Tokenization is a big word for a simple idea. Imagine owning a pizza, you could sell the whole thing or each slice separately. Now imagine that same pizza isn’t food — it’s a building, a painting, or a company. Tokenization takes something valuable in the real world and breaks it into small digital pieces called tokens. Each token represents fractional ownership and lives on a blockchain — a secure digital ledger that records who owns what. Instead of lawyers, bankers, and piles of paperwork, you can buy or sell those pieces instantly, like sending an email.

At its core, tokenization is doing for finance what the internet did for information — making it fast, global, and accessible. Today, trading or transferring ownership can take days and cost money as it passes through layers of middlemen. Tokenization changes that. It divides assets — real estate, bonds, art — into tradeable digital shares. Smart contracts — self-executing programs on the blockchain — automate rules and payments, ensuring transfers happen exactly as intended, without human delay or error.

The improvement to finance is profound. Transactions that took days now settle in seconds. Investments once requiring millions can be accessed for a few dollars. Transparency becomes standard because every trade is recorded on the blockchain. Fewer intermediaries mean lower fees, and fractional ownership brings liquidity to previously frozen markets. A building in New York, a sculpture in Paris, or a bond in Tokyo could all exist as tokens — traded globally, 24/7, without friction.

From thirty thousand feet, tokenization looks like the next great upgrade to the global financial system. It’s when the paper-based world of ownership finally catches up to the digital age. Just as music shifted from CDs to streaming and movies moved from DVDs to Netflix, assets are becoming digital, portable, and programmable. Tokenization isn’t about speculation, it’s about transforming how value itself moves, connecting every market, investor, and asset into one continuous, global network.

What happens when every asset — stocks, bonds, real estate, even fine art — becomes a tradable token on a blockchain? Ownership will no longer be locked inside vaults or brokerages but will move fluidly across digital networks at the speed of code. A trader in Singapore could buy a fraction of a New York skyscraper while someone in Paris sells part of a California solar farm — all in seconds, without bankers, borders, or bureaucracy. This isn’t science fiction — it’s the next logical step in market evolution.

The thesis is simple but seismic: tokenization will transform global finance the way exchange-traded funds (ETFs) revolutionized investing. Just as ETFs unlocked access, liquidity, and transparency for everyday investors, tokenization will do the same on a far grander scale — blurring boundaries between traditional and digital markets and democratizing access to wealth. The traders who understand it early — who learn how tokenized assets are created, valued, and exchanged — will lead the next decade of innovation.

In trader’s terms, tokenization means converting ownership rights of an asset into a digital token on a blockchain. Each token represents full or fractional ownership, recorded permanently and securely. It’s the difference between needing a middleman to tell you what you own and having that proof built into the asset itself.

Tokenization isn’t cryptocurrency. Bitcoin and Ethereum are new forms of money; tokenization is about reinventing ownership. It gives existing assets — stocks, bonds, real estate, commodities — a digital twin that moves as easily as a text message. It doesn’t replace money — it makes everything else move with the same speed and simplicity as digital cash.

To see this in action, imagine a ten-million-dollar office building split into ten thousand digital tokens. Each represents one ten-thousandth of the property. Anyone, anywhere, can buy, sell, or trade those tokens around the clock. Ownership changes hands in seconds, every transaction recorded automatically. Or picture a Tesla share represented as a token. Instead of waiting two days for settlement, the trade clears almost instantly — and that same token can be used as collateral for a loan across borders, with no paperwork or delays.

Behind this shift is a technological trio rewriting the rules of finance: blockchain, smart contracts, and digital custody. Blockchain ensures every transaction is verifiable and tamper-proof. Smart contracts automate settlements and payments the instant conditions are met. Digital custody replaces clearinghouses and custodians with cryptographic security. Together, they form the foundation of a faster, fairer, and more fluid market.

Liquidity has always been the heartbeat of finance, but tokenization gives that heart a pacemaker that never turns off. In traditional markets, there are opening bells, closing prices, and weekends off. Tokenized assets trade globally, across time zones, without friction from borders, currency conversions, or clearing delays. It’s finance operating on internet time.

The quiet revolution is fractional ownership. Assets once locked behind massive capital requirements — a skyscraper, a corporate bond, a painting — can be divided into thousands of tradable tokens. Participation is no longer limited to institutions. A teacher in Nairobi, a developer in Berlin, and a trader in Chicago can all trade the same sliver of a global asset pool. Liquidity, once a privilege, becomes a participation right.

Continuous liquidity pools complete the transformation. Tokenized assets flow through decentralized global platforms, where buyers and sellers connect directly. Markets become continuous, real-time, and always “on,” powered by automated smart contracts and global demand.

Consider a tokenized real-estate fund or U.S. Treasury moving seamlessly across borders. In today’s system, those trades take days and intermediaries. In a tokenized world, they settle instantly, fractionally, and securely. Settlement delays will seem as outdated as waiting for a check to clear.

For traders, this is a paradigm shift. Liquidity is no longer dictated by institutions — it’s crowdsourced. Market depth is created not by market makers alone, but by a global network of participants. The market never sleeps, and neither does opportunity.

Tokenization’s inevitability rests on five pillars: efficiency, liquidity, transparency, cost reduction, and institutional momentum. Traditional settlement cycles take days; tokenized assets settle in seconds. Fractional tokens expand participation. Every transaction is verifiable on-chain. Smart contracts reduce intermediaries and costs. And major players — BlackRock, JPMorgan, Citi, and governments from Singapore to Switzerland — are already embracing it. Like streaming replacing DVDs, tokenization is replacing paper-based ownership. The future of finance isn’t waiting for permission — it’s already being coded.

Tokenization won’t just change how assets are recorded — it will transform how trading works. Markets will become truly 24/7, with crypto, stocks, and commodities merging into one continuous ecosystem. Smart contracts will handle dividends, interest, and margin calls automatically. Collateral will move instantly, unlocking liquidity once trapped in illiquid holdings. And with on-chain transparency, volatility will be reshaped by real-time data rather than secrecy. Tokenization won’t just change what traders trade — it will change how they see the market.

Back in 1993, Wall Street dismissed the first ETF as a novelty. Three decades later, ETFs are the backbone of global investing. Tokenization is poised to do the same — only faster. The idea is simple: take a traditional asset and turn it into a digital token that moves as easily as information. You could send a U.S. Treasury as effortlessly as a text, and that kind of efficiency makes regulators sweat and traders grin.

Skeptics are singing the same tune they did about ETFs: “This will never work.” Then it does. Innovation in finance isn’t polite — it arrives, knocks over the filing cabinets, and rewires the system. Adoption is slow until it’s sudden, ignored until it’s everywhere.

Tokenization isn’t a new wrapper; it’s a rebuild. Today’s financial plumbing is creaky, slow, and expensive. Tokenization replaces it with instantaneous settlement, transparency, and automation. It’s as transformative as the smartphone was to communication — changing not just tools, but human behavior.

This revolution stretches beyond Wall Street. Tokenization isn’t just efficient, it’s inclusive. Imagine a teacher in Jakarta holding a slice of the S&P 500 in her digital wallet as collateral for a loan, or a worker in London sending instant, interest-bearing payments to family in São Paulo. Tokenization opens doors long closed to ordinary investors. For institutions, it’s a chance to modernize their DNA — making assets portable, programmable, and alive.

The debate is no longer whether tokenization works — it does. The question is whether established players will adapt or watch new entrants build a parallel system that outpaces them. History isn’t kind to institutions that wait for permission to innovate. The system is ready. The benefits are undeniable. The choice is clear: climb aboard or be left on the dock as the new economy sails away.

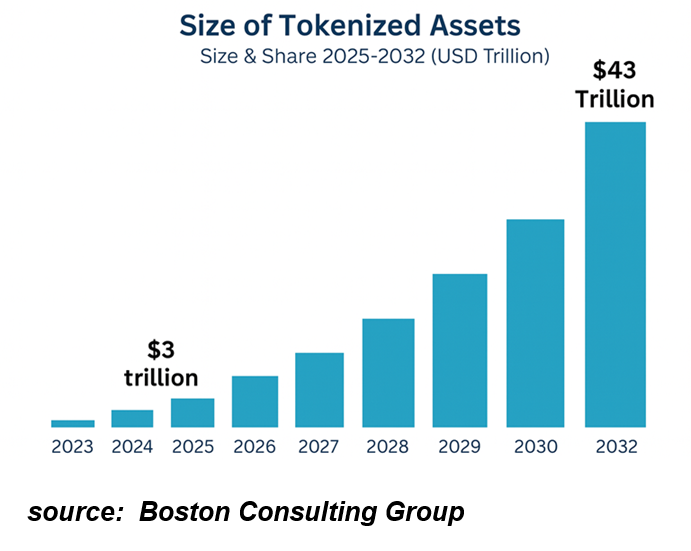

Look at that chart — it doesn’t climb, it erupts. Boston Consulting Group says tokenized assets are set to explode from $3 trillion to $43 trillion by 2032. The traders who grasp this shift early won’t just ride the wave — they could own the ocean.

The current financial system, for all its prestige, is a marvel of inefficiency. It’s like sending an email that takes two days and requires three signatures to arrive. We can stream 4K video from across the world in seconds, yet moving money from New York to London still feels like sending a carrier pigeon with a business degree. Every transaction trudges through layers of custodians and clearinghouses, each taking a bite as it passes.

But that’s how every legacy system looks before it gets replaced. People once swore they’d never shop online or store data in “the cloud.” Then came Amazon and AWS, and the old world quietly folded. Tokenization is that story playing out in finance.

What it’s really saying to the old system is: thank you for your service, but your shift is over. Streaming killed the DVD, email buried the post office, and blockchain will turn ownership into something frictionless and programmable. It’s not rebellion — it’s evolution.

And then there’s transparency — Wall Street’s favorite word in press releases but least favorite in practice. Tokenization doesn’t promise transparency; it enforces it. Every transaction and ownership transfer is recorded on a public, tamper-proof ledger. No “trust us,” no fine print, no proprietary opacity. When trust is verified by code instead of conference calls, the middlemen start to look less like stewards and more like toll collectors on a road that no longer needs them.

Publicly, Wall Street applauds this shift. Privately, it’s terrified. Transparency erases shadows, eliminates hidden fees, and exposes decades of creative accounting disguised as “market structure.” Tokenization threatens the fog that keeps their power intact. When every transaction is verifiable in real time, the “trust us, we’re professionals” routine collapses.

So yes, they’ll talk about innovation, fund research, and host blockchain conferences — but that’s not adoption; it’s containment. The foxes are building fences before the chickens learn to fly. Tokenization doesn’t just change how finance operates; it changes who controls it. And that’s why Wall Street smiles for the cameras while quietly praying this “transparent ledger” thing blows over before the next earnings call.

Every major technological revolution comes with the same script: confusion, skepticism, and a tiny group of people who see the opportunity before everyone else. The internet, smartphones, social media, even streaming — all began as fringe experiments that suddenly went mainstream once someone made them easy, accessible, and irresistible. The lesson is simple: the leaders of each boom aren’t always the ones with the best technology; they’re the ones who simplify adoption and scale trust faster than the herd can react.

Take AOL in the 1990s. They didn’t invent the internet, and they weren’t the fastest or the most sophisticated. What they did was genius — they made getting online simple. Those shiny free trial CDs filled every mailbox in America. You didn’t need to understand modems or TCP/IP — just pop in the disk, follow the steps, and boom: “You’ve got mail.” AOL didn’t sell the internet; they sold access. And for a few years, they owned the gateway to a new digital world simply because they made the complex frictionless. That’s how revolutions start — not with the most advanced technology, but with the most usable one.

We’ve seen the same playbook in every tech boom since. When Apple launched the iPhone in 2007, smartphones already existed. Blackberry and Nokia had them. What Apple did was make them intuitive turning a phone into a lifestyle device. Suddenly, the internet wasn’t something you logged into; it was something you carried in your pocket. When Netflix pivoted from mailing DVDs to streaming movies, people thought the bandwidth wasn’t ready. But Netflix bet on convenience — and convenience always wins. Even Tesla, mocked early for building “luxury toys,” understood the formula: don’t just sell technology, sell a movement.

Learning from these cycles means recognizing patterns, not products. The winners of each era made it easier for people to cross the bridge into something new. They lowered friction, told better stories, and created communities around progress. Traders and investors who study these leaders — rather than waiting for mass acceptance — get a crucial head start. They understand that before every tidal wave of adoption, there’s a calm where the smart money is quietly positioning.

Tokenization is shaping up to follow the same arc. It’s early, complex, and easy to dismiss. But, some company or platform — is going to play the AOL role, making blockchain finance drop-dead simple for the masses. They’ll turn wallets into something your grandmother can use, and the world will change overnight. The key to catching the next wave is learning from history. The leaders of every tech boom didn’t chase the herd. They watched where the world was headed, built the bridge first, and made sure everyone else could walk across it with ease.

Among the traditional giants of global finance, several major banks and brokerages are quietly positioning themselves to lead the coming wave of asset tokenization. They see the same transformation that electronic trading, exchange-traded funds, and online brokerage once brought — only this time, the infrastructure itself is changing. Each of these institutions brings deep liquidity, regulatory credibility, and global client bases that could make the difference between tokenization remaining a niche experiment and becoming the backbone of the financial system.

J.P. Morgan has been among the most aggressive in moving tokenization from theory to practice. The bank developed its own blockchain-based network, Onyx, and introduced a digital deposit token known as JPM Coin, which allows institutional clients to move value instantly across borders. It is also exploring tokenized representations of money-market funds and other securities, giving clients access to programmable cash and near-instant settlement. Because J.P. Morgan already dominates in global payments and custody services, it’s uniquely positioned to integrate tokenized assets directly into the existing financial system, rather than trying to build an alternative one.

UBS is following a similar path through its “UBS Tokenize” platform, which enables the issuance and distribution of tokenized bonds, structured products, and investment funds. The Swiss bank has already completed several real-world pilots, including tokenized fixed-income securities on public blockchains. UBS’s strength lies in its ability to combine its wealth-management network with institutional market access, allowing it to bridge traditional investors and the emerging world of digital securities. By making complex assets easily tradable on-chain, UBS is demonstrating how tokenization can serve both high-net-worth clients and global institutions simultaneously.

Citigroup has also stepped forward with initiatives focused on tokenizing private-market assets, such as pre-IPO shares and alternative investments. Partnering with Switzerland’s SIX Digital Exchange, Citi aims to use blockchain infrastructure to modernize settlement and unlock liquidity for traditionally illiquid assets. As one of the largest custodians and securities-services providers in the world, Citi’s involvement signals that tokenization is not just a fintech curiosity but an institutional priority. Its scale and regulatory relationships could make it a critical player in bringing transparency and interoperability to global markets.

Meanwhile, Goldman Sachs and BNY Mellon have joined forces to create tokenized versions of money-market funds for institutional investors. This may sound modest compared to crypto experiments, but it represents an important bridge between traditional capital markets and blockchain infrastructure. For firms that already manage trillions in client assets, the ability to settle instantly and provide 24/7 liquidity is more than a convenience, it’s a competitive advantage. Goldman and BNY Mellon are proving that tokenization doesn’t require a revolution overnight; it can evolve quietly through practical use cases that improve efficiency without frightening regulators.

Even U.S. Bancorp, a smaller player compared to the global behemoths, has recognized the shift underway. The bank recently formed a dedicated digital-assets unit focused on tokenization and blockchain-based payment systems. This move underscores how tokenization is no longer confined to experimental labs or crypto startups — it’s becoming a mainstream banking objective. For regional and national banks alike, digital assets represent a chance to modernize operations, reduce settlement risk, and offer new investment products in tokenized form.

Collectively, these moves mark a turning point. The financial establishment isn’t ignoring blockchain anymore, it’s absorbing it. Tokenization gives these firms the chance to reinvent the infrastructure of finance while preserving their relevance in an increasingly digital world. Whether it’s J.P. Morgan’s efficiency, UBS’s innovation, Citi’s scale, Goldman Sachs’s adaptability, or U.S. Bancorp’s agility, each is racing to capture the same prize: the role of gatekeeper in a market that may soon have no gates at all.

Let’s get something straight: VantagePoint’s A.I. isn’t just the future of trading — it’s the present. Traders still clinging to old habits are fighting a heavyweight bout with one hand tied behind their back. Because artificial intelligence has quietly crossed the line from novelty to necessity. It doesn’t trade on emotion, bias, or bad headlines. It trades on probabilities, patterns, and precision. It learns from every tick of data and gets better every day while human traders burn out, hesitate, or second-guess.

At VantagePoint, we don’t chase hype — we build proof. Since 1991. Every A.I. forecast we deploy must pass a brutal five-year gauntlet of machine learning tests and meet one non-negotiable requirement: a minimum 70% verified accuracy rate. That’s not marketing — it’s protection. It’s how we preserve our credibility and your capital. Because while others throw darts at the market, we refine the math that drives smarter, faster, more profitable decisions.

But here’s the truth no one on financial TV will tell you: the market no longer rewards the bold — it rewards the informed. A.I. is the difference between guessing and knowing. Between catching the move and watching it happen without you. The traders using it aren’t superhuman; they’ve simply outsourced their weaknesses and amplified their strengths. A.I. doesn’t get emotional, distracted, or tired, it just works.

That’s why we’re inviting you to something rare: a Free Live Trading Masterclass where we’ll show you, in real time, how A.I. identifies trades before the herd sees them coming. You’ll watch how it spots the patterns no chart or talking head can reveal, and we’ll even show you three stocks our predictive models have flagged as ready to move.

This isn’t magic, it’s math. It’s about leverage — the kind that comes from insight, not risk. This is your chance to see how professional-grade A.I. can turn your trading from reactive to predictive… and your portfolio from uncertain to unstoppable.

So, ask yourself: are you ready to stop gambling and start compounding? 👉 Click here to claim your free seat. Don’t wait. The markets are evolving — with or without you.

It’s not magic.

It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.