When it comes to understanding economics and finance, I keep things simple. I have a North Star. Not a model, not a spreadsheet, not a PhD dissertation wrapped in Greek letters. Just one brutally honest comparison that tells me whether the system is working… or just telling me it is.

All I do is compare the percentage increase in the price of Gold since we closed the Gold Window and abandoned the Gold Standard to a broad stock market proxy like the Dow Jones Industrial Average. Why? Because it’s my reality detector. My built-in nonsense filter. It doesn’t care about narratives, press releases, or economists with confident eyebrows. It just measures outcomes.

Back in 1971, money was supposed to mean something. In theory, it was anchored to gold. That shiny rock in the vault wasn’t decoration, it was discipline. So gold, whether policymakers like it or not, has become the ultimate report card. It grades how well the economy and the entire financial system have been managed since that fateful day.

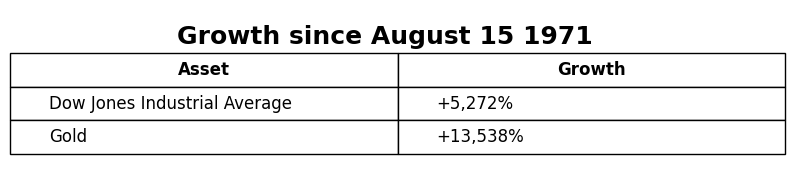

Now, if you only look at the Dow, the story sounds terrific. Up 5,272%. A triumph. A parade. A chest-thumping celebration of modern finance. Turn $1,000 into $53,720 and you start to feel pretty clever.

Then you glance at Gold. That same $1,000 becomes $136,385.

And suddenly the parade gets quiet.

Want to look at it another way? In 1971, it took roughly 25.4 ounces of gold to purchase the Dow Jones Industrial Average. Today, that same index can be acquired for just 9.97 ounces. On the surface, equities appear to have delivered substantial gains over the past five decades. But when measured against gold, a different picture emerges.

The comparison reframes the narrative. Gold, often dismissed as a “barbarous relic,” has in fact outpaced the Dow in preserving purchasing power. By this measure, the Dow has effectively underperformed gold by approximately 61% since the closing of the gold window.

What this highlights is not simply asset performance, but the lens through which performance is evaluated. When denominated in dollars, equities tell one story. When denominated in gold, they tell another entirely.

What does it tell you about economics when what used to be money outperforms the 30 top industrial companies in the United States by that kind of margin? What does it say about stewardship, about policy, about the invisible hands that are apparently very busy doing something?

Think about it.

And that uncomfortable little comparison, that stubborn reality detector, is exactly why this conversation matters. Since the Gold window was closed in 1971, the world has been asked to believe in paper while quietly watching gold keep score, and it has done so with unnerving consistency, outpacing even the proud machinery of the Dow. But here is the detail that deserves your full attention: the largest, most informed buyers of Gold today are not speculators or survivalists, but central banks themselves. The very institutions that design, manage, and defend the fiat system are steadily accumulating the one asset that sits outside it. When those entrusted to steward paper money choose, in size, to hold what used to be money, they are revealing a preference that words will never admit. And for the thoughtful observer, that contradiction speaks louder than any policy statement ever could.

There is a strange pattern in history that only becomes clear after events have already unfolded. The people who understand what is coming are almost always ignored the longest. Not because they lack intelligence or experience, but because what they say is uncomfortable during times of prosperity. When everything appears to be working, warnings feel unnecessary. And so, they are dismissed.

For more than fifty years, while the global economy expanded and markets reached new highs, a consistent warning was repeated. It centered on debt, currencies, and the illusion of stability created by unlimited money creation. These ideas were not fringe or poorly reasoned. They were grounded in observation and experience. Yet they were still ignored.

Those warnings came from thinkers aligned with the Austrian school of economics. They were not speaking from theory alone. They had operated in real markets, moved capital across borders, and witnessed monetary fragility firsthand. While they disagreed on many things, they shared one conclusion. The system was becoming dangerously dependent on debt and intervention.

What makes their message relevant today is not a single prediction. It is the process they described. Governments borrowing beyond their means. Central banks responding to every slowdown with more liquidity. Interest rates pushed lower to hide the true cost of debt. And eventually, a growing risk not of recession, but of lost confidence in money itself.

At the time, these warnings felt abstract. Markets were rising and confidence was high. Inflation appeared contained. The system seemed stable. It felt as though modern finance had solved its own problems. But these thinkers were not guessing. They were observing patterns that have repeated throughout history. They studied past debt cycles, currency collapses, and economic expansions built on credit. What they recognized was familiar. Prosperity built on expanding debt is not permanent. It is borrowed time.

As the years passed, the message did not change. What changed was the environment. Financial crises came and went. Each time, the response was more intervention, more liquidity, and more debt. And each time, recovery reinforced the belief that the system was working.

This created a dangerous illusion. As long as markets recovered, the warnings seemed unnecessary. But the underlying conditions continued to build. Debt expanded. Dependence deepened. And risk became less visible, not less real. The Austrian school repeatedly emphasized a simple truth. Money works because it is trusted. Trust is not guaranteed. And once weakened, it is difficult to restore. The more intervention required to maintain stability, the more that trust is quietly tested.

Over time, their observations formed a consistent narrative. Debt cycles expand until they reach limits. Currency debasement reduces purchasing power. Inflation emerges after long delays. And historical patterns repeat, even when they appear different on the surface. What stands out when revisiting these warnings is their tone. They were not dramatic. They did not rely on predictions of exact timing. They focused on inevitability. When money supply grows faster than value, adjustment follows.

Today, many of the conditions they described are visible. Inflation has returned across major economies. Debt levels are historically high. Central banks are struggling to balance growth and stability. What once seemed theoretical now appears practical. The most unsettling realization is how long these signals were present. The issue was not a lack of information. It was a lack of willingness to listen. Prosperity has a way of silencing uncomfortable truths. And for a long time, prosperity appeared to justify ignoring them.

Now those limitations are reappearing. Not as something new, but as something familiar. The names and tools may have changed. But the underlying mechanics have not. Monetary history does not disappear. It repeats.

History does not announce itself loudly. It moves quietly, repeating patterns in new forms. The Austrian school emphasized that monetary systems evolve in appearance, but not in structure. Debt growing faster than productivity leads to imbalance. Money growing faster than value leads to instability. They viewed history as a guide, not a theory. Empires did not fail because of ignorance. They failed because they believed they could manage money without consequence. Currency debasement has taken many forms. But the outcome has remained consistent.

The pattern itself is straightforward. Growth begins with real productivity. Credit accelerates that growth. Over time, dependence on debt increases. Intervention replaces correction. And eventually, the imbalance becomes visible. For years, economies operated comfortably within the early stages of this cycle. Confidence remained high. The risks appeared manageable. And modern financial tools gave the impression that the cycle could be controlled.

But history suggests otherwise.

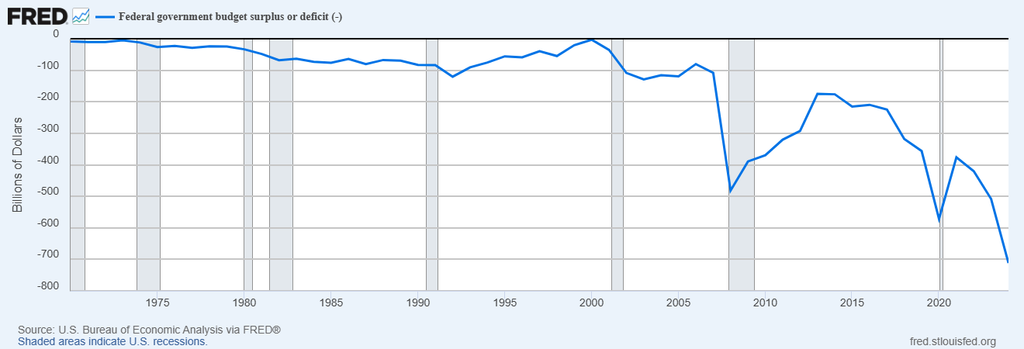

Study the chart above of annual budget deficits. This all started in 1971 when we closed the gold window in favor of fiat and started throwing money at every problem that arose.

We need to understand that whenever we study government finance, their projections depend on a truly heroic assumption. Namely, that nothing bad will happen. No wars, no recessions, no surprises that require Uncle Sam to reach deeper into the taxpayer’s pocket. That assumption has never been accurate; we have been at war in one form or another since I have been alive. That reality showed up again last month, kicked the door in, and asked for another $200 billion to fund the Iranian conflict.

And that is just the opening act.

Even under this cheerful, everything-goes-right fantasy, the US government is still expected to pile up more than $22 trillion in deficits over the next decade. Not a typo. Trillion, with a T. The kind of number that makes Monopoly money look responsibly managed.

Of course, deficits do not pay for themselves. They get financed the old-fashioned way. By issuing more debt and hoping someone buys it. And when not enough people volunteer, the Federal Reserve steps in, fires up the printing press, and creates money out of thin air like a magician who never learned the word “stop.”

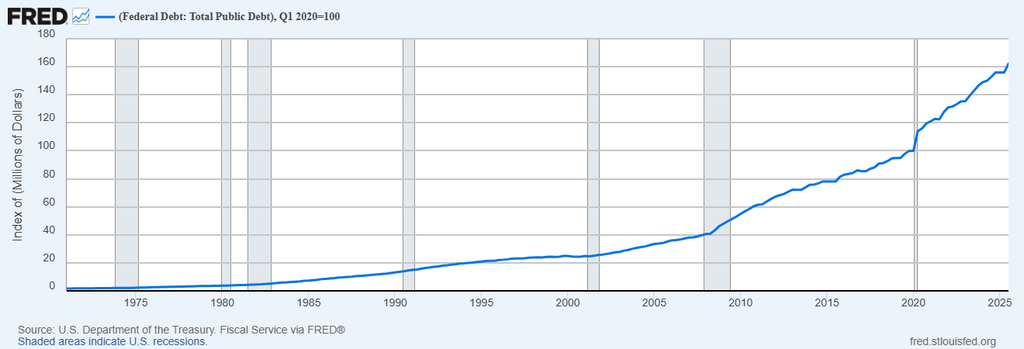

The federal debt has now wandered past $39 trillion, which puts it somewhere north of 124% of GDP. That sounds alarming until you remember that GDP is a bit like a bathroom scale that counts your shoes, your coat, and maybe the dog as “healthy weight.” It treats government spending as a positive, which is a charming idea if you believe maxing out a credit card improves your net worth. In reality, government spending is less “growth” and more “we’ll deal with this later,” except later always shows up with interest.

In the United States, government spending makes up at least 37% of GDP. Which means a large chunk of what we call “economic output” is just money being borrowed, spent, and congratulated for existing. Take that out, and the picture starts to look less like a booming economy and more like a very expensive addiction.

Now consider this. That extra $200 billion the Pentagon wants for the Iran situation gets counted as a positive in GDP. Tanks roll out, spreadsheets light up, and economists nod approvingly as if we just invented something useful. But remove government spending from the equation and suddenly the economy looks a lot less like a success story and a lot more like a carefully managed illusion.

Of course, suggesting that might get you labeled as someone with “unapproved thoughts.” In a world where numbers are massaged, definitions are flexible, and reality is optional, pointing out the obvious can start to sound like a conspiracy. Which is usually a good sign you are getting close to the truth.

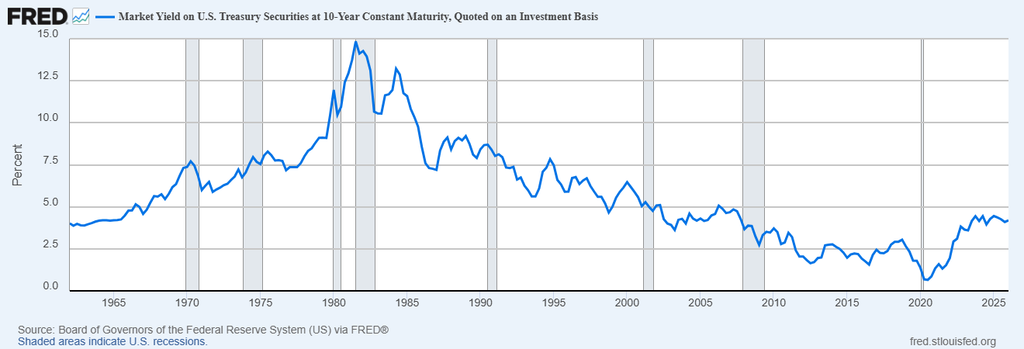

The most important price in markets, and in free market capitalism, is the cost of money, also known as interest rates. It determines everything. Risk, investment, savings, speculation. And yet somehow, we allow that price to be dictated not by millions of buyers and sellers, but by a handful of bureaucrats in Washington, D.C. That is not a free market. That is price control at the highest level.

Start with first principles. Central planning does not work. Not for shoes. Not for wheat. Not for anything that requires real supply and demand. And yet, for reasons nobody can clearly explain, we make a special exception for money, the single most important input in the entire system. The truth is simple. No committee knows what interest rates should be. Only a free market of savers and borrowers can discover that price. Anything else is guesswork with consequences.

Look at the record. Rates pushed to near zero after 2008, then slowly rose, then forced back to zero in 2020, followed by one of the fastest hiking cycles in history as inflation surged. From zero to over five percent in less than two years, and now back toward easing before inflation is fully under control. This is not precision. It is reaction. And when the most important price in capitalism is constantly being guessed at, volatility is not a surprise. It is the result.

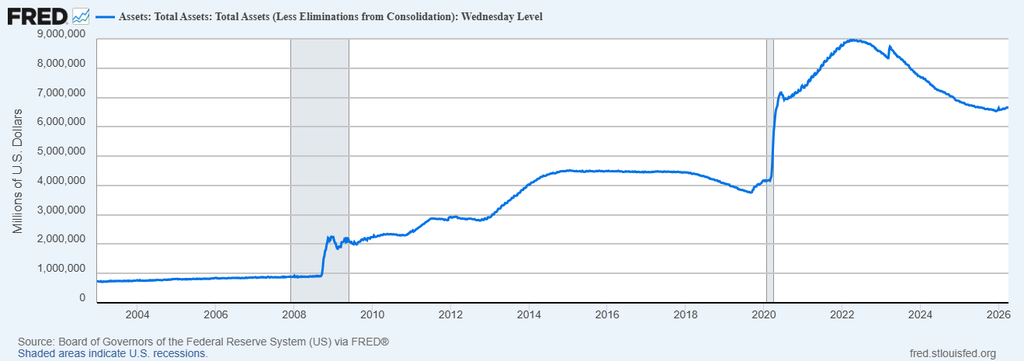

The Fed just told you it’s done shrinking its balance sheet and is ready to grow it again. Of course, they won’t call it money printing. They’ve dressed it up in a nice suit and named it “reserve management.” Sounds harmless. It’s not. When you buy Treasuries with money you just created, you’re printing. Period.

And here’s the part they hope you don’t notice. This movie has played before. The Fed expands. Then it promises to shrink. Something breaks. Then it runs right back to printing again. And every time, the balance sheet never goes back down to where it started. It just steps higher… and stays there.

Before 2020, the balance sheet was about $4 trillion. Then it exploded to nearly $9 trillion. Even after all the talk about tightening, it’s still massively elevated and now heading higher again. Translation. The dollar gets diluted every time they do this. This isn’t a mistake. It’s the system. And if you want to know what comes next, look at what happened the last time they flipped the switch. They are just getting started.

Now look at that chart. In 2008, the Fed’s balance sheet stood at about $905 billion. Today it’s roughly $6.6 trillion. That’s a 635% increase in just 18 years. If you’re wondering why your dollar buys less, look no further than that number.

When debt funds productivity, it creates growth. When it funds the appearance of stability, it creates risk. Over the past two decades, every crisis has been met with more borrowing, more stimulus, and lower rates. Not because the system is strong, but because higher rates would expose how fragile it has become. That is the tradeoff. Stability today in exchange for greater instability later.

At the same time, markets have shifted. They are no longer driven purely by fundamentals. They are driven by expectations of intervention. Investors are not asking what something is worth. They are asking what central banks will do next. That changes behavior. Risk is not eliminated, it is deferred. And each intervention reinforces the belief that support will always be there, increasing dependency across the system.

Over time, confidence replaces fundamentals as the primary driver. That creates a feedback loop where stability encourages risk, and risk demands more intervention. But this balance is fragile. Small changes can trigger large reactions because the system depends on support. Eventually, options narrow. Policymakers can delay outcomes, but they cannot remove them. And when adjustment comes, it is not a surprise. It is the result of a structure that has been building for years.

All this financial engineering has not delivered stability. It has delivered cycles. Boom, bust, rescue, repeat. Each time the system is stressed, the response is the same. More liquidity, more intervention, more debt layered on top of existing debt. The result is not resolution. It is accumulation. Over time, this has changed how people view the system itself. Trust has eroded. Not in a dramatic way, but in a steady, persistent way. People no longer assume institutions have control. They question it. And when trust weakens, the entire foundation of the financial system begins to shift.

What people feel most is not policy. It is purchasing power. Money does not disappear overnight. It erodes slowly. Groceries cost more. Housing becomes less attainable. Everyday life becomes more expensive without a clear explanation that satisfies anyone paying attention. This is the real consequence of monetary expansion. Inflation is not just a number. It is a transfer of wealth. Savers lose. Asset holders gain. And for those sitting in cash or relying on fixed income, the impact is immediate and ongoing.

In response, the market has adapted. Bitcoin and other crypto emerged as a reaction to this environment. A system designed, at least in principle, to operate outside of centralized control. A way to hold value that cannot be easily diluted by policy decisions. But even here, the outcome is not simple. Crypto introduces new volatility, new risks, and new uncertainties. It reflects the same underlying truth. People are looking for ways to escape a system they no longer fully trust.

Much of the inflation has not shown up evenly across the economy. It has flowed into financial assets. Stocks, real estate, and other markets have absorbed a significant share of the liquidity created over the past decade. This has pushed asset prices higher and widened the gap between those who own assets and those who do not.

For savers, this creates a problem. Traditional strategies no longer work the same way. Holding cash guarantees loss of purchasing power. Passive participation is no longer enough. The environment has changed, and the rules have changed with it. The consequences are visible across generations. Retirees, who once relied on stable income and predictable costs, now face uncertainty. Many delay retirement or adjust their expectations downward. The system they planned for no longer behaves the way it used to. At the same time, younger generations face a different challenge. Home ownership feels increasingly out of reach. Costs rise faster than incomes. The traditional path to financial stability becomes harder to follow. The pressure is not theoretical. It is lived.

In this environment, the role of the individual changes. It is no longer enough to save. It is no longer enough to wait. The system rewards participation, not passivity. Capital must move. It must adapt to changing conditions. This is where trading enters the picture. Not as speculation, but as a response. A way to engage with markets that are being driven by liquidity, policy, and volatility. In a world where purchasing power is constantly under pressure, trading becomes less of a choice and more of a necessity.

Saving money the old way is no longer safe. It’s a slow bleed. You park your cash, feel responsible, maybe even a little proud… and all the while it’s quietly losing value. Inflation doesn’t knock on the door. It just helps itself.

And that “safe” fixed income everyone talks about? If inflation is higher than your return, you’re not earning… you’re shrinking. You just don’t see it in real time. But it’s happening every single day.

Doing nothing used to be conservative. Now it’s a guaranteed way to fall behind.

Once upon a time, markets were driven by things like earnings, productivity, and whether a company actually made money. It was all very quaint. Today, markets are driven by liquidity, central banks, and wherever the largest pile of money feels like wandering next. Fundamentals still exist, of course, in the same way a user manual exists for a toaster. Technically important, rarely consulted.

What really moves prices now is policy. Interest rates get nudged, liquidity gets injected, and capital flows stampede from one corner of the market to another like caffeinated cattle. The result is not stability. It is motion. Constant, occasionally violent motion.

Volatility is the setting. And if you think you are investing in the same system your parents did, you might also believe gas still costs 50 cents and your retirement plan comes with a gold watch.

Capital can no longer sit still. It must move. In today’s market, where you place your money matters more than simply being invested. The difference between strength and weakness is not subtle. It shows up clearly in relative performance.

The winners keep winning. The laggards continue to drain capital. Holding underperforming assets is not neutral. It is a slow erosion of wealth. And most investors do not recognize it until the damage is already done.

This is the shift. It is not about being in the market. It is about being aligned with what is working. Capital must be positioned with strength, or it will be left behind.

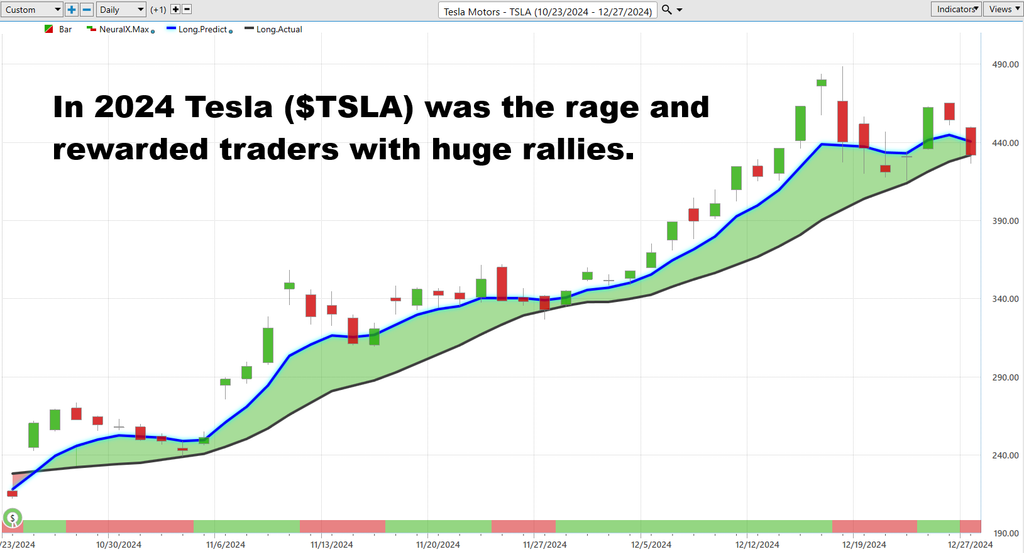

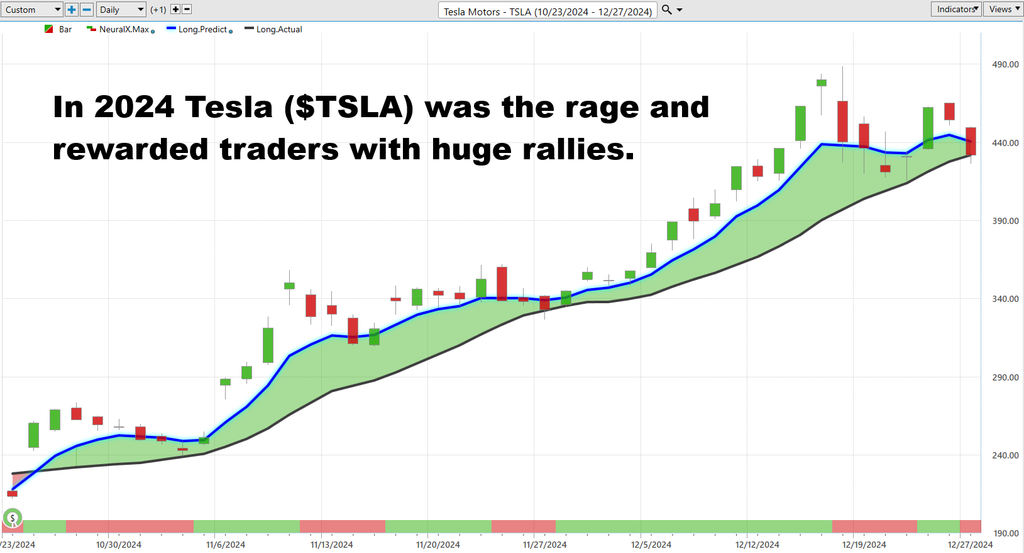

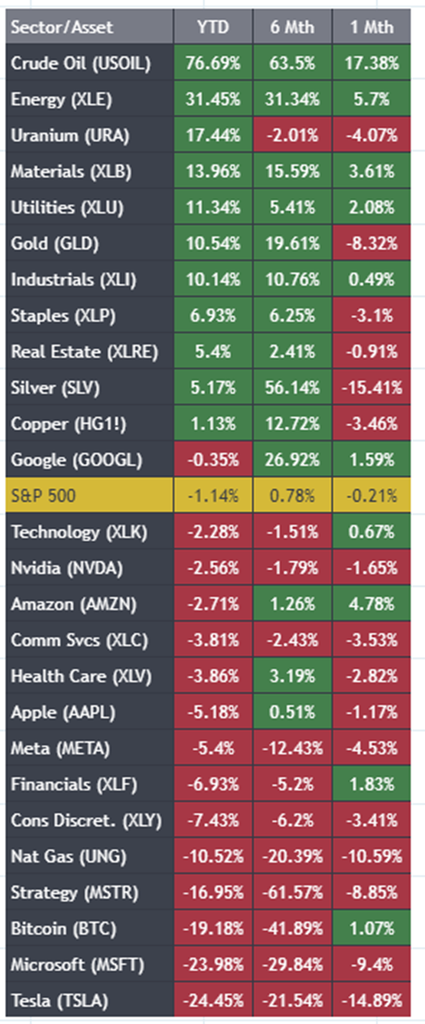

You can observe this for yourself by simply looking at the performance of a stock like Tesla ($TSLA) in 2024 when the Magnificent 7 were dominating the markets versus today where the market has abruptly changed.

Volatility has a branding problem. It’s often described as risk, instability, something to be avoided. But in practice, volatility is simply movement. And movement is where opportunity lives. Markets that don’t move don’t offer much to work with.

What matters is not whether volatility exists, but how it’s interpreted. For some, it creates uncertainty. For others, it creates structure. Price swings, when viewed correctly, are not random. They reflect shifts in positioning, liquidity, and expectation. That is where repeatable opportunity begins to take shape.

The distinction is important. Volatility does not inherently destroy capital. Misunderstanding it does. And in an environment where volatility is persistent, the ability to navigate it becomes less of an advantage and more of a requirement.

The modern market presents a challenge that is easy to underestimate. The volume of information, the speed of price movement, and the number of interconnected variables have reached a level that no individual can fully process in real time. What was once manageable through analysis and experience has become something far more complex.

Today, markets are influenced simultaneously by interest rates, currencies, commodities, geopolitical developments, and policy decisions. These forces do not operate in isolation. They interact, reinforce, and at times contradict one another. The result is a landscape where cause and effect are no longer linear, and where traditional analysis can quickly fall behind.

This is the reality investors now face. The limitation is no longer access to information, but the ability to synthesize it. And increasingly, the question is not whether you have the data, but whether you can keep up with what the data is telling you.

If markets are moving faster than you can think… and reacting to forces you can’t track… then trying to do it all yourself is like bringing a knife to a gunfight. You might get lucky once. But over time, you’re outmatched.

This is where VantagePoint AI changes the game. It doesn’t guess. It processes. It tracks relationships across markets, spots patterns you’d never see, and gives you a directional edge before the move becomes obvious. No emotion. No hesitation. Just data doing what data does best.

Run the numbers again before you draw your conclusions. Since 1971, Gold has outpaced the Dow Jones Industrial Average by a massive margin, turning the same $1,000 into more than double the outcome.

And here is the uncomfortable truth for traders. The old playbook is not keeping up. When the landscape shifts this dramatically, instinct and tradition are not enough. To stay competitive, to keep pace with markets that move faster than ever, traders must learn to trade with VantagePoint AI.

Our AI doesn’t replace you. It puts you in a position to stop reacting… and start anticipating.

Trading has a public relations problem. Most people still picture chaos, noise, and blown-up accounts. But what’s happened is far more rational. Trading has grown exponentially because of one simple reality. Persistent currency debasement. When money loses value over time, people are forced to do something with it. Sitting still is no longer safe.

At the same time, both individuals and institutions have shifted toward shorter duration. Not out of preference, but out of necessity. The longer you hold, the more exposure you have to inflation, policy mistakes, and market shocks. So capital moves faster. It goes where strength is, captures opportunity, and avoids prolonged risk. This is not speculation. It is adaptation.

There was a time when buy and hold made sense. Find a quality asset, hold it forever, and let time do the work. The tide would eventually lift you. Today, that tide is unpredictable and often working against you. Trading replaces blind patience with active decision making. It is not about guessing. It is about managing risk, working with probabilities, and staying in the game. Done correctly, it is not reckless. It is practical.

The objective has changed. You are not trading to get rich. You are trading to maintain your position. In an environment where purchasing power is steadily declining, standing still is the same as moving backward.

This is the new mandate. Capital must be managed with intention. It must adapt to where opportunity exists and avoid where risk is concentrated. Passive strategies no longer provide the same protection they once did.

In this environment, participation is required. Not for speculation, but for preservation. The goal is simple. Stay aligned with what is working and protect what you have.

The market is fractured. What used to be “safe” can fall apart fast… because even the definition of quality keeps shifting under your feet.

The only edge now is seeing those shifts early… and that’s exactly where VantagePoint changes the game.

You can feel it, can’t you?

The rules have changed. Quietly. Persistently. And now, undeniably. What once worked no longer delivers the same result.

You have seen the shift. Saving is no longer enough. Buy and hold is no longer safe. The market now rewards those who can move with precision, not patience alone. The question is no longer whether you should adapt. The question is how. And increasingly, the answer lies in VantagePoint AI software that can operate at a speed and depth no individual can match.

When you choose VantagePoint AI, you are choosing to work with a tool that sees the market faster than you can. VantagePoint AI analyzes thousands of data points in seconds, identifying trends before they become obvious. It tracks intermarket relationships across currencies, commodities, and equities simultaneously. And it does so without emotion. No hesitation. No second-guessing. Just clean, disciplined execution based on data.

More importantly, this is not about reacting to what has already happened. VantagePoint software is designed to anticipate what is likely to happen next. It simplifies overwhelming complexity, filters out noise, and highlights high-probability opportunities that most traders never see. As markets evolve, VantagePoint AI continuously adapts, ensuring that you are aligned with current conditions rather than relying on outdated strategies.

This is the advantage. Not replacing your judgment but enhancing it. Not removing you from the process but elevating your position within it.

If you are serious about protecting your purchasing power and participating in today’s markets with confidence, now is the time to act. Learn how to trade with AI in a way that is practical, repeatable, and built for the market we are actually in. Because in this environment, the edge belongs to those who are prepared.

Join us for a Free Live Online “Learn How to Trade with VantagePoint AI” Masterclass.

Bring your charts.

Bring your skepticism.

Then see what happens when you stop guessing… and start seeing patterns most traders miss.

Because in a market like this, there are only two kinds of traders:

Those who follow real strength… And those who are simply hoping they’re right.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.