Prices are rising faster than the numbers you’re being shown, because the system measuring them is designed to lie politely. In a real ‘free market,’ technology makes life cheaper. That’s not theory. That’s how progress works. But something is breaking that relationship, and it’s not technology.

It’s money.

You’re not crazy. You’re not bad with money. And you’re not imagining things.

Currency debasement is now outrunning innovation. Inflation is no longer an accident but a requirement. The result is hidden price increases, shrinking purchasing power, and a quiet erosion of privacy.

This isn’t an academic debate. It shows up every time you renew insurance, shop for groceries, or try to plan for your future. You don’t need an economics degree to understand it. You just need a mailbox, grocery cart, or monthly bill that arrives with a sly smile.

The prices that matter most are rising, and they’re rising faster than anything you’ll ever see reflected in the CPI. Housing costs don’t politely follow government formulas. Insurance premiums behave like they’ve discovered steroids. Healthcare pricing reads like a ransom note. Education costs more and delivers less. Food looks the same but somehow shrinks, spoils faster, and tastes like it gave up trying. Energy prices surge, retreat, and surge again, always managing to land higher than where they started.

What makes this especially aggravating is not just the financial hit. It’s the emotional one. People feel like they’re running faster just to stay in the same place. They do everything they were told to do. Work hard. Save responsibly. Plan ahead. And yet, the math never quite works out anymore. The spreadsheet says one thing. Real life says something else entirely.

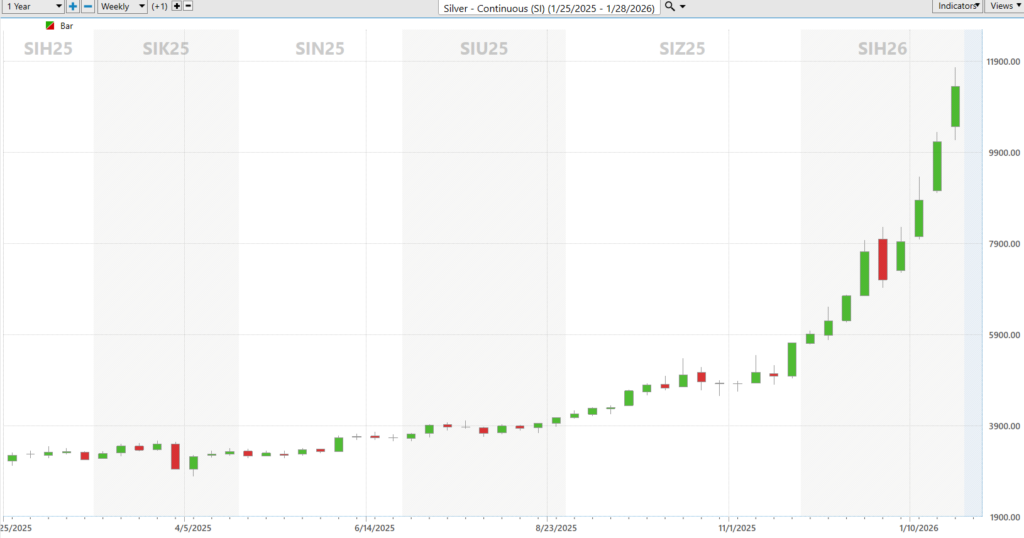

Here’s the part that never makes the press release. When gold is trading at $5,500 an ounce and silver has ripped to $121, that’s not a metals story. It’s a purchasing power story. And notice how convenient it becomes that anything which does not flatter the consumer price index simply does not count. CPI doesn’t measure asset prices, housing access, financing costs, credit card interest rates, insurance spikes, healthcare degradation, education debt, shrinkflation, subscription creep, taxes, regional pain, time lost, or the cost of protecting purchasing power itself. If it does not make inflation look tame, it gets averaged, substituted, smoothed, or ignored.

Gold and silver refuse to cooperate with that narrative. They don’t ask permission. They don’t require models. They simply re-price the truth. And when an asset exposes debasement instead of concealing it, the solution is never to listen. It is to pretend it does not exist.

Most people sense that something is wrong, but they cannot quite put their finger on it. They’re told inflation is under control, while their bank account quietly disagrees. They’re told the economy is strong, while their margin for error shrinks. The disconnect creates a low-grade, persistent irritation. Not panic. Not outrage. Just the nagging suspicion that the story being told does not match the story being lived.

The CPI tells a story. The problem is that it is not the story people are really living.

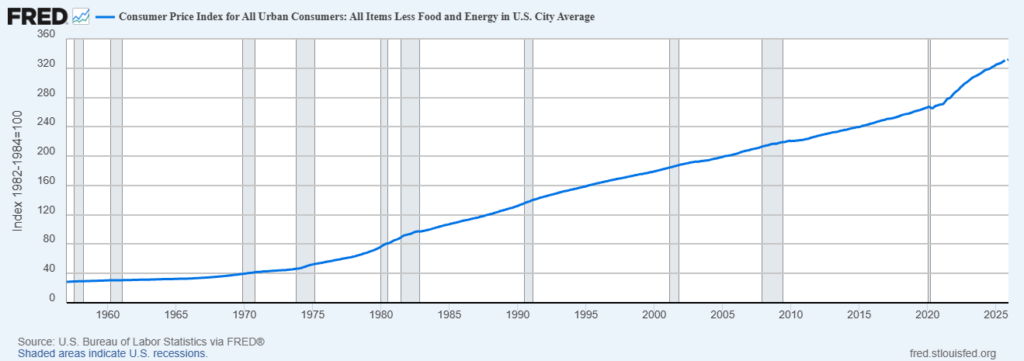

Imagine you had no idea this chart was CPI. No label. No explanation. You would look at it and say, without hesitation, “That’s the mother of all growth charts!” Smooth. Relentless. Up and to the right for decades. Barely a pullback. A trend any momentum trader would kill to own. And yet we are told, straight-faced, that inflation is “under control.” That this thing has somehow cooled off. That the pressure is easing. That is gaslighting, plain and simple. Because charts don’t lie. This one says prices rise every single year, without fail. It says purchasing power bleeds quietly, continuously, and permanently. And when leaders point at this line and tell you it is no longer a problem, they are not arguing with you. They’re arguing with facts.

CPI is selective by design, adjusted by formula, and political by necessity. It measures what can be smoothed, substituted, and explained away, not what hits household budgets the hardest.

Substitution is the quiet trick that makes the numbers behave. If steak gets expensive, the basket assumes you switch to chicken. If chicken rises, maybe pork. If quality drops, that is treated as irrelevant. The math says you adapted. Your lifestyle says you compromised. CPI calls that stability.

When assets inflate, CPI shrugs.

Quality degradation never makes the spreadsheet. Products get smaller. Ingredients get cheaper. Durability disappears. Subscriptions replace ownership. Fees replace price tags. The cost shows up everywhere except where inflation is officially measured.

Here is the simplest test. If the same product costs the same but is smaller, lower quality, or now requires a subscription, did the price really stay flat? Or did the system just change how the pain is counted?

In a functioning free market, prices should fall, not rise. Not because demand disappears, but because technology relentlessly drives marginal costs toward zero.

This is observable. Computing power becomes faster and cheaper with each iteration. Data storage expands while costs collapse. Communication, once expensive and constrained, is now instant and nearly free. Energy efficiency improves as systems become smarter, lighter, and more optimized. These are not anomalies. They are the natural outcomes of competition and innovation.

In a healthy market, productivity gains accrue to the consumer. Businesses compete by delivering more for less. Inefficiency is punished. Efficiency is rewarded. Over time, prices decline while quality improves. That pattern held for much of economic history whenever markets were allowed to function without distortion.

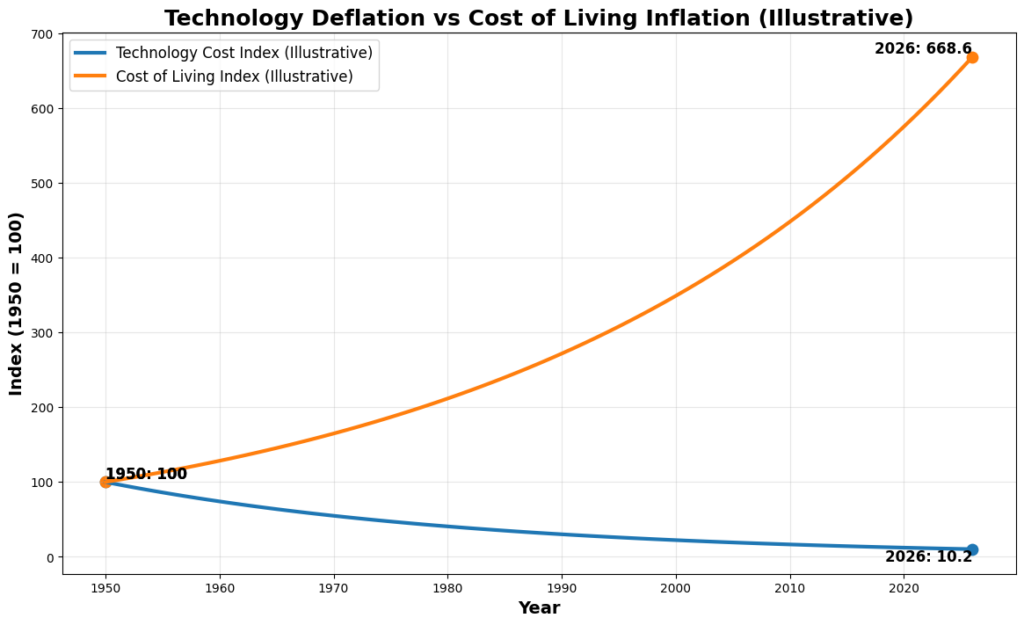

Let’s be clear before anyone reaches for a red pen. This following image is for illustrative purposes only. But here’s the punchline. If the government were being honest, they would publish a chart that looks an awful lot like this one below. One line showing the relentless collapse in the cost of anything touched by technology. Computing, storage, communication, efficiency. Down, down, down. The other line showing the cost of living doing what it has done for decades. Up. Every year. No mercy. No pause. That is the story nobody wants to put on a podium. Technology is doing exactly what it is supposed to do. It is making things cheaper, faster, and more abundant. Meanwhile, the cost of simply existing keeps climbing like it missed the memo. If those two realities were shown side by side in an official report, the question would become unavoidable. If technology keeps getting cheaper, why does life keep getting more expensive? And once you ask that question, the problem stops being innovation and starts being money.

The discomfort comes when this logic collides with modern reality. If technology is advancing at an exponential pace, why do prices feel heavier, not lighter? Why does abundance coexist with scarcity?

Technology is doing exactly what it should. Money is not. If money were sound, technology would make life steadily cheaper.

Here is where the narrative breaks down. Not because technology failed, but because money stopped doing its job.

Currency debasement is now accelerating faster than innovation. Productivity is rising, but the unit used to measure it is shrinking. That mismatch is the defining conflict of the modern economy. It explains why progress feels hollow and why growth no longer translates into relief.

The reason is structural. The system is built on debt, and debt does not tolerate falling prices. It requires inflation to remain serviceable. Without it, the math stops working. So, inflation is not an unintended side effect. It is the operating requirement.

That reality flips our debt-based capitalist system on its head. Instead of allowing prices to fall, policy intervenes to keep prices rising. Abundance becomes a problem to be managed rather than a benefit to be shared.

We are not experiencing inflation because things are scarce. We are experiencing inflation because money is too abundant. Or depending on which press release you read, we are experiencing very mild inflation, if at all.

Source: Truflation

When inflation shows up everywhere except the CPI, money does not sit still. It moves. Capital goes hunting for assets that reflect reality, not models. That’s why rotation accelerates. Money flows toward things that cannot be diluted, substituted, or explained away. Commodities, materials, energy, and hard-asset businesses start outperforming while the broad averages stall. This is not a mystery. It is money responding to pressure the official numbers refuse to acknowledge.

Think of money like a product on a shelf. Friedrich Hayek said it should compete just like anything else. If one version keeps shrinking, breaking, or losing value, people stop using it. They choose the one that holds up. Over time, money naturally moves toward whatever does the best job of staying strong. You do not need a PhD to understand it. Money goes where it is treated best.

That is exactly what 2026 looks like. The so-called “real stuff economy” is sprinting ahead. When the currency weakens, tangible inputs reprice first. Margins adjust. Cash flows respond. Meanwhile, indexes loaded with promises about the future lag behind. Rotation does not happen because traders get emotional. It happens because capital gets practical.

For traders, the edge is staying aligned with where that capital is headed. When people feel trapped, they start looking for exits. Not dramatic ones. Practical ones.

Money moves away from abstractions and toward reality, toward assets that cannot be printed, massaged, or statistically smoothed away. That shift rarely shows up in headlines first. It shows up in relative performance. Commodities, materials, energy, and other hard-asset–linked areas begin to lead while the broader market averages lag behind. This is price discovery responding to monetary pressure that the official statistics refuse to acknowledge.

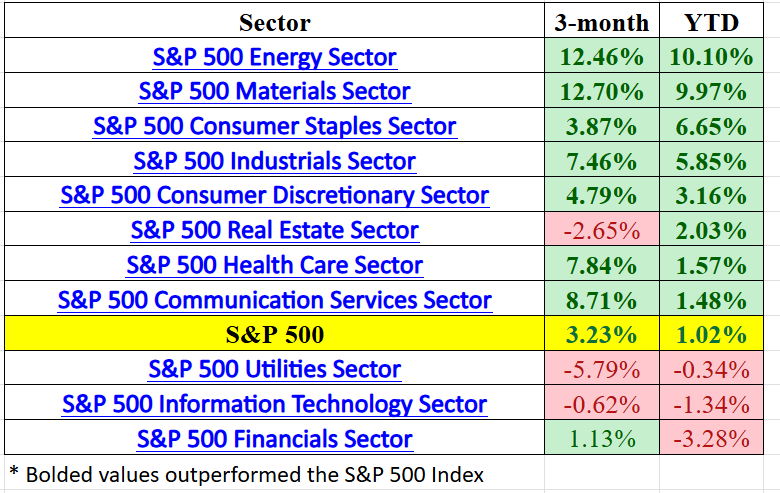

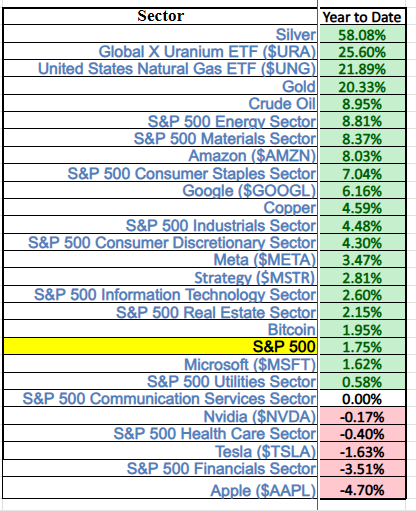

You can see that reality clearly in the sector performance data from multiple time frames this past week. Over the last three months and year to date, the S&P 500 Energy Sector and S&P 500 Materials Sector are decisively outperforming the S&P 500 Index itself. Industrials and Consumer Staples are also holding leadership, while Information Technology, Financials, and Utilities lag or slip into negative territory. That is not random rotation. That is capital repositioning itself toward real inputs, real costs, and real assets as purchasing power erodes.

Zooming out to the broader performance table reinforces the same message. Silver, uranium, natural gas, gold, and crude oil are leading year to date, well ahead of the broad index. Meanwhile, many of the largest and most celebrated technology names are underperforming or outright negative. This is the market speaking plainly. When inflation is understated and currency value is questioned, money flows to what measures the problem, not what benefits from ignoring it. The so-called “real stuff economy” is not just participating. It is leading. And the market, as always, is telling the truth long before the statistics catch up.

Before anyone starts pointing fingers, let us acknowledge a simple fact. Most people are busy trying to live their lives. They have jobs. Families. Deadlines. Dentists. Group texts that never stop. By the time dinner is over and the dishes are done, the last thing anyone wants to do is contemplate the structural integrity of the global monetary system.

Cognitive overload is the background noise of modern life. Alerts buzz. Feeds scroll. Tasks stack up. The brain does what it must to survive. It prioritizes the immediate and postpones the abstract. Rent due tomorrow beats currency debasement every time.

Short term survival crowds out long-term thinking, not because people are careless, but because they are human. Worrying about next month feels indulgent when this week is already expensive.

And conveniently, the system thrives on this distraction. A population too busy to think deeply is easier to manage, easier to steer, and far less likely to ask uncomfortable questions. This is not malice. It is efficient. And it is precisely why none of this feels urgent until it suddenly is.

For more than fifty years, the petrodollar did the heavy lifting quietly. Energy was priced in dollars, demand stayed strong, and deficits felt painless. It worked because there was no alternative.

That monopoly is breaking. Energy trade is spreading across currencies. Deals are getting settled without the dollar in the middle. It is not loud, and it does not need headlines to matter.

As dollar dominance weakens, discipline shows up. When money loses exclusivity, it loses forgiveness. Tradeoffs return. Constraints reappear. The system does not explode. It just starts telling the truth again.

This shift is structural, not dramatic. But it changes the rules quietly. And quiet changes tend to be the ones that matter most.

Before we go any further, let’s engage in a few simple thought experiments.

You do not need to believe anything I am saying. You only need to answer a few basic questions honestly and see whether the official story survives contact with reality. If the answers contradict what you have been told, the problem is not the questions. It is the system.

Technology is now woven into nearly every moment of daily life, yet its cost keeps collapsing. A device in your pocket today holds more computing power than entire governments once commanded, offers instant global communication, unlimited storage, navigation, and access to nearly all recorded knowledge. And the price for all of that continues to fall, often bundled, subsidized, or treated as disposable. If technology were the source of inflation, this would be impossible. The most powerful tools ever created would be rare, expensive, and inaccessible. Instead, they are ubiquitous and increasingly cheap.

The same pattern holds once you look beyond hardware. Music, movies, software, maps, communication, and data all approach zero marginal cost. Once created, they can be replicated endlessly for almost nothing. Scarcity has been eliminated wherever technology dominates. Consumers receive more value for less money, sometimes for free. Yet at the same time, the costs that define daily life keep rising. Housing, healthcare, insurance, education, and energy move relentlessly higher. That divergence matters because it tells you where inflation is not coming from.

Look at what technology has replaced. Cameras, calculators, encyclopedias, filing cabinets, phone books, music players, navigation systems, and entire entertainment centers have collapsed into a single device. What once cost tens of thousands of dollars, required physical space, and constant maintenance now costs a fraction of that and improves every year. If innovation were driving inflation, replacing all of that would cost more, not less. The fact that it costs dramatically less exposes the real source of rising prices.

The conclusion becomes difficult to avoid. Price increases are not coming from productivity, innovation, or efficiency. They are coming from money itself. When the unit of measurement weakens, the things that cannot be digitized, replicated, or automated reprice higher. Technology is doing what it has always done, driving costs down. The relentless rise in the cost of living is not a failure of progress. It is a signal that the currency measuring that progress is losing its value.

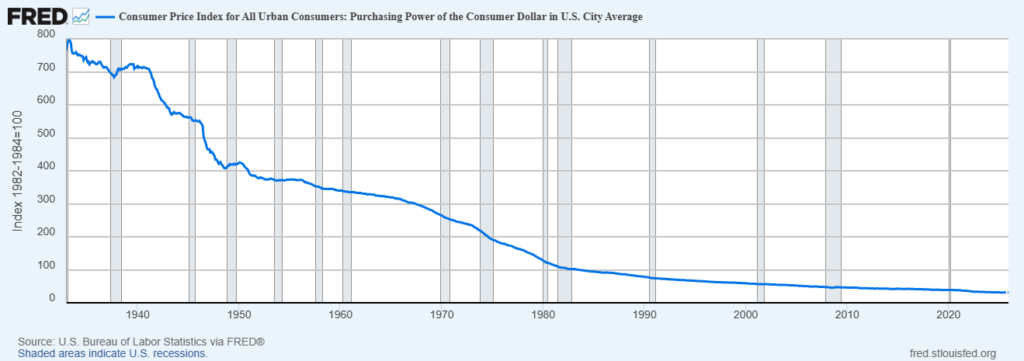

Here is the Federal Reserve’s Chart of the purchasing power of the U.S. Dollar since 1933. If you did not know what this chart was, you would swear it was the long-term price of a failed company. Down. Down again. Then down some more. No rallies. No recoveries. Just a steady grind lower that never seems to find a floor. But this is not a stock. This is the purchasing power of the U.S. dollar.

Isaac Newton had a law for this. A force in motion tends to stay in motion unless acted upon by an equal and opposite force. Inflation has been in motion for over a century, and there has been no equal and opposite force applied. No anchor. No restraint. No discipline. So the trend continues. Purchasing power keeps falling because nothing has been allowed to stop it. And when policymakers tell you this decline has somehow been defeated, remember this chart. Trends do not lie. They only end when something powerful enough finally stands in their way.

These questions are uncomfortable because it forces a binary answer.

Follow these questions honestly and a pattern emerges. Prices are not rising because we are failing. Life is not harder because progress stopped. The evidence points somewhere else entirely. Toward money that no longer measures value honestly.

None of this requires panic, and it does not demand radical conclusions. The goal is not to predict the future, but to prepare for a range of outcomes. In periods of structural change, resilience matters more than precision.

One practical step is to hold some assets outside the traditional financial system. Not as a rejection of it, but as diversification. Systems can fail, rules can shift, and access can be interrupted. Optionality has value.

Reducing reliance on debt matters for similar reasons. Debt narrows flexibility. It amplifies vulnerability during transitions. In an environment shaped by monetary adjustment, leverage cuts both ways.

Favoring scarce assets over promises is less about ideology and more about arithmetic. Scarcity cannot be revised by policy. Promises can. Over time, the distinction becomes consequential.

Finally, invest time in understanding money itself. It is one of the most influential forces in daily life and one of the least examined. Clarity does not eliminate uncertainty, but it improves decision-making.

You only need resilience.

This is not about panic. It is about clarity. When technology accelerates and productivity improves, life should feel lighter, not heavier. When that relationship breaks, the signal matters.

Innovation is doing what it has always done. It is expanding capacity, reducing costs, and increasing efficiency. The friction shows up elsewhere. It shows up in money that no longer holds value the way people expect it to. It shows up in systems that quietly trade resilience for control.

Once that becomes clear, the conversation shifts. The question is no longer whether progress will continue. It will. The question becomes simpler and more personal. What do you want your savings to depend on?

Alvin Toffler warned that the future would arrive faster and faster, and that speed is no longer theoretical. It is visible in markets that rotate before most traders can react, in narratives that shift overnight, and in price action that punishes hesitation. The old approach of waiting for confirmation, digesting yesterday’s news, and reacting slowly is no longer just inefficient. It is dangerous. In an environment where change accelerates, decision-making must accelerate with it.

That is precisely why VantagePoint’s patented artificial intelligence is no longer optional for traders who want to stay relevant.

The purpose of VantagePoint A.I. is not to predict headlines or guess outcomes. Its purpose is simpler and far more powerful. It keeps you on the right side of the right trend at the right time. By analyzing intermarket relationships, price behavior, and forecasting trend shifts, VantagePoint helps predict market trends 3 days ahead of everyone else and let’s traders get a jump start with what the market is actually going to do, not what they hope it will do.

The opening weeks of 2026 make this painfully clear. Massive rotational shifts are already underway. Gold trading above $5,500 per ounce and silver surging past $120 per ounce are not random events, the U.S. dollar is losing value. When the unit of measurement weakens, price action distorts, correlations change, and traditional analysis breaks down. Traders who rely on static indicators are left reacting. Traders who use adaptive intelligence stay aligned.

This is where VantagePoint A.I. delivers its real advantage. It processes more variables than any human can manage. It removes emotional bias. It adapts as conditions change. Instead of asking whether a market should move, it identifies when it is moving and whether that move is likely to persist. In fast, rotational markets, that distinction matters. VantagePoint A.I. doesn’t get tired, distracted, or anchored to outdated assumptions. It responds to reality as it unfolds.

The goal is not to trade more. It is to trade better. To avoid being early, late, or on the wrong side altogether. VantagePoint A.I. exists to give traders clarity in accelerating markets and confidence when others are frozen by uncertainty. If the future truly is arriving faster, then the edge belongs to those who can see it forming in real time.

I invite you to see how this plays out in real time, you can attend a free live online masterclass and watch VantagePoint A.I. at work. The session walks through how the software identifies emerging trends, filters out noise, and supports clearer decision-making without emotional interference. It is a practical look at how letting VantagePoint A.I. handle the heavy lifting can help traders operate with greater confidence, discipline, and consistency.

The invitation is simple.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.