If you’ve been trading long enough, you already know something most beginners eventually discover the hard way. Markets don’t ring a bell before they do something violent. One surprise headline. One geopolitical shock. One overnight futures plunge. And suddenly the stock you were confidently holding is opening 8% lower before you even have time to react.

Right now, traders are navigating a landscape filled with uncertainty. The war in the Middle East has added another layer of geopolitical risk to already fragile markets. At the same time, the broader economic backdrop is hardly comforting. Rising government debt continues to expand at a pace that concerns policymakers and investors alike. Inflation, while no longer at peak levels, remains sticky enough to keep interest rates higher than many expected.

Beneath the surface, parts of the market, particularly high-growth technology sectors, show signs of valuations that could prove vulnerable if sentiment suddenly shifts. Individually, none of these forces necessarily trigger an immediate crisis. But together they create something far more dangerous. They create an environment where volatility becomes the norm and markets react violently to headlines.

Economic shocks can spread through financial markets faster than investors expect.

This is where traders quietly separate into two camps. The first group tries to call the top, call the bottom, catch the big move, and brag about it later. The second group takes a very different approach. They build strategies designed to survive when the market refuses to cooperate.

That second group tends to be silent and stays in the game a lot longer.

Right now, many of those traders are quietly doing something that does not look flashy on social media. They are collecting premium using put credit spreads. They are not trying to predict every twist in the news cycle or guess the next economic surprise. They are positioning themselves so that time, probability, and trend work in their favor.

Because today’s markets move fast. Faster than most traders expect.

Prices whip around on geopolitical headlines, economic data, and algorithmic flows that can push markets violently in one direction and then reverse them just as quickly. Large overnight gaps have become more common, and those gaps punish traders who rely on perfect timing or oversized directional bets.

That reality forces disciplined traders to rethink how they operate. Instead of swinging for the fences on every trade, many professionals shift toward strategies that lean toward generating premium while protecting capital.

The focus: define risk before entering the trade, favor probability over prediction, and allow the market’s natural tendency toward time decay to work in your favor.

This is where put credit spreads enter the picture. They allow traders to participate in strong uptrends while strictly limiting the downside risk if the market suddenly turns against them.

It may not be the most glamorous strategy. But in unpredictable markets, discipline can best heroics.

The first rule of trading is something almost nobody believes until the market personally demonstrates it with a two-by-four. Your first job is not to make money. Your first job is not to lose money.

That may sound as exciting as a lecture from your high school algebra teacher. But the market has a way of turning this boring little rule into the most important idea you will ever learn. Volatility changes the entire game.

News shocks hit the tape and suddenly stocks open five percent lower before coffee has finished brewing. Emotional markets exaggerate every move. Fear and greed start acting like they have been drinking tequila together all weekend. And leverage, which looked so clever when the trade was working, suddenly behaves like a financial chainsaw.

In other words, mistakes get amplified.

This is why traders who survive chaotic markets develop a slightly paranoid attitude about risk. They want to know the worst possible outcome before the trade ever happens. They avoid positions where losses can grow into something that resembles a small national debt. And instead of trying to predict every twitch of the market, they start thinking in terms of probabilities.

That shift in thinking quietly separates professionals from amateurs.

Once traders begin focusing on defined risk and probability, the toolbox naturally changes. Strategies that limit downside exposure start looking far more attractive than heroic all-or-nothing bets. Which is exactly why many disciplined traders eventually arrive at a very practical solution.

They start using credit spreads.

At its core, the options market is built on a very simple economic exchange that looks remarkably similar to the insurance business. One participant is looking for protection. The other is willing to provide it for a price.

When traders sell options, they are effectively stepping into the role of the insurance company. The buyer pays a premium for the right to protection against a specific price move. The seller collects that premium in exchange for accepting the obligation tied to that contract.

It is a straightforward transaction, but one rooted in a statistical reality that experienced traders understand well.

Most options expire worthless.

This is not a flaw in the system. It is the system working exactly as designed. Options are time-sensitive instruments. Every day that passes brings the contract closer to expiration, and with that passage of time the value of the option gradually erodes. For traders who sell options, this phenomenon known as time decay becomes a structural advantage.

This dynamic is why many professional traders gravitate toward strategies built around premium collection rather than premium speculation.

When you sell premium, the trade does not require perfection. The underlying asset can move higher. It can move sideways. In many cases it can even decline modestly and the trade can still succeed. As long as price remains within a defined range, the option’s value continues to decay, allowing the seller to retain the premium collected at the outset.

But this approach carries an important caveat.

Selling options without protection, often called naked option selling, can expose traders to theoretically unlimited losses if markets move violently against the position. In volatile environments, that risk can quickly become unacceptable. For that reason, many disciplined traders turn to structures that maintain the advantages of premium collection while strictly controlling downside exposure.

That is where defined-risk spreads enter the picture.

Options traders, like bankers and insurers, tend to prefer arrangements where the risks are known in advance and the math is tolerable. One of the cleaner structures that accomplishes this is the put credit spread.

At its simplest, a put credit spread is built from two transactions executed at the same time and with the same expiration date. The trader sells one put option and buys another put option at a lower strike price. The short put generates income. The long put acts as protection if the market falls further than expected.

Think of it as a small financial sandwich.

The premium collected from the put you sell is larger than the premium paid for the put you buy. The difference between those two prices becomes a net credit deposited into the trader’s account immediately.

Consider a simple example.

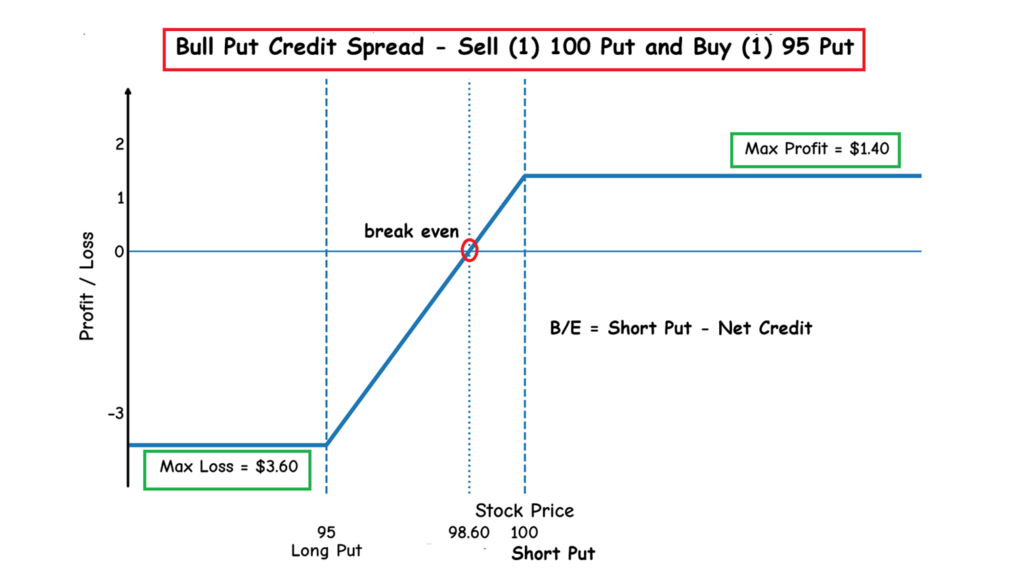

Imagine a stock trading at $110. A trader sells the $100 put. At the same time, the trader buys the $95 put, both with the same expiration date. The short $100 put brings in more premium than the $95 put costs, so the trader receives money upfront for establishing the spread.

From there the economics are straightforward.

The maximum profit is the credit received when the spread is opened. If the stock remains above $100 at expiration, both options expire worthless and the trader keeps the entire premium.

The maximum loss is also clearly defined. It is the width between the strikes, in this case $5, minus the credit received at entry. If the stock falls below $95, the protective put limits any additional damage.

This is why the structure appeals to disciplined traders.

The trade does not require the stock to rally dramatically. In fact the stock does not need to rise at all. It simply needs to stay above the short strike price. As long as the market remains above that level, time decay quietly works in the background and the trader collects the premium that was paid at the start of the trade.

Let’s get something straight right away.

A put credit spread is a bullish trade. But not the chest-thumping, high-testosterone kind of bullish where you are betting the farm on a massive breakout. This is a calmer, smarter kind of bullish.

Traders are not trying to predict fireworks. Traders are simply saying the market is strong enough not to collapse.

That distinction matters. Because a put credit spread does not need a huge rally to work. It does not need a viral headline, a surprise earnings blowout, or a rocket ship move to the moon. It just needs the market to behave reasonably.

And in an uptrend, the odds of that happening improve.

There are three very friendly scenarios where put credit spreads quietly do their job.

First, the obvious one. The stock keeps rising. The market marches higher, the strike price stays safely below the action, and time decay slowly melts the value of the option sold.

The premium collected becomes the trader’s.

Second scenario. The stock goes sideways. No drama. No excitement. Just boring consolidation above support. Traders get impatient. Headlines get quiet. But for the credit spread seller this is beautiful.

Time keeps passing, the option keeps losing value, and the position quietly moves toward profitability.

Third scenario. The stock pulls back a little. Not a collapse. Not a panic. Just a mild dip that stays above the strike price you selected.

Still fine.

Because when a put credit spread sells below the market, it’s saying something very simple. “I believe this stock will stay above this level for the next several weeks.”

This is choosing a price level that strong trends are unlikely to violate. And that is the key.

Learning how to trade put credit spreads is like discovering you don’t have to swing for the fences every time you step up to the plate. Instead of betting the farm on a big move and hoping the market cooperates, a trader gets paid upfront simply for being reasonably right. When a stock is trending higher, they can position themselves below the market, collect premium, and let time quietly work in their favor while the crowd argues about headlines. They know the risk before the trade begins, they know the potential reward, and they don’t need perfection to win. The real beauty is this: these traders are building a disciplined process that steadily pulls income out of the market one calculated trade at a time.

Strong trends act like a tailwind. They push probability and make it far more likely the spread expires harmlessly, leaving the trader with the premium and the satisfaction of having taken another small, disciplined bite out of the market.

But if you ever want to see a trader age one decade overnight, introduce them to the concept of selling naked options.

On paper it looks fantastic. The premium rolls in. The probabilities look friendly. The strategy feels sophisticated, almost professional. For a while everything works beautifully. Then one morning the market wakes up on the wrong side of the bed and decides to demonstrate what the word unlimited actually means.

That’s the problem.

Selling naked options, the income may be limited but the potential loss can be about as contained as a bar fight in a crowded saloon. A single violent move can turn a comfortable trade into a financial experience that resembles a small natural disaster.

I view put credit spreads like a seatbelt in a car driven by someone who just discovered espresso.

With a put credit spread, it’s selling one put and buying another put at a lower strike price. That second option may feel unnecessary at first. It costs money. It reduces the amount of premium collected. But what it really does is something far more valuable.

It can cap the damage.

No matter how ugly things get, the maximum loss is already defined. The worst possible outcome is known before the trade even begins. That may not make traders happy, but it does keep them from experiencing the sort of financial trauma.

And in volatile markets, that protection becomes even more important.

Markets today can gap down overnight for all sorts of reasons. Geopolitical developments. Economic shocks. Earnings surprises that arrive with the subtlety of a bowling ball through a window. By the time the market opens, the price may already be somewhere entirely different from where it was the night before.

Limited risk changes how a trader reacts to those moments.

Instead of panic, there is perspective. Instead of emotional decision-making, there is structure. Because when the trade was opened, the worst-case scenario was already on the table.

And that knowledge allows traders to do something rare in volatile markets. Remain calm.

Defined-risk trades like credit spreads help control the potential loss on a single position, but the trader must still control how much capital is exposed. This is where position sizing becomes the quiet backbone of professional trading.

Seasoned traders operate under a rule that sounds simple but carries enormous consequences.

No single trade should threaten the portfolio.

The goal is not to win every trade. The goal is to remain in the game long enough for probabilities to work in our favor. That requires structuring positions so that an unexpected loss becomes an inconvenience rather than a catastrophe.

A common guideline many experienced traders follow is to risk between 1% and 3% of total trading capital per trade. This may seem conservative to beginners, especially when markets appear full of opportunity. But this discipline is precisely what allows professionals to endure the inevitable losing streaks that occur in every trading career.

Losses are part of the business.

When risk is limited to a small percentage of capital, a string of unsuccessful trades does not destroy the account. The trader retains both financial and psychological capital, which is just as important. Confidence remains intact. Decisions remain rational.

Credit spreads make this process much easier.

Because the maximum loss of the spread is known at the moment the trade is entered, position sizing becomes a straightforward calculation. The trader can determine in advance exactly how much capital is at risk and adjust the size of the trade accordingly.

This clarity transforms the entire exercise.

Trading stops resembling speculation driven by excitement or fear. Instead, it becomes a disciplined process of measured risk management, where every position fits within a carefully controlled framework designed to protect capital first and grow it steadily over time.

In a put credit spread, strike selection is where probability is built.

You are not just picking numbers. You’re defining the line in the sand where the trade either works or fails.

One common approach is to sell spreads beneath major support levels. Support represents areas where buyers have previously stepped in with conviction. If the market has respected that level multiple times, placing your short strike below it adds an extra layer of protection. In essence, you are positioning your trade underneath a price zone where demand has historically appeared.

Another method many traders use involves probability metrics. Options markets constantly estimate the likelihood that a strike price will finish in or out of the money. Experienced traders often look for strikes with roughly 70% to 85% probability of expiring worthless. This means the market itself is suggesting that the odds favor the spread expiring safely.

But perhaps the most powerful factor is trend confirmation.

When a stock is making higher highs, it signals persistent demand. When it is outperforming the broader market, it shows leadership. And when price action reflects institutional accumulation, it indicates that larger players are steadily building positions.

These are the environments where put credit spreads tend to thrive.

Strong trends act like a tailwind. They support the price structure beneath the market and make it less likely that the stock will collapse through your strike level. By selecting strikes below support, aligning with probability metrics, and focusing on assets in strong uptrends, traders quietly stack the odds in their favor.

In the end, successful strike selection is about positioning the trade where probability and trend are already working on your side.

Markets have a habit of becoming chaotic at the worst possible moments.

Headlines appear without warning. Prices gap overnight. Volatility expands and markets begin moving faster than most traders can react. In these environments, prediction becomes unreliable and emotional decisions become dangerous.

This is where discipline becomes far more valuable than brilliance.

Consider a practical example. Suppose volatility expands and a trader begins selling $5 wide put credit spreads while collecting $1.40 in premium. Each winning trade generates $140. The maximum theoretical loss is $360 if the spread moves completely against the position.

However, most experienced credit spread traders rarely allow the trade to reach that maximum loss.

Instead, many adopt a simple rule: place a stop roughly equal to the premium collected. In this case, the trader would exit the trade if losses approach $140. This adjustment dramatically changes the risk profile. Instead of risking $360, the trader risks roughly the same amount they stand to gain.

Over a large sample of trades, that shift improves the probabilities.

Put credit spreads allow traders to collect premium, define risk, benefit from time decay, and participate in strong trends without exposing the portfolio to catastrophic downside. They transform trading from speculation into structured probability.

And when markets become especially volatile, one principle matters more than any indicator or forecast.

Always know your worst-case scenario.

Because if the worst case is manageable, the trader remains calm, survives the chaos, and stays in the game long enough for probability to work in their favor.

The markets ahead will reward a different kind of trader.

Not the loudest voice. Not the boldest prediction. The trader who wins will be the one who sees clearly. The one who knows where the trend is forming, where risk is building, and where probabilities are quietly shifting beneath the surface. They will observe what the market is doing rather than insisting on what it “should” be doing. They will follow evidence, control risk, and understand that markets can be generous one moment and punishing the next. In an environment like this, balance is not hesitation. It is strength.

That clarity is exactly what VantagePoint A.I. now makes possible.

Instead of guessing where the market might go next, imagine having a software that continuously analyzes thousands of intermarket relationships and forecasts where strength is emerging and where weakness is beginning to appear. That is the power of VantagePoint A.I. It allows traders to align themselves with the dominant trend while defining risk with precision.

If you would like to see how this works in real time, I invite you to attend a free live online masterclass where you can discover VantagePoint A.I. in action. During this session you will learn exactly how the technology identifies emerging trends, highlights potential turning points, and helps traders position themselves before the crowd catches on.

Reserve your seat and discover how trading with A.I. can help you approach the markets with greater confidence, discipline, and consistency.

Unlike human analysis, VantagePoint A.I. does not become distracted by headlines, narratives, or emotion. It focuses only on what matters. It evaluates intermarket relationships, trend direction, and probability-driven signals across multiple time frames simultaneously. In effect, it performs the analytical work that most traders attempt manually and rarely accomplish effectively.

This kind of intelligence provides a different form of leverage. Not financial leverage, but decision leverage. Instead of reacting late, you gain earlier awareness. Instead of chasing moves after they are obvious, you begin to recognize the conditions that precede them. Over time, this is how consistency is built.

And consistency is ultimately the trader’s greatest advantage.

Register for your VantagePoint A.I. Masterclass here.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.