In 1971, America gathered around the television to watch The Brady Bunch, a lighthearted sitcom about a blended family with six kids, a stay-at-home mom, a live-in maid, and a dad whose biggest professional challenge appeared to be remembering where he left his briefcase. No one watching thought, “This is wildly unrealistic.” They thought, “That looks about right.” It wasn’t aspirational. It was familiar.

Fast-forward to today and that same setup is treated like a fairy tale — somewhere between The Hobbit and winning the lottery. One income supporting eight people and household help? Please. That’s not a sitcom anymore; that’s science fiction. We laugh at it now the way we laugh at old rotary phones or cars without seatbelts, assuming society simply “moved on.”

But here’s the uncomfortable part we tend to skip past: The Brady Bunch wasn’t fantasy when it aired.

It was a snapshot of a middle-class economy that worked. Not perfectly, not magically, but predictably. One income bought stability. A home wasn’t a speculative asset. And no one needed a PhD in finance to make the math work.

The joke, it turns out, isn’t that the show was unrealistic. The joke is that we’re told things are better now, while quietly accepting a reality that would have baffled the Bradys, confused their maid, and probably sent Mike Brady straight back to the office asking for a raise just to keep the lights on.

Back in the 1960s, being “middle class” didn’t mean you were one medical bill away from moving in with your parents or one interest-rate hike away from developing a nervous twitch. It meant something almost exotic by today’s standards. One income paid for a house, food, a car, clothing, and the occasional vacation without requiring a ‘side hustle,’ a spouse with a second job, or a deep personal relationship with Visa and Mastercard.

The numbers themselves were almost suspiciously boring. Homes were modestly priced. Interest rates were what they were, but they applied to prices that hadn’t been inflated like a parade balloon. You didn’t need a spreadsheet to figure out whether you could afford a mortgage. You needed a pencil. Possibly not even a sharp one.

Most important, money behaved itself. It stayed roughly where you left it. Prices didn’t sprint ahead of wages like they were late for a flight. Saving money wasn’t an act of quiet heroism, it was just what happened when you didn’t spend all of it. A dollar in your pocket wasn’t auditioning for a disappearing act.

In other words, the middle class wasn’t wealthy, but it was stable. And stability, it turns out, is wildly underrated — mostly because once you lose it, everyone pretends it never existed in the first place.

Before the gold window slammed shut in 1971, the groundwork had already been laid. In the 1960s, the U.S. quietly removed silver from its coinage. Not because silver suddenly lost its usefulness, but because it became too valuable to keep in the money. When the metal inside the coin is worth more than the coin itself, the problem isn’t silver, it’s the currency. That’s not policy innovation. That’s a warning flare.

This is an old story. It shows up repeatedly in history. First, governments debase the coinage. Then they explain it with reassuring language about “efficiency” and “modernization.” What they don’t say is the obvious part: the country is spending more than it can afford. When real money disappears from circulation, it’s because it’s being hoarded, melted, or exported. People don’t do that unless they know something is wrong.

By the time Nixon closed the gold window in August of 1971, the ending was already written. Gold didn’t leave the system overnight, it was pushed out, piece by piece. Silver was the canary in the coal mine. And once you see that pattern, you realize 1971 wasn’t a sudden mistake. It was the final admission that the bill had come due.

Fiat currency sounds abstract, which is helpful, because abstraction tends to reduce panic. In practical terms, FIAT means money backed by confidence, managed by policy, and constrained primarily by good intentions. After 1971, the dollar was no longer a claim on anything scarce; it was a claim on the credibility of the institutions issuing it. This was presented not as a gamble, but as progress.

The immediate effects were underwhelming, which is precisely why the shift worked. There was no instant collapse, no visible crisis, and no reason for the average household to object. Inflation crept in gradually, prices rose steadily, and wages followed just enough to maintain the appearance of balance. The system didn’t break. It stretched. And stretching, unlike breaking, is easy to normalize.

The illusion came from the measuring stick itself. When the unit used to measure wealth is slowly shrinking, rising numbers feel like success. Homes appear more valuable, portfolios look healthier, and incomes seem larger. But what’s actually happening is dilution, not enrichment. Fiat currency didn’t make people richer, it made the difference between nominal growth and real prosperity harder to see.

This is where the trick really gets good. Prices start going up, and everyone nods approvingly. Your house is worth more. Your portfolio is bigger. Your neighbor feels smarter. On paper, we’re all doing great. And if you question this, you’re gently reminded that rising prices are a feature, not a bug. Growth, they call it. Progress, if they’re feeling poetic.

In 1971, the average homebuyer faced a 7.5% mortgage on a $28,000 house, which translated into about $175 a month in interest. Crude, yes, but at least legible. You didn’t need a finance degree to understand what was happening to your money. You paid the bank, you paid yourself, and at the end of the month there was usually something left over.

Fast-forward 54 years of well-intentioned policies, subsidies, innovations, and earnest press conferences designed to make housing “more affordable,” and the result is a 6% mortgage on a $420,000 house, roughly $2,100 a month, just for interest. The rate went down. The payment exploded. And, somehow, we’re told this is a victory.

So, congratulations are apparently in order.

And that’s the illusion in a nutshell. Bigger numbers everywhere, smaller lives underneath.

We mistake price inflation for prosperity, and debt for wealth, because the scoreboard keeps going up.

The problem isn’t that homes became expensive. It’s that the measuring stick quietly shrank and nobody bothered to tell the passengers.

The reason The Brady Bunch now reads like escapism has less to do with shifting values and more to do with arithmetic. The economic structure that made a single-income household viable no longer exists. Housing, healthcare, education, and basic living costs have risen faster than wages for decades, not because families suddenly became irresponsible, but because the price of participation in the middle class steadily increased.

As a result, the two-income household didn’t emerge as a lifestyle upgrade. It emerged as a requirement. What was once a buffer: an additional income for savings, security, or discretionary spending, became the baseline needed to service housing costs, manage debt, and absorb inflation. The modern household works more not to accumulate wealth, but to maintain stability.

This is often framed as a cultural evolution or a change in priorities, but that misses the point. The shift was driven by monetary dynamics, not personal choices. When the purchasing power of money erodes over time, households compensate the only way they can: by supplying more labor. The disappearance of the one-income family was an economic necessity created by a system in which money quietly lost its ability to do what it once did.

Currency debasement has a branding problem. When people hear the term, they imagine hyperinflation, wheelbarrows, and collapse. What happens in developed economies is far more orderly and far more effective. The value of money declines gradually, predictably, and with enough technical language to keep it out of casual conversation. Nothing breaks. It just costs more.

Because the process is incremental, it’s rarely identified as the cause of anything. Housing becomes “unaffordable,” healthcare becomes “complex,” education becomes “an investment,” and wages are said to be “lagging.” Each issue is debated in isolation, as if they were unrelated phenomena rather than symptoms of the same underlying dynamic. The monetary system fades into the background, treated as a constant rather than a variable.

The result is a form of collective misdiagnosis. People sense that something is wrong, but the explanation is always elsewhere: zoning laws, demographics, globalization, technology. Those factors matter, but they operate within a framework defined by the currency itself. When the unit of account is quietly diluted over decades, the economy doesn’t announce it. It simply recalibrates around lower purchasing power and calls the adjustment normal.

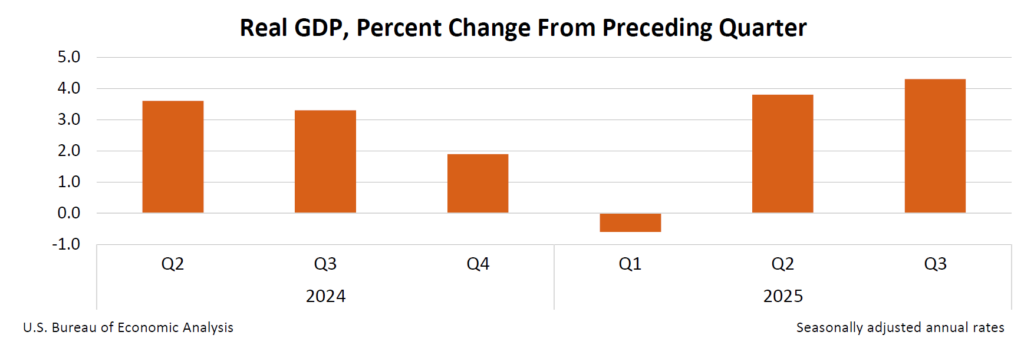

Lately, the rumor mill in finance has been humming with talk of blockbuster GDP growth in 2026. The Trump administration is promoting 5 to 6 percent GDP groweth, maybe more. Champagne numbers. The kind of figures that make economists beam and politicians suddenly discover spreadsheets. On the surface, it sounds impressive — until you remember that GDP measures activity, not well-being. A house that costs twice as much and requires two incomes to service counts as “growth,” even if it leaves everyone more stressed and permanently one layoff away from panic.

Source: U.S. Bureau of Economic Analysis

If the analysts were serious, they’d stop tracking GDP and start tracking something far more subversive: how many 30-year-olds can afford to buy a home without parental assistance or a financial miracle? Then check the 40-year-olds? The 50-year-olds? At some point, an economy that produces glowing growth statistics but can’t house its own working population starts to look less like success and more like a very elaborate accounting trick.

In the 1960s, a working 30-year-old didn’t need a trust fund, a dual income, or a miracle to buy a home: they needed a job. That was it. A paycheck, a modest mortgage, and some discipline, and the deal got done. Today, that same 30-year-old can do everything right, work hard, save diligently, avoid dumb mistakes — and still be priced out like he wandered into the wrong auction. We call it a “market,” we call it “progress,” but what it really is is a system that moved the goalposts so far downfield that owning a home before middle age went from expectation to fantasy, and we’re all supposed to pretend that’s normal.

Housing used to be the byproduct of a functioning economy. Now it’s a luxury good, priced like one, financed like one, and defended as one. And yet we’re told to celebrate growth as if rising output automatically translates into rising lives. It doesn’t. It just means more money is changing hands, often to solve problems that didn’t exist when money still knew how to behave.

That’s the real lesson of Brady Bunch economics. The goal wasn’t growth for growth’s sake. The incentives were aligned toward stability, affordability, and predictability. When an economy can house its middle class on one income, you don’t need to brag about GDP. The scoreboard takes care of itself.

Housing has become America’s favorite political bar fight: loud, emotional, and guaranteed to end with someone throwing a chair. Every politician in Washington now claims to be the Champion of Affordable Housing, which is impressive, because none of them can explain, slowly and with or without crayons, how affordability is supposed to work in the real world. They shout “make housing cheaper” the way medieval villagers shouted “bring rain,” as if yelling at the sky were a serious economic policy.

Here’s the small, inconvenient math problem they keep tripping over. If interest rates stay high, home prices eventually fall. Great news for first time buyers, until you realize this also detonates the balance sheet of the Boomer class, for whom the house is not a place to live but a 30-year-old retirement strategy with vinyl siding. Watching home prices drop is, for them, like watching the value of their pension go up in flames while a senator assures them it is “for the children.”

So, the alternative is to slash interest rates. Monthly payments look friendlier, politicians pat themselves on the back, and everyone pretends this is progress, right up until housing prices take off like a NASA launch. Lower rates do not make houses cheaper. They make them more expensive in nicer fonts. Congratulations, you can now afford the payment on a home that costs twice as much as it did five minutes ago.

Pick your poison. High rates anger homeowners. Low rates lock out buyers. There is no magical third option, despite what the fancy presentation slides in Washington suggest. The uncomfortable truth is that nobody in D.C. believes in the free market anymore. They believe in managing, nudging, tweaking, stimulating, rescuing, and “fixing” it, usually right after they have broken it. And they are far too blind, arrogant, and self important to admit that decades of economic micromanagement have turned the housing market into a policy Frankenstein, stitched together with good intentions, animated by cheap money, and now rampaging through the countryside wondering why no one can afford a place to live.

Here’s the punchline no one wants to say out loud: The Brady Bunch didn’t become unrealistic because people changed. It became unrealistic because the money did. The rules quietly shifted, the measuring stick shrank, and everyone was told this was “normal.” Smile, nod, and work more hours.

A system that once rewarded stability now rewards leverage. A system that once made saving easy now punishes it. And when people struggle, we blame their choices instead of the framework that made those choices inevitable. That’s not an accident. That’s how bad systems protect themselves: by convincing you the problem is personal.

So, stop chasing the illusion. Stop measuring success by numbers that rise while life gets harder. The lesson isn’t nostalgia. It’s clarity. When money works, families work. When money breaks, everything else follows. The bill didn’t disappear. It just took 50 years to arrive. Fiat currency is a shell game run by accountants, narrated by economists, and staged on a set so elaborate you don’t notice your wallet getting lighter until the curtain call.

Traders heading into 2026 might want to keep their seatbelts fastened and their coffee within arm’s reach, because this is shaping up to be the kind of market that humbles certainty and punishes complacency. Sharp swings will not be bugs in the system, they will be features, and anyone expecting smooth diversification is likely to discover that correlations have a nasty habit of converging right when you need them not to. Commodities will continue to act like the market’s truth serum, sniffing out monetary excess and policy drift long before the official data admits it, while central banks keep improvising in a world they no longer fully control. In an environment like this, the job is not to predict every twist and turn, but to stay flexible, respect price behavior, and remember that when money is being managed by committee, markets tend to move by ambush.

Now, more than ever, the preservation of wealth depends on clear judgment and disciplined action. When the value of money is steadily reduced, the greatest risk is not volatility but being positioned on the wrong side of a sustained move.

VantagePoint A.I. trading software was built to address that single problem. It removes opinion, emotion, and guesswork, and replaces them with objective analysis designed to identify trend direction before it becomes obvious.

What makes trading with VantagePoint’s artificial intelligence revolutionary is not speed or complexity, but purpose. VantagePoint A.I. does not react to headlines or narratives. Its sole function is to analyze market behavior and forecast probable direction so the trader can align with strength and avoid weakness. The goal is simple and practical: keep you on the right side of the right trend at the right time, where probabilities do the heavy lifting.

For those who wish to see this process firsthand, we invite you to attend a free live online masterclass. You’ll learn how traders use VantagePoint A.I. to make clearer decisions, reduce emotional errors, and adapt to changing markets with confidence. There is no cost to attend — only the opportunity to understand how disciplined, data-driven trading can help protect and grow your capital in an era of ongoing debasement.

Register for the masterclass here.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.