The conventional approach for bullish options traders has long been straightforward: buy a call and wait for the move. The problem, as many discover, is that time is rarely on their side. Premiums decay, expectations fall short, and a significant percentage of these trades expire worthless. Today we are going to explore a unique options trading tactic that pros are using very effectively in trending markets. It is called a ZEBRA which stands for Zero Extrinsic Back Ratio. The name sounds technical, but the idea is straightforward. You are using options in a smarter way to control risk and reduce time decay.

The Zebra strategy reframes the time decay equation. It is designed to replicate the economic exposure of owning stock, but with defined risk and far more efficient use of capital. Structurally, the trade involves purchasing two deep in-the-money call options while simultaneously selling one at-the-money call, all within the same expiration cycle. The objective is precise: use the premium collected from the short call to offset most of the time value embedded in the long calls.

Most people trade options and they lose because options are deteriorating assets. The options premium is composed of time value which is also known as extrinsic value and instrinsic value. The Zebra zeroes out the extrinsic value risk as much as possible and allows traders to control 100 shares of stocks for every ZEBRA they build.

The result is a position that behaves much closer to the underlying equity itself. Price movement translates more directly into profit and loss, often allowing traders to participate in gains almost immediately following an upward move. Unlike a traditional long call, where the break-even point can sit meaningfully above the current price, the Zebra’s break-even is typically positioned much closer to where the stock is trading.

From a risk perspective, the structure is equally deliberate. The maximum loss is defined upfront, limited to the initial debit paid to establish the position. While this introduces a higher capital commitment than a single call option, it remains significantly lower than purchasing shares outright, offering a middle ground between leverage and capital efficiency.

The deeper in the money an option is the lower the time value (extrinsic value) associated with its premium. On the other hand, at the money call options are composed of 100% time value.

The deep in the money options hold mostly intrinsic value, while the option you sell brings in premium to offset time decay.

This options structure creates a synthetic position where the profit and loss resemble the underlying movement of the stock. If the stock goes up, a trader makes money. If it goes down, a trader loses money. But unlike stocks, a trader does not have to put up the full amount of capital.

In plain English, a trader is controlling the same 100 shares with less money. They’re reducing the daily bleed from time decay. And doing it with a structure that puts the odds significantly more in a trader’s favor. Simply put, we are looking at financial engineering using options.

Before a trader can understand a ZEBRA, they need to understand what they’re paying for when a trader buy an option. Every option has two parts. One part is real. The other part is temporary. If a trader cannot separate the two, a trader is not trading. A trader is guessing.

Intrinsic value is the tangible piece. It answers a straightforward question. What would this option be worth if it expired today? The math is clean. For a call option, the trader subtracts the strike price from the current stock price. If a stock is trading at $100 and the strike is $70, the intrinsic value is $30. That number is not theoretical. It reflects real, immediate value embedded in the contract.

Extrinsic value, by contrast, is where interpretation enters the picture. Often referred to as time value, it is the portion of the option’s price that exceeds its intrinsic value. It reflects what traders are willing to pay for the possibility that favorable price movement occurs before expiration. Time remaining, expected volatility, and overall market demand all shape this premium. The formula is equally straightforward. Take the option’s market price and subtract its intrinsic value. What remains is extrinsic value.

But the implications are more nuanced. Extrinsic value is not static. It decays. As the clock moves toward expiration, that speculative premium erodes, regardless of whether the underlying stock moves. This is where many traders find themselves on the wrong side of the equation. They are directionally correct, but structurally disadvantaged.

In this sense, the distinction between intrinsic and extrinsic value is more than a definition. It is a framework. It forces the trader to ask a more precise question. Am I paying for what is real, or am I paying for what might happen? The answer often determines the outcome.

This is where most traders get into trouble. They buy options loaded with extrinsic value. The stock moves in the right direction, but time decay works against them. The trade feels right, but the outcome is wrong. Not because of direction, but because of structure.

This is exactly why the ZEBRA matters. Deep in the money options are mostly intrinsic value. There is very little time premium left to decay. And when a trader sells an at-the-money option, they collect maximum extrinsic value. The result is a position where time decay is reduced. They’re no longer fighting the clock.

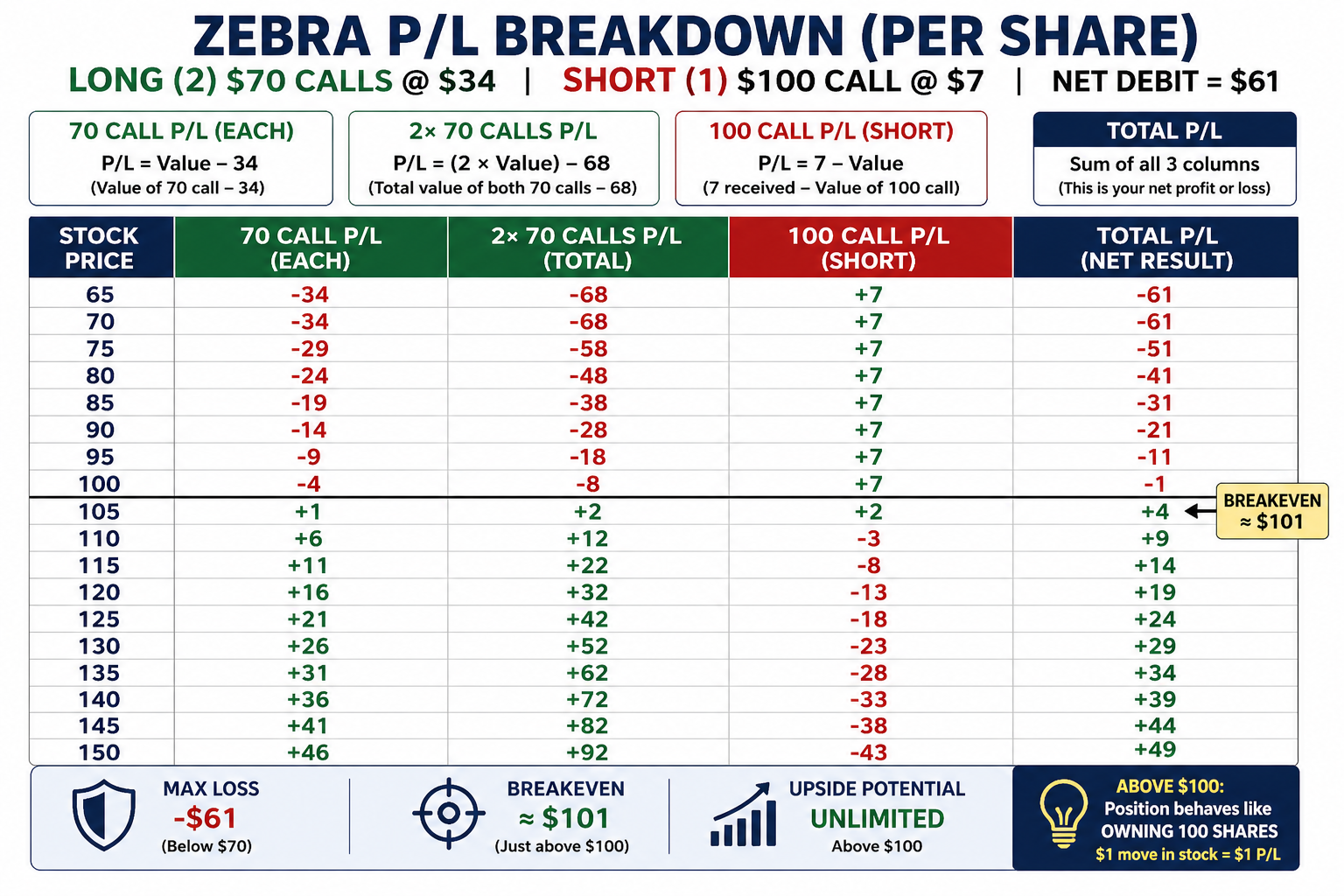

Let’s walk through a simple example so you can see how this works in the real world. Imagine a stock trading at $100. A trader would buy two $70 calls and sell one $100 call. That is the ZEBRA. Now here is what that structure creates.

- Buy 2 × $70 calls @ $34 = $68

- Sell 1 × $100 call @ $7 = $7 credit

- Net debit = $61

The $70 calls have $30 of intrinsic value with the stock trading at $100. Which means that they have $4 of extrinsic value or time value in their premium.

The $100 call on the other hand is trading at $7 and it by definition is 100% time value.

Structurally speaking since the trader paid $8 in time value on the $70 calls, and then collected $7 dollars in time value for the 100 call, they only have $1 of time value exposure on this trade. Meaning that if the market just sits at the current price, and all-time value disappears as we get closer to expiration date, the worst outcome from a time value perspective is that a trader will lose $1 of time value.

This concept and idea is at the core of the ZEBRA trade. A trader short at the money call option offsets the time decay affiliated with the 2 long deep in the money call options.

A trader’s position ends up with roughly the same exposure as owning 100 shares of stock. In options terms, that means a trader is sitting around a +100 delta. If the stock goes up, their position should move with the stock one for one.

But here is where it gets interesting. From a risk perspective, the structure is equally deliberate. The maximum loss is defined upfront, limited to the initial debit paid to establish the position. While this introduces higher capital commitment than a single call option, it remains significantly lower than purchasing shares outright, offering a middle ground between leverage and capital efficiency.

They’re not paying $10,000 to control those 100 shares. They’re using options to get similar exposure with less capital. That is a big deal, especially for smaller accounts. If a stock is trading at $100 and a trader buys 100 shares their capital requirement is $10,000. With the ZEBRA on this example the capital requirement is the net debit of the trade which in this instance is $6,100. That is 39% less than that of owning the stock outright.

At the same time, they’re not dealing with the same level of time decay that hurts most option buyers. The deep in the money calls hold real value, and the option a trader sold helps offset decay. So, the trader gets stock-like movement without the constant drag.

That is the goal of the ZEBRA. Keep the upside behavior of stock, lower the cost to participate, and reduce the time decay that usually works against a trader.

I have laid it all out in the table below which shows the value of the ZEBRA at expiration at multiple price levels, while also illustrating the net P/L for each leg of the trade.

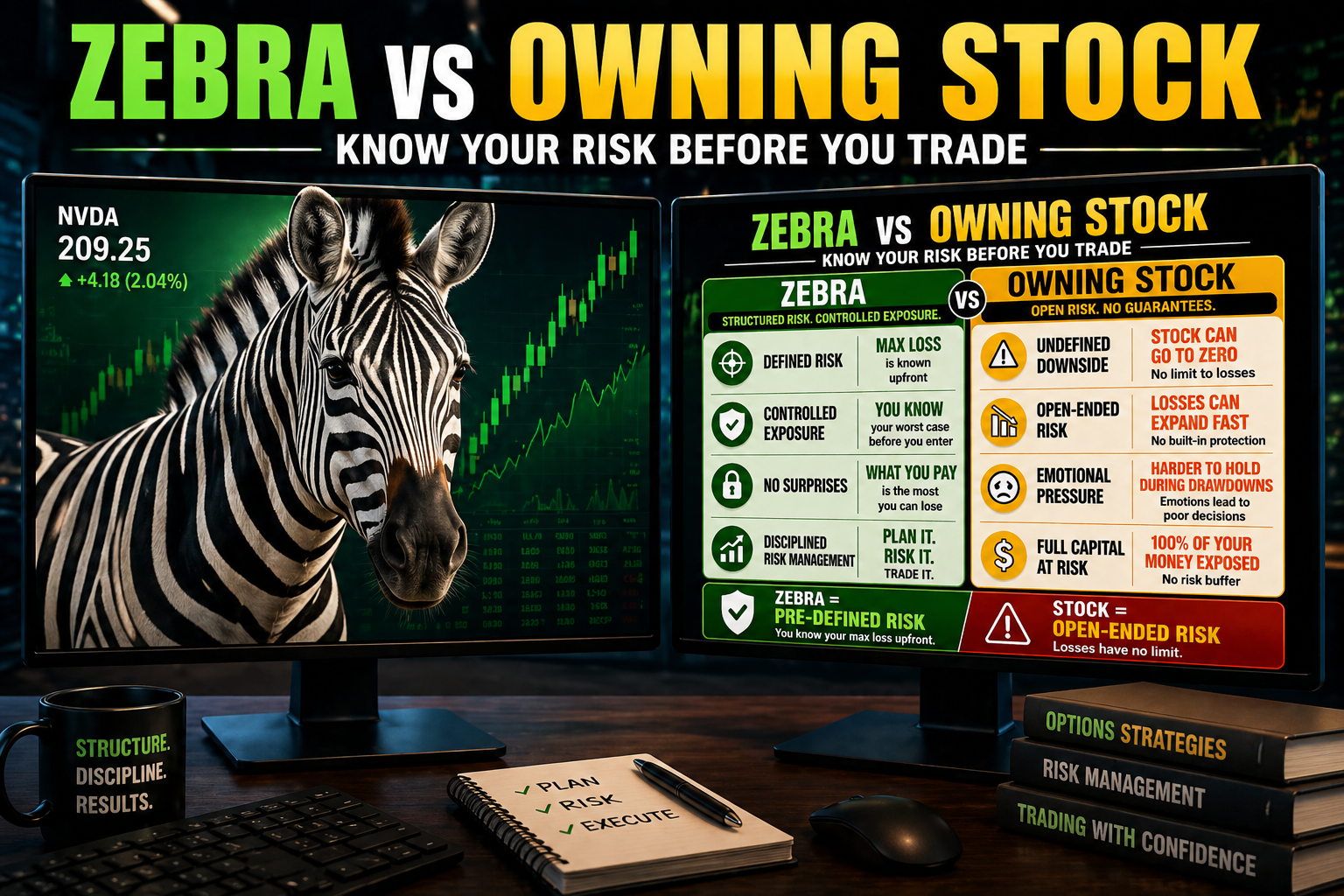

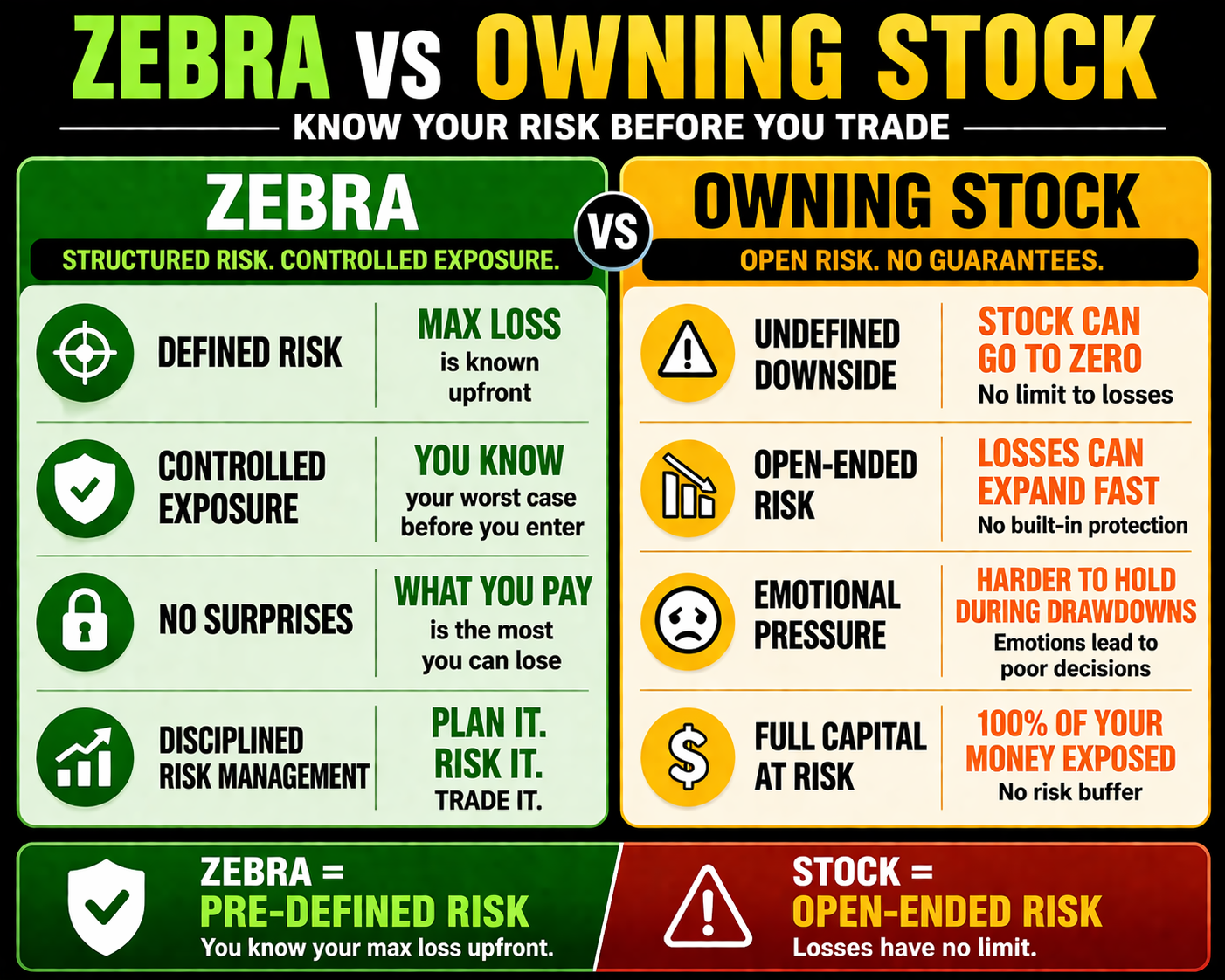

Every great trade begins with a clear understanding of risk. The ZEBRA strategy has one distinct advantage in this regard. A trader’s risk is defined at the outset. It is the total amount a trader pays to enter the trade. No surprises. No hidden exposure. That number represents their worst-case scenario.

What determines that risk is equally straightforward. It is shaped by the price of the deep in-the-money options a trader purchases, the premium a trader collects from the option a trader sells, and the time remaining until expiration. These three elements work together to define the cost basis and, therefore, the exposure.

However, it would be a mistake to assume that defined risk means no risk. It does not. The ZEBRA structure reduces certain disadvantages, but it does not eliminate uncertainty. A trader remains exposed to the direction of the underlying stock. A trader carries assignment risk from the short option. And in less active markets, liquidity can become a factor.

The intelligent trader does not ignore these realities. They acknowledge them. Because in the end, the truth is disarmingly simple. If the stock moves against a trader, they will lose money. The structure may be refined, but the market’s verdict remains final.

he Zebra is not for gamblers.

It is for traders who want stock-like exposure, defined risk, and a structure that works with them instead of against them.

Used correctly, it can be powerful.

Used carelessly, it will teach a trader a lesson they will not forget.

At its core, every trade comes down to one question. Where does a trader need to be right? In the case of a ZEBRA, that answer is found in the breakeven point. It is the line between a good idea and a profitable one.

Consider our simple example. If a trader builds a ZEBRA using the $70 calls and a trader’s net cost is $61, breakeven sits at $101. The math is clean. Above that level, the position works in a trader’s favor. Below it, the structure begins to lose ground.

What makes this particularly important is how often traders overlook it. They focus on direction. They focus on conviction. But markets do not reward opinions. They reward precision. The breakeven tells a trader exactly how much room a trader has and how much margin for error exists in the trade.

In that sense, breakeven is not just a number. It is a discipline. It forces the trader to define expectations clearly and measure outcomes objectively. And in a structure like the ZEBRA, where capital efficiency and reduced decay are central, that clarity becomes a critical edge.

Let’s be clear about what a trader is trying to accomplish. A trader is stepping into a position that is designed to move with the stock. When the stock rises, a trader’s position rises. That is the objective. And in a ZEBRA structure, that objective remains firmly intact.

The upside here is substantial. Like owning shares outright, a trader’s profit potential is, in theory, unlimited. As the stock climbs, a trader’s position participates in that move. A trader is not boxed into a narrow range. They’re aligned with the trend.

But understand this. A trader is not capturing every dollar of that move. The short option a trader sold acts as a counterbalance. It helps reduce time decay and lowers a trader’s cost. In return, it slightly tempers the upside. That is the trade-off.

And it is a rational one. The trader is exchanging a portion of theoretical profit for a more durable position. Less decay. More staying power. Greater efficiency of capital. These are the characteristics that define professional trading.

So, the question is not whether a trader can make money. The question is how a trader wants to make it. With full exposure and full cost, or with a structure that gives a trader leverage, control, and a disciplined approach to risk and reward.

Most traders think the only way to control a stock is to buy it outright. If a stock is $100, a trader needs $10,000 to own 100 shares. That ties up a lot of capital. A ZEBRA gives a trader another way. It lets a trader control the same 100 shares, but with much less money upfront.

Here’s the difference. When a trader owns stock, a trader pays the full price and take on all the risk. If the stock drops, a trader’s losses grow with it. With a ZEBRA, a trader’s risk is defined from the start. A trader knows exactly how much a trader can lose, and it is usually far less than buying the stock. At the same time, a trader’s position still moves very similarly to the stock when it goes up.

The big idea is capital efficiency. With a ZEBRA, a trader keeps more cash available instead of tying it all up in one trade. That gives a trader flexibility. A trader can take more opportunities, manage risk better, and stay in control. So instead of paying full price for exposure, they’re using a smarter structure to get similar results with less capital at risk.

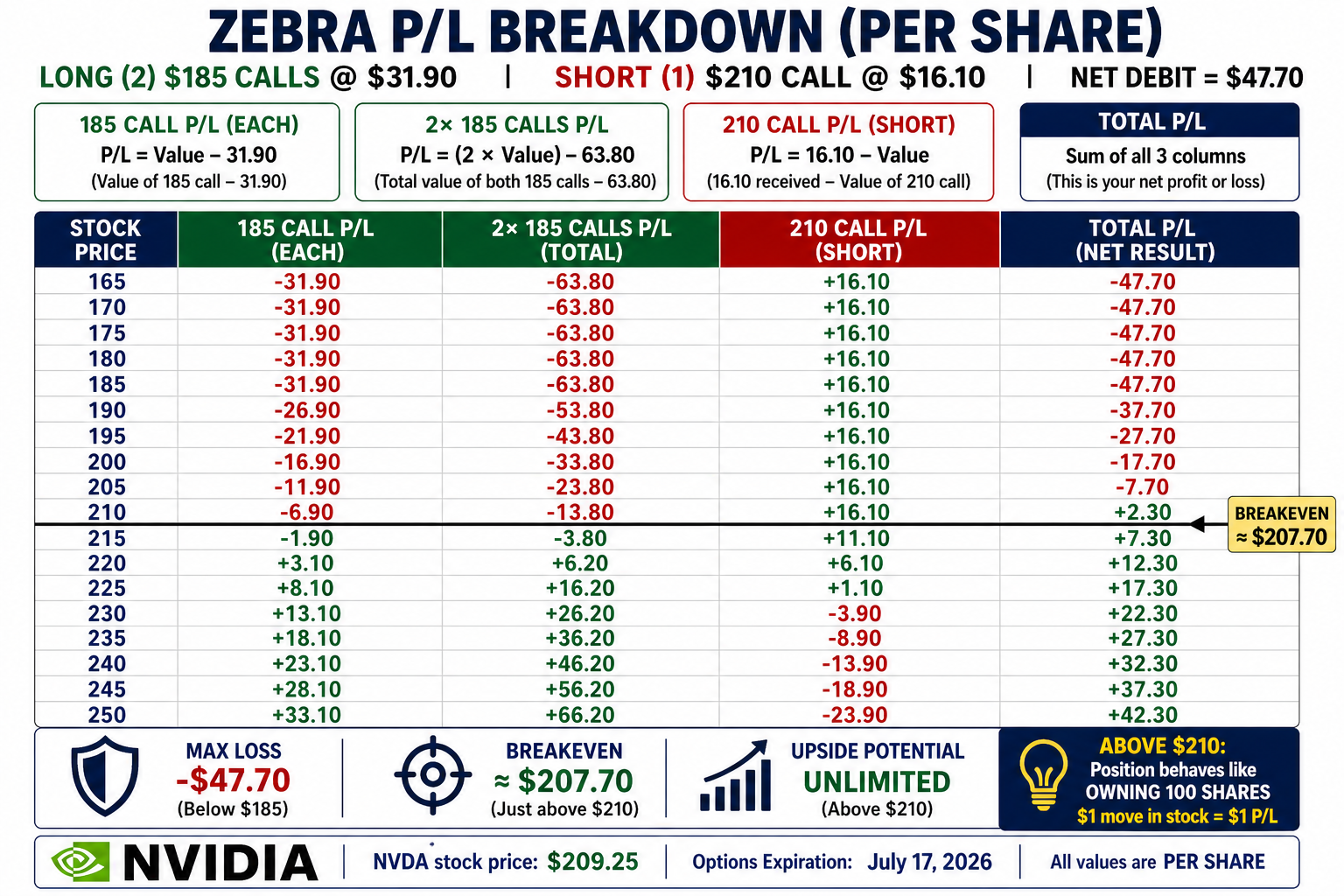

ZEBRAs have real world implications that allow options traders to effectively slay time decay and use capital more efficiently. Here is a real-world example involving $Nvidia ($NVDA) stock.

NVDA stock is currently trading at $209.25

If we look out to the July 17, 2026 options expirations we can construct a ZEBRA as follows:

Buy 2 July 17 $185 $NVDA calls @ $31.90 each.

Sell 1 July 17 $210 $NVDA call @ $16.10

At first glance, the structure appears complex. Buy two $185 calls at $31.90 and sell one $210 call at $16.10, for a net debit of $47.70. But the intent is more straightforward than it looks. The trader is using options to replicate the behavior of owning stock, while committing far less capital upfront. Instead of paying over $20,900 to buy 100 shares of NVDA, the position controls similar exposure for only $4,770, a fraction of that amount, with risk defined from the outset.

The mechanics become clearer when a trader looks at how the trade behaves across price levels. Below $185, the position reaches its maximum loss, capped at the initial $47.70 paid. As the stock rises toward $210, the long calls begin to recover from that cost. Once the stock moves above $210, the short call activates, and the position transitions. From that point forward, it behaves much like owning 100 shares of NVDA, with gains increasing roughly dollar for dollar as the stock climbs.

What makes the trade compelling is not just the upside, but the structure. The breakeven sits just below the current stock price, around $208, meaning the trader does not need a dramatic move to begin profiting. At the same time, the downside is fixed and known in advance. For newer traders, that combination; defined risk, stock-like participation, and capital efficiency, captures the essence of why strategies like the ZEBRA exist in the first place.

What stands out in this trade, and what many newer traders miss, is that the structure is not just about leverage or defined risk. It is about how the premium is constructed. In this case, the trader has collected more extrinsic value from the short $210 call than was paid across the two long $185 calls. That is a subtle but important distinction. It means the position is not fighting time decay in the traditional sense. In fact, it has a slight structural advantage from the outset.

That advantage shows up in the breakeven. With NVDA trading around $209.25, the position does not need the stock to rise to make money. It can tolerate a modest pullback. The breakeven sits near $207.70, which is below the current price. Compare that to owning the shares outright, where a trader’s breakeven is exactly where they bought the stock. Here, the options structure effectively lowers that entry point, giving the trader a small cushion.

The implication is not that the trade is risk-free, but that it is more efficient. The trader has created a position that behaves like owning stock above $210, while also benefiting from a slight edge in premium pricing. It is a reminder that in options, returns are not driven solely by direction. They are shaped by structure. And in this case, the structure allows the trader to be slightly wrong on direction and still come out ahead.

The P/L table below shows how the trade behaves across different prices.

Here’s what most traders never fully grasp. It is not just the strategy that determines the outcome. It is the quality of a trader’s decisions before they ever place the trade. The ZEBRA structure gives a trader powerful advantages. It improves capital efficiency. It allows a trader to control meaningful exposure with less money. It defines risk from the start. But even the best structure can fail if it is applied at the wrong time, in the wrong market, or against the wrong trend.

This is where trading with VantagePoint artificial intelligence changes the game. Because now, instead of guessing, a trader can lean on a system designed to analyze relationships across markets, identify emerging trends, and forecast direction before it becomes obvious. The real power is not just in finding a trade like a ZEBRA. It is in knowing when the probabilities are aligned in your favor. That is what separates disciplined traders from everyone else.

Think about what you are after. You want leverage but controlled. You want capital efficiency, but without reckless exposure. You want risk management, but without missing opportunity. And above all, you want clarity. Because better decisions lead to better trades, and better trades lead to better outcomes. When you combine a structure like ZEBRA with intelligent market forecasting, you are no longer reacting. You are positioning.

That is precisely the objective behind VantagePoint AI. Its purpose is simple, but profound. To keep you, the trader, on the right side of the right trend at the right time. It removes the noise. It filters the distractions. And it gives you a forward-looking view of where strength is building and where risk is increasing, so you can act with confidence instead of hesitation.

If you want to see how this works in real time, you are invited to attend a free live online trading masterclass. You will learn how traders are using VantagePoint AI to identify high-probability opportunities, align with momentum, and apply strategies like the ZEBRA with greater precision. Save your seat and experience what it means to trade with a structured edge and a smarter decision-making process.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.