Most traders come to the market with a quiet, unspoken assumption: prices rise. Not always, not in a straight line, but over time the tide lifts. It is a comforting belief. It is also an expensive one when the tide turns.

Because when the market stops cooperating, something curious happens. Confidence does not fade gradually. It vanishes all at once. Conviction turns into hesitation. Decisions become second-guesses. And the same trader who once bought every dip with enthusiasm may now find himself paralyzed, watching losses accumulate with disciplined consistency.

The problem is not a lack of intelligence. It is not a lack of effort. It is far simpler, and far more dangerous. The strategies that performed beautifully in a rising market begin to fail without warning. Buying the dip becomes buying weakness. Patience becomes stubbornness. What once felt like opportunity begins to feel like punishment.

This is the moment where most traders draw the wrong conclusion. They blame the market. They call it irrational. Unfair. Unpredictable.

But the market is doing exactly what it has always done. It is changing character. And here is the truth that separates professionals from everyone else: downtrends are not the problem. Using the wrong strategy and the wrong tools in the wrong environment is the problem. There is no such thing as a bad market. Only a mismatched approach.

We just finished the first quarter for 2026. What I often find very helpful to genuinely understand what “IS” occuring in the markets is that I study the “scoreboard” to see how everything performed.

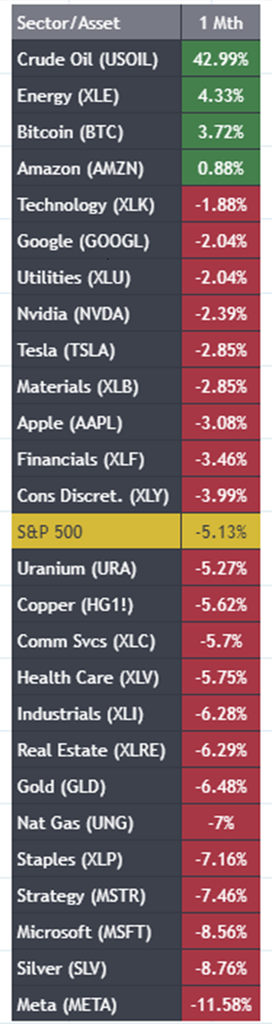

Here is the 1-month scoreboard.

This is screaming one message to anyone willing to listen. There are 27 key assets here, including the 11 stock market sectors and the S&P 500 Index, and only 4 assets finished the month higher. That means a staggering 85% of key assets trended lower, confirming broad-based weakness across the market. This is not selective selling. It is systemic pressure.

Leadership is extremely narrow and almost entirely concentrated in Energy.

Start with the outlier. Crude Oil ($USOIL) up +42.99% in one month is not a trend. That is a shockwave. It signals a supply disruption or geopolitical premium being aggressively repriced. When the underlying commodity moves like that, it pulls capital into the entire complex. That is exactly what you see with Energy ($XLE) still positive while nearly everything else is red. This is classic capital rotation into “real assets” when uncertainty rises and confidence in growth weakens.

Now look at the broader tape. The S&P 500 down -5.13% tells you the average stock is struggling. But the real insight is beneath the surface. Growth leadership is breaking. Technology ($XLK), $NVDA, $AAPL, $MSFT, $TSLA, and $META are all negative. That is not random. That is institutional money reducing exposure to duration sensitive assets. When leaders fall, passive flows weaken, and downside pressure accelerates. This is a regime shift.

What makes this even more important is what is not working. Defensive sectors like Utilities ($XLU) and Staples ($XLP) are also down. Safe havens like Gold ($GLD) and Silver ($SLV) are falling. Even Bonds by proxy through rate sensitivity are not providing relief. That tells you this is not a clean risk-off environment. It is a liquidity and repricing event. When both risk assets and traditional hedges decline together, it usually means forced selling is somewhere in the system.

Then you have Bitcoin ($BTC) quietly positive. That matters. It suggests there is still speculative appetite, but it is becoming more selective. Capital is not leaving the market entirely. It is concentrating into specific narratives. Energy and selective alternatives are absorbing flows while broad equities bleed.

Final takeaway. This is a market where market selection is everything. If you are long the wrong sector, you are fighting the tape. If you are short weak sectors, you are aligned with it. And if you are trying to treat this like a balanced bull market, the scoreboard is already telling you the outcome.

Now let’s zoom out to the 3-month scorecard:

Out of the entire group, only 10 markets are up while 17 are down, meaning roughly 63% of assets are trending lower over this three-month period. That kind of imbalance tells us this is a market where weakness is the dominant force.

When nearly two-thirds of assets are moving lower together, it reflects broad risk-off behavior and sustained selling pressure across the system. This is a coordinated shift in capital away from risk and into a much narrower set of opportunities. This is a full-blown regime shift.

Over three months, the scoreboard confirms what the one-month view hinted at. Capital is not rotating randomly. It is systematically abandoning growth and piling into hard assets and defensive cash flow sectors.

Start at the top. Crude Oil ($USOIL) up +75.63% is extraordinary. That is not a trade. That is a macro event. It is pulling everything with it. Energy ($XLE) up +31.16%, Uranium ($URA) +15.18%, and Materials ($XLB) +10.37% all confirm the same thing. This is a coordinated move into the “real economy.” When you see Energy, Materials, and Utilities ($XLU) all outperforming together, you are looking at inflation pressure, supply constraints, or geopolitical stress driving capital into tangible assets.

Now contrast that with what is happening elsewhere. The S&P 500 down -5.46% is just the headline. The real damage is underneath. Technology ($XLK) down -7.19%, $NVDA, $AAPL, $MSFT, $TSLA, and $META all deeply negative. That is a liquidation of leadership. When the generals fall, the army does not hold the line. This is not sector rotation within equities. This is capital exiting duration-sensitive growth entirely.

And here is where it gets even more telling. Bitcoin ($BTC) down -22.82% and $MSTR down -21.1%. That is speculative excess being unwound. When both high-growth equities and crypto are declining together, it signals tightening liquidity conditions. The market is no longer rewarding future narratives. It is demanding present cash flow and real assets.

Even more important is the positioning of defensives. Staples ($XLP), Utilities ($XLU), and Gold ($GLD) are positive. That is classic late-cycle behavior. But this is not a gentle rotation. It is aggressive. Meanwhile, Financials ($XLF) down -10.49% is a warning sign. Financials typically reflect the health of the system. Weakness there suggests stress beneath the surface, whether from credit, rates, or liquidity.

Final takeaway.

This is a market dividing into two worlds:

- World 1: Hard assets, energy, and defensive yield

- World 2: Growth, speculation, and long-duration assets under pressure

There is no middle ground right now.

If you are aligned with Energy, Materials, and select defensives, you’re trading with the trend. If you are holding Tech, Crypto, or high-beta growth, you’ve been fighting a macro tide.

There is a tendency, especially among less experienced traders, to treat the market as a single, continuous environment. It is not. It is a rotating system, shifting between distinct regimes that demand entirely different behavior. Broadly speaking, there are three: the uptrend, where capital is rewarded for participation; the downtrend, where capital is rewarded for selectivity and timing; and the sideways market, where capital is quietly eroded by noise and false signals.

The transition between these regimes is rarely announced. There is no headline that declares the rules have changed. Instead, the evidence emerges in the structure of price itself. In a downtrend, the pattern becomes unmistakable for those willing to see it: lower highs, where rallies fail to reach prior peaks, and lower lows, where selling pressure pushes prices beneath previous support. It is not simply that prices are falling. It is that the market is systematically rejecting strength.

This is where the real shift occurs. Selling pressure begins to dominate the landscape, not as a momentary event but as a persistent force. Rallies, which once offered continuation, now serve a different function. They become exits. They become traps. Brief, convincing advances that lure in buyers before the trend reasserts itself with greater force.

And this is the inflection point where many traders falter. They continue to apply the logic of a rising market to a falling one. They buy weakness expecting recovery. They wait for confirmation that never comes. What worked before does not merely underperform. It actively produces losses.

The uncomfortable reality is that markets do not reward consistency of belief. They reward consistency of adaptation. Because while bull markets reward patience, bear markets reward precision.

If you listen to enough financial television, you might come away with the impression that markets fall because of “concerns.” Concerns about inflation. Concerns about geopolitics. Concerns about whether the Federal Reserve chair had oatmeal or eggs. This is comforting. It suggests a tidy, narrative-driven world. It is also mostly nonsense.

Markets don’t fall because people are concerned. Markets fall because money disappears. Or more precisely, because liquidity packs its bags, leaves town, and doesn’t leave a forwarding address.

Liquidity is the party punch bowl. When it’s full, everyone is a genius. Prices rise, risks are ignored, and even questionable ideas find eager buyers. But when that punch bowl gets pulled away, the room changes quickly. Buyers become scarce. Sellers become urgent. And urgency, in markets, is where things start to break.

Enter the margin call. The only signal in finance that doesn’t care about your opinion, your thesis, or your feelings about where things “should” be going. A margin call is not a suggestion. It is a demand. “Sell something. Now.” Preferably your most liquid assets, because those are the only ones someone can get rid of in a hurry.

This is where the professionals quietly reposition while everyone else loudly rationalizes. Institutions don’t wait around for confirmation. They reduce exposure, raise cash, and move capital where the damage is less severe. It is less dramatic than panic, but far more effective.

Now comes the fun part. Down moves are not polite. They do not unfold at a gentleman’s pace. Markets tend to go up the escalator and down the elevator, with occasional stops only to let more people panic. What took months to build can unravel in days, sometimes hours.

And once the process begins, it feeds on itself. Selling leads to more selling. Prices drop, which triggers more margin calls, which forces more selling, which pushes prices lower still. Assets that once behaved independently begin to move together, as if they’ve joined a synchronized swimming team nobody asked for. Correlations rise. Diversification quietly exits stage left.

By this point, the narrative has usually caught up. Headlines explain what just happened, with great confidence and perfect hindsight. But the real story was mechanical from the start.

Because downtrends are not random events. They are systems in motion. Cold, efficient, and entirely indifferent to anyone who thought this time would be different.

When the market is falling, your job is not to argue with it. Your job is to align with it.

Most traders make the same mistake right here. They see a stock drop and think it’s “cheap.” They assume value. They assume a bounce. They assume wrong.

In a downtrend, weakness is information.

The cleanest trades come from stocks that are already breaking down. Names that have lost support. Names that can’t rally. Names that look heavy every time they try to move higher.

Traders have a few choices.

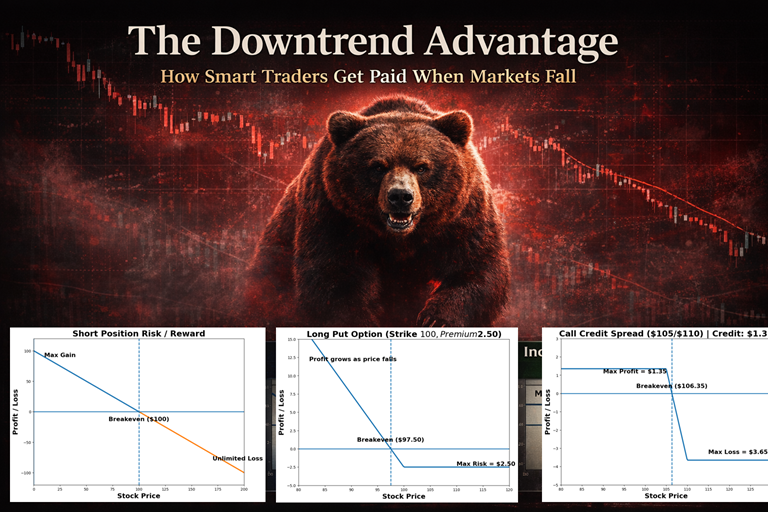

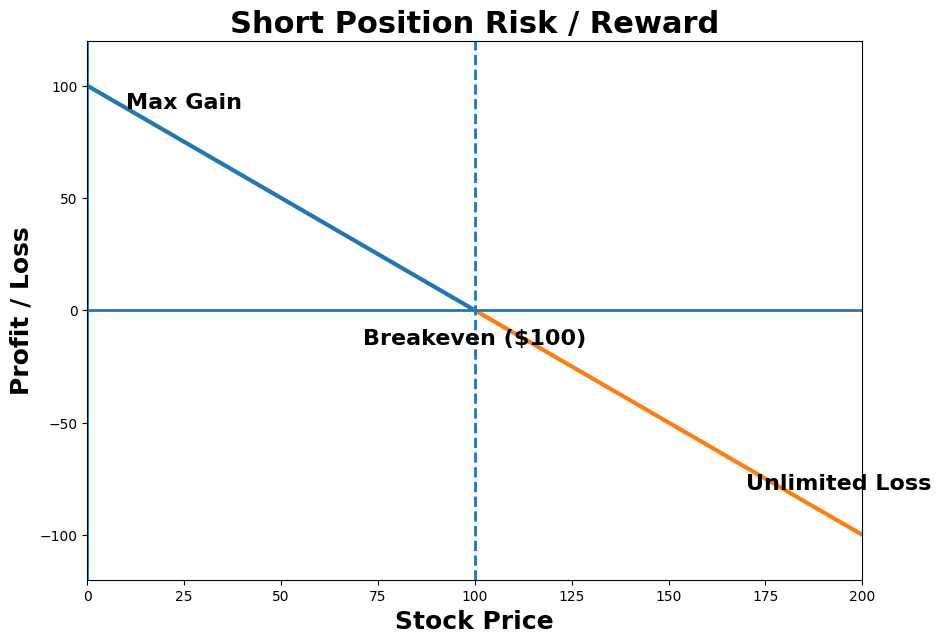

First, short selling. Targeting stocks that are clearly under pressure and breaking key levels. Not guessing. Not anticipating. Waiting for confirmation, then acting. Short selling is not complicated. This is how it works.

Most beginners are taught one idea: buy low, sell high. That makes intuitive sense. Buy something cheap, wait for it to rise, and then sell it for a profit. Simple.

But the market has a second gear most people don’t realize exists: traders can flip the entire process and profit when prices fall. Instead of buying first, the trader sells first at a higher price, then buys later at a lower price. This is called short selling.

Here’s the deal. Imagine a buyer, cash in hand, ready to pay $50,000 for a Mercedes SLC. You shake on it… but you don’t own the car. Not yet. So now the clock is ticking. If you can go out into the market and find that exact car for $45,000, you deliver it, pocket the $5,000 difference, and walk away smiling. But if the only one you can find is priced at $55,000, you still have to deliver… and that extra $5,000 comes straight out of your pocket. You sold first, then had to go buy later. That’s the entire game.

Now take that same idea and drop it into the stock market. Instead of cars, you’re dealing with shares. Your broker lends you stock, you sell it at today’s price, say $100, and now you owe those shares back. If the stock falls to $80, you buy it back cheaper, return the shares, and keep the $20 difference. But if the stock climbs to $120, you still have to buy it back, and that loss is yours to eat. You flipped the normal script. You sold high first, hoping to buy lower later.

And here’s the part most beginners miss. Your upside is capped, because the best-case scenario is the stock goes to zero. But your downside is wide open, because a stock can keep rising far beyond where you sold it. That’s why short selling isn’t about being clever… it’s about being disciplined. You are borrowing both the asset and the time. And if the market moves against you, it will collect its payment whether you’re ready or not.

Second, buying puts. Same idea, different vehicle. A trader positions for continued downside in stocks that are already trending lower. Not hoping for a collapse. Just following the path that’s already in motion.

The focus is momentum.

Not trying to call the bottom. Not trying to be early. But instead identifying what is already weak and staying on that side of the trade.

Because here’s the reality most traders learn the hard way:

Weak stocks don’t stabilize.

Weak stocks get weaker.

At its core, a put option is not a prediction. It is a contract. It gives a trader the right, but not the obligation, to sell a stock at a fixed price within a defined period of time. So, if a stock is trading at $100, and they buy a one month at the money put for $2.50, what they are really purchasing is the ability to sell that stock at $100, no matter how far it may fall over the next 30 days. In a market increasingly defined by uncertainty, that right carries both strategic value and very real cost.

The mechanics are straightforward, but the implications are anything but. If the stock declines to $90, the right to sell at $100 becomes valuable. A trader can either exercise that right or simply sell the option itself at a higher price, capturing the difference. But if the stock remains at $100 or rises above it, that right becomes less meaningful by the day. Time, in this case, is not an ally. It is a decaying asset. Each day that passes without a downward move erodes the value of the position, quietly and predictably.

And this is where the risk profile becomes both elegant and unforgiving. The maximum loss is known from the outset: the $2.50 you paid. It is defined, contained, almost comforting. But the probability of losing that premium is not trivial. For the trade to work, the stock must move lower with enough speed and magnitude to overcome both the cost of the option and the passage of time. In other words, this is not just betting on direction. It’s betting on timing and velocity. And in today’s market, that distinction is often the difference between a controlled loss and a realized opportunity.

Now let’s talk about a different type of trader.

Not the one chasing momentum. The one playing probabilities.

This trader doesn’t need a dramatic move. In fact, they prefer the opposite. They want the market to struggle. To stall. To try and fail.

This is where call credit spreads and bear call spreads come into play.

Selling a call credit spread in a falling market is a bit like setting up a toll booth on a road no one wants to drive on. The stock is sitting at $100, looking a little tired, maybe even hungover from its last rally, and then selling the $105 call while buying the $110 call for protection, collecting a tidy $1.35 for the trouble. It’s really a wager that this stock is not only unlikely to go up, but especially unlikely to climb past $105 before the arrangement expires. It is, in essence, betting on inertia… and collecting rent while waiting.

Now, the beauty of this trade is that time is finally working for a trader, which in markets is about as rare as a politician refusing a microphone. If the stock drifts sideways or, better yet, continues its descent, those call options sold start to wither like lettuce in the Florida sun. As long as the stock stays below $105, the trader keeps the full $1.35.

Of course, this is not a free lunch, despite Wall Street’s best efforts to market it as one. The risk is defined, but very real. The spread between $105 and $110 is $5, and after collecting $1.35, the maximum loss is $3.65 if the stock stages an inconvenient resurrection and blasts through $110. So, what you have here is a trade that wins small and often, and loses bigger if ignored. In other words, it rewards discipline and punishes optimism… which is pretty much the market’s favorite pastime.

It’s positioning above the market, selling premium into strength, and letting time do the heavy lifting. The ideal scenario is simple. Price goes nowhere. Or drifts lower. Or rallies a little and then rolls over.

A trader wins as long as the market fails to do one thing. Sustain a move higher.

That’s the edge.

In a downtrend, rallies are often short-lived. They look convincing for a moment, pull in buyers, and then fade. That repeated failure creates opportunity. It’s selling into those rallies. Not aggressively. Not emotionally. Systematically.

And while directional traders are dealing with volatility and timing, you’re letting time decay work in your favor every single day the market doesn’t cooperate with the bulls.

This is a quieter way to succeed. Less dramatic. More consistent when executed properly.

Because the goal here isn’t to be right about direction. The goal is to be right about behavior.

And in a falling market, one behavior shows up again and again. The market tries to go up. And fails.

There is an important structural distinction between short selling and options-based strategies that often gets overlooked in the pursuit of directional conviction. When a trader sells a stock short, they are effectively taking on open-ended risk. In theory, a stock can rise indefinitely, which means the potential loss has no defined ceiling. By contrast, options introduce a level of precision. Whether you are buying puts or structuring a spread, the risk can be quantified at the outset. You know, before the trade is placed, exactly what is at stake. That clarity changes not only the math of the trade, but the psychology behind it.

Within that framework, selling call credit spreads offers a particularly pragmatic approach. The trade does not require a dramatic move lower. It simply requires that the market fail to sustain a move higher. Time decay becomes the quiet ally, working in the background each day the position remains intact. The trade-off is clear. Profit potential is limited, but so is risk, and outcomes tend to be more consistent. For many traders, that consistency translates into something equally valuable. The ability to hold the position without the constant pressure that comes with undefined risk.

Over the past three months, the bears have had the advantage. That is not dramatic. It is simply what the data shows. When you study the scoreboard, the message is clear. The majority of sectors and key assets have moved lower. This is not isolated weakness. It is broad-based pressure across the market.

It does not mean it is the end of the world. Markets move in cycles. Strength rotates. Weakness rotates. But there is one question that does not change. Where is money being made? Right now, money is being made by understanding the direction of the trend and positioning accordingly.

If a market is falling persistently, you have to look at bearish strategies. And in this type of environment, that perspective has paid off. Traders who adapted to the downside, who respected the trend, and who focused on where the pressure was building have had the edge.

Before you think about strategy, before you think about entries, before you even think about risk… you need to answer one question:

Where is the money going?

Because not all markets are worth your time.

This is where most traders get it wrong. They jump straight into setups. They search for patterns. They look for signals. But they ignore the most important variable sitting right in front of them.

Relative strength.

If a sector is weak, you don’t fight it. You lean into it. That’s your hunting ground for shorts and puts. If a sector is strong, you don’t short it just because the broader market is struggling. That’s how traders get run over.

Right now, you’ve already done the work. You’ve seen the one-month trend. You’ve confirmed it over three months. You’ve identified rotation.

So use it.

Focus on the weakest sectors. The names that can’t rally. The ones breaking support and staying there. That’s where the clean trades live. Learn how to take advantage of falling prices.

And just as important, know what to avoid. Use VantagePoint.

Because at the end of the day, you’re not just trading stocks.

You’re trading strength and weakness.

Once market selection is clear, the next decision becomes more precise. Not what to trade, but how to express that view.

This is where many traders create unnecessary friction. They recognize weakness but apply the wrong tool to exploit it. The result is not just underperformance. It is avoidable loss.

Different environments demand different strategies.

In a clean downtrend, where price is making lower highs and lower lows, the objective is straightforward. You align with momentum. That typically means short exposure or long puts. You are not anticipating a reversal. You are participating in continuation. The edge comes from clarity of direction.

In a more fragmented environment, where the market rallies but cannot sustain those moves, the opportunity shifts. This is where income strategies become more effective. Selling call credit spreads into resistance allows you to benefit from repeated failure rather than directional conviction. The market does not need to collapse. It simply needs to fail to move higher.

Then there are periods of elevated volatility, where direction becomes less reliable and price action becomes more reactive. In these environments, the priority changes. Position sizes are reduced. Risk is defined more tightly. Hedging becomes a consideration. The goal is no longer to maximize return, but to preserve flexibility.

The common thread across all three is alignment.

The strategy must reflect the environment. Not the other way around.

Because when the tool matches the condition, execution becomes simpler. And when it doesn’t, even a correct idea can produce the wrong result.

Benchmarking against the S&P 500 is supposed to be a compass. It tells you where strength lives and, just as importantly, where it doesn’t. The goal is simple. Avoid buying weakness. Align with outperformance. And in normal markets, that works cleanly. Capital flows into leaders, trends persist, and relative strength often translates into absolute gains. But the graphic tells a different story right now. When the S&P 500 itself is down across multiple time frames, the definition of “outperformance” becomes distorted. Energy stands out as a true leader, but much of the rest of the board is a study in relative decline rather than genuine strength.

That’s where the challenge becomes real for traders. Take Health Care (XLV) as an example. On a relative basis, it is outperforming the broader index year to date. But in absolute terms, it is still negative. You are losing money, just not as much as you would have in the S&P 500. And that’s the uncomfortable truth of bear markets. Outperformance doesn’t always mean profit. It often just means reduced damage. Which forces a different mindset altogether. The objective shifts from chasing returns to managing exposure, from seeking growth to preserving capital, and from asking “what’s going up?” to asking “what’s falling the least… or rising despite the pressure?”

In downtrends, the natural tendency is to protect your capital.

In fact, the traders who last the longest, the ones who are still standing when the dust settles, are the ones who understand that defense is part of the game. Not an afterthought. Not a last resort. A core strategy.

Because in a downtrend, the market is not trying to reward you. It’s trying to take from you.

There is a quieter way to navigate a falling market. Less surgical. More observational. It begins with a simple premise. You don’t need perfect timing to align with a powerful trend. You need to be on the right side of capital flows.

This is where inverse ETFs enter the conversation. They are not elegant instruments, but they are efficient. They allow traders to express a bearish view on an index or sector without the complexity of shorting individual names or structuring options. The trade is straightforward. If the market declines, the position works. No need to identify the weakest stock in the room. You’re trading the room itself.

Alongside this is sector rotation. Not every part of the market declines equally. Even in broad weakness, there are pockets of relative strength. Capital does not disappear. It relocates. It moves out of underperforming sectors and into areas showing resilience or benefiting from the prevailing macro environment. We have seen this repeatedly. Energy rising while the broader market struggles. Defensive sectors holding ground while growth unwinds.

The advantage here is clarity. You are not required to pick the exact top or bottom. You are aligning with direction, not precision. Capturing the bulk of a move rather than optimizing the entry.

And this is where the macro lens becomes essential. Because price alone tells you what is happening. Capital flows tell you why.

They reveal leadership. They expose weakness. And in a downtrend, they make one thing unmistakably clear.

Money is always moving. The only question is whether you are moving with it or against it.

And this is how the emotional cycle plays out.

Because the real signal in a falling market isn’t news. It isn’t opinions. It isn’t forecasts.

It’s the margin call.

That’s when decisions stop being optional. That’s when selling becomes forced. And that’s when trends accelerate in a way that catches most traders completely off guard.

You don’t negotiate with that kind of pressure. You either respect it, or you get run over by it.

That’s the lesson.

Bear markets don’t negotiate.

They enforce discipline.

There is an old illusion in markets that risk is something you can think about after the trade is placed. In rising markets, that illusion can persist for quite some time. In falling markets, it is removed with remarkable efficiency.

Because markets do not decline politely.

They fall with speed. With urgency. What took weeks to build can unravel in a matter of days. Losses, once contained, begin to compound. And the trader who was comfortable just days ago finds himself reacting instead of deciding.

The priority, then, becomes unmistakably clear.

Not profit.

Survival.

Because the trader who preserves capital retains the ability to act. To adapt. To take advantage of the next opportunity when conditions shift once again.

Right now, the market is telling a story most traders don’t want to hear.

Not in words. In behavior. And behavior is always louder.

Look closely and you’ll see it. Not everything is falling equally. In fact, some areas aren’t falling at all. Capital is concentrating. Moving with purpose. Energy pushing higher while broad indexes struggle. Strength in one corner. Weakness almost everywhere else.

At the same time, something else is happening. The old rules are starting to crack. Assets that were supposed to act as safe havens are no longer behaving that way. When fear enters the system, they should rise. They’re not. Or not enough to matter.

That’s a signal. Because when what should happen… doesn’t happen… something bigger is shifting underneath the surface.

Now layer in volatility.

Not the kind you measure neatly on a chart. The kind you feel. Fast moves. Failed rallies. Sudden reversals. Markets that look stable in the morning and uncertain by the close.

This is not a calm environment. It’s a transitional one.

And this is where most traders get trapped. They trade expectations. They trade narratives. They trade what they think should happen based on how things used to work. But the market is under no obligation to behave the way it did yesterday. It only reflects what is happening right now. And right now, capital is rotating. Leadership is narrow. Confidence is uneven. And the gap between expectation and reality is widening.

That gap is where opportunity lives.

If you’re willing to see it.

Because the takeaway is simple. Not easy. But simple.

Follow price. Follow performance. Not narratives.

And here’s the part that stings a little. The edge is being ready for whatever happens next. Because the trader who adapts gets paid. The trader who doesn’t… funds the account of the one who does.

At this point, we can retire a very popular myth. The idea that falling markets are something to endure, survive, or politely avoid until things “get better.”

That’s a lovely sentiment. It’s also a great way to miss the point entirely.

Because downtrends are not a malfunction of the system. They are the system doing exactly what it’s designed to do. Repricing risk. Exposing excess. Separating those who adapt from those who insist on being right.

And for the prepared trader, this is not bad news. It’s inventory.

Opportunity doesn’t disappear in a falling market. It changes shape. It moves faster. It becomes less forgiving. And it quietly shifts into the hands of those willing to play by a new set of rules.

The first rule is simple. Match your strategy to the environment. If the market or sector is falling, stop pretending it’s rising. This is not philosophy. It’s survival with a profit motive.

The second is less glamorous but far more important. Risk management is what keeps you in the game long enough to take advantage of anything. Without it, even the best idea becomes an expensive lesson.

And finally, adaptability. The trait that sounds obvious, feels easy, and proves elusive the moment money is on the line. Markets change. Conditions shift. And the trader who adjusts accordingly tends to keep both their sanity and their capital.

The rest spend a great deal of time explaining why things should have worked.

This market? It’s not forgiving.

The traders who are winning right now aren’t smarter.

They’re just better equipped.

They’ve got one tool doing the heavy lifting.

Not hype. Not magic. Just raw advantage.

Here’s why traders are switching to VantagePoint, fast:

Speed.

The next big setup? VantagePoint AI already predicted it.

No emotions.

VantagePoint AI doesn’t feel one way or another about the trade. It just helps you execute the plan. Every time.

Deeper insight.

VantagePoint is scanning relationships, trends, correlations… stuff you don’t even see.

It never sleeps.

Markets move overnight. Globally. Constantly. VantagePoint AI is watching everything.

And this is the killer… risk control.

Most of your losses? Bad trades you never should’ve taken.

Now listen, it does not guarantee profits.

But it changes the game.

Period.

Because now you’re not guessing anymore.

We’re running a live online trading masterclass.

You’ll see VantagePoint AI trading software in action.

Real markets. Real analysis. Real decisions; what to trade… and what to ignore.

No fluff. No theory. Just the tool… doing its job.

👉 Join the AI Trading Masterclass

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.