Most people hear the word “options” and immediately assume they’ve stumbled into a secret Wall Street casino filled with equations, Greek symbols, and traders screaming into six computer monitors while drinking cold espresso.

Relax.

Options are not magic.

They are simply agreements built around price, time, and risk.

That’s it.

In fact, you already understand the basic idea of an option even if you’ve never traded one in your life.

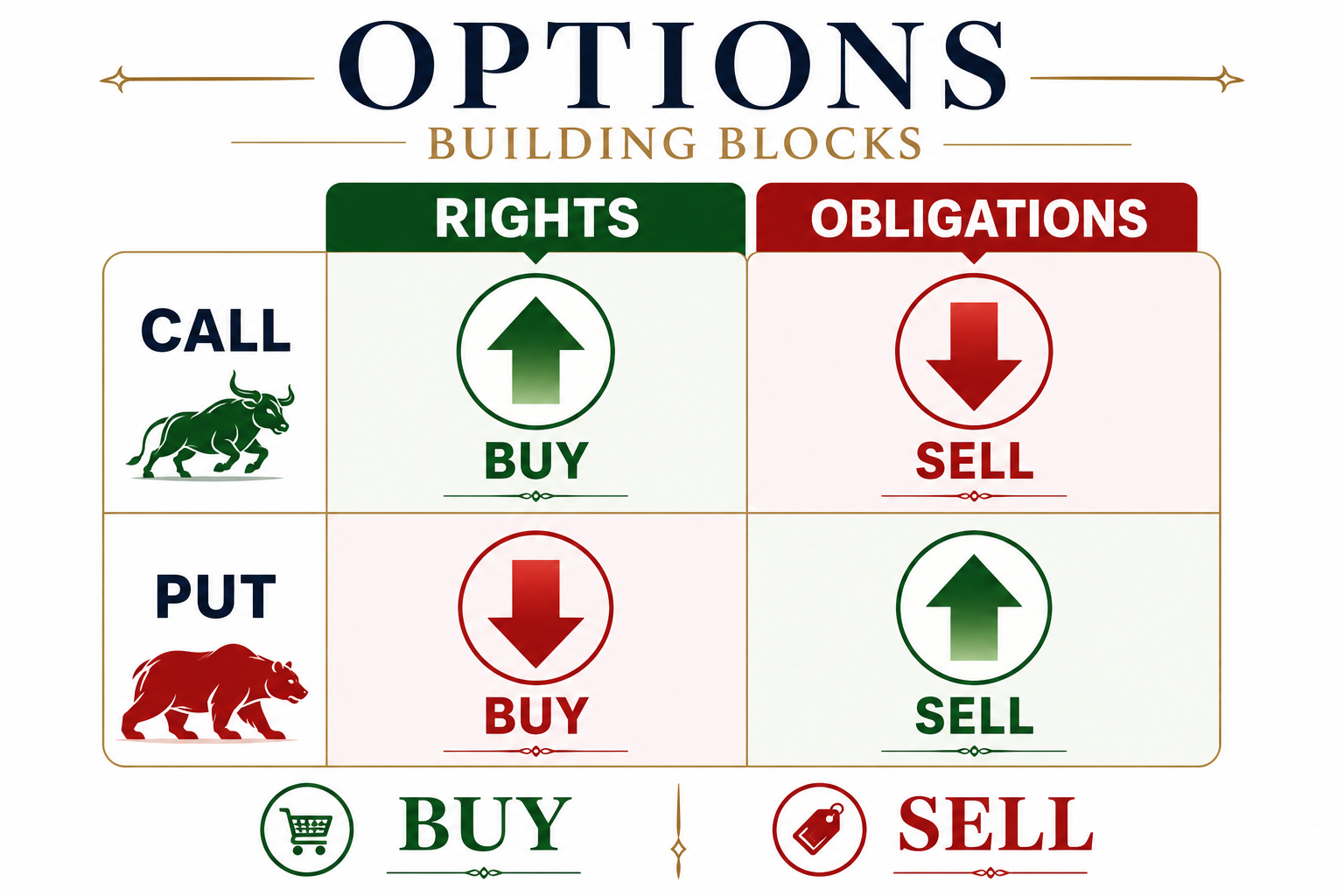

To really understand options, you first need to understand the difference between a “right” and an “obligation.”

Because that one distinction changes everything.

When you buy an option, you are buying a right.

Not a responsibility.

Not a commitment.

Not a requirement to act.

You are paying for flexibility.

Whoever sold or created that option has a contractual obligation. Unless they liquidate their position they are contractually obligated to deliver on the contractual agreement if you choose to exercise your option.

Specifically, you as a buyer, are paying a premium to gain the right to buy or sell an asset at a specific price before a certain expiration date.

That’s the core idea behind every option contract ever created.

An option is simply a temporary contractual agreement tied to price and time.

The buyer has a right.

The buyer is never obligated to act.

That matters because it defines the risk.

The easiest way to understand this is to think about insurance.

Every insurance policy you’ve ever owned is basically an options contract.

You pay a premium to an insurance company for protection over a specific period of time.

Your car insurance expires.

Your health insurance expires.

Your homeowners insurance expires.

If something bad happens while the policy is active, you have protection.

If nothing happens, the policy simply expires.

That doesn’t mean the insurance was worthless.

It means you paid for protection and peace of mind during that period.

Options work the same way.

Now let’s talk about a Call Option.

A Call Option gives the buyer the right, but not the obligation, to buy an underlying asset at a specific price before expiration.

That agreed-upon purchase price is called the strike price.

The buyer pays a premium for this right.

And here’s where things start getting interesting.

As the buyer of a call option, a trader’s upside can theoretically be unlimited because a stock can theoretically continue rising forever.

Meanwhile, the risk is limited to the premium paid for the option.

That asymmetry is one reason options attract traders.

Now another important detail:

Each stock option contract controls 100 shares of stock.

So when a trader buys one option contract, they are controlling 100 shares of the underlying asset without necessarily paying for all 100 shares outright.

Every option also comes with an expiration date.

That expiration date defines how long the contract remains active.

Most stock options trade in short-term durations like 30, 60, or 90 days.

But there are also LEAPS, which are long-term options that can extend a year or more into the future.

Every option has a premium.

The premium is simply the price of the contract.

It is the amount the buyer pays to obtain the rights embedded in the option.

In exchange for paying that premium, the buyer controls 100 shares of stock until expiration.

And now you’re beginning to see why options are so powerful.

They allow traders to control opportunity, risk, and time in ways ordinary stock ownership cannot.

To make this crystal clear, let’s walk through a simple real-world example.

Imagine, hypothetically, you find a house selling for $300,000. You think the neighborhood is improving fast and prices may rise. But you’re not ready to buy the house today. So you give the seller a small deposit for the right to buy the house at $300,000 anytime over the next 100 days.

Now suppose the market explodes and the house becomes worth $350,000.

Your agreement suddenly became valuable.

Why?

Because you locked in the right to buy something at a lower price.

That is the basic logic behind a call option.

A call option gives you the right, but not the obligation, to buy a stock at a specific price before a certain date.

That “specific price” is called the strike price.

That “certain date” is called expiration.

Suppose a stock is trading at $100 per share.

In this hypothetical example, you believe the stock may rise sharply over the next two months. Instead of buying the stock outright, you buy a call option with a strike price of $105.

What are you really saying?

You’re saying:

“I want the right to buy this stock at $105 before expiration.”

Now imagine the stock climbs to $130.

Suddenly, the right to buy the stock at $105 becomes very valuable because the market price is now much higher.

You secured an opportunity using a smaller amount of money than buying the stock itself.

That is one reason traders use options.

But options are not only used for speculation.

They are also used for protection.

This is where put options enter the picture.

A put option gives you the right to sell a stock at a fixed price before expiration.

Think about insurance on your car.

You hope you never need it.

But if something bad happens, you want protection.

A put option works similarly.

Suppose you own a stock trading at $100. You are worried the market could suddenly collapse, but you do not want to sell your shares yet.

You could buy a put option with a strike price of $95.

Now imagine disaster strikes and the stock falls to $70.

Without protection, you would simply absorb the loss.

But with the put option, a trader still has the right to sell the stock at $95.

That protection has value.

This is why professional traders, hedge funds, and institutions use options constantly. They are tools for managing uncertainty.

And uncertainty is everywhere in financial markets.

Now let’s simplify two important terms you’ll hear repeatedly.

The strike price is simply the agreed-upon price written into the contract.

The expiration date is the deadline.

Every option has a clock attached to it.

That clock matters.

A lot.

If the stock does not move the way you expected before expiration, the option can lose value or even expire worthless.

That is one of the biggest differences between stocks and options.

A stock can theoretically be held forever.

An option cannot.

Time changes everything in options trading.

This is why experienced traders pay close attention not only to price movement, but also to timing.

Now you may be wondering:

“Why use options instead of simply buying stock?”

Good question.

Because options allow traders to shape risk and opportunity in ways stocks alone cannot.

Some traders use options to speculate on large price moves.

Some use them to generate monthly income.

Some use them to protect portfolios during dangerous markets.

Some use them to reduce the amount of money committed to a trade.

Others use them to benefit from volatility itself.

Options create flexibility.

And flexibility matters because markets can be very volatile and unpredictable.

But let’s be honest about something important right now.

Options involve risk.

A call option can expire worthless.

A put option can lose value quickly.

Leverage cuts both ways.

When traders misuse options without understanding risk, losses can happen fast.

That is why options require some study to comprehend all of the possibilities.

It is about understanding structure, probability, and risk management.

Professional traders do not survive because they predict every move correctly.

They survive because they manage risk intelligently.

That is the real lesson behind options.

As we move through this Options Mastery Series, you’ll learn how professional traders structure trades differently depending on whether they expect a market to rise, fall, move sideways, become volatile, or calm down.

You’ll discover options strategies.

Strategies designed for protection.

Strategies designed for speculation.

And strategies designed simply to survive difficult markets.

But before any of that can happen, you must understand one simple truth:

An option is just a contract built around price, time, and uncertainty.

Once you understand that idea, the entire world of options starts becoming much easier to understand.

At first glance, options appear complicated because Wall Street has spent decades wrapping them in technical jargon, mathematical formulas, and enough Greek terminology to intimidate almost everyone outside a hedge fund conference room.

But the foundation is actually simple.

Every option transaction begins with one critical distinction:

Rights versus obligations.

That is the entire framework illustrated in this graphic.

When you buy an option, you are purchasing a right.

When you sell an option, you are accepting an obligation.

A Call Option gives the buyer the right to buy an underlying asset at a specific price before expiration. The seller of that call option, however, carries the contractual obligation to deliver the asset if the buyer decides to exercise that right.

A Put Option works in reverse.

The buyer of a put option purchases the right to sell an asset at a predetermined price before expiration. Meanwhile, the seller of that put option accepts the obligation to buy the asset if assigned.

That distinction matters enormously because it explains why options can behave so differently from stocks.

The buyer controls opportunity.

The seller accepts responsibility.

One side purchases flexibility. The other side accepts contractual exposure.

And suddenly the market starts looking less like chaos and more like a structured exchange of risk.

Professional traders often position themselves on the obligation side of the equation because obligations generate premiums. In exchange for accepting risk and contractual responsibility, option sellers collect income from buyers seeking rights and protection.

That single idea opens the door to an entire universe of strategies:

- Covered calls

- Cash-secured puts

- Credit spreads

- Iron condors

- Calendars

- Income portfolios

But before any trader attempts sophisticated structures, they must first understand the foundation beneath everything:

Who owns the right?

And who carries the obligation?

Because every advanced options strategy is ultimately nothing more than a carefully constructed combination of those two forces interacting with price, time, and uncertainty.

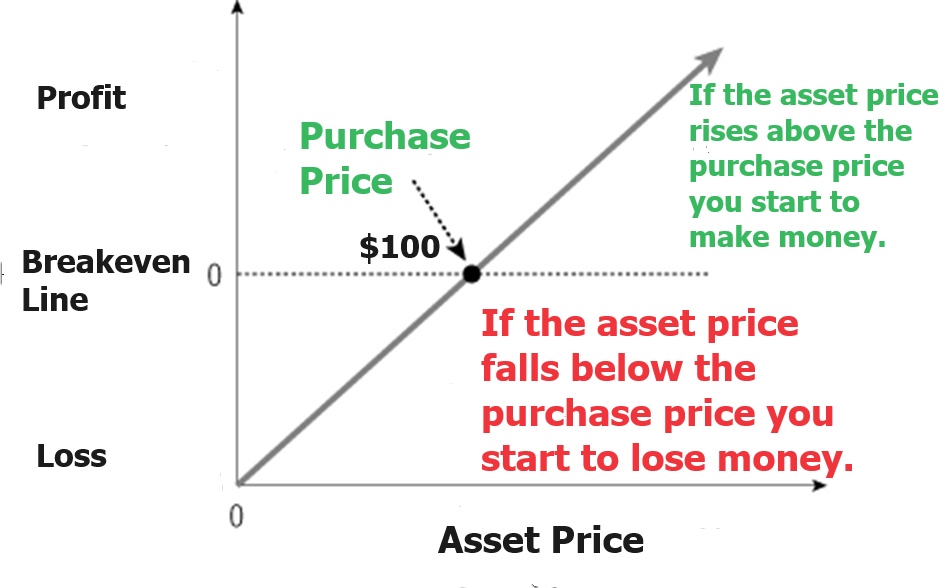

One of the most overlooked realities in investing is that every time you buy a stock, you are already accepting a risk-reward profile whether you realize it or not. If you purchase shares of a company at $100, your downside is immediate and very real. The stock can fall to $90, $70, or in extreme situations, even lower. Meanwhile, your upside is uncertain and dependent upon the market eventually rewarding your thesis. Options simply take this invisible relationship between risk and reward and make it explicit. They force traders to define time, exposure, obligation, and opportunity in advance rather than discovering those realities emotionally after volatility arrives.

That is why sophisticated traders often view options not as speculation, but as architecture. A stock purchase by itself is relatively simple: unlimited upside combined with potentially severe downside exposure. Options, however, allow traders to reshape that equation. They can reduce risk, generate income, hedge uncertainty, or structure positions around very specific market expectations. But before anyone can understand advanced strategies, they must first understand the basic exchange taking place underneath every options contract: one side is purchasing rights, while the other side is accepting obligations in exchange for compensation. Everything else in the options universe is built from that foundation.

The graph below shows the risk reward profile of buying a stock.

Factors to Consider When Buying Call Options

Buying a call option may appear deceptively simple on the surface. After all, the investor is merely expressing a bullish opinion on a stock. But beneath that straightforward premise sits a layered decision-making process involving capital allocation, probability, time, leverage, and risk tolerance. Unlike buying shares outright, purchasing a call option requires the trader to make several interconnected decisions before capital is ever committed.

The first consideration is premium outlay, which immediately changes the economics of the trade. One of the primary reasons investors gravitate toward call options instead of buying stock directly is leverage. Suppose a stock is trading at $100 per share and an investor has $1,500 risk capital available to invest. Purchasing the stock outright would allow ownership of only 15 shares. But if a one-month at-the-money call option costs $3 per share, or $300 per contract, that same $1,500 suddenly controls five contracts, representing 500 shares of stock. The investor does not own the shares, but they now possess the right to buy them at the agreed-upon strike price before expiration. This dramatically expands upside exposure while simultaneously introducing new forms of risk.

The second major decision involves selecting the strike price, which is arguably one of the most important variables in options trading. The strike price determines the level at which the buyer has the right to purchase the stock. Lower strike prices generally carry higher premiums because they provide more immediate value and greater sensitivity to stock movement. Meanwhile, out-of-the-money calls are cheaper because the stock must travel farther before the option acquires intrinsic value. Choosing the strike price is ultimately a balancing act between affordability, probability, and desired leverage.

Then comes the question of time to expiration, which introduces another layer of complexity unique to options markets. In options trading, time itself carries value. Longer-dated options generally cost more because they provide the stock with additional time to move favorably. Shorter-dated contracts are cheaper but place immediate pressure on the investor to be correct not only on direction, but also on timing.

Once strike price and expiration have been selected, the investor must determine position size. Returning to the earlier example, if each call contract costs $300 and the investor has $1,500 available, should all five contracts be purchased? Or is it more prudent to buy one or two contracts and maintain cash reserves? This is where options trading begins transitioning from pure speculation into portfolio management and risk control.

Finally, there is the question of execution. Options prices can move quickly, particularly during volatile markets or around earnings announcements. As a result, traders must decide whether to use market orders, which prioritize immediate execution, or limit orders, which prioritize price control. In practice, this seemingly minor operational detail can materially impact profitability over time, especially in less liquid options markets with wide bid-ask spreads.

Taken together, these decisions illustrate an important reality about options trading: buying a call option is not simply a directional bet. It is a structured decision involving leverage, timing, pricing, probability, and capital management all at once.

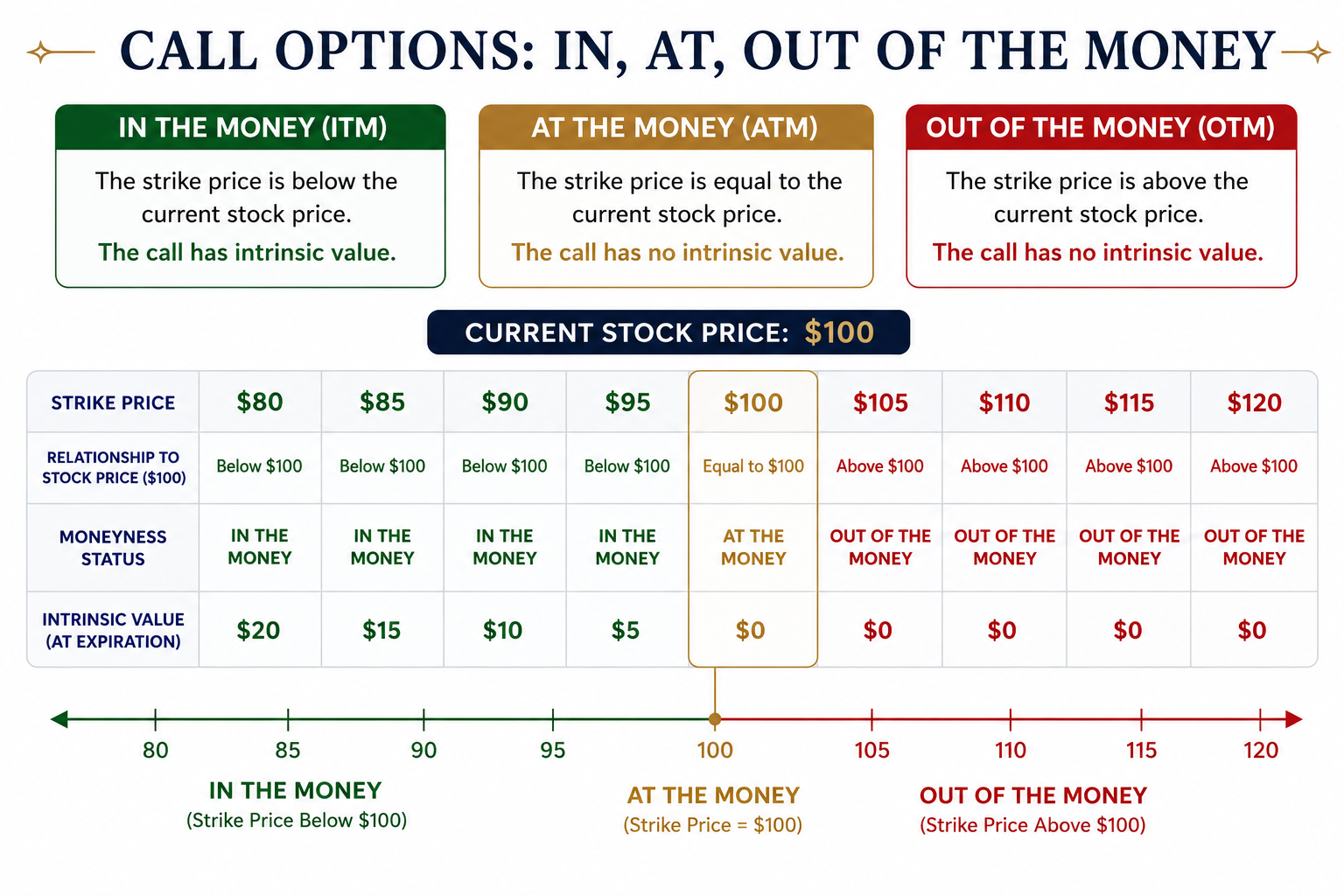

One of the most important concepts in options trading is understanding the relationship between the stock price and the strike price. This relationship determines whether a call option is considered in the money, at the money, or out of the money. While the terminology may sound intimidating at first, the logic is actually very straightforward once you visualize it.

The graphic below simplifies this process using a stock currently trading at $100. If the strike price is below the current stock price, the call option already possesses intrinsic value and is considered in the money. If the strike price is exactly equal to the current stock price, the option is at the money. And if the strike price is above the current stock price, the option is out of the money because the stock has not yet risen high enough to make the contract profitable at expiration. Understanding these distinctions is foundational because nearly every options strategy ultimately builds upon this simple framework.

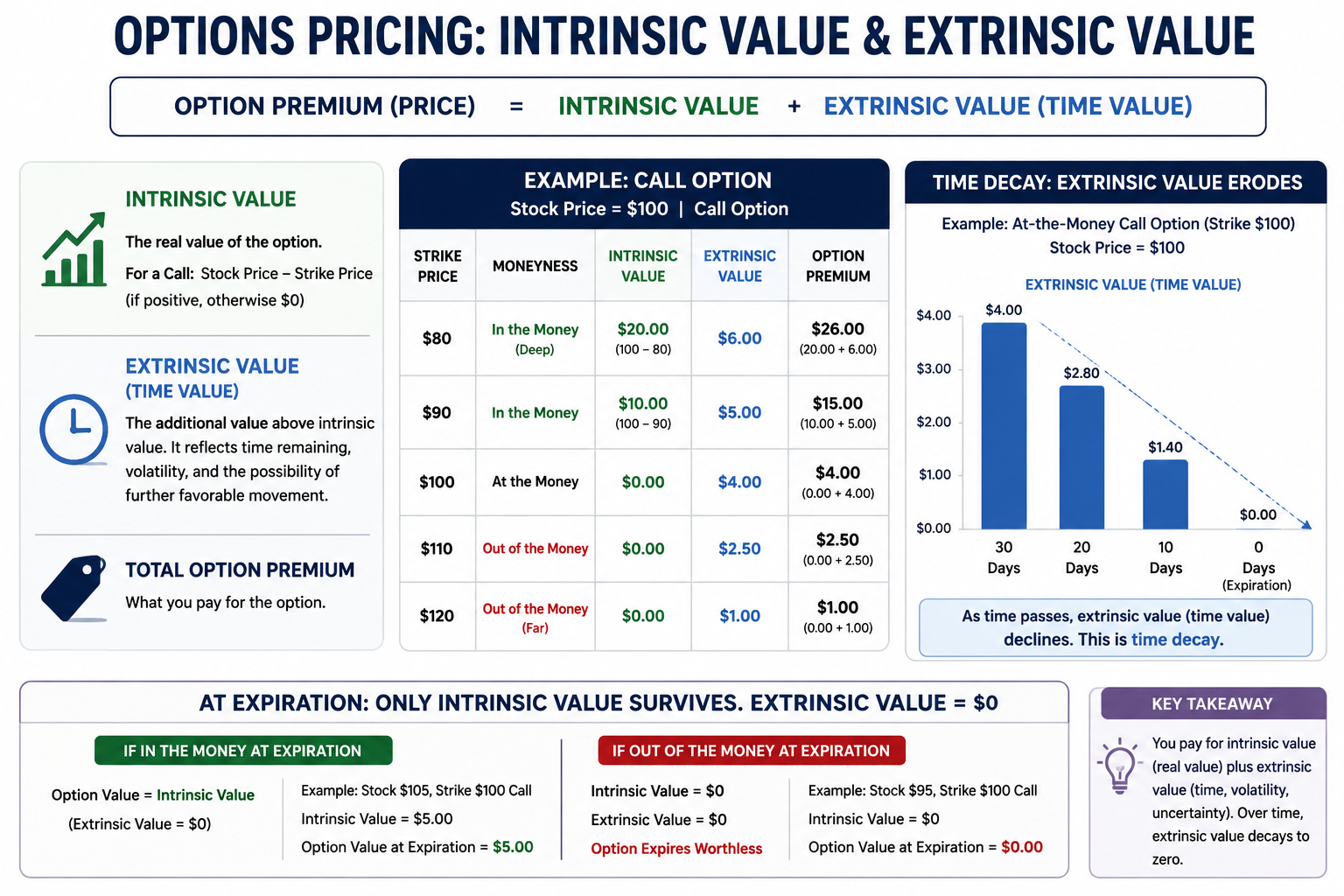

One of the most important concepts in options trading is understanding that an option’s premium consists of two separate components: intrinsic value and extrinsic value. Intrinsic value is the “real” value already embedded in the contract. For example, if a stock is trading at $120 and a trader owns a $100 call option, that option already possesses $20 of intrinsic value because they have the right to buy the stock $20 below the current market price. Extrinsic value, by contrast, is everything beyond that intrinsic value. It represents time, uncertainty, volatility, and the possibility that the stock could move even further before expiration. In practical terms, the market is assigning value not only to where the stock is today, but also to what could happen tomorrow.

This is where time decay quietly becomes one of the most powerful forces in the entire options market. Every option contract comes with an expiration date, which means time itself is constantly disappearing. As each day passes, a portion of the option’s extrinsic value erodes. The closer the contract moves toward expiration, the faster this decay accelerates. A useful way to think about this is that extrinsic value is essentially the “hope premium” embedded inside the option. It reflects the market’s belief that additional movement could still occur before the clock runs out. But that hope cannot survive forever because expiration eventually removes all remaining uncertainty from the equation. At that moment, the market no longer cares what the stock might do next week or next month. The only thing that matters is where the stock is trading right now.

That is why, at expiration, only intrinsic value survives. Extrinsic value always falls to zero. If a call option finishes in the money, its value at expiration consists entirely of intrinsic value. Using the earlier example, if the stock closes at $120 and the strike price is $100, the option settles with exactly $20 of value remaining. But if the stock closes below the strike price, the option expires worthless because there is no intrinsic value left to preserve. This dynamic explains why experienced options traders constantly monitor not only price direction, but also time remaining until expiration. In the options market, the passage of time is not neutral. It is an active force steadily transferring value away from buyers and toward sellers every single day.

If I were explaining to a new trader how to buy naked call options, the very first thing I would emphasize is that options are not simply “cheap stock substitutes.” They are time-sensitive contracts whose value is influenced by price movement, volatility, and the passage of time simultaneously. That distinction matters enormously because many traders enter the options market believing they only need to predict whether a stock will rise. In reality, successful call option buying requires understanding not only direction, but also timing and probability.

One of the most important concepts to master early is that every option contract comes with an expiration date. Unlike owning stock, where time can theoretically work in your favor indefinitely, call options are deteriorating assets. Every day that passes reduces a portion of the option’s extrinsic value through time decay. As a result, the stock must not only move higher, it must do so before expiration arrives. Many investors correctly identify a strong company or long-term trend and still lose money because the move occurred too slowly. This is why experienced options traders pay close attention to expiration cycles, time remaining, and the expected speed of a move.

I would also want a new trader to fully appreciate the power and danger of leverage. A single option contract controls 100 shares of stock while requiring only a fraction of the capital needed to purchase those shares outright. This creates the possibility for substantial percentage gains when the trade works favorably. But leverage cuts both ways. Because the option premium itself can fluctuate dramatically, relatively small moves in the underlying stock can create very large gains or losses in the option. This is why position sizing and capital allocation become essential disciplines rather than optional considerations.

Another foundational lesson involves understanding intrinsic value and extrinsic value. Intrinsic value represents the real economic value already embedded inside the option. Extrinsic value represents the additional premium associated with time remaining, volatility, and future uncertainty. At expiration, all extrinsic value disappears completely. Only intrinsic value survives. This means that option buyers are constantly fighting a clock that is steadily eroding a portion of the contract’s value every single day. Understanding this dynamic explains much of how options pricing behaves in the real world.

Volatility is another critical component that many new traders initially underestimate. During periods of elevated uncertainty, option premiums can become extremely expensive because implied volatility is incorporated into pricing. Earnings announcements are a classic example. A trader may correctly anticipate that a stock will rise following earnings and still lose money if the implied volatility collapses afterward. Professional traders therefore evaluate not only directional conviction, but also whether volatility itself is relatively expensive or inexpensive before entering a position.

Most importantly, I would want a developing trader to understand that buying naked calls is not, by itself, a complete strategy. It is a directional tool. Professional options traders think in terms of probability distributions, risk exposure, expected movement, and portfolio construction. Before placing a trade, they ask:

- How much can I lose?

- How quickly does the stock need to move?

- How much time do I have?

- Is implied volatility elevated?

- What is the probability this option expires worthless?

Those questions could be the difference between speculation and structured risk management.

Ultimately, successful options trading is about understanding the relationship between price, time, volatility, leverage, and probability, and learning how those forces interact before the expiration clock runs out.

Understanding these concepts is how Options Mastery is achieved. Remember there are four options building blocks that need complete understanding. They are:

Buying calls

Buying Puts

Selling Calls

Selling Puts

My suggestion is to take the time to understand each quadrant individually. In this series we will explore each component in thorough detail. Afterwards we will continue by illustrating the power and advantage of learning how to mix and match the different quadrants.

Below is an interactive Call Options Payoff Calculator which allows you change the inputs and clearly see a theoretical risk/reward profile of the trade. By simply interacting and changing any or all of the values, you will graphically see a hypothetical risk, the theoretical reward, and the potential break even price and the number of days before the option expires. This simple tool can allow a trader to understand the basic principles around potential risk and reward very clearly before entering into the trade.

Long Call Payoff Calculator

Change the inputs below to update the chart and worksheet.

Long Call Payoff Worksheet

This worksheet updates from the same inputs as the chart. Values are shown in stock-price points, not total contract dollars.

| Stock Price at Expiration | Option Value at Expiration | Net Profit / Loss in Points |

|---|

The blue line shows profit or loss at expiration in stock-price points. Below the breakeven price, the trade loses value. Above the breakeven price, the trade profits point-for-point with the stock.

Disclaimer: The Call Options Payoff Calculator shown above is an educational illustration created by the author for this article. It is not a Vantagepoint AI product, feature, or service, and it does not generate forecasts, signals, or trade recommendations. All values, scenarios, and outcomes displayed are entirely hypothetical and intended solely to demonstrate the basic mechanics of a call option. This tool should not be used to place, plan, or evaluate actual trades. It does not account for real market conditions, commissions, slippage, bid ask spreads, changes in implied volatility, dividends, early assignment risk, or any of the other factors that affect actual options trading outcomes. Options trading involves substantial risk and is not suitable for every investor. Hypothetical examples are not indicative of future results. Always consult a qualified financial professional before making any trading or investment decision.

Every trader lives with risk. The only question is whether that risk is understood before the trade is placed or discovered afterward when the market delivers an unpleasant surprise.

Many stock investors comfort themselves with stop losses. And stop losses can certainly be useful. But markets do not move politely in straight lines. Stocks gap. News breaks overnight. Earnings disappoint. Panic spreads. A stock closes at $100 and opens the next morning at $82. In those moments, theoretical risk management collides with reality. The market does not ask where your stop was placed.

This is where options become extraordinarily powerful.

With options, risk can often be defined in advance with remarkable precision. Before entering the trade, the investor can know exactly how much capital is exposed and exactly how much is at stake. The risk is not vague. It is not estimated. It can be carved in stone. That ability to structure exposure is one of the great advantages of options trading and one of the primary reasons sophisticated traders and institutions rely upon options so heavily.

Because in the end, successful trading is not about eliminating risk. That is impossible. Successful trading is about understanding risk, controlling risk, and accepting only the level of risk that makes sense for the potential reward.

Another foundational lesson involves understanding intrinsic value and extrinsic value. Intrinsic value represents the real economic value already embedded inside the option. Extrinsic value represents the additional premium associated with time remaining, volatility, and future uncertainty. At expiration, all extrinsic value disappears completely. Only intrinsic value survives. This means that option buyers are constantly fighting a clock that is steadily eroding a portion of the contract’s value every single day. Understanding this dynamic explains much of how options pricing behaves in the real world.

Volatility is another critical component that many new traders initially underestimate. During periods of elevated uncertainty, option premiums can become extremely expensive because implied volatility is incorporated into pricing. Earnings announcements are a classic example. A trader may correctly anticipate that a stock will rise following earnings and still lose money if the implied volatility collapses afterward. Professional traders therefore evaluate not only directional conviction, but also whether volatility itself is relatively expensive or inexpensive before entering a position.

Most importantly, I would want a developing trader to understand that buying naked calls is not, by itself, a complete strategy. It is a directional tool. Professional options traders think in terms of probability distributions, risk exposure, expected movement, and portfolio construction. Before placing a trade, they ask:

- How much can I lose?

- How quickly does the stock need to move?

- How much time do I have?

- Is implied volatility elevated?

- What is the probability this option expires worthless?

Those questions are the difference between speculation and structured risk management.

Ultimately, options trading is not simply about predicting whether a stock will rise. It is about understanding the relationship between price, time, volatility, leverage, and probability, and learning how those forces interact before the expiration clock runs out.

Understanding these concepts is how Options Mastery can be achieved. Remember there are four options building blocks that need complete understanding. They are:

Buying calls

Buying Puts

Selling Calls

Selling Puts

My suggestion is to take the time to understand each on individually. In this series we will explore each in thorough detail. Afterwards we will continue by illustrating the power and advantage of learning how to mix and match the different quadrants.

Most traders spend years searching for the perfect strategy.

But the strategy itself is rarely the deciding factor.

The real difference between profitable traders and struggling traders is usually determined before the trade is ever placed. It is determined by the quality of the decision behind the trade.

A simple call option, properly understood, offers extraordinary advantages. It can improve capital efficiency. It can define risk with precision. It can provide substantial exposure to a stock without requiring the same capital as purchasing shares outright. But even the finest strategy will fail when applied against the wrong trend, in the wrong market, or at the wrong moment.

This is where VantagePoint AI changes the equation.

Most traders rely upon instinct, headlines, opinions, or delayed information. VantagePoint AI was built to do something very different. It analyzes the relationships between markets, identifies emerging trends, and helps forecast direction before the move becomes obvious to the crowd.

That distinction matters enormously.

Because the objective is not merely to place trades.

The objective is to place trades when the probabilities appear to be aligned in your favor.

If you remember only one idea from this discussion, remember this:

The purpose of options trading is not to make you rich quickly.

It is to help ensure that no single mistake can prevent you from becoming wealthy at all.

That is the philosophy behind intelligent speculation.

Not reckless leverage.

Controlled leverage.

Not gambling.

Structured opportunity with clearly defined risk.

This is why sophisticated traders are obsessed with clarity. They want defined exposure. They want disciplined execution. They want a process that removes emotional decision-making at the exact moment emotions become most dangerous.

And that is precisely the role VantagePoint AI was designed to serve.

VantagePoint’s AI does not panic.

It does not hesitate.

It does not move stops because of fear or chase trades because of greed.

It evaluates probabilities objectively and helps traders remain aligned with the market’s dominant trend before emotion interferes with execution.

Which means the trader is no longer reacting emotionally to headlines, volatility, or fear.

They are positioning intelligently.

VantagePoint AI has one mission:

To help keep traders on the right side of the right trend at the right time.

It filters noise.

It removes distraction.

And it provides a forward-looking perspective on where strength may be building and where risk may quietly be increasing beneath the surface.

VantagePoint AI is not designed to replace traders.

It is designed to improve the quality of their decisions.

In our free live online trading masterclass, you will see exactly how experienced traders use VantagePoint AI to forecast trends, identify high-probability opportunities, and apply strategies such as learning to buy call options with greater precision and discipline.

You will see real examples.

Real forecasts.

Real market relationships.

No hype.

No exaggerated promises.

Just a clear demonstration of how machine learning can help traders make more informed decisions under uncertainty.

If you are curious, attend the class and judge it for yourself.

Because there is an enormous difference between guessing…

…and knowing where probabilities may already be shifting in your favor.

Reserve your seat for the live masterclass today.

It is not magic.

Its machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.