important. It may be benefiting from superior management, stronger earnings growth, better industry conditions, or simply greater institutional demand. Whatever the reason, the market is signaling that capital prefers this asset over the alternatives. Institutions pay attention because money has a way of revealing information before headlines do.

One of the biggest mistakes traders make is assuming that a stock must be “cheap” before it can become attractive. Institutions often take the opposite view. A stock demonstrating exceptional relative strength is frequently placed at the top of the research pile, not the bottom. Strength attracts attention, attention attracts capital, and capital attracts more buyers.

The cycle can become remarkably self-reinforcing. This brings us to one of the most important observations in the market:

Winners keep winning.

Not forever. Not in a straight line. But far more often than most investors realize.

This is not because institutions enjoy chasing prices. It is because institutions are in the business of allocating capital toward what is working. Their mandate is not to find the most interesting story. Their mandate is to find the strongest opportunities.

The takeaway for traders is simple. Start asking which stock is outperforming its benchmark, its sector, and its competitors. Relative strength will not predict the future with certainty, but it often reveals where institutional money is already placing its confidence.

And in the markets, confidence has a funny way of becoming momentum.

Few concepts in investing are more misunderstood than a stock making a new high. Most investors see a stock at a new 52-week high or a new 10-year high and immediately assume the opportunity has already passed. The stock looks expensive. It feels late. Human nature encourages us to search for bargains, not records.

Institutional investors often reach the opposite conclusion.

A stock does not accidentally climb to a new high. Along the way it has encountered profit takers, skeptics, short sellers, earnings reports, economic uncertainty, and countless opportunities to fail. Yet buyers have continued stepping in at progressively higher prices. The market has conducted an extended voting process, and the verdict has been overwhelmingly positive.

For institutions, a new high is evidence that demand is exceeding supply. More importantly, it often signals that a company is doing something exceptionally well. A stock reaching a new 10-year high has survived recessions, interest rate cycles, competitive threats, and market corrections. It has not merely survived. It has demonstrated leadership over an extended period of time.

New highs also eliminate one of the market’s greatest obstacles: resistance. Investors who bought at lower levels are generally sitting on gains, not losses. There are fewer trapped shareholders waiting to sell simply to break even. That allows strong trends to continue developing as institutional money accumulates positions over time.

This is why many of the market’s greatest winners spend years making one new high after another. They rarely look cheap. In fact, they often appear expensive throughout much of their advance. What institutions understand is that sustained leadership rarely occurs by accident. A company making a new high has often earned that valuation through superior execution, stronger earnings, growing market share, or persistent institutional demand.

The lesson for traders is simple. Do not automatically dismiss a stock because it is making a new high. Ask why. Ask what is driving institutional demand. Ask why capital continues choosing this company over thousands of alternatives.

Because sometimes the market’s most important opportunities are not hiding among the biggest losers.

They are hiding in plain sight, at new highs, where leadership is already revealing itself.

Here’s a painful truth that most traders eventually discover after donating enough money to Wall Street to put a broker’s kid through college: the market doesn’t care about your story. It doesn’t care how exciting the company sounds, how charismatic the CEO is, or how many podcasts, television appearances, and social media posts are devoted to the stock. Stories can attract attention, but attention alone does not move markets. Money moves markets.

To be fair, stories do matter. Every great company has a story. Every major innovation has a story. Every bull market is built around a story that captures investors’ imagination. The problem is that many traders become so fascinated by the narrative that they stop paying attention to what the market is actually saying.

Consider two companies operating in the same industry. One stock is making new highs, growing earnings, attracting institutional money, and outperforming its competitors. The other stock is struggling, missing expectations, and lagging the broader market. Now imagine the weaker company has the more exciting story, receives more media coverage, and generates far more investor excitement.

Which company do you think institutions favor?

The answer reveals a great deal about how professional money managers think. Institutions follow evidence. Retail traders often follow excitement. The market has a long history of rewarding evidence while punishing investors who confuse a compelling narrative with a profitable investment.

In fact, the history of Wall Street is filled with wonderful stories that produced disappointing returns. Every speculative bubble was built on a narrative that sounded convincing at the time. The internet was going to change everything. Bitcoin is going to change everything. Artificial intelligence is going to change everything. In many cases, those stories were correct.

But being right about a story and making money from it are two very different things.

The institutions that consistently outperform understand this distinction. They are not paid to be entertained. They are not paid to make bold predictions about the distant future. They are paid to allocate capital efficiently. That means they need evidence that money is actually flowing into an asset before they commit meaningful resources.

Notice what all of these examples have in common. They are observable. They are measurable. They are happening in real time. The market is already revealing where buyers are placing their money and where confidence is building.

This is why some of the greatest traders in history became obsessed with price. Not because price predicts the future, but because price reveals what is happening right now. The trend is a report card. And report cards tend to be far more reliable than promises.

For traders, the lesson is straightforward. Listen to the story. Study the company. Understand the business. But before risking a single dollar, ask yourself one simple question:

Does the trend agree with the story?

Because when the story and the trend disagree, institutions almost always trust the trend. More often than not, that decision proves to be the correct one.

For decades, individual investors have been told that Wall Street possesses an insurmountable advantage. The institutions have bigger research departments, bigger computers, bigger budgets, and access to more information. There is some truth in that assessment. But there is another truth that receives far less attention. The most successful institutions follow a handful of simple principles that any trader can adopt immediately.

This mindset changes everything. Instead of asking, “Will this trade work?” institutions ask, “Do I have an edge?” That subtle shift encourages discipline, risk management, and objectivity. It also eliminates much of the emotional decision-making that causes traders to abandon sound strategies at precisely the wrong time.

The important lesson is to follow capital flows. Markets are ultimately voting machines. Every day, billions of dollars move from one asset class to another, from one sector to another, and from one stock to another. Institutions pay close attention to these flows because they reveal where confidence is increasing and where confidence is deteriorating.

This brings us to perhaps the most valuable lesson of all: risk comes first. The public often assumes that professional investors spend most of their time searching for the next big winner. In reality, many spend just as much time thinking about what could go wrong. They understand that preserving capital is a prerequisite for compounding capital.

The great irony is that none of these lessons require a billion-dollar fund, an Ivy League degree, or a corner office overlooking Manhattan. They require discipline. They require patience. They require the willingness to focus on evidence instead of opinions. These are skills available to every trader willing to develop them.

The graphic below summarizes many of the advantages institutions seek when evaluating opportunities. Yet the real value is not found in copying every institutional process. It is found in understanding the principles behind those processes. Follow performance. Measure relative strength. Think in probabilities. Follow capital flows. Respect risk.

Do those things consistently, and you will already be thinking more like Wall Street than most of Wall Street’s customers.

There is a curious belief on Wall Street that bigger is always better. Bigger funds, bigger research departments, bigger trading desks, and bigger budgets are assumed to create better results. Yet in investing, as in many areas of life, size often brings its own set of problems. The larger an institution becomes, the more difficult it becomes to move quickly, adapt to changing circumstances, and take advantage of smaller opportunities.

Individual traders should not underestimate the significance of this fact.

Imagine you are managing a $100 billion pension fund. If you discover an attractive company with a market capitalization of $2 billion, you may not be able to buy enough shares to make a meaningful difference in your portfolio. Even if the company doubles, the impact on overall performance may be negligible. For the individual trader, however, that same opportunity could be highly rewarding. Many of the market’s greatest winners spent years as companies too small to attract serious institutional attention.

This leads to one of the retail trader’s greatest advantages: flexibility. An individual trader can buy almost any publicly traded company with the click of a button. Institutions often cannot. They must consider liquidity constraints, position limits, regulatory requirements, and the practical challenge of deploying enormous amounts of capital. What appears to be a simple decision for a retail trader can become a complex operation for a large institution.

The absence of bureaucracy is more valuable than many investors realize. Institutions often operate by committee. Committees can be useful because they reduce impulsive decision-making. They can also be problematic because they tend to produce consensus. And consensus rarely discovers exceptional opportunities before everyone else.

Another advantage enjoyed by retail traders is the freedom to concentrate. Most institutions are required to diversify across dozens or even hundreds of positions. Diversification serves an important purpose, particularly when managing other people’s money. But exceptional investment returns often come from a small number of outstanding decisions. Individual traders have the ability to focus their capital on their highest-conviction ideas.

Time horizon may be the most underrated advantage of all. Institutional managers are often judged quarterly. Some are judged monthly. Their clients, boards, and shareholders demand regular explanations for every fluctuation in performance. Individual traders answer to no one but themselves. They can ignore short-term noise and allow a successful investment thesis to unfold over years rather than weeks.

This does not mean retail traders are destined to outperform institutions. The freedom enjoyed by individual investors can easily become a disadvantage when combined with impatience, excessive trading, or poor risk management. Flexibility is only valuable when exercised with discipline.

The graphic below highlights several areas where individual traders possess meaningful advantages over institutional investors. Notice that none of these advantages involve superior information. None require advanced degrees or sophisticated trading systems. They stem from something much simpler: the ability to act without the constraints imposed by size.

This is one of the great ironies of investing. Many retail traders spend years wishing they had the resources of a large institution, while many institutions would gladly trade some of those resources for greater agility. The challenge is not becoming a billion-dollar fund manager. The challenge is recognizing and exploiting the advantages you already possess.

Warren Buffett has often observed that managing a small amount of capital is far easier than managing a large amount of capital. In fact, he has repeatedly suggested that if he were managing a much smaller portfolio today, he could likely achieve significantly higher returns. The reason is straightforward. Smaller investors can pursue opportunities that are simply too small to matter to large institutions.

The lesson for traders is clear. Learn from Wall Street’s discipline. Learn from its emphasis on performance, relative strength, and risk management. But never forget that individual traders possess advantages that even the largest institutions cannot buy. When combined with patience, sound judgment, and a willingness to follow evidence rather than emotion, those advantages can become extraordinarily powerful.

Spend enough time around Wall Street and you begin to notice something curious and the evidence typically follows a familiar pattern.

Strong assets tend to attract capital. Strong businesses tend to attract investors. Strong trends tend to attract additional participation. This does not mean every winner keeps winning forever. It simply means that leadership is rarely random. Before institutional money commits billions of dollars to an opportunity, it usually wants evidence that the opportunity is already demonstrating strength.

This brings us to what might be called the Institutional Playbook. It is not a secret formula. It is a framework for making decisions in an uncertain world. The first question is whether the asset is outperforming its benchmark. The second is whether it is outperforming its peers. The third is whether the trend is strengthening or weakening. Only after those questions are answered does deeper analysis begin.

Notice what is absent from this process.

There is no requirement to predict where a stock will trade five years from now. There is no requirement to identify the next revolutionary technology before anyone else. There is no requirement to be the smartest person in the room. The process is designed to identify probabilities, not certainties.

Perhaps the most important part of the playbook is risk management. Great investors understand that capital is finite. Every investment decision involves opportunity cost. Every dollar allocated to one idea cannot be allocated elsewhere. This is why successful investors spend so much time evaluating risk. They understand that avoiding large losses is often just as important as capturing large gains.

For traders, the practical application is remarkably straightforward. Before entering any position, ask a series of simple questions. Is this asset outperforming the market? Is it outperforming its sector? Is capital flowing toward it or away from it? Is the trend improving across multiple timeframes? And perhaps most importantly, what would cause me to admit I am wrong?

These questions may not sound revolutionary. They are not supposed to be. The most effective investment frameworks are often surprisingly simple. Complexity frequently creates the illusion of sophistication while obscuring the factors that matter most.

The lesson from studying institutional investors is not that they possess secret information. The lesson is that they operate within a disciplined framework. They follow evidence. They monitor performance. They respect risk. They remain flexible when facts change. And they understand that the market’s strongest opportunities often reveal themselves through their behavior long before they become obvious in the headlines.

That is the essence of the institutional playbook. Not certainty. Not brilliance.

Observation. Discipline. And the willingness to follow the evidence wherever it leads.

There is a lesson here for every trader. The market is not a debating society, an opinion poll, or a place where the most persuasive story necessarily wins. Every trading day, investors cast their votes with real money. Those votes appear in price, performance, and trend. The market continuously reveals where confidence is growing and where confidence is fading.

Yet there is another lesson, one that many traders overlook. You do not need to become an institution to benefit from institutional thinking. In fact, some of your greatest advantages come from remaining exactly what you are. You can move faster, adapt more quickly, focus on opportunities too small for large institutions to notice, and change your mind without convening a committee or answering to shareholders.

The successful trader borrows Wall Street’s discipline without inheriting Wall Street’s limitations. That means following performance instead of predictions. It means paying attention to relative strength instead of headlines. It means respecting risk before pursuing reward and understanding that capital leaves clues long before the financial media notices them.

Ironically, some of the biggest investing trends of the last twenty years were first recognized by individual investors long before institutional money arrived. Bitcoin, AI, social media, and electric vehicles all attracted retail interest well before they became institutional darlings. Institutions often provide the capital. Retail traders often provide the curiosity.

The purpose of this article was never to convince you that institutions possess secret knowledge. Quite the opposite. Their greatest advantage is not access to information. It is the discipline to follow evidence wherever it leads. The good news is that discipline is available to every trader willing to develop it.

The next market leader may already be revealing itself today. The trend may already be strengthening. Institutional money may already be accumulating shares. The clues are there for anyone willing to look. The challenge is not finding more information. The challenge is learning which information matters.

In the end, the market rewards those who pay attention to what is happening, not what they hope will happen.

And leaders tend to leave footprints.

Throughout this article, we’ve explored how institutional investors identify opportunity. Notice that they do not begin with predictions. They do not begin with opinions. They do not begin with headlines. They begin with evidence. They look for relative strength, leadership, capital flows, and performance. In short, they focus on where money is actually being made.

That sounds simple enough. The challenge, of course, is execution. There are thousands of stocks, ETFs, currencies, commodities, and global markets competing for your attention every day. No individual trader can manually track every opportunity, every intermarket relationship, every emerging trend, and every shift in institutional capital. This is precisely where technology can create a meaningful advantage.

VantagePoint AI was built to solve this problem. Instead of asking traders to guess where the next opportunity may emerge, VantagePoint uses patented artificial intelligence to analyze the relationships between markets and forecast the assets demonstrating leadership before those trends become obvious to the crowd. It helps traders answer the same questions institutions ask every day: Where is money flowing? Which assets are outperforming? Which trends are strengthening? And where is the probability of success improving?

The most successful traders understand that extraordinary results often come from consistently placing yourself on the right side of the right trend at the right time. That is why institutions focus on performance. That is why they monitor leadership. And that is why over 47,000 traders around the world use VantagePoint AI to help uncover opportunities that may otherwise remain hidden in plain sight.

There is one final point worth considering.

Institutional investors have entire teams dedicated to finding leadership. They have analysts, economists, research departments, and access to enormous resources. Yet despite all of that, they are still trying to answer the same basic question every trader faces every day: “Where is the next opportunity?” The difference is that institutions understand the cost of being late. By the time a trend becomes obvious, much of the move has already occurred. By the time the headlines appear, the smart money is often already positioned.

The goal is not simply to identify winners. The goal is to identify them while they are still emerging.

Imagine reviewing your watchlist next month with a completely different perspective. Instead of asking, “What should I buy?” you’ll know how to ask the questions institutions ask. Which assets are leading? Which trends are strengthening? Where is capital flowing? Which opportunities deserve immediate attention? That shift in perspective can permanently change the way you view financial markets.

During a free live online trading MasterClass, you’ll see exactly how traders use VantagePoint AI to identify emerging market leaders, measure relative strength, uncover hidden intermarket relationships, and separate genuine opportunities from market noise. More importantly, you’ll see real-world examples of how these tools can help traders focus their attention on assets demonstrating the same characteristics institutional investors seek every day.

If you’ve ever wondered how professional money managers identify leadership before it becomes obvious, how they separate strength from speculation, or how they determine where capital is flowing next, this MasterClass was designed for you.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.