I’ve been watching the Fed since the 1980’s. By no means do I consider myself an expert. But in all those years I’ve learned a thing or two I’d like to share with you.

The consensus of the population is the Central Planners at the Fed are expert managers and have control and knowledge in everything they do and every decision they make. My purpose in writing this article is not to throw stones at the Fed. Instead, it is to challenge the paradigm of Central Planning which is how the Fed functions.

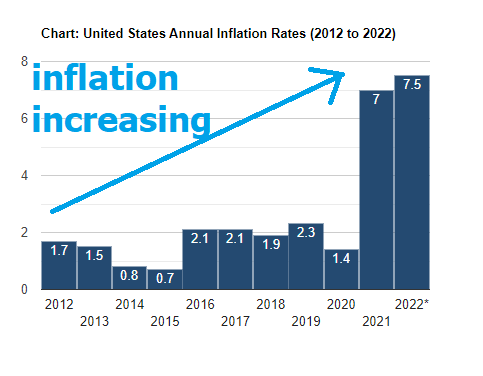

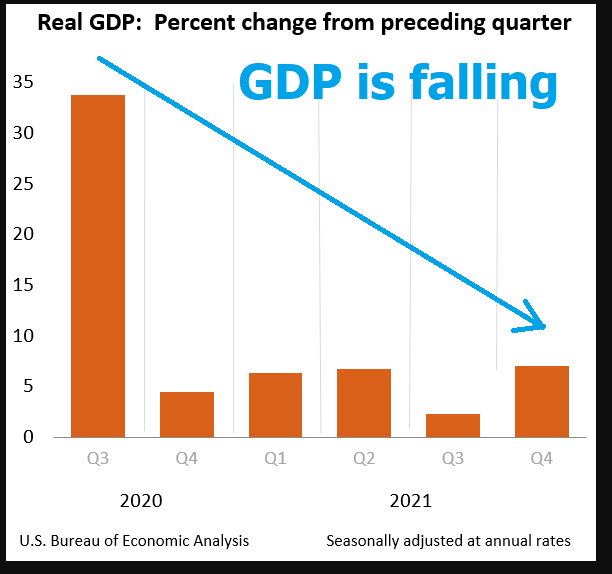

Over the last 30 years the Fed has continually manipulated Interest Rates to near-zero with the justification that this would spur economic growth. The solution to all the economy’s problems according to the Fed was cheaper money to create more jobs and more productivity. But here we are with their grand vision having come to fruition and instead we have record debt levels, slowing GDP and rising inflationary pressures. This has all been accompanied by among the best unemployment numbers in the last 50 years.

Call me suspicious, but this is exactly what was not supposed to occur.

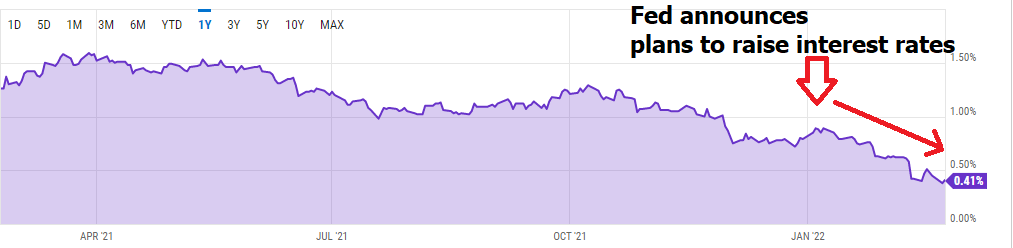

Over the last two months, Fed Chairman Jerome Powell through the Fed’s Open Market Committee and through its allies in the banking community has signaled multiple times they were going to stop making bond purchases and begin raising interest rates. As a matter of fact, the stories in the economic media tell us that there are four planned interest rate increases for 2022 and 3 more for 2023. People take these pronouncements as being the gospel truth without ever stopping to examine their possibility or feasibility of occurring. The only way this can occur is if the population receiving the communication is completely ignorant of economics.

Let me explain.

Often in the media there is great talk and bluster about the word ‘recession.’ This word is very easy to define on an individual basis. For an individual the word recession means “contraction.” If you’re working at a job and you are forced to take a 10% pay cut to keep your job, you are experiencing a recession.

However, when we look at the collective economy the word “recession” is much more nuanced. When economists talk about the aggregate economy there are essentially four major distinctions all related to GDP growth and inflation. The four possibilities are as follows:

- Inflation is falling. GDP growth is accelerating.

- Inflation is increasing. GDP growth is accelerating.

- Inflation is falling. GDP growth is decelerating.

- Inflation is increasing. GDP growth is decelerating.

Before you can wrestle with trying to understand the Fed edicts and pronouncements you need to determine where we are with relation to inflation and GDP growth.

When I look at these primary metrics, I see that inflation is increasing.

And GDP is decelerating.

This is the worst of all four possibilities regarding inflation and economic growth. But to add fuel to the fire the Fed is announcing they’re going to stop their bond purchases and increase interest rates in this the most precarious of economic environments.

Hmmmmm.

Let me tell you why I am beyond suspicious this can ever occur.

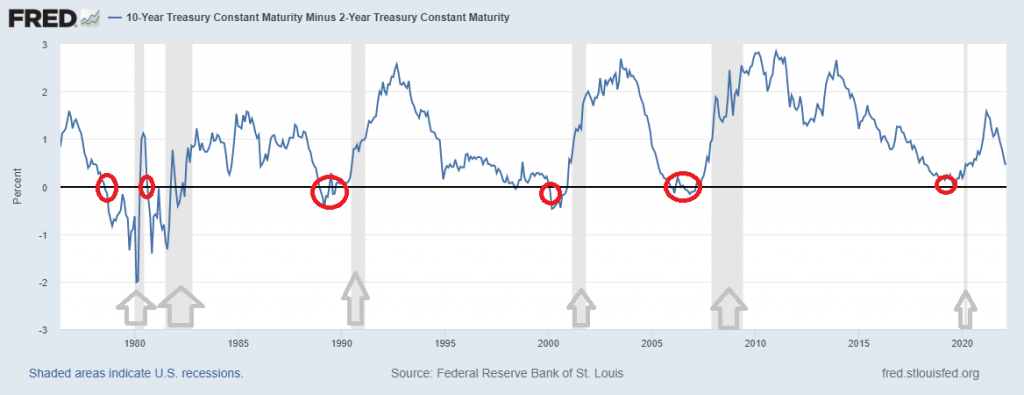

The one indicator everyone in the business world uses to measure whether a recession will occur is the YIELD CURVE. I recently wrote an article about the yield curve which you can find here.

All that an investor or trader needs to do is look at the spread between the 2-year T-note and the 10-year t-note and you will see that the spread has been contracting massively over the past two months. This is time coincident with the Fed announcing that they were planning or raising interest rates.

FACT: The most the Fed can increase interest rates is the value of this spread without inverting the yield curve and causing a recession.

As I write this, it is trading at 41 basis points. Yesterday it was at 38 basis points.

The reason I consider this significant is the Fed has absolutely ZERO room to maneuver without inverting the yield curve and pushing the economy into a recession.

Let’s explore.

When the Fed raises interest rates the increase is traditionally 25 basis points or ¼ of a point. So, if the Fed raises interest rates by 25 basis points, we expect that the best-case scenario for the yield curve would be subtracting 25 basis points from its current value of 41 basis points. Even for that to occur we would have to make a huge assumption this spread would remain stable and not contract any further.

Why is this important?

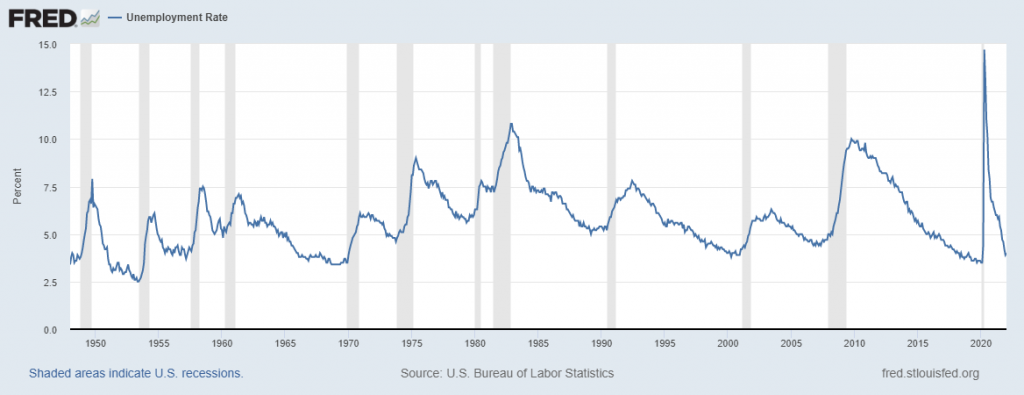

Because once the yield curve goes negative, we traditionally see a recession within 6 months in the economy. These recessions are not to be taken lightly! They are periods of great economic unrest. The grey areas on the chart are the time frames where the recessions occurred. These were moments when we saw a “contraction” of GDP accompanied by increased unemployment.

Economists say there have been 33 recessions in the United States since 1854 through to now in total. Since 1980, there have been four such periods of negative economic growth that were considered recessions.

In 1980 the Fed Funds rate reached 20% to combat double digit inflation. It’s a completely different battlefield today when interest rates are stuck at near zero percent.

The challenge for the FED is they know if they raise interest rates, they can trigger a full-scale recession or depression simply based upon how much debt has been created since the economic lockdowns and pandemic began two years ago. Based upon the spread of the yield curve being only 41 basis points my conclusion is that they do not have the room to raise interest rates more than one time. I think that the FED recognizes that they want to raise rates to fight inflation but doing so at this stage of the economic cycle will collapse the economy.

In 2019 they raised rates and almost crashed the economy and the markets when they said they would taper their bond purchases. Since that time frame they increased their bond purchases exponentially and dropped interest rates to zero for the last three years.

Since the Great Financial Crisis of 2008, and the “Too Big To Fail” aftermath in the markets, and the economy I have never witnessed an environment where we have rising inflation, decreasing GDP and the FED raising rates thinking they are going to make things better.

- If the FED moves to raise interest rates, they invert the yield curve.

- If they raise interest rates again, they guarantee the recession will be deeper and longer. And let’s not forget that this is an election year.

Here is a question for you to ponder the next time you hear the media talking about the Fed raising interest rates and tapering their bond purchases. Over the last 13 years the Fed has increased their balance sheet by over $9 trillion.

30% of the companies in the Russell 3000 stock index cannot cover their interest payments with their earnings. The Fed has been supporting these companies for 13 years by purchasing their junk bonds when no one else would. What happens to all the ZOMBIES when the Fed cuts their bond purchases?

The Fed wants to give off the image that it is all knowing and all powerful, but it is very limited in its choices. Since they manipulated interest rates to zero over the last decade, they have created quite a unique dilemma for themselves.

You’re familiar with these companies, AMC, Macy’s, Boeing, ADT, ROKU, the four major airlines (Delta, United, American, and Southwest), Mattel, Carnival, Exxon Mobil, and Marriott International, to name just a few. When the Zombie company employs too many people the narrative becomes “too big to fail”, like it did in the 2008 financial crises.

The monetary policies seen over the past decade have exacerbated the Zombie company problem. The historically low interest rates, coupled with quantitative easing (QE) have helped these companies amass over $2.6 trillion in debt that they cannot service. A decade of binge borrowing has turned many corporations into the walking dead. This level of indebtedness impedes their ability to hire and continues to spur on malinvestment.

These deeply indebted companies are trying to muscle through their troubles by borrowing even more money from the Fed.

So, what is the Fed going to do?

My opinion is they will kick the can down the road and make sure that they do not address the real structural issues in the economy since it is politically unfeasible to do so.

I suspect some ZOMBIE company will cry potential bankruptcy and the Fed will re-entertain their “too big to fail” policies which have been completely ineffective for the last 13 years.

Make no mistake about it, 2022 is an election year and the Fed, while it’s supposed to be agnostic to the political process, is very much a political creature. The last thing the Fed wants to be responsible for is an economic recession or depression in an election year.

The long and short of it that the spread between the 2-year note and 10-year note tells a trader how many basis points the Fed has to work with. Right now, the margin is too thin, and my conclusion is that regardless how many people say the Fed will raise rates 7 times in the next two years, I’ll put my chips on the economic reality they simply are powerless to do anything that will help the economy.

I think a much higher probability is that they will continue to flood the economy with money and continue to debase the currency.

And so, we’ve arrived at that long-awaited monetary policy endpoint.

What does this mean to you as an investor and trader?

As more and more money is being printed and the Fed continues to support financial markets it is crystal clear how fragile the economy is. In my opinion, they cannot afford to not support markets without the whole house of cards come tumbling down.

Dollars are being debased. Financial assets are increasing in price because the Fed is purchasing assets that no one else will.

While I have shared my opinion with you about what I see is the fundamental current economic environment, I want to be clear I never let my opinion interfere with my trading decisions.

My reality is always formed by what I see, hear, feel, and understand. I’ve come to appreciate that what I see, hear, feel, and understand is a very small universe indeed. Therefore, I use artificial intelligence, neural networks, and machine learning to guide my trading decisions.

Everybody has had horrible trades. The difference between the winners and losers in life is that the winners learned very powerful lessons from their losses.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution. This is the Feedback Loop that is responsible for building the fortunes of every successful trader I know.

If you think about this question, you will begin to appreciate that AI applies mistake prevention to discover what is true and workable. Artificial Intelligence applies the mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

That should get you pretty excited because it is a game-changer.

It sounds very elementary and obvious. But overlooking the obvious things often hurt a traders’ portfolio.

The basics are regularly overlooked by inexperienced traders.

It is very sad, and unnecessary in today’s day and age of machine learning and artificial intelligence.

A stock may have a very alluring story.

A stock may have a very effective management team.

A stock may have incredible earnings.

A stock may have infrastructure, partnerships, uniqueness, etc.,

But, if these elements are not reflected in the price, you are focused on what “SHOULD” occur in the market.

And the word should is responsible for more losses in trading than any other.

Bad Traders Obsess on the SHOULD. Every other word out of their mouths’ is SHOULD.

I can’t recall how many times a trader has told me all the reasons why his portfolio is heavily invested in a stock because of a great story, in spite of the stock being in a firm downtrend. It is horribly painful to listen to.

The beauty of neural networks, artificial intelligence and machine learning is that it is fundamentally focused on pattern recognition to determine the best move forward. When these technologies flash a change in forecast it is newsworthy. We often do not understand why something is occurring but that does not mean that we cannot take advantage of it.

I think the Fed will continue in the race to debase. When traders recognize their only real option is flooding the economy with more money, we are going to have a massive stock market meltup soon.

But I do not let that opinion get in the way of my trading behavior. I’ve learned to balance my analytical insight which is often wrong with the power of world class trend analysis which has proven to be up to 87.4% accurate.

Most humans have a really hard time learning from bad experiences. The ego gets in the way, each and every time.

Since artificial intelligence has beaten humans in Poker, Chess, Jeopardy and Go!, do you really think trading is any different?

Knowledge. Useful knowledge. And its application is what A.I. delivers.

You should find out. Join us for a FREE Live Training.

We’ll show you at least three stocks that have been identified by the A.I. that are poised for big movement… and remember, movement of any kind is an opportunity for profits!

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

Intrigued? Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.