Every market cycle eventually reaches the moment when the story stops working, and the math takes over. We may be approaching that moment now. For much of the past decade, the dominant storyline was straightforward. Growth might slow from time to time, inflation might flare up briefly, but policymakers had tools to stabilize the system. Central banks could cut rates. Governments could stimulate demand. Liquidity could smooth over almost any rough patch.

But the economic environment emerging today looks different, and the usual playbook is starting to feel less reliable. Inflation remains stubborn, even as signs of slower growth appear across large parts of the global economy. Consumers are facing higher costs for energy, food, and housing. At the same time, businesses are navigating supply constraints, geopolitical tensions, and rising financing costs. It is an unusual combination that economists have a name for but policymakers rarely like to say out loud.

Stagflation.

It’s the economic scenario that frustrates both investors and governments because it breaks the normal policy playbook. When economies weaken, central banks typically lower interest rates to stimulate activity. When inflation rises, they tighten financial conditions to cool demand. Stagflation forces both problems to appear simultaneously, leaving policymakers trapped between two conflicting responses. The result is a policy dilemma where every potential solution risks making the other side of the problem worse.

That tension is already visible in markets. Growth-sensitive assets have struggled to gain traction, while a different group of assets has begun quietly outperforming. Commodities are rising. Energy producers are strengthening. Materials companies are showing resilience. The market may not be saying stagflation yet, but it’s starting to trade as if it expects it.

Consider what markets are already telling us. While the S&P 500 Index has struggled to gain traction this year, energy stocks have surged, materials have outperformed, and commodity prices have pushed higher across metals and industrial inputs. The leadership inside the market is quietly shifting toward the sectors most tied to the physical economy.

Last Friday, Scott Bessent, the U.S. Treasury Secretary, went on Fox Business and delivered an interview that sounded less like a routine policy update and more like a man attempting to juggle chainsaws while assuring the audience that juggling chainsaws is a perfectly normal and safe activity. Iran may be trying to create economic chaos. The United States might “unsanction” hundreds of millions of barrels of Russian oil to stabilize energy markets. Tariffs could return to their previous levels in five months.

That is a lot to cram into a five-minute television segment, and it has the distinct aroma of someone explaining that the airplane is experiencing “minor turbulence” while passengers can see a wing falling off outside the window.

But the interesting part of the interview was not what Bessent said. It was the broader context surrounding it. Because Bessent currently holds what may be the hardest job in Washington. His task is to calmly explain to the world that everything is under control while the numbers behind him increasingly resemble a calculus problem solved by someone who skipped math class.

Traders recognize this situation instantly. In poker they call it a “tell.” When someone is bluffing, or under pressure, they reveal something unintentionally. A nervous twitch. A strange pause. Talking a little too confidently. The cards may remain hidden, but everyone at the table knows something is going on.

Right now, Washington has a few tells showing.

Bessent is dealing with an oil shock tied to conflict near the Strait of Hormuz, the legal collapse of a tariff framework that was supposed to help reduce government debt, a federal court order requiring up to $175 billion in refunds to importers, and lawsuits from more than twenty states attempting to dismantle the replacement tariff authority, while the U.S. Dollar slowly deteriorates its purchasing power. Meanwhile oil has surged above $100 a barrel for the first time since the Russian invasion of Ukraine, reigniting inflation fears just as equity markets suffer one of their roughest weeks of the year. All of this is occuring months before the mid-term elections.

And then there is the fiscal math, which grows more alarming by the day. The Congressional Budget Office now estimates that U.S. primary deficits will be roughly $1.6 trillion larger over the next decade than previously projected. Add roughly $400 billion in additional interest costs and more than $1 trillion per year already being spent servicing the national debt, and the United States is rapidly approaching $40 trillion in total obligations.

Study the Federal Debt chart below, and it certainly looks like we are in a completely vertical breakout.

This is why Gold has been climbing like a homesick angel. Since 2008, every major expansion of the Federal Reserve balance sheet has coincided with a strong rally in gold prices. When central banks manufacture money and governments manufacture debt, investors tend to manufacture an interest in precious metals.

But here is the part many commentators are missing.

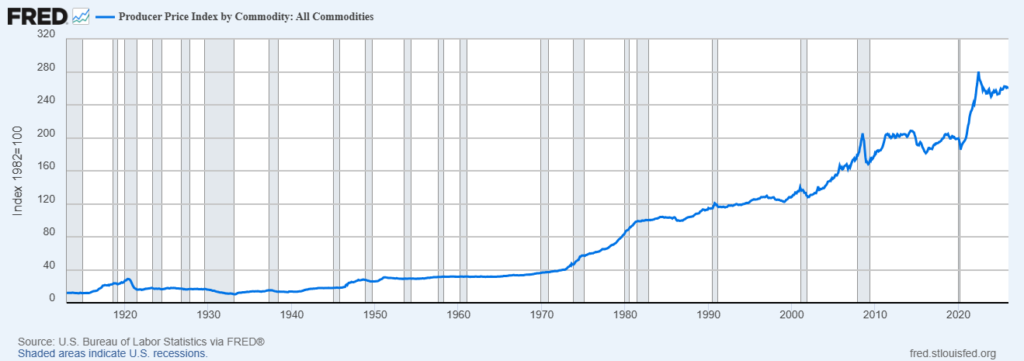

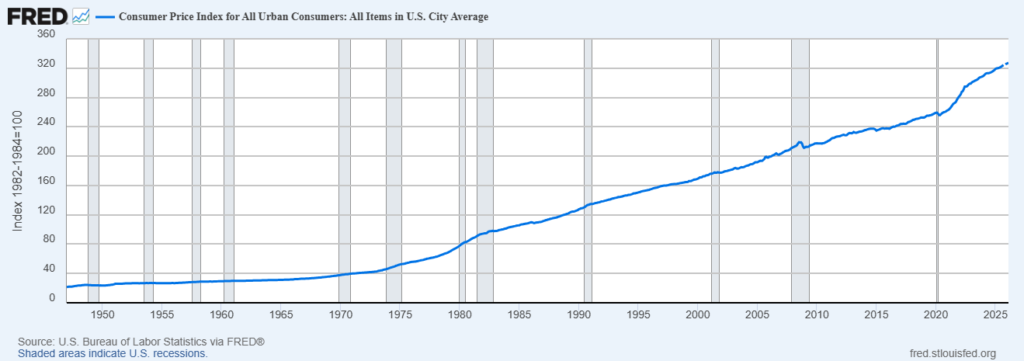

Gold is not the only asset sending this message. Across the commodity complex, the same pattern appears. Energy companies are outperforming. Industrial firms are gaining ground. Materials producers are quietly leaving the S&P 500 Index in the dust. Even consumer staples are holding up better than the high-growth darlings that dominated the previous decade. As a trader when I study the Producer Price Index chart below, it looks to me like we are approaching all-time highs and getting ready to break out. Again.

In other words, capital is migrating back toward things that physically exist. The items people dig out of the ground, refine, transport, manufacture, and eventually sell.

Not theories. Not algorithms. Not venture-capital pitch decks.

Real stuff.

If you live inside the political bubble of Washington, D.C., the economy is always booming. Why would it not be? The place runs on a printing press that never runs out of ink. When money runs low, they print more. When spending gets out of control, they print even more. From inside that marble palace, the economy looks like a permanent fireworks show.

But step outside the Beltway and the view changes fast.

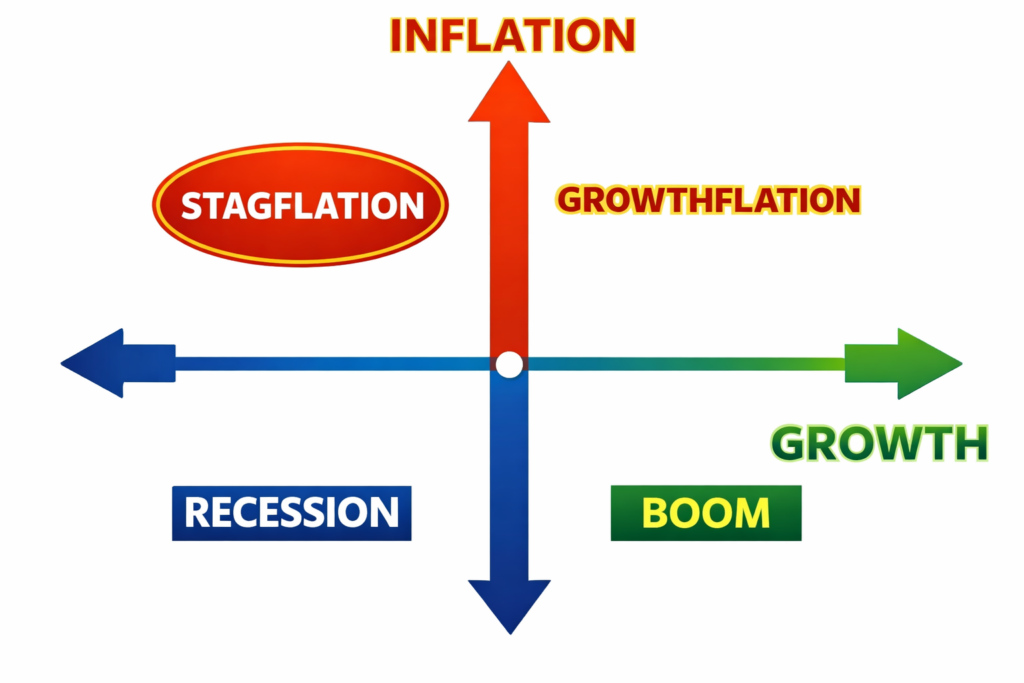

Out here in the real economy, people cannot print their way out of trouble. Businesses live and die by profit. Families live and die by paychecks. Which means it helps to understand the four basic economic neighborhoods we cycle through. Boom. Growthflation. Recession. Stagflation.

These are not academic words economists toss around to justify their salaries.

A Boom is the good times rolling. Businesses are hiring. Paychecks are growing. Confidence is high and money moves fast. Companies expand, investors pile into markets, and optimism spreads like wildfire.

In a boom, people stop worrying about survival and start thinking about opportunities. New businesses launch. Innovation explodes. Risk feels justified because the tide is lifting almost every boat in the harbor.

Booms feel permanent while they are happening. They never are.

Growthflation is what happens when the economy is still expanding but the cost of living starts climbing right alongside it.

Jobs exist. Profits are rising. The headlines say growth is healthy. But quietly, prices begin creeping upward across the board. Groceries cost more. Energy costs more. Housing costs more.

So yes, the economy is growing. But the dollars in your wallet are shrinking in purchasing power. It is prosperity with friction.

You are moving forward, but the treadmill keeps speeding up.

A Recession is when the economic engine sputters.

Businesses pull back. Hiring freezes appear. Consumers stop spending because uncertainty creeps in. Projects get canceled. Expansion plans vanish overnight.

Suddenly optimism disappears and survival becomes the priority. Companies protect cash. Investors become cautious. Everyone begins asking the same question.

How long is this going to last?

Recessions are the economy hitting the brakes after driving too fast for too long.

Stagflation is the nightmare scenario.

The economy slows down or stalls completely. Growth disappears. Jobs become harder to find.

But prices keep rising anyway.

So, the economy is not moving forward. Yet everything costs more. Food. Energy. Housing. Insurance. All of it.

It is the worst of both worlds. Weak growth and rising inflation at the same time.

And unlike a normal recession, the usual policy tools do not work very well. Stimulate the economy and inflation gets worse. Fight inflation and growth collapses.

Which is why stagflation has historically been the most painful quadrant on the entire economic map.

Once traders understand the four economic quadrants, the political fog machine stops working quite so well. You start hearing policy speeches differently. The buzzwords, the reassuring phrases, the confident forecasts suddenly sound like what they are. Carefully polished doublespeak designed to make bad news sound like a minor scheduling inconvenience.

Here is the trick politicians hope you never learn. The economy can only live in one of four neighborhoods. Boom. Growthflation. Recession. Stagflation.

That is it. There is no fifth option called “temporary transitional macro softness.”

A trader only needs to do a little kindergarten math to understand what is really going on. If it is not a boom and it is not growthflation, then the remaining choices are recession or stagflation. And for political careers, those two words are the economic equivalent of garlic to a vampire.

Stagflation is what happens when the economy stops growing but prices keep rising, which quietly eats away at the value of money and makes it much harder for businesses and investors to create real wealth.

When inflation rises and growth slows at the same time, the investment landscape begins to change quickly. The assets that dominated the previous cycle often start losing momentum. Companies that rely heavily on cheap capital or distant growth projections become more sensitive to higher borrowing costs. Investors begin reassessing the assumptions that supported the last decade of market leadership.

That reassessment usually leads to a simple question.

What assets benefit from this kind of environment?

In stagflation, money tends to flow toward scarce, tangible assets like gold, energy, and essential commodities because when growth slows and currencies lose purchasing power, investors look for things the government cannot print and the world still needs every single day.

Precious metals often play a central role in this shift. Gold has long been viewed as a store of value during periods of monetary uncertainty. When investors begin questioning the stability of currencies or the sustainability of government debt, gold frequently attracts capital. Unlike financial assets, it cannot be printed, diluted, or expanded by a central bank policy decision.

Energy markets tell a similar story. Oil and natural gas remain foundational inputs for transportation, manufacturing, and power generation. When geopolitical tensions disrupt supply chains or global demand remains resilient, energy prices can move sharply higher. Those dynamics tend to reward producers and the broader ecosystem of companies connected to energy production.

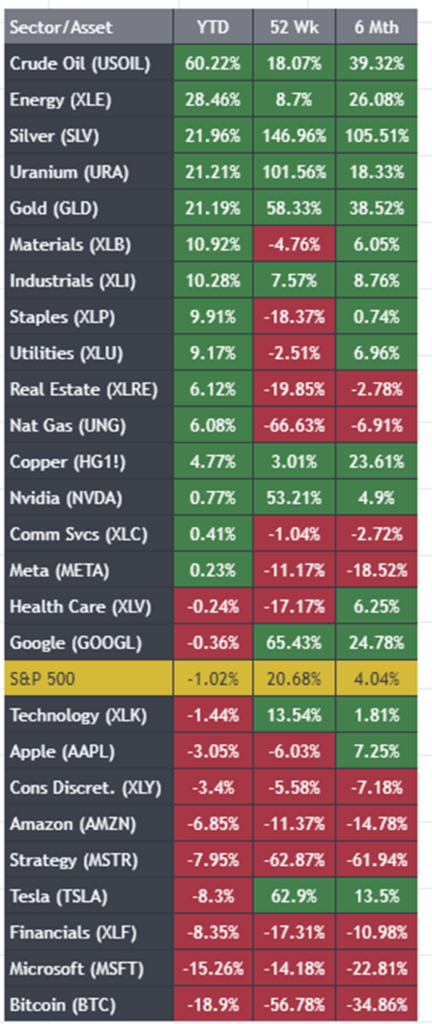

The scoreboard is not subtle about what is happening. The things that come out of the ground or keep the lights on are sprinting ahead, while the digital darlings that dominated the last decade are wheezing somewhere behind the pack. Oil, energy, gold, silver, uranium, and other assorted pieces of the physical world are running laps around the S&P 500 Index, which is trudging along like a tourist who took a wrong turn in a marathon. When the assets tied to fuel, metals, and industrial inputs start leading the market while growth stocks stall, the market is quietly whispering a word economists hate to say out loud. Stagflation.

Meanwhile the former royalty of Wall Street, the so-called Mag 7, appear to have misplaced their crowns somewhere below the equator of the S&P 500 Index. Most of them are negative for the year, which is not exactly what you expect from companies that were previously treated like the economic equivalent of Greek gods. When silicon chips, cloud software, and electric dreams start lagging while oil wells, copper mines, and precious metals take the lead, the market is telling you something very simple. In uncertain times, investors start favoring the things the government cannot print and the world cannot live without.

History provides a useful reference point. During the inflationary period of the 1970s, commodities and resource companies dramatically outperformed many traditional equities. Energy producers became market leaders, metals and mining stocks surged, and investors increasingly sought exposure to industries tied to real resources.

Put these forces together and a pattern begins to emerge. When inflation persists and growth slows, capital gradually rotates away from financial abstractions and back toward the tangible assets.

Toward oil wells. Copper mines. Farmland. Factories.

Toward the real stuff that keeps the global economy running.

Behind every big market move there is usually a bigger story hiding in plain sight. In this case the story is debt. Not the kind of debt that shows up in headlines for a day and disappears. The kind that quietly compounds year after year until the numbers begin to overwhelm the narrative.

The United States is now carrying nearly $39 trillion in national debt, and the cost of servicing that debt is climbing rapidly. According to the Congressional Budget Office, interest payments alone are already exceeding $1 trillion per year. That means a significant portion of government spending is no longer going toward infrastructure, defense, or social programs. It is simply paying interest on money already borrowed.

This creates a difficult balancing act for the Federal Reserve. If inflation rises, the traditional response would be higher interest rates. But higher rates also increase the cost of servicing the national debt and can place additional strain on financial markets. Lower rates, on the other hand, may help stabilize the economy but risk allowing inflation to run hotter for longer.

That tension is exactly why investors are paying closer attention to real assets. When fiscal deficits expand and monetary policy becomes constrained, confidence in financial assets can begin to weaken. Capital naturally starts searching for places where purchasing power may be better preserved.

Over time, that process tends to benefit commodities, energy producers, and other sectors tied to the physical economy. These assets are directly linked to real demand and supply constraints rather than policy decisions or financial engineering.

When debt grows faster than the economy that must support it, markets begin to adjust. And increasingly, they are adjusting toward the parts of the economy that produce tangible goods and essential resources.

In other words, toward the real economy.

You know you are in stagflation when the economy stalls, prices keep climbing like they are on an escalator, your paycheck buys less every month, and the experts on television start using fancy words to avoid saying the two words nobody in power wants to admit.

The two words are “stagflation” and “recession.”

Those are the terms policymakers and politicians try hardest to avoid because once either word enters the public conversation, it signals that the economic story they have been selling is breaking down.

In plain English, it means the economy is not healthy and people are feeling it in their wallets.

One of the quiet realities of markets is that large institutional capital rarely waits for economists to declare a new regime. By the time the official narrative arrives, the money has already moved. Pension funds, sovereign wealth funds, commodity traders, and macro hedge funds tend to react to incentives rather than headlines. When inflation pressures rise and growth becomes uncertain, they start reallocating capital toward assets that behave differently from the traditional equity portfolio.

You can see this rotation beginning to appear across markets. Energy producers, materials companies, and industrial firms have begun outperforming the S&P 500 Index. Commodity prices have strengthened. Supply constrained industries are attracting renewed interest. These shifts are not accidental. They reflect a strategic adjustment by investors who recognize that the macro environment is changing.

Institutional investors think in terms of regimes. When growth is strong and inflation is stable, technology and growth stocks tend to dominate because future earnings are discounted at lower rates. But when inflation rises and economic momentum slows, those same long duration assets become more sensitive to interest rates and capital costs. In that environment, assets tied to real production begin to look more attractive.

Something similar appears to be happening again. Capital is gradually moving toward companies that extract resources, manufacture inputs, and provide essential infrastructure for the global economy. These businesses are tied directly to supply and demand dynamics rather than financial leverage or distant earnings projections.

The important point is that these rotations tend to develop slowly at first. They can look like short term anomalies or temporary sector moves. But over time they often reveal a deeper shift in market leadership.

By the time most investors recognize the pattern, the institutions have already been positioning for it for months.

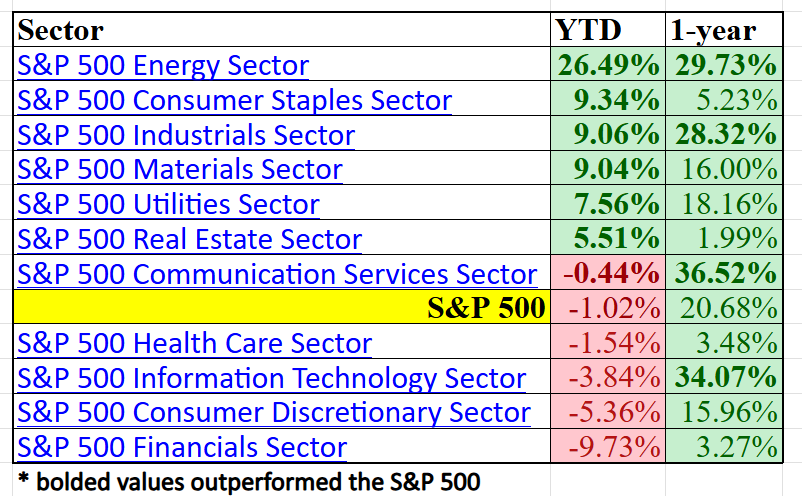

Study the sector performance scoreboard below to better understand who is winning. Simply observe where the trends are consistent and where they are broken. That will provide a pretty important clue as to the macro environment we are operating in.

Every market cycle produces a familiar character. The investor who prepares for the next market using the strategy that worked perfectly in the last one. Economists sometimes call this recency bias. Traders usually call it something simpler: fighting the last war.

For most of the past decade the winning formula was clear. Interest rates were low, liquidity was abundant, and investors were willing to pay increasingly higher prices for companies promising rapid growth in the future. Technology and high growth stocks became the dominant leaders of the market. As long as capital remained cheap and economic growth stayed relatively stable, that strategy worked exceptionally well.

But stagflation changes the rules.

When inflation rises and growth slows, the math behind long duration growth investments begins to look different. Borrowing costs increase. Profit margins face pressure from rising input costs. Investors become less willing to pay premium valuations for earnings that may arrive many years in the future.

This is where many traders and investors make their biggest mistake.

They continue chasing yesterday’s winners.

They remain heavily concentrated in the sectors that dominated the previous cycle, convinced that the old leadership will soon return. Meanwhile, the market leadership has already begun rotating somewhere else. Energy companies start outperforming. Materials producers gain momentum. Industrial firms that manufacture the physical inputs of the global economy begin quietly climbing higher while investors are still debating the latest software upgrade.

Markets rarely ring a bell when leadership changes. Instead, the shift happens gradually. A few sectors begin outperforming across several time frames. Capital flows slowly migrate toward companies tied to real production and essential resources.

By the time the broader investing public recognizes the shift, institutional investors have often been positioning for months.

The lesson appears in nearly every market cycle.

The next winners rarely look like the last ones.

For traders, the most important question in any macro shift is not whether the narrative sounds convincing. The real question is what the market is doing with capital. Markets tend to move first and explain themselves later. By the time a theme becomes widely accepted, the largest institutional flows have often already repositioned.

If you have never traded a stagflationary market before, the first rule: forget the old playbook. The strategies that worked during easy money and smooth economic growth can get your head handed to you when growth stalls and prices keep climbing.

In stagflation, the market becomes brutally selective. Weak companies get punished. Overhyped sectors lose their shine. Meanwhile the boring, real-world stuff suddenly starts acting like a superstar. Energy. Commodities. Hard assets. Businesses tied to necessities instead of luxuries. Money does not disappear. It simply relocates.

So, trade what is working, not what you wish would work. Follow strength. Cut losses fast. And remember that markets do not care about opinions, narratives, or economic speeches. They only care about where capital is flowing.

Many traders watch three simple signals when evaluating a potential stagflation shift:

• Sector relative strength vs the S&P 500 Index

• Commodity trend confirmation across energy, metals, and agriculture

• Institutional capital rotation into energy, materials, and industrial companies

None of these indicators work in isolation, but together they can reveal where capital is beginning to concentrate.

When inflation rises, growth slows, and debt explodes, markets start rewarding the things that cannot be printed.

Stagflation tends to reward a very different group of assets than the ones that led the previous cycle. Real assets such as commodities, energy producers, materials companies, and industrial firms become increasingly important because their businesses are directly tied to the physical economy. They produce resources, goods, and infrastructure that remain in demand regardless of shifts in financial sentiment.

At the same time, assets that depend heavily on cheap capital or long-dated growth expectations often face greater pressure. Rising input costs, higher interest rates, and slower economic growth can challenge business models built on future expansion rather than present profitability. This dynamic can gradually reshape market leadership.

For traders and investors alike, the lesson is straightforward. Market regimes change, sometimes slowly and sometimes all at once. Those who adapt early often find opportunities where others are still focused on the previous cycle’s winners.

In an environment defined by slower growth and persistent inflation, capital has a tendency to migrate toward the parts of the economy that produce tangible value. The companies and sectors tied to real resources, real production, and real demand.

When government debt expands rapidly and interest costs begin consuming larger portions of public budgets, policymakers face difficult tradeoffs. Tight monetary policy may help contain inflation, but it can also slow growth and increase borrowing costs across the system. Looser policy may support markets in the short term but risks further weakening the purchasing power of currencies.

These tensions can shape asset performance in subtle but meaningful ways. Periods characterized by rising inflation and slower growth often see investors rediscover the value of tangible assets. Commodities, energy producers, materials companies, and other businesses tied to the physical economy tend to benefit from price increases that ripple through supply chains. At the same time, assets that rely heavily on long term growth assumptions may struggle to maintain their valuations.

None of this suggests that one cycle replaces another permanently. Market leadership evolves over time as economic conditions shift. But when inflation persists, fiscal pressures grow, and geopolitical risks rise, investors often begin to rethink where stability and value can be found.

In those moments, the market’s focus tends to move away from financial abstractions and back toward assets grounded in real economic activity. It is a reminder that while policy debates and economic forecasts may change from year to year, the underlying drivers of value in the global economy often remain surprisingly consistent.

The lesson is simple. Opinions do not matter. Narratives do not matter. Price action does. When capital begins moving toward certain sectors and away from others, that movement is the market revealing where opportunity and risk truly reside. Traders who watch the scoreboard carefully can see these shifts developing long before they appear in headlines.

We are living through unusually abnormal times. The economic environment is shifting in ways that many investors have never experienced in their careers. Inflation, debt expansion, geopolitical stress, and changing market leadership are all colliding at once. In environments like this, behaving normally is dangerous. Acting as if the world still operates under the same conditions that existed ten years ago is a recipe for either extinction or obsolescence in the financial markets.

Protecting your wealth in this environment is not a theoretical exercise. It is not something that can be solved with hopeful thinking or yesterday’s strategies. The traders who survive and prosper are the ones who adapt, who study the data, and who follow the evidence wherever it leads. They recognize that the market does not reward stubbornness. It rewards preparation, discipline, and the ability to act on high-probability information.

This is precisely why VantagePoint artificial intelligence trading software has become such a powerful tool for traders. AI was not designed to replace judgment. It was designed to strengthen it. By analyzing massive amounts of market data and identifying probabilistic patterns that humans might miss, AI allows traders to make decisions based on evidence rather than emotion. In uncertain environments, that edge becomes incredibly valuable.

If you would like to see how traders are using VantagePoint’s patented artificial intelligence to forecast market trends, identify strength early, and make better trading decisions, I invite you to attend a free live online masterclass titled “Learn to Trade with VantagePoint” In this one-hour session you will see exactly how our AI tools are helping traders cut through the noise, understand the probabilities, and navigate markets that are becoming increasingly complex.

The truth is that markets are always evolving. The strategies that worked in the last cycle rarely work the same way in the next. The traders who succeed are the ones willing to learn, adapt, and use the best tools available to them. VantagePoint Artificial intelligence is rapidly becoming one of those tools, helping traders transform uncertainty into informed action.

In abnormal times, the advantage goes to those who see clearly and act decisively. AI can help provide that clarity. And in markets where the unprepared are punished, clarity may be the most valuable asset of all

Register for the masterclass here.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.