[fusion_builder_container hundred_percent=”no” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” overlay_color=”” video_preview_image=”” border_color=”” border_style=”solid” padding_top=”” padding_bottom=”” padding_left=”” padding_right=”” type=”legacy”][fusion_builder_row][fusion_builder_column type=”1_1″ layout=”1_1″ background_position=”left top” background_color=”” border_color=”” border_style=”solid” border_position=”all” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” center_content=”no” last=”true” min_height=”” hover_type=”none” link=”” first=”true” border_sizes_top=”” border_sizes_bottom=”” border_sizes_left=”” border_sizes_right=”” type=”1_1″][fusion_text]

Retirement Hyperinflation: Developing an Investment Thesis

I have spent the better part of my life looking for answers. While it is humbling to admit, I recognize now that while I was still learning, the questions I was asking were ineffective and not valuable.

When your attention is on the wrong question, it is complicating the puzzle you are trying to solve.

Recently, I was talking with an old friend of mine who was sharing with me their experiences of trading the markets in October 1987 during Black Monday when the stock market fell 22% in one day.

This is what he told me.

When Black Monday occurred, most brokers were shell-shocked at the carnage that had occurred. The market had been trending downwards for two months. Everyone in the business thought that the market would continue lower but very few people thought that the market would lose 22% of its value in one day.

All day long watching the prices go lower and lower was quite depressing.

At about noon he started asking himself the question….”Where is that money going to go?”

It was not going into Gold, Silver, Platinum.

It was not flowing into foreign currencies.

At about 2:15pm on that fateful day, the question became, “where does scared money go?”

And with that simple question the answer became obvious.

He concluded that all those shell-shocked stock traders would pour all their assets into the security offered by full faith and trust of the US government. U.S. Treasury Bonds were yielding 8% at that time. The trade was obvious. Traders who had just lost 22% in one day would pour their money into treasury bills and bonds.

Bonds closed at 3:00pm so he only had 45 minutes to contact his customers and make his excited recommendation:

“I am suggesting that we buy out of the money call options on the US Treasury Bonds. You’ll know right away if I am wrong on right. If I am right, I think we might 10x on this trade. If we are wrong, you will probably lose 50% before the week is out.”

A handful of clients agreed with his recommendation.

The outcome was that a $500 investment turned into $6,000 in a few days. This still stands as one of the most memorable and successful trades of his career.

The catalyst for that trade was a very focused and appropriate question.

The answer was obvious once the correct question was asked.

Often, one of the most important parts of trading is developing an investment thesis. An investment thesis serves as a guide in choosing trades that agree with your objectives, risk tolerance, and understanding of the current economic landscape. In other words, it’s like a game plan.

This thesis can involve a very short or much longer time frame. At its core the thesis tries to answer the question as to what the opportunity is and what are the risks by providing as much pertinent detail as possible.

While this sounds like an intellectual exercise, it is quite practical. At its core, you minimize the theory and really drill down and focus on “where the money is being made, and why.” Sometimes an investment thesis is very difficult to construct because of the amount of uncertainty in the world. At other times, it is the most obvious thing in the world.

Let me provide a current example of an investment thesis, my “Retirement Hyperinflation Thesis.”

Please look at the chart below of the Ten-Year Government Bond Yields for the last 10 years.

In 2007 one year before the Financial Crisis if you invested one million dollars into the ten year treasury it would yield 5% or $50,000. This is how many couples approached retirement. This $50,000 figure is actually quite frugal for anybody planning their retirement.

However, in 2011 when yields hit 3%, trying to get that same $50,000 annual cash flow would now require that you invest $1,666,666. In other words, over a period of 4 years trying to maintain a $50,000 cash flow cost 66.66% more!

A few months later in 2012 when yields hit 2%, you would now require to invest $2,500,000.00 to achieve that same $50,000 annual cash flow. This represents an increase of 150% from just 5 years earlier.

As I write these words, the 10 year bond is yielding .78%. If you wanted to achieve a $50,000 annual cash flow you would be required to invest $6,410,00 to accomplish that same objective. This is a 541% increase in the cost of retirement over a 13 year period.

You have witnessed hyperinflation in the retirement market. The problem is that the only people aware of this have been financial planners trying to structure retirement plans for their customers and people hoping to retire. This is one of the casualties of the Federal Reserve’s persistent Quantitative Easing of the last 12 years.

It is not that retirement has been outlawed, but that one of the largest markets in the world which symbolized the full faith and credit of the U.S Government has been decimated by the Federal Reserves persistent interest rate manipulation.

What makes the situation more tragic though is that if you invested the same one million dollars in bonds today your coupon of .78% would yield an annual cash flow of $7,800.00 which is 84% less of a cash flow than what you could have achieved 13 years earlier.

This is noteworthy and central to any investment thesis you develop moving forward. Why? Because the Federal Reserve has announced that they are targeting a 2% inflation rate. Who is going to invest and accept a negative annual return on their bonds?

They key question for all of those trillions of dollars in U.S. Treasuries is the exact opposite of what it was in October 1987.

Where are all those funds going to go?

Where does scared money run to when the YIELD FIELD has been decimated?

Money is what moves markets. Since the worldwide bond market size is over $100 trillion this is by far the most important question and development that all traders and investors have to confront moving forward.

There are only five alternatives:

Cash? Some will choose cash because it is the easiest solution. But it is also most prone to the risk of loss of purchasing power due to inflation. In third world countries, banks often pay a very high interest rate on your deposits. The problem is that the interest rate is always less than the inflation rate. What good does it do you if your bank is paying you 80% annual interest if the currency is debased or devalued 85%? The financially illiterate always keep their wealth in cash and it never ends well for them. Cash is not a viable solution if you agree with the facts of presented by the Retirement Hyperinflation Thesis.

Real Estate? Traditionally Real Estate has been a tremendous store of value around the world. The problem I see with Real Estate moving forward is that in that a higher than normal unemployment rate is affecting a tenant’s ability to make regular rent payments. A year ago, nobody would’ve thought that in 2020 there would be over 40 million unemployed Americans. Real Estate can be a place where some money will flow but between the management fees and economic uncertainty the opportunity to earn yield today is questionable.

Gold? Traditional investors hate gold because it does not pay interest. But, as I have pointed out in my other columns, if you purchased Gold in 1971 when we came off the Gold standard, you would be up 5400% which is far more than any other index or investment. The Dow on the other hand over the last 49 years is up roughly 2985%. The smart money always places a good portion of their wealth in gold. It can be problematic to store and secure, but history shows that it maintains its purchasing power. So, we can assume that a percentage of those bond funds unable to earn yield will find a home in the Gold market.

Bitcoin? While bitcoin has proven the best performing investment of all time, it is not for everyone. To successfully invest in bitcoin requires a preliminary education in understanding what digital assets and “digital scarcity” are and the custodial steps that are required to safely secure your investment. Bitcoin has proven to be a wonderful store of value and in my opinion every portfolio should consider holding 2% of their net worth in this asset. You can read more about my perspective on bitcoin here, here and here. While Bitcoin will attract some attention from those interested in maintaining purchasing power, it is a smaller asset class and the relatively new kid on the block. Assuming my “Retirement Hyperinflation Thesis” is accurate money will flow into this asset class as well from people all over the world who are looking to preserve their purchasing power.

Stocks? 2020 has been a year of incredible chaos and uncertainty.

We have witnessed:

- a global pandemic

- government-mandated shelter-in-place orders

- an economic shock that caused a liquidity crisis

- the largest monetary stimulus package in history

- and one of the fastest recoveries on record for asset prices coming out of a recession

This has all occurred against the backdrop of a presidential election, and this was just the first 9 months of the year.

As we move ahead traders are aware that the European Central Bank is echoing the Federal Reserves policy that they are also looking at at least a 2% inflation target.

How have the markets fared through all this volatility? A picture paints a thousand words and corroborates what I am implying in the Retirement Hyperinflation Thesis.

The chart shows you the year to date comparative performance of Bitcoin, Gold and the S&P 500.

You can clearly see that all three markets appear to be very strongly correlated this year. Bitcoin has been by far the best overall performer and the most volatile. Gold has been the least volatile and stocks have climbed above the beginning of the year levels. These are the results when the Fed manipulates the most important metric in capitalism – interest rates which represent the cost of money.

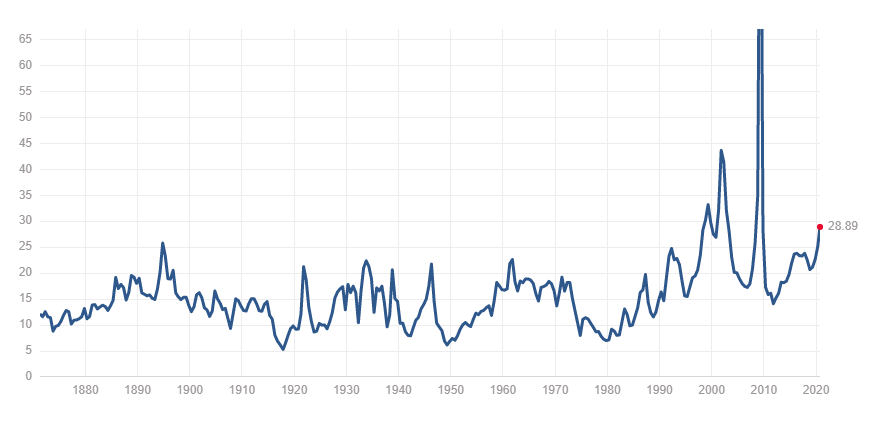

We are in an environment where we have the lowest interest rates in the history of the free world and commission free brokerage rates. Throw in all of the economic uncertainty and we have a recipe for continued massive volatility. Here is a chart of the S&P 500 Price to Earnings Ratio for the last 100 years and you can see that we are normal valuation levels are an era of another time in history. The two previous spikes are the dotcom bubble bursting in 2000 as well as the Great Financial Crisis Bubble.

The S&P 500 has performed well this year only because of the FANG stocks which have been up over 40%.

- Apple

- Netflix

- Microsoft

- Amazon

- Nvidia

The rest of the S&P 500 has lagged very much behind these stellar performers.

Every trader and investor have been affected by the “Retirement Hyperinflation Thesis.” Clearly a buy and hold mentality is very precarious and risky in today’s economy. Recently I listened to an interview of a Financial Treasurer who managed a balance sheet of several billions of dollars. He commented that his company made about $50 million in net profits every year but had $500 million of cash on their balance sheet. He was deeply offended by the reality that if he stayed in CASH, due to the current Federal Reserve policies he would witness the evaporation of 2% of his companies reserves purchasing power which equated to $10 million dollars. He felt that the Fed was literally twisting his arm and forcing him to do one of three things with his cash:

- Buy back his company stock

- Buy Gold

- Buy Bitcoin

Regardless of your risk profile these are the only legitimate alternatives facing every investor and trader today.

So how are you going to navigate the terrain of the financial markets?

The race to debase is very real. This economic environment is forcing traders into much shorter time frames as everyone in the marketplace chases yield.

Real asset prices will keep rising as the yield chase intensifies. Cheap capital will keep flooding the market. And our economy will continue its addiction to a horrible monetary stimulus drug that is being handed out like candy in Washington DC.

Do you have the tools and ability to find the strongest trends at right time in this economic environment? What is your plan for maintaining your purchasing power as this trend accelerates?

I’d like to invite you to visit with us at one of our live Master Class Webinars where we show how artificial intelligence is the only means to stay consistently up to date on the risk and reward opportunities in this environment.

What all traders and investors want is an accurate, proven solution that alerts you when a high probability trend is unfolding. The Vantagepoint A.I. forecasts have proven to be up to 87.4% accurate in determining the trend three days in advance.

Visit With US and check out the a.i. at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]