This week’s AI stock spotlight is BlackBerry ($BB)

BlackBerry is one of those rare corporate creatures that managed to go from king of the hill to cautionary tale to possible comeback story without ever fully leaving the building. Founded in 1984, it built the first smartphone empire before smartphones ate it alive. It pivoted from phones to software, from hardware to cybersecurity, from typing emails on tiny keyboards to helping machines talk to other machines without accidentally crashing into walls. Today the company sells secure communications software and embedded operating systems used in everything from cars to industrial systems. The reason traders still care is simple: dead companies do not suddenly become profitable again, build billion dollar software backlogs, and start showing up in momentum screens.

Wall Street has spent years treating BlackBerry like that old rock band everybody assumes broke up decades ago. Meanwhile management quietly rebuilt the business around cybersecurity, embedded operating systems, government communications, and automotive software. The result is a stock that now trades less like a nostalgia trade and more like a turnaround story with actual cash flow attached to it.

BlackBerry’s business model is surprisingly simple once you remove the emotional trauma from everyone who owned one in 2008. The company now operates primarily through Secure Communications and QNX. Secure Communications sells cybersecurity, endpoint protection, and government-grade communications software. QNX provides embedded software used in automobiles, industrial systems, robotics, and safety-critical devices. Those recurring software revenues matter because software businesses scale better than hardware businesses and generally involve fewer warehouses full of unsold gadgets.

The moat here is not flashy. It is boring. But boring is good. QNX powers systems inside more than 275 million vehicles worldwide and has deep integration into safety-critical applications where customers hate switching vendors because mistakes tend to involve lawsuits, recalls, or exploding machinery. Industry trends also favor BlackBerry. Cybersecurity spending keeps rising. Connected vehicles keep expanding. Robotics and machine automation require secure embedded systems. Financially, the company has moved from bleeding cash toward profitability, improved margins, and positive operating cash flow. The bear case is slow growth. The bull case is software operating leverage. Base case: gradual re-rating as investors realize this is no longer a smartphone company.

BlackBerry today makes money from two buckets. The first is Secure Communications, where governments, enterprises, and regulated industries buy secure software because ransomware attacks are bad for business and embarrassing in congressional hearings. The second bucket is QNX, which sits quietly inside cars, medical devices, industrial equipment, and increasingly robotics systems. Revenue is driven primarily by software licensing, subscriptions, royalties, and support contracts.

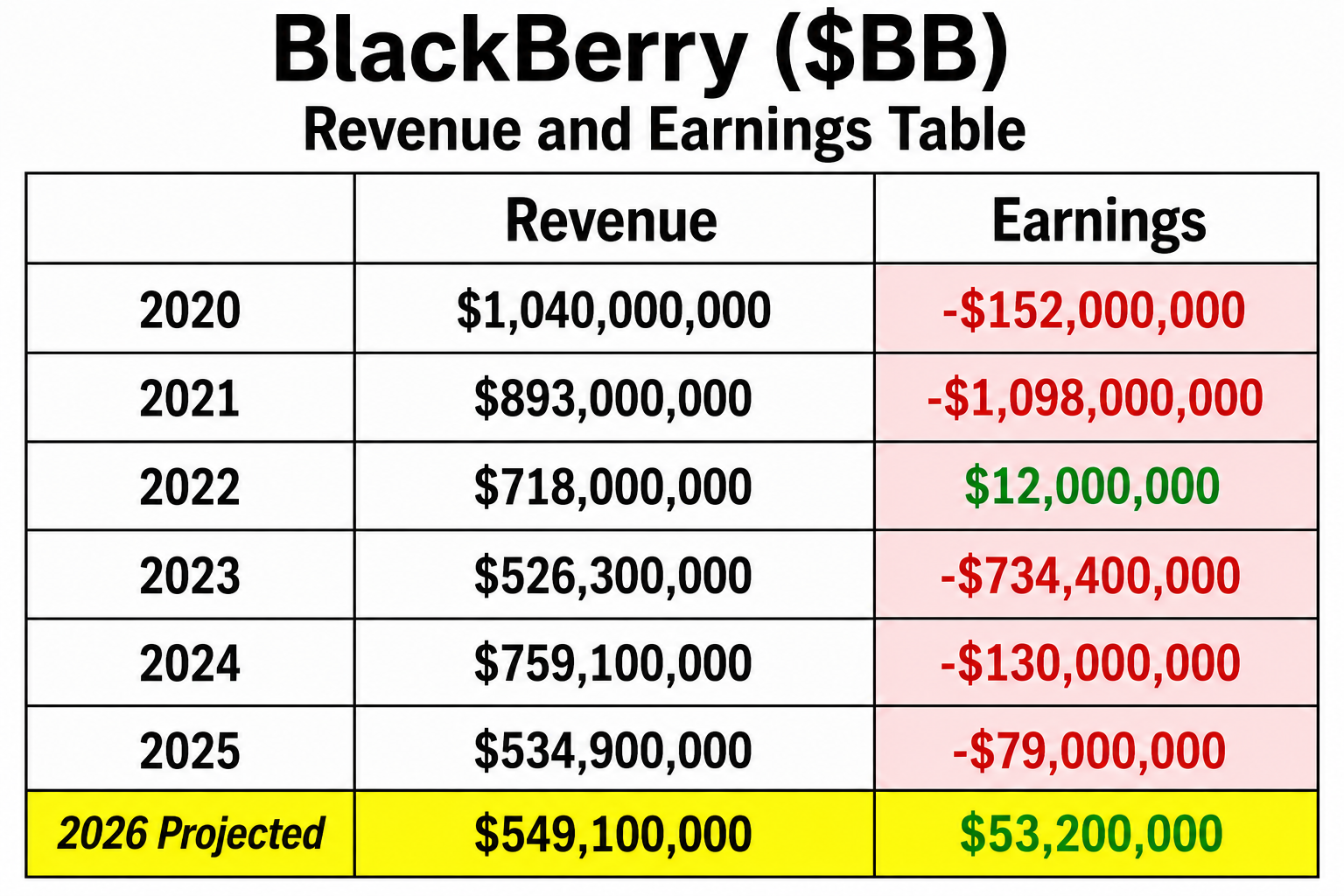

For traders looking at BlackBerry’s financial history, the uncomfortable truth is hard to ignore: in five of the last seven years, the company lost money, accumulating roughly -$1.28 billion in losses. That would normally trigger alarm bells loud enough to wake up even the most patient value investor. But markets rarely reward history alone. The more important question is whether losses are accelerating or shrinking. In BlackBerry’s case, the company appears to be moving from survival mode toward profitability, shifting from a collapsing hardware story into a software and embedded systems story. Should traders be concerned? Yes, but perhaps not for the reason many think. The bigger risk is not the historical losses themselves. It is whether management can finally prove that improved margins, QNX growth, and positive earnings are durable rather than another temporary stop on a very long turnaround tour.

Headquartered in Waterloo, Ontario, under CEO John Giamatteo, BlackBerry employs several thousand workers globally and competes against cybersecurity firms, embedded software vendors, and specialized operating system providers. Competitors include companies involved in automotive software, cybersecurity platforms, and enterprise communications. The competitive position is stronger than many assume because replacing deeply embedded software inside mission-critical systems is about as fun as replacing plumbing inside a skyscraper.

The financial condition over the past five years looks like a patient leaving intensive care and learning to jog again. Revenue has generally trended lower from historical levels as legacy businesses disappeared, but profitability trends have improved sharply. Fiscal 2026 revenue was about $549 million with positive net income around $53 million, a meaningful reversal from losses seen in prior years. The improvement came largely from cost control, higher-margin software revenue, and stronger execution.

What traders misunderstand most about BlackBerry finances is this: they still analyze it like a failing handset manufacturer. That company died years ago. Today’s company is software-heavy, less capital intensive, and increasingly dependent on recurring revenue streams. Revenue growth remains modest, but margin expansion and operating leverage matter more at this stage.

Cash position matters because software turnarounds usually die from running out of oxygen before they reach profitability. BlackBerry appears to have moved beyond that risk. Traders waiting for explosive revenue acceleration may miss the point. The market is currently rewarding improved quality of earnings more than pure growth.

The first question traders are asking right now is whether the turnaround is actually complete. Management says yes. Investors remain suspicious because this company has burned people before. Recent earnings strength and improving profitability suggest the answer is increasingly yes.

The second question is whether QNX growth is sustainable. This matters because QNX has become the crown jewel. With nearly $950 million in backlog and expansion beyond automotive into robotics and medical applications, investors see a longer runway.

The third question is whether cybersecurity becomes a growth engine again or remains merely stable. Demand has improved, but cybersecurity remains competitive and pricing pressure exists. Traders want acceleration, not merely stability.

Recent news tells a simple story: profitability arrived, backlog expanded, and management started speaking like people who believe the turnaround worked. QNX revenue growth accelerated. Management forecast stronger revenue ahead. Software demand remained resilient. These are real developments, not financial engineering tricks.

What is already priced in is the turnaround narrative itself. The market knows profitability improved. What may not be fully priced in is the possibility that QNX expands outside automotive faster than expected. Wall Street also tends to underestimate sticky software businesses embedded inside regulated systems.

Why is the stock up? Because traders finally discovered that companies moving from losses to profits tend to attract capital. Over the past 90 days, improving earnings, stronger guidance, and software momentum pushed sentiment higher. The market rewarded execution. Revolutionary concept, I know.

The semiconductor trend also matters indirectly. While BlackBerry is not a semiconductor company, the powerful rally in leveraged semiconductor products like SOXL reflects broader enthusiasm around AI infrastructure, autonomous systems, connected devices, and machine intelligence. Those trends create demand for embedded operating systems and secure machine-to-machine communications. BlackBerry rides behind that wave rather than creating it.

Analysts have historically failed by expecting either instant recovery or total collapse. The reality was uglier and slower. Now they risk underestimating operating leverage. At the same time, bulls should remember that software turnarounds often look strongest right before growth slows.

What could go right? QNX expands beyond automotive faster than expected. Cybersecurity stabilizes and returns to growth. Margins continue expanding.

What could go wrong? Automotive demand weakens. Cybersecurity pricing compresses. Growth stalls and investors remember why they stopped believing.

The biggest upside surprise would be QNX becoming a broader industrial and robotics platform.

The biggest blind spot is execution risk. Turnarounds rarely travel in straight lines.

Listen, BlackBerry is not for dividend investors, widows, or people seeking emotional closure from their old smartphones. This stock is best suited for momentum traders, turnaround traders, and investors who understand software operating leverage.

For the trend to continue, profitability must keep improving, QNX growth must remain strong, and backlog conversion must stay healthy. Early warning signs would include slowing QNX revenue growth, shrinking cash flow, or guidance cuts.

In markets, resurrection stories are dangerous because many corpses stay dead. BlackBerry’s unusual feature is that this one appears to have regained a pulse.

In this analysis we will review and evaluate forecasts using the following set of indicators and tools.

Wall Street Analysts Ratings and Forecasts

52 Week High and Low Boundaries

Best-Case / Worst-Case Scenario Analysis

VantagePoint AI Predictive Blue Line

Neural Network Forecast (Machine Learning)

VantagePoint AI Daily Range Forecast

Intermarket Analysis

Our Suggestion

We use artificial intelligence to improve probabilities, not replace judgment. Because here’s what many traders miss: a powerful signal means very little if the underlying business is weak. That’s why we study the fundamentals too. Revenue growth. Earnings. Cash flow. Competitive position. The real economics behind the ticker symbol. When fundamentals and price action move in harmony, the probabilities often shift dramatically in the trader’s favor.

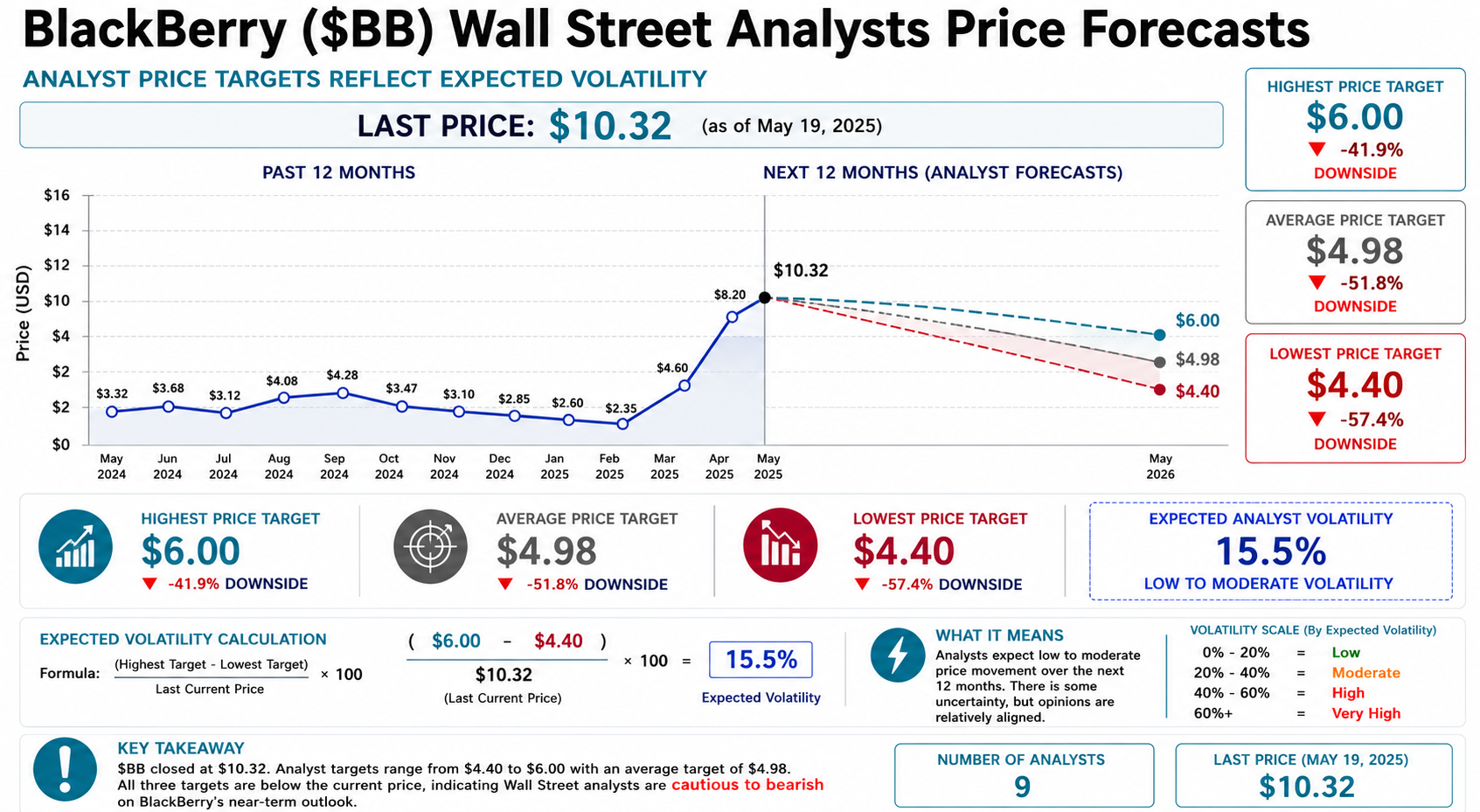

Wall Street Analysts Price Forecasts

Wall Street analysts and weather forecasters have something in common: both make bold predictions with charts, arrows, and confidence right up until reality arrives carrying a baseball bat. In the case of BlackBerry, reality arrived fast. The stock climbed to $10.32, while Wall Street’s highest analyst target sits at $6.00, the average target at $4.98, and the low target at $4.40. When the actual market price is standing comfortably above even the most optimistic forecast, it suggests analysts did not merely miss the move. They missed the move, the road, and possibly the entire map.

That leaves Wall Street with two choices. Reprice forecasts to align with improving fundamentals, stronger growth expectations, and changing sentiment, or remain preserved forever in the museum exhibit labeled: “Bad Opinions That Looked Smart at the Time.” Analysts tend to adjust slowly because changing your mind publicly is expensive in finance. Markets, however, have no such emotional attachment. Markets move first and explain themselves later.

One of the most useful lessons from this exercise is not whether analysts are right or wrong. It is understanding disagreement. The spread between the most bullish target ($6.00) and most bearish target ($4.40) creates a forecast range of $1.60. Relative to the current price of $10.32, that implies approximately 15.5% expected volatility. Traders should think of this range less as prophecy and more as a map of uncertainty. Large variance means disagreement. Disagreement creates volatility. Volatility creates opportunity, assuming you do not accidentally confuse conviction with correctness.

The takeaway is straightforward. Wall Street remains cautious to bearish on BlackBerry despite the stock already outrunning its forecasts. Either future estimates move higher as the company proves its turnaround story, or analysts risk joining rotary phones, fax machines, and BlackBerry keyboards in the nostalgia section of financial history.

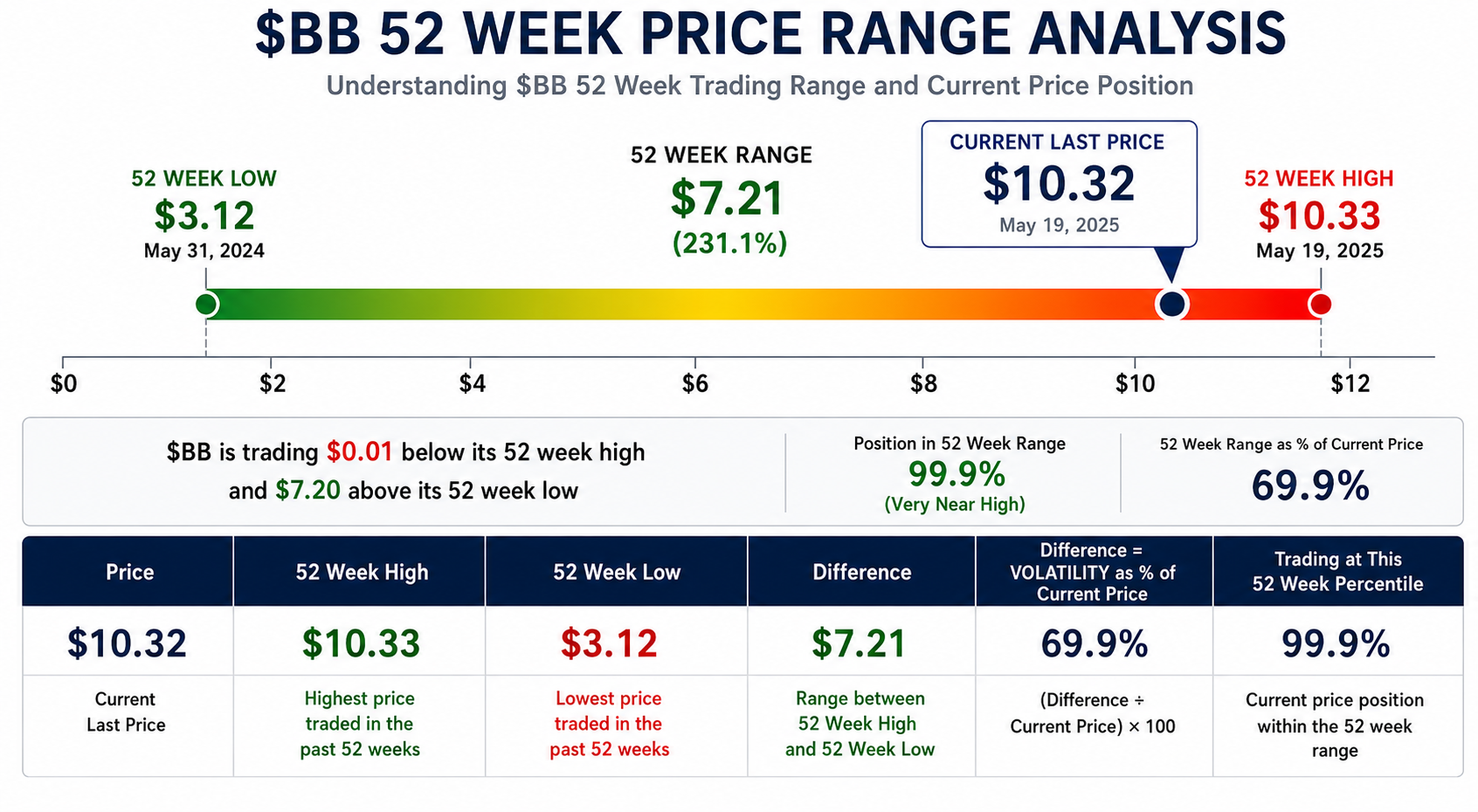

52-Week High and Low Boundaries

The most important number in BlackBerry right now is not earnings, analyst forecasts, or even the debate around cybersecurity versus QNX. It is this: $BB is trading at $10.32, just one penny below its 52 week high of $10.33 and nearly 231% above its 52 week low of $3.12. Markets rarely reward companies by accident, and they almost never push stocks to the upper edge of a yearly range unless something fundamental, or at least narrative-driven, has changed. At 99.9% of its 52 week range, BlackBerry is not quietly improving. It is screaming that investors are repricing the story.

What makes this setup especially notable is the speed of the move. Over the last year, BlackBerry went from a stock flirting with irrelevance near $3.12 to one pressing against new highs while much of Wall Street remains skeptical. The total trading range of $7.21 represents nearly 70% of the current share price, which tells traders one thing very clearly: volatility is not a side effect here. Volatility is the feature. Historically, stocks clustered near the top decile of their yearly range tend to force investors into uncomfortable decisions. Shorts cover. Analysts revise. Momentum traders pile in. Skeptics become historians.

The takeaway for traders is straightforward. Stocks sitting at 99.9% of their 52-week range deserve attention because strength tends to beget strength until proven otherwise. For the bullish case to remain intact, $BB must continue holding near these upper boundaries and avoid sharp failures back into the middle of the range. Early warning signs would be repeated failures at the $10.33 high or a decisive break below recent support zones. Right now, however, the scoreboard says something very simple: BlackBerry is trading like a company investors believe has changed, whether Wall Street analysts agree yet or not.

BlackBerry spent years wandering the market wilderness after collapsing from a 10 year peak near $28.77 to an all-time low around $2.01, a fall from grace so dramatic even the analysts stopped returning its calls. Today, at $10.32, the stock sits just pennies below its 52 week high of $10.33, proving that sometimes the market rewards survivors long before it forgives them. Even after the rally, $BB still trades roughly 64% below its former highs, which tells traders this comeback story may be early, or it may simply be catching up to historical reality.

Best-Case/Worst-Case Scenario Analysis

The best way to understand volatility is to simply measure the largest uninterrupted rallies and declines in a stock over the past year. This simple exercise provides a very real-world understanding of how quickly a stock can rise and fall, and the results can be revealing. Markets speak in price action, not opinions. And in BlackBerry’s case, the message is loud: this stock moves fast, punishes hesitation, and rewards momentum.

Let’s start with the upside because that is where the story has changed most dramatically. Over the last year, $BB delivered uninterrupted rallies of +34.8%, +40.2%, and a staggering +219.2% advance from the lows near $3.12 to current levels pressing against the $10.33 52 week high. Those are not normal moves. They suggest aggressive repricing, improving sentiment, and increasing conviction that the turnaround story may finally have traction. When stocks begin living near yearly highs after triple-digit advances, institutions tend to pay attention whether they want to or not.

The best case scenario is relatively straightforward. If improving fundamentals, QNX growth, margin expansion, and momentum continue reinforcing each other, history suggests BlackBerry can produce outsized moves much faster than traders expect. Strong trends often persist longer than logic says they should. That is particularly true when Wall Street analysts remain skeptical while price continues climbing.

Now for the part traders cannot ignore. BlackBerry also experienced uninterrupted declines of -32.5%, -14.9%, and a painful -38.2%. These pullbacks matter because they reveal the other side of momentum. This is not a stock designed for weak conviction or loose risk management. Historically, when sentiment breaks, the declines tend to be swift and emotionally exhausting.

The takeaway is simple. The best case scenario says BlackBerry remains a momentum-driven turnaround story capable of explosive upside. The worst case scenario says traders should mentally prepare for drawdowns in the 15% to 40% range, because history suggests those are normal occurrences. Respect both sides of the distribution because in a stock like $BB, volatility is not a bug. It is the product.

Next we compare $BB to the broader stock market averages.

Performance metrics are supposed to answer one question: is capital flowing toward a stock or away from it? In BlackBerry’s case, the answer is not subtle. Capital is pouring into this stock like traders just discovered the company exists again. When a stock dramatically outperforms major indexes across multiple time frames simultaneously, it usually means institutions are repricing expectations faster than analysts are updating spreadsheets.

The big picture is overwhelming outperformance. Over the last year, $BB gained 155.45%, crushing the S&P 500 Index (+28.20%), the Nasdaq Composite (+40.80%), the Dow Jones Industrials (+21.28%), and the Russell 2000 (+41.63%). More importantly, this strength is not isolated to one lucky period. BlackBerry leads across annual, six month, year to date, monthly, and weekly time frames. That consistency matters because strong stocks tend to remain strong longer than most investors expect.

Perhaps the most revealing statistic is year to date performance. While major indexes are grinding out gains between roughly 6% and 17%, BlackBerry has advanced 171.58%. That tells traders this is no longer simply a market beta story. It is stock-specific momentum. The monthly gain of nearly 85% and weekly gain above 25% also suggest momentum remains extremely powerful, though such moves historically come with elevated volatility.

The takeaway is straightforward. Relative strength is often one of the clearest indicators of where institutional money wants to be. Right now, the scoreboard says BlackBerry is not merely outperforming the market. It is operating in an entirely different zip code. The question for traders is no longer whether BlackBerry is strong. The question is whether the trend can continue before expectations finally catch up to price.

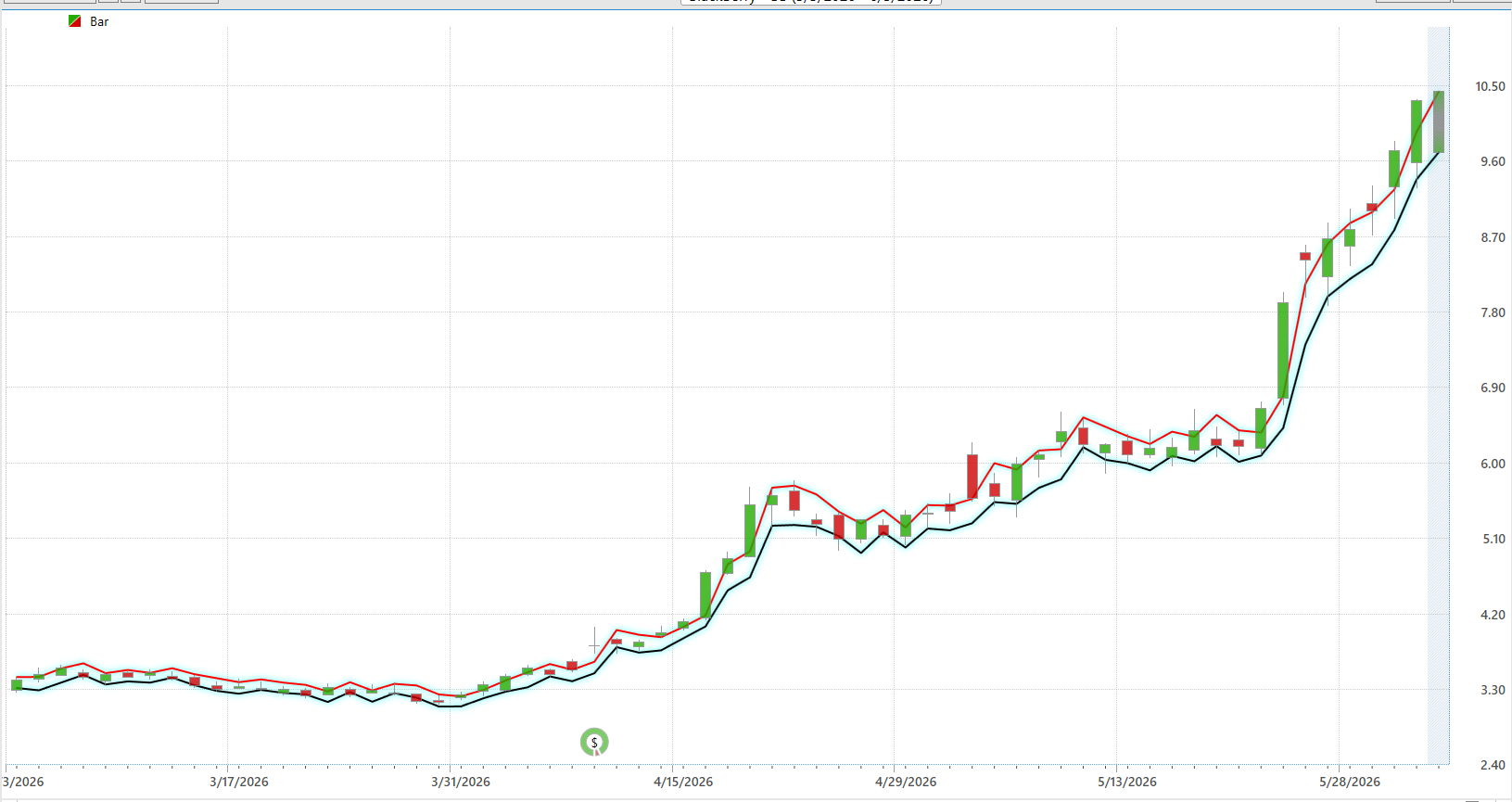

Vantagepoint AI Predictive Blue Line

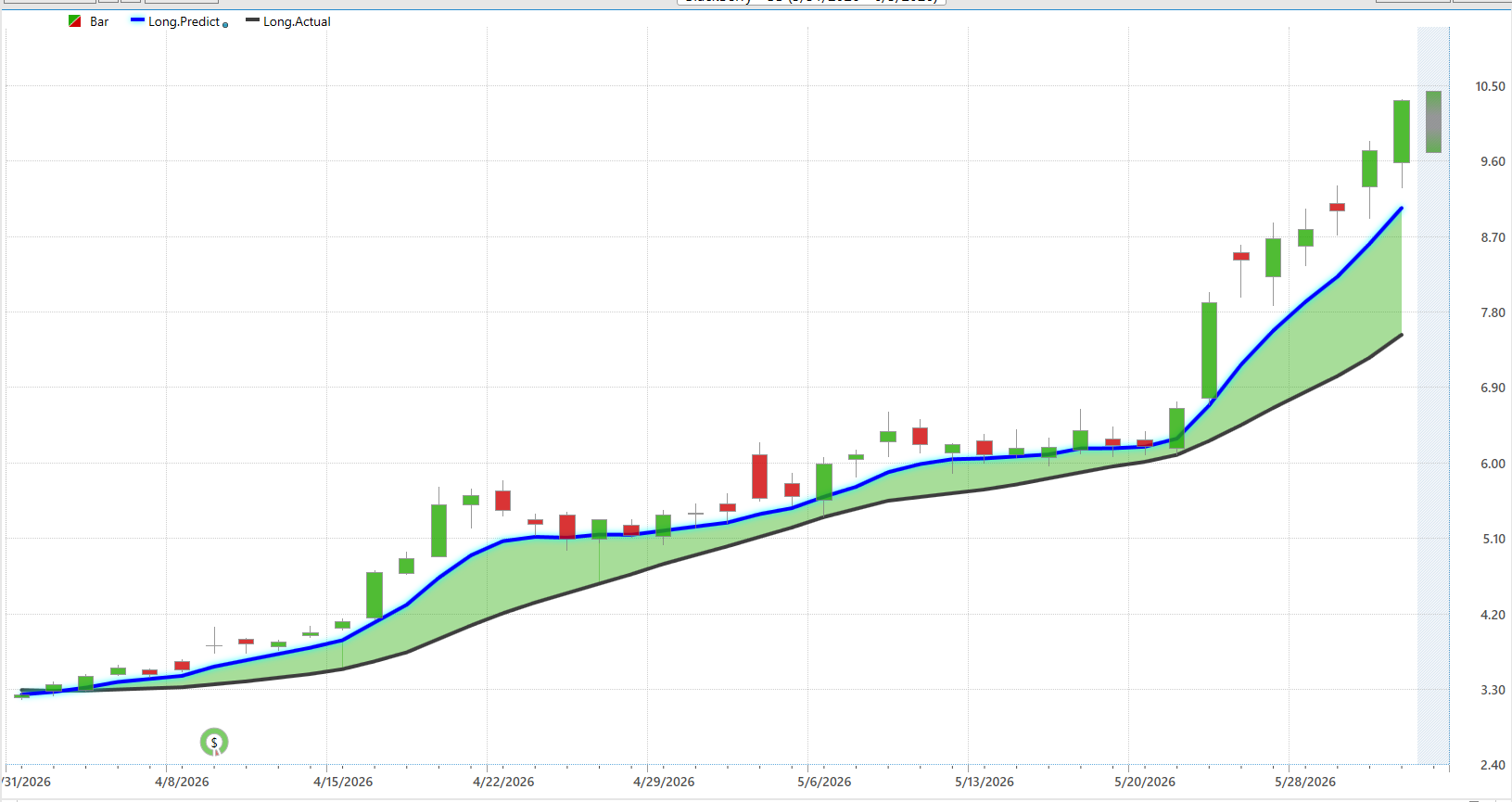

If price is the headline, the predictive blue line is the part of the story traders read before everyone else catches up. In BlackBerry’s case, the message from the chart is difficult to miss: the predictive blue line remains decisively above the black line ( 10 day simple moving average) and the spread between the two continues widening. That widening gap matters because it suggests momentum is not merely positive, it is accelerating. Markets often reward acceleration far more aggressively than stability.

What stands out is how orderly the trend has become despite the magnitude of the move. Throughout April and early May, the predictive blue line steadily climbed while the actual trend slowly followed behind. Then something changed. As price exploded higher into late May and early June, the predictive line steepened sharply upward while maintaining healthy separation from the slower actual trend line. That widening green zone between prediction and reality reflects strengthening trend conditions and increasing upside momentum.

For traders, this chart creates a relatively simple framework. As long as the predictive blue line remains above the actual trend line and continues making higher highs, the benefit of the doubt belongs to the bulls. The risk, of course, is that accelerated trends eventually create accelerated expectations. The earliest warning sign would not necessarily be price weakness itself. It would be flattening or contraction in the predictive blue line, particularly if the distance between prediction and reality begins narrowing. Right now, however, the predictive forecast is telling traders something straightforward: the trend remains firmly intact, and momentum continues to lead price higher.

VantagePoint AI Neural Index (Machine Learning)

A neural network sounds complicated because the name came from computer science instead of marketing. In plain English, a neural network is simply an artificial intelligence system designed to recognize patterns by learning from enormous amounts of historical data and relationships that humans would struggle to process simultaneously. Instead of relying on one indicator, it studies hundreds or thousands of intermarket relationships, price movements, correlations, and market behaviors to determine whether near-term strength or weakness is more probable. For traders, this matters because markets are increasingly driven by speed, complexity, and relationships across assets that traditional indicators often miss.

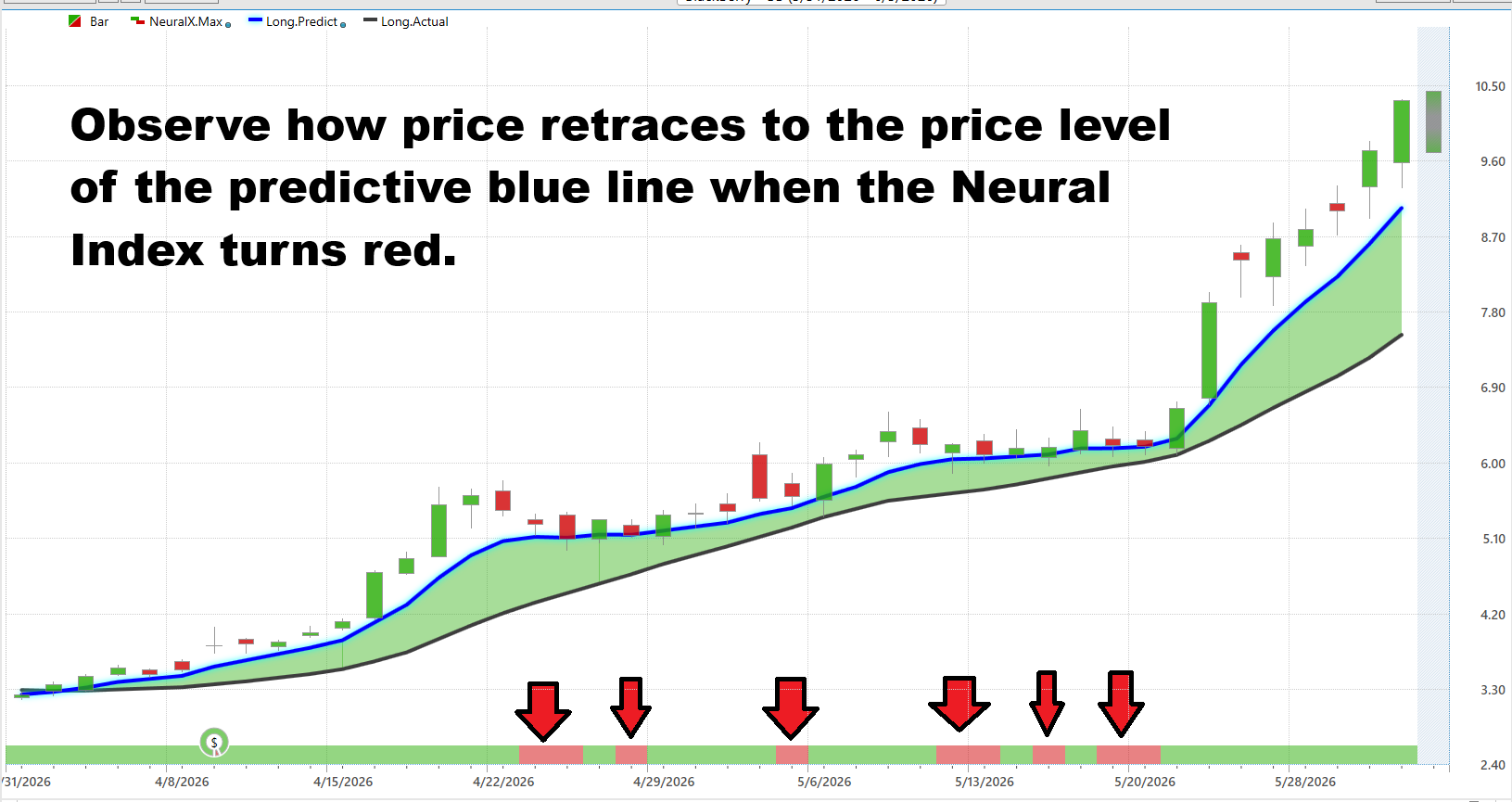

The Neural Index specifically functions as a short-term confirmation tool designed to forecast directional strength or weakness over roughly the next 48 to 72 hours. In the chart for $BB, the signal has spent the overwhelming majority of time in green, with only short intermittent periods of red. That matters because sustained green readings during a strong uptrend suggest underlying buying pressure remains intact even when price pauses or consolidates.

What makes the Neural Index particularly useful is how it improves decision making. Traders often struggle with one question: is weakness a reversal or simply a pause? Historically, when the Neural Index flips red, it frequently signals short-term weakness over the next few trading sessions rather than a complete trend change. These moments often see price retrace back toward the predictive blue line, or occasionally slightly below it, before buyers re-emerge. In strong trends, these pullbacks can become opportunities rather than warnings.

Looking specifically at BlackBerry, the pattern is revealing. Several short-lived red periods appeared throughout April and May, yet most were followed by stabilization and renewed advances as price gravitated back toward predictive support. The takeaway is straightforward: right now the combination of a rising predictive blue line, sustained green Neural Index readings, and widening separation between prediction and actual trend suggests momentum remains firmly bullish. Traders should continue monitoring for clusters of red readings because isolated signals often represent noise, while persistent red signals can indicate the character of the trend is changing.

VantagePoint AI Daily Range Forecast

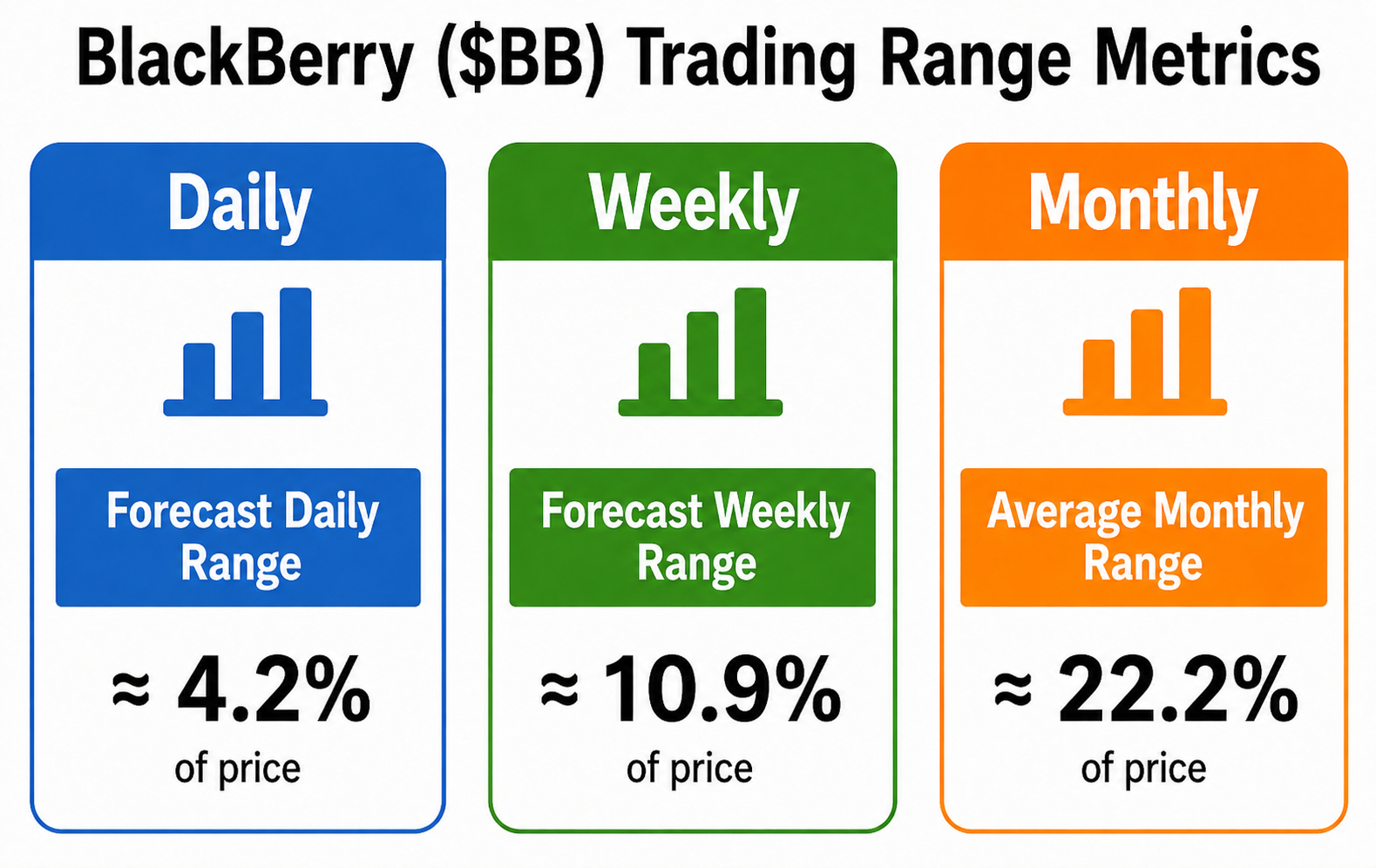

Professional traders understand a simple truth: price does not move randomly. It breathes. It expands. It contracts. And understanding the rhythm of those movements often matters more than predicting tomorrow’s headlines. BlackBerry currently exhibits a forecast daily range of approximately 4.2% of price, which immediately tells us this is not a sleepy utility stock. This is a security with enough daily movement to create opportunity, and enough volatility to punish careless execution.

The Daily Range Forecast chart reveals something more important than volatility alone. It reveals consistency. Throughout March and early April, price largely respected the forecast bands, oscillating around predicted ranges while gradually building a stronger trend foundation. As momentum accelerated into late May, the forecast range expanded along with price. That expansion matters because volatility tends to increase when institutional participation increases. Strong trends rarely emerge quietly.

At roughly 4.2% average daily movement, traders should begin each session with realistic expectations. On a stock trading near $10.32, this implies normal daily movement approaching $0.43 per day. Many traders fail because they mistake normal volatility for abnormal behavior. They sell strength too early or panic during ordinary pullbacks. Forecast ranges help solve this problem by creating context.

The most revealing feature in the chart is how closely price has respected the forecast structure during the advance. The red upper forecast band and lower projected boundary have acted less like rigid limits and more like guardrails. As long as price continues operating within or near those projected ranges, trend continuation remains the higher probability outcome.

The lesson is straightforward. Forecast ranges are statistical expectations based upon very carefully crafted probabilities. BlackBerry’s current readings suggest traders should prepare for larger-than-average daily swings while recognizing that elevated volatility is often the admission ticket for outsized returns. In markets, the stocks capable of moving the fastest usually demand the strongest stomachs.

VantagePoint AI Intermarket Analysis

Intermarket analysis is the practice of studying how different markets, industries, currencies, commodities, and asset classes influence one another. Traders use it because stocks rarely move in isolation. Capital flows between sectors, currencies impact earnings, commodities influence costs, and interest rates change behavior. The attached intermarket graphic makes this idea visible. BlackBerry sits in the center because its future increasingly depends on relationships across technology, automotive, cybersecurity, commodities, currencies, retail spending, and broader risk appetite. Think of it less like one stock and more like a traffic hub connecting multiple highways.

The biggest driver remains technology and intelligent machines. BlackBerry’s QNX operating system powers millions of vehicles and increasingly touches robotics, industrial automation, and connected devices. The intermarket map highlights these relationships through technology-heavy connections like retail tech, semiconductors, innovation ETFs, and broader market benchmarks. When money flows aggressively into growth themes, artificial intelligence, automation, and digital infrastructure, BlackBerry tends to benefit because investors increasingly view the company as part cybersecurity platform and part intelligent machine infrastructure play. Strong performance in broader growth assets often creates tailwinds.

Interest rates, currencies, and economic activity form the second layer. The chart shows exposure to currencies like the euro and yen, treasury products, commodities, and broader economic proxies because borrowing costs and economic growth still matter. Lower rates generally help speculative growth names because future earnings become more valuable. Strong economies help vehicle production, factory automation, and enterprise spending. Meanwhile, cybersecurity demand acts as a stabilizer. When uncertainty rises, cyber threats increase, or geopolitical stress builds, businesses still need protection. That creates an additional demand stream that is less dependent on consumers buying cars.

The big picture is straightforward. BlackBerry is no longer simply an old smartphone company trying to survive. The intermarket map shows a company increasingly connected to artificial intelligence, automotive technology, cybersecurity, robotics, commodities, currencies, and risk appetite itself. When these forces align, momentum can become powerful very quickly. When they diverge, volatility increases. That is why traders study intermarket relationships: because understanding what influences a stock often becomes more valuable than simply watching the stock itself.

Here are the 32 Key drivers of $BB price action.

Our Suggestion

The biggest question traders should ask is simple: Why is BlackBerry back on the leaderboards after years in the penalty box?

The answer is that the story changed faster than Wall Street adjusted. This is no longer a smartphone relic. It is increasingly viewed as a software company with exposure to automotive operating systems, robotics, cybersecurity, AI infrastructure, and embedded systems. QNX now powers systems in over 275 million vehicles with a backlog approaching $950 million, while management is expanding beyond automotive into robotics, industrial systems, and medical applications. Markets reward improving narratives long before fundamentals fully catch up. Right now, price is telling traders that institutions believe the turnaround is real.

The second big question: what are the risks? First, revenue growth remains modest relative to the magnitude of the stock move. That creates expectation risk. Second, QNX still carries heavy exposure to automotive cycles. If vehicle production weakens, growth assumptions become vulnerable. Third, cybersecurity remains competitive and pricing pressure never disappears. Finally, the stock itself has become a risk factor. When a stock rallies more than 150% annually and over 170% year-to-date, expectations can outrun execution very quickly. Traders should remember that momentum stocks rarely decline politely.

The next major event is earnings. BlackBerry’s next earnings call is currently expected around June 25, 2026 for fiscal Q1 2027, though the company labels this as a planning date until formally announced.

Heading into earnings, expectations are no longer modest. Wall Street is looking for revenue between roughly $132 million and $140 million, while consensus earnings estimates sit near $0.03 to $0.04 per share. Those numbers alone matter less than what they imply: investors are increasingly pricing BlackBerry as a company emerging from restructuring and entering a more durable growth phase. After a stock move of this magnitude, simply meeting expectations may not be enough. The market will be looking for evidence that the transformation story still has momentum.

The real focus will likely center on what sits beneath the headline numbers. Traders should pay close attention to QNX growth rates, backlog expansion, and whether Secure Communications can sustain momentum. Margin expansion remains critical because profitability, not revenue alone, is what has helped reignite investor interest. Equally important will be management commentary around robotics, industrial applications, and opportunities beyond automotive markets. And perhaps most important of all: does management raise its outlook for fiscal 2027? In momentum-driven stories, guidance often matters more than results.

The takeaway is straightforward. BlackBerry is back on leaderboards because the market believes it has transformed from a restructuring story into a growth story. The challenge now is proving that growth can justify the speed of the repricing. The next earnings report matters because momentum traders want confirmation. Skeptics want proof. Both groups will be watching the same numbers.

Use the VantagePoint AI Daily Range Forecast to isolate short term trading opportunities. Practice great money management on all of your trades.

It’s not magic.

It’s machine learning.

Disclaimer: THERE IS A HIGH DEGREE OF RISK INVOLVED IN TRADING. IT IS NOT PRUDENT OR ADVISABLE TO MAKE TRADING DECISIONS THAT ARE BEYOND YOUR FINANCIAL MEANS OR INVOLVE TRADING CAPITAL THAT YOU ARE NOT WILLING AND CAPABLE OF LOSING.

VANTAGEPOINT’S MARKETING CAMPAIGNS, OF ANY KIND, DO NOT CONSTITUTE TRADING ADVICE OR AN ENDORSEMENT OR RECOMMENDATION BY VANTAGEPOINT AI OR ANY ASSOCIATED AFFILIATES OF ANY TRADING METHODS, PROGRAMS, SYSTEMS OR ROUTINES. VANTAGEPOINT’S PERSONNEL ARE NOT LICENSED BROKERS OR ADVISORS AND DO NOT OFFER TRADING ADVICE.