Wall Street has done it again, folks — they’ve managed to make optimism look like a financial derivative.

From the very beginning of organized markets, traders and investors have relied on comparisons to understand value. We have always measured one thing against another — price against earnings, price against assets, price against revenue — because numbers alone tell us little. It’s the relationship between numbers that reveals the truth. These valuation ratios became the compass points of investing: the quiet, reliable instruments that helped us judge whether a business was healthy, overextended, or full of unrealized potential.

Consider the Price-to-Book ratio. It tells us how much we are paying over the company’s tangible worth — the real machinery, land, inventory, capital, not just the story. Or Price-to-Sales, the simplest, most honest measure of how expensive each dollar of actual business activity has become. And of course, Price-to-Earnings, the classic gauge of how much we are paying for every dollar of profits a company makes. These measures endured for centuries because they reflect reality. They center the analysis not on opinion, but on proportion. They were trusted not because they were clever, but because they were true.

But now, something has shifted. These ratios are no longer pure reflections of value. They’re being bent and stretched by the silent force of currency debasement. When the measuring stick — the dollar itself — grows weaker, prices swell not because the assets are worth more, but because the currency is worth less. Price inflates. The ratios soar. And the illusion appears: prosperity without productivity, wealth without growth. The danger is subtle but profound, when the yardstick shrinks, everything looks bigger.

This is why we must look with clear eyes. The ratios still matter, they always will. But today, we must interpret them not just as signals of corporate value, but as signals of the currency’s condition itself. In markets like these, the traders who understand that distinction are the ones who keep their footing while others lose theirs.

What we’re looking at right now is one of the greatest magic tricks ever pulled in the financial markets. Stocks are going up… portfolios are swelling… CNBC is smiling like a used-car salesman on commission. And everyone’s feeling proud of themselves, like they suddenly became investment geniuses overnight.

But here’s the punchline: the market isn’t going up because everything is healthy. It’s going up because the yardstick we’re measuring it with is shrinking. The dollars in your pocket are losing value faster than a politician breaks a promise, so of course the numbers on the screen are getting bigger. You could call it prosperity… if you ignore the part where your purchasing power is quietly being mugged behind the convenience store.

This bull market has muscles drawn on with a Sharpie. It looks strong, it poses strong, it flexes strong… but the real economy underneath is limping like it stepped on a rake. The media calls it “growth.” They call it “momentum.” I call it the illusion of wealth created by a currency that’s getting softer than overcooked spaghetti.

Let’s be clear about something: this market isn’t running on innovation, productivity, or sound policy — it’s running on debasement. Trillions of freshly minted dollars have been pumped into the system, and Wall Street’s been mainlining it like rocket fuel. The so-called “bull market” is less a testament to economic strength and more a monument to the greatest monetary experiment in American history.

You can see it everywhere. Corporate debt at record highs. Federal deficits expanding faster than GDP. Liquidity injections that never seem to stop. The dollar’s purchasing power quietly eroding with every press conference from the Federal Reserve. And yet, somehow, the S&P 500 keeps pushing higher, not because earnings justify it, but because the alternative is too ugly to contemplate.

This is what happens when policymakers mistake money printing for prosperity. They’ve turned the market into a hall of mirrors, every reflection brighter than the last, every distortion more dangerous. Traders celebrate new highs while the foundations of real value crumble beneath their feet.

But make no mistake: this isn’t sustainable. You can’t inflate your way to wealth any more than you can drink your way to sobriety. The bull keeps running because the Fed keeps feeding it. And when that feeding stops — when rates normalize, when debt markets demand accountability — this overvalued, overleveraged, overconfident market is going to find out what gravity feels like again.

Nominal gains are up.

Real wealth? Not so much.

And most folks won’t notice until the music stops and the chairs disappear.

Now we get to the part where the clown car really empties out. Let’s talk about the actual valuations, those tidy little ratios that used to mean something before the market started freebasing liquidity. We’ve got Price-to-Sales, Price-to-Book, Price-to-Earnings; all the old guard metrics. The financial equivalent of the sober uncle at Thanksgiving trying to remind everyone that maybe, just maybe, polishing off your fourth bottle of bourbon before dinner is a bad idea.

But right now? Those ratios aren’t just stretched, they’re doing splits on a trampoline. We’re paying record prices for every dollar of revenue, every dollar of book value, every dollar of earnings. And not because the companies suddenly started breathing fire and printing gold. No. It’s because everyone’s lost their mind and decided numbers don’t matter as long as the Fed keeps the party punch flowing.

Wall Street calls this “the new normal.” They pat you on the head and tell you valuation is outdated—like cholesterol warnings or common sense. But here’s the thing: valuations are like gravity. You can jump, you can climb, you can strap yourself to a SpaceX rocket… but eventually, you’re coming back down to earth.

And when valuations snap back to reality, they don’t land gently. They land like a piano dropped from the roof.

From thirty thousand feet, the picture is unmistakable: we’ve crossed into the most expensive stock market in modern history. Compared to the dot-com peak in 2000, the S&P 500 today trades at roughly 80 percent higher on price-to-book, 50 percent higher on price-to-sales, and modestly higher on P/E. Against 2008, the disparity is even starker, valuations are now nearly double what they were before the financial system imploded. By any historical measure, this isn’t optimism, it’s euphoria in a business suit.

The story investors must believe to think everything’s fine is almost theological. They must believe that valuation no longer matters because the economy has evolved beyond the need for arithmetic. They must believe that innovation, A.I., and liquidity will permanently levitate earnings and prevent recessions. They must believe that the cost of money will stay low enough, long enough, to justify infinite multiples. In other words, that capitalism has been upgraded to a version where risk has been debugged and cycles are obsolete.

This is not a market built on cash flows or balance sheets, it’s built on faith. Faith that growth will always outrun debt, that central banks will always provide rescue, and that the laws of economic gravity no longer apply. It’s the same story we told ourselves in 2000 and 2008, only with glossier tech and faster trading algorithms. The names have changed, but the plot hasn’t: a crowd of true believers chasing the next miracle, convinced that this time, the future has already paid for itself.

Philosophically speaking, the narrative you have to believe today is that multiples don’t matter because technology, A.I., and central banks have rewritten the laws of gravity. You must believe that risk has been democratized, profit margins are permanent, and the future has already paid for itself. You must also assume that a dollar printed by the Fed is just as real as one earned by a worker, and that liquidity — not productivity — is the new foundation of value.

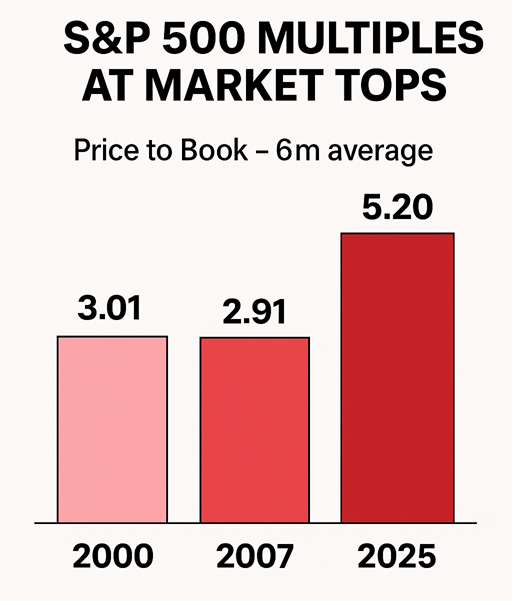

The Price-to-Book ratio was once the gold standard for sanity checks in equity markets — a measure that told investors how much they were paying above a company’s tangible net worth. But in this cycle, that margin of safety has all but disappeared. The market is now valuing companies not on what they own, or even what they earn, but on the belief that central banks will never let the music stop.

During the dot-com bubble, Price-to-Book ratios spiked as investors chased future promise over present value. During the Global Financial Crisis, those ratios collapsed, reminding everyone that assets, not optimism, ultimately anchor prices. Today, the ratio sits even higher than those peaks and for far more precarious reasons. This time, it isn’t just tech euphoria driving valuations; it’s the gravitational pull of easy money and artificially suppressed interest rates.

When the cost of capital is near zero, every dream looks profitable. The result? Investors are bidding up paper wealth while the real economy struggles under the weight of rising costs and slowing productivity. Companies aren’t necessarily more valuable, they’re just being priced in a currency that’s losing credibility.

The irony is striking: the margin of safety that Benjamin Graham built his entire investing philosophy upon has vanished, not because investors stopped caring about risk, but because the system itself taught them not to.

In the price-to-book ratio (P/B), “book” refers to book value, or the net value of a company’s assets minus its liabilities, essentially what shareholders would theoretically receive if the company were liquidated. It’s the accounting value of a business, as recorded on the balance sheet.

The P/B ratio compares how much investors are willing to pay for every dollar of that book value.

Price represents the market’s collective belief about future earnings, innovation, or competitive advantage.

Book represents the cold, hard accounting reality — factories, patents, inventory, cash, minus debt.

The P/B ratio measures how much market value (price) has inflated relative to accounting value (book).

A ratio near 1.0 means investors value the company roughly equal to its tangible worth.

A ratio above 3.0 (like today’s 5.2) means investors are paying five dollars for every dollar of net assets — not for what the company is, but for what they believe it will become.

It’s not a measure of profit. It’s a measure of belief versus balance sheet.

The current environment is one where intangible assets — code, data, brand, and A.I. capacity — dominate. Investors aren’t buying factories or inventories; they’re buying the idea that software and automation will multiply productivity forever.

That belief system drives price far ahead of book because book value can’t capture intangible assets that make up most of the modern economy. The market has become a faith-based enterprise, built on a conviction that the future will be exponentially more valuable than the present.

In short:

“Book value is what accountants see. Price is what dreamers pay.”

We’re living in a period where dreamers have more capital than accountants.

At prior market tops — 2000, 2007, and now — prices surged faster than book value because of the same recurring human pattern:

Excess liquidity – easy money policies flood markets with capital seeking return.

Technological revolutions – internet in 2000, housing finance in 2007, A.I. in 2025.

Narrative dominance – belief that the world has fundamentally changed and old valuation anchors no longer apply.

Book value grows slowly; price can re-rate instantly when enthusiasm peaks. Each time, the story shifts — “dot-com will change everything,” “housing never falls,” “A.I. will automate infinite growth.”

But the structure is the same: price becomes a vote on imagination rather than an assessment of value.

Bottom line:

The P/B ratio today tells us we’ve built a market where faith in the future is priced higher than ownership of the present. It’s not wrong, it’s just fragile. The moment belief wavers; price falls faster than book can adjust.

Okay, now imagine you’re buying a lemonade stand.

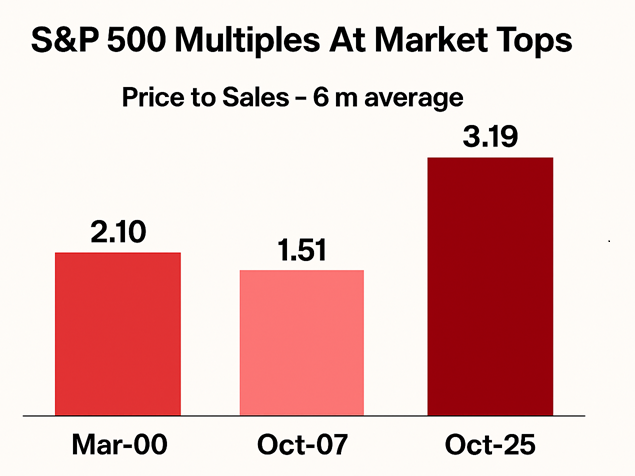

If the stand sells $10,000 of lemonade, and you’re willing to pay $20,000 to own it, that’s a price-to-sales ratio of 2. You’re paying twice what it sells in a year because you think it’ll sell more lemonade later, or you just really believe in it.

Now look at the chart:

* In 2000, people were paying $2.10for every $1 of sales.

* In 2007, they paid only $1.51, a little more reasonable.

* But in 2025, they’re paying $3.19 for every $1 of sales — the highest ever.

That means investors today are more excited, more hopeful, and maybe more overconfident than they were during the dot-com bubble or the housing bubble.

So, what can we conclude?

It’s not that companies are bad, it’s that prices have run far ahead of what businesses actually sell. It’s like paying $3 for a $1 lemonade stand just because you hope it’ll be worth $10 someday.

When everyone in the market starts thinking like that — paying more for less — it usually means people are believing stories more than they’re checking math.

That’s how bubbles form.

Here’s the thing about Price-to-Sales, it’s the cleanest, most unforgiving mirror in finance. It doesn’t care about accounting tricks, stock buybacks, or corporate spin. It just measures how much investors are willing to pay for one dollar of a company’s actual revenue. And right now, that mirror’s showing a clown world reflection.

We’re paying more per dollar of sales than at the peak of the dot-com bubble and the Global Financial Crisis. Think about that. Back then, we had wild optimism about the internet or a housing boom that seemed unstoppable. Today, we’ve got debt, deficits, and debasement — and somehow valuations are even higher.

This isn’t growth. It’s inflation wearing a party hat. The Fed’s cheap money has been feeding asset prices like a goose before Christmas. Companies haven’t gotten dramatically more productive; the dollar’s gotten dramatically weaker. So, when traders brag about “record highs,” what they’re really celebrating is the shrinking value of the money those prices are measured in.

It’s not that the market’s lying to us, it’s that the scale is broken.

Stay with me here — imagine you’re buying that same lemonade stand again.

This time, instead of looking at sales, you look at profits — how much money the stand actually makes after paying for lemons, sugar, and cups.

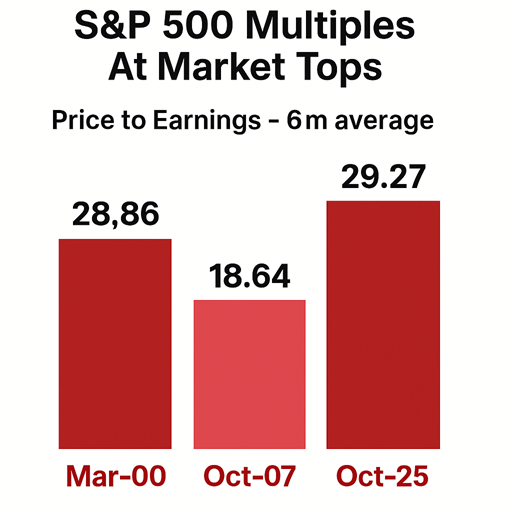

If the stand earns $1000 of profit, and you’re willing to pay $29000 to own it, that’s a price-to-earnings ratio (P/E) of 29. It tells you how many years of profits it would take to earn back what you paid if everything stayed the same.

Now, here’s what the chart shows:

In 2000, during the dot-com boom, people paid $28.86 for every $1 of earnings.

In 2007, right before the financial crisis, that dropped to $18.64 — investors were more cautious.

In 2025, people are paying $29.27 for every $1 of profit, which is even higher than 2000.

What does that mean?

Today’s investors are acting like profits don’t have to catch up, they’re buying stocks for what they hope companies will earn in the future. They’re saying, “I’ll pay $29 now because I believe this stand will make a lot more lemonade later.”

In the past, when people got this excited — 2000 and 2007 — it didn’t end well. Prices ran ahead of reality, and eventually, reality caught up.

In simple terms:

Right now, the market is very expensive again. People are paying record prices for each dollar of earnings, just like the last two times before big corrections. It’s a sign that belief and excitement are driving prices more than profits are.

And the good old Price-to-Earnings ratio — that polite little number Wall Street waves around to convince us everything’s fine. “Relax,” they say, “the P/E is only 30… or 40… or somewhere between fantasy and hallucination.” Once upon a time, this ratio meant something. It told you how much optimism was baked into a company’s future. Now it’s more like a funhouse mirror reflecting the Federal Reserve’s balance sheet.

We’re in the golden age of earnings illusion. Companies aren’t growing profits so much as they’re engineering them through buybacks, cost-cutting, and enough accounting adjustments to make Houdini blush. Earnings season used to be about measuring business performance; now it’s a quarterly séance to summon the ghost of free cash flow.

Meanwhile, the Fed keeps pumping liquidity like a frat boy guarding the keg, and everyone pretends that rising prices mean rising prosperity. The higher the market climbs, the less anyone asks what’s holding it up. Spoiler: it’s debt. Mountains of it. And the only thing thicker than the optimism on CNBC is the denial that someday, interest rates will wake up and ask to be paid.

So yes, the market looks great, if you squint hard enough and ignore reality. But behind those record multiples, the P/E is quietly whispering a different story: growth isn’t what it used to be, and the money measuring it isn’t either.

Now let’s talk about the gas in this bull’s tank — and no, it’s not innovation, productivity, or “economic resilience” like the talking heads love to chirp about. It’s debasement. Pure, unfiltered monetary dilution. The Federal Reserve has been printing dollars like a toddler cranking out finger paintings — sloppy, enthusiastic, and completely unaware of the mess being made.

When you pump trillions of fresh dollars into the system, everything priced in dollars goes up. Stocks go up. Houses go up. Even NFTs of cartoon pigeons go up. Not because they’ve become inherently more valuable, but because the money used to buy them has become inherently less valuable. It’s like measuring your height with a ruler that keeps shrinking. Presto, you’re a giant!

Here’s the dirty little secret Wall Street hopes you never notice: asset inflation feels great. It makes people feel richer, feel smarter, and feel like they’re winning. And when people feel good, they don’t ask questions. They don’t look under the hood. They don’t wonder why wages aren’t keeping pace, or why groceries now cost what rent used to. They just look at their brokerage app and smile like everything’s fine.

But remember this: prosperity built on diluted currency isn’t prosperity.

It’s a hall of mirrors; shiny, impressive, and guaranteed to collapse the moment someone turns on the real lights.

Every magic trick has one thing the magician desperately hopes you never notice. In this bull market, that thing is liquidity. If the Fed keeps the dollars flowing like a busted fire hydrant, everyone acts like the laws of finance have been suspended. “Valuation doesn’t matter! Debt doesn’t matter! Fundamentals are for old people!”

But here’s where the spell cracks: the moment money stops being free.

When borrowing costs rise, when credit tightens, when the bond market gets indigestion, the whole parade comes to a screeching halt. Suddenly, everyone who was “investing for the long term” is sprinting for the exits like the building just caught fire.

And trust me… it happens fast.

Not gradually. Not politely.

One day the market is a victory parade — the next day it’s a liquidation sale with blood on the floor.

Because when investors stop asking “What’s the story?” and start asking “Where’s the cash?” — that’s when valuation matters again. That’s when the delusion evaporates. And that’s when price finally remembers it has a gravitational pull.

The moment confidence breaks, the entire structure collapses like a soufflé in a hurricane.

Let’s just call this what it is. The stock market isn’t rising because America suddenly unlocked a new era of innovation and productivity. It’s rising because we have flooded the system with trillions of new dollars. Money so cheap and abundant that asset prices had to go higher. Wall Street has been riding that wave like a rocket strapped to a bottle of lighter fluid.

And you can see the evidence everywhere. Corporate debt has never been higher. The federal deficit is running hotter than GDP itself. The Fed keeps supplying liquidity, and the dollar keeps losing purchasing power — quietly, slowly, steadily. Yet markets keep climbing because the idea of letting them fall has become politically and psychologically unacceptable. No one wants to be the adult in the room.

And we need to be honest about the road ahead. This isn’t sustainable. Sooner or later, every market finds itself standing in front of the mirror with the lights on. And when that happens, all the makeup, smoke, and mood lighting disappears. Value steps back into the room like the stern parent who just got home early and wants to know why the house smells like bourbon and bad decisions.

But here’s where the winners separate from the tourists:

The traders who survive — and thrive — in the markets aren’t the ones who predict the exact day the music stops. They’re the ones who know the music will stop and position themselves accordingly.

They don’t chase hype.

They don’t trust headlines.

They watch value, strength, and flow.

Because while the crowd screams for more confetti, the pros are already looking for the exit… and sharpening their knives for the opportunities that come *after* the crash.

In the end, what we’re witnessing is a market suspended in midair — not because it has learned how to fly, but because the ground beneath it has been quietly lowered. A bull market fueled by debased currency and artificial liquidity can, for a time, appear unstoppable. It can rewrite narratives, bend assumptions, and make even the most seasoned observers question the meaning of value itself. But no market stays untethered forever.

At some point, the printing slows. The liquidity thins. The narrative shifts. And when it does, valuations that once seemed justified by momentum and sentiment will be measured again against earnings, assets, and reality. The market will remember what value means, just as it always has — abruptly, often painfully, and with little regard for how comfortable the prior illusion felt.

For traders, the challenge isn’t to predict when that shift occurs — but to be prepared for it. To know how to identify real strength in a landscape where price alone can mislead. To distinguish leadership from leverage. And to navigate volatility not as chaos, but as opportunity.

That’s why we invite you to join our live FREE A.I. trading masterclass. Not to chase stories — but to learn how to see the market clearly, even when the signals are distorted and the noise is deafening. The tools are here. The moment is here. The advantage is available to those who choose to take it.

VantagePoint’s A.I. changes everything. A.I. doesn’t get emotional. It doesn’t care about headlines, pundits, or the drama of the moment. It watches the data the way a hawk watches the field — with absolute attention and no bias. It identifies trends when they’re beginning, not after they’ve already become obvious. And it calculates probability the way only machines can: coldly, cleanly, and relentlessly. When the market behaves rationally, A.I. confirms the move. When the market behaves irrationally, A.I. alerts us to the opportunity. In both cases, clarity replaces confusion.

Once you see this in action, you’ll never go back to trading blind. It’s like turning on the lights in a room you didn’t even realize was dark. When you trade with A.I., you stop hoping and start knowing — and that’s where the real money is made.

So here is your invitation — and I mean this sincerely: attend a complimentary live online A.I. trading masterclass. No speeches. No marketing fluff. Just a real demonstration, on real charts, in real time. Watch the A.I. identify leaders, rank strength, and reveal hidden opportunity in a market most investors barely understand. If you want to overcome noise, sharpen your edge, and trade with the calm confidence of someone who finally knows why they’re making every decision — this is your moment.

Come see the A.I. in action. Let clarity replace confusion. Let advantage replace hope.

Reserve your seat and step into the future while everyone else is still reacting to the past.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.