There are only two ways a government pays its bills. It can tax you now or borrow from you and tax you later. The United States prefers to do both at the same time… then debate it on television. For decades, this worked because the world willingly financed the system. That willingness was not accidental.

It was built on the petrodollar system. Oil was priced in dollars, trade flowed through dollars, and those dollars recycled into U.S. Treasuries. It created automatic demand for U.S. debt and turned financing into a global habit. The U.S. got funding, the world got liquidity, and the system fed itself. It felt permanent, which is usually when systems begin to break.

And now it is breaking. The petrodollar system is no longer intact, it is fractured. Trade is diversifying, capital is becoming more selective, and alternatives are no longer theoretical. What was once structural demand is now optional demand. That is a fundamental shift.

At the same time, inflation has moved from theory into reality. It shows up in daily life and in every investment decision. When purchasing power erodes, fixed income becomes harder to justify. A so-called “risk-free” bond starts to resemble a guaranteed slow loss. Investors begin asking harder questions.

The most important one is simple. Why lend long-term money to a borrower who can print the repayment currency? The old answer was obligation. The new answer is choice. And once choice enters the system, competition follows immediately.

Which brings us to the fork in the road. There are only two paths forward. Either the United States redesigns Treasuries to compete for global capital… or all roads lead back to the money printer. One path earns demand. The other manufactures it.

If demand is no longer automatic, it must be earned. Not with messaging, but with incentives that make capital stay. This is where the conversation shifts from policy to design. The future of Treasury demand will need to be engineered, not assumed.

And that design still comes down to three levers: Improve real returns, reduce friction, and add strategic incentives. Pull those correctly and capital flows in. Ignore them and capital leaves without hesitation. Markets are not patriotic, they are practical.

For years, markets operated on a simple belief. When conditions deteriorate, policymakers provide liquidity. This response became predictable, then expected, then embedded. Asset prices recovered repeatedly, reinforcing confidence in intervention. Eventually, markets stopped questioning whether support would arrive.

That shift changed behavior. Risk was not eliminated; it was repriced under the assumption of rescue. Capital flowed toward assets expected to be supported. The question became less about value and more about protection. Markets started pricing policy as much as fundamentals.

But all support mechanisms trace back to one reality. The United States must fund itself. If Treasury demand is strong, liquidity flows smoothly through the system. If demand weakens, the burden shifts inward. What was once external funding becomes internal support.

That shift has consequences. Financing becomes monetization. Voluntary demand becomes manufactured demand. And the Federal Reserve becomes the buyer of last resort. The system still functions, but confidence begins to erode.

Liquidity can stabilize prices, but it cannot permanently restore trust. That is the key difference today. The issue is not whether the system can print. It is whether printing can replace genuine demand. And increasingly, markets are questioning that assumption.

There are moments in markets when a chart stops being a chart and starts becoming a message.

This is one of those moments.

A five-year view of the U.S. Treasury market tells a story that is difficult to ignore and even harder to explain away. The overwhelming majority of buyers over that period are now underwater. Not marginally. Structurally. What was once considered the safest asset in the world has quietly delivered losses to those who treated it as a store of stability. That is not a technical anomaly. It is a signal.

And yet, the more revealing detail is not buried in the past. It is unfolding right now.

Traditionally, when risk assets come under pressure, capital rotates into Treasuries. It is one of the oldest reflexes in modern finance. Stocks weaken, volatility rises, and money seeks safety in the full faith and credit of the United States government. That relationship has been reinforced across decades of crises, corrections, and geopolitical uncertainty.

But that is not what is happening.

Since the escalation of conflict with Iran, one would reasonably expect even a modest bid in Treasuries. Not a surge. Not a flight to safety. Just a recognition of their role in the hierarchy of assets. Instead, the most recent monthly candle tells a different story. Prices have pushed to new lows.

That divergence matters.

Because markets operate on two parallel tracks. What is happening. And what should be happening. Most of the time, those tracks move together. When they separate, it creates tension. And when that tension builds, it often resolves in ways that are both sudden and consequential.

This is one of those moments.

If Treasuries are not attracting capital during periods of uncertainty, it raises a more fundamental question. What, exactly, is the market seeking for safety? Because if the traditional safe haven is not behaving like one, then the definition of safety itself may be changing.

That is not a small shift. That is a structural one.

For traders, this is where discipline matters. Not opinions. Not narratives. Observations. The market is signaling, clearly and persistently, that demand for Treasuries is not what it once was. The price action reflects it. The trend confirms it.

And trends, particularly in markets as large and consequential as U.S. Treasuries, rarely move without reason.

This is not about predicting what comes next. It is about recognizing what is already here.

Because until the Treasury market begins to show sustained strength, until it reclaims its role as a destination for capital rather than a source of losses, the message remains unchanged.

Something beneath the surface is not functioning the way it used to.

And markets often tell you the truth long before anyone is willing to say it out loud.

Money moves with precision. It flows to where it is treated best. Not where it is directed, but where it is rewarded and protected. Today, capital has options across asset classes and geographies. That reality changes the competitive landscape.

Treasuries now compete with commodities, gold, Bitcoin, and inflation-resistant equities. Each offers a different form of protection or upside. Capital evaluates these choices constantly. It does not wait for permission.

So, Treasuries must evolve. The same three levers still apply. Improve real returns so investors keep more of what they earn. Reduce friction so ownership is seamless. Add incentives that go beyond yield.

Every viable solution fits inside that framework. There is no fourth lever hiding somewhere. Get those right and demand rebuilds. Get them wrong and capital reallocates elsewhere.

Start with tax advantages. Investors care about after-tax, after-inflation returns. Municipal bonds proved this decades ago. Lower yields become acceptable when what you keep is protected. That principle still holds.

Apply that logic to Treasuries. Make interest structurally tax-free and credible over time. Then layer in inflation protection and commodity linkage. Now the instrument evolves beyond a traditional bond. It becomes a store of value inside the system.

This changes investor behavior. The question shifts from yield comparison to capital preservation. Treasuries begin competing on purchasing power instead of nominal return. That is a stronger position in an inflation-aware world.

When policy aligns with real investor priorities, demand follows naturally. Not because it is forced, but because it makes sense. Capital does not need persuasion when incentives are clear. It responds automatically.

Next comes strategic alignment. The global economy still runs on energy and commodities. Aligning Treasuries with those flows strengthens their relevance. Commodity-linked yields create built-in hedging characteristics. This ties debt instruments to real economic activity. Then expand incentives beyond yield. Direct tax credits tied to Treasury ownership change behavior quickly. Corporations, sovereign funds, and allies respond to measurable advantages. Participation becomes strategic, not just financial.

Finally, address the reality of digital competition. Bitcoin represents scarcity and optionality in a way traditional assets do not. Ignoring it does not reduce its influence. Integrating it changes the equation.

Bitcoin-enhanced Treasuries introduce asymmetry. Investors gain stability with a layer of upside. That appeals to capital already moving outside the system. It transforms Treasuries from static instruments into adaptive ones.

All these ideas reflect a single shift. Demand is no longer structural, it is competitive. Capital is mobile, informed, and selective. It evaluates real returns, not stated intentions. And it reallocates quickly when conditions change.

The United States is no longer the default destination. But it must become the preferred one. That requires alignment with how capital behaves. Not how policy assumes it behaves.

This is the transition from forced demand to earned demand. It is not theoretical; it is already happening. And it is redefining how the system funds itself.

For traders, this is not background noise. It is the core driver of capital flows. Changes in Treasury demand ripples through every major market. Yields move, currencies adjust, and equity valuations respond. Sector leadership follows those shifts.

These are not isolated effects. They are transmission mechanisms. Understanding them provides an edge. Ignoring them creates blind spots.

The takeaway is straightforward. Watch where incentives are strongest. That is where capital will go. And capital, more than any narrative, determines market direction.

Repatriation of capital sounds complicated, but it is not. It is money leaving one place to defend another. Investors sell what they can to protect what they must. Sometimes it is a choice. Often it is not. When pressure builds, capital moves up the food chain toward safety, liquidity, and survival.

This is how cracks turn into breaks. In 1998, Long-Term Capital Management was forced to unwind positions when leverage met reality. In 2008, funds and banks sold anything liquid to meet obligations as the financial system seized. In March 2020, even U.S. Treasuries were sold in a dash for cash as institutions scrambled for dollars. Each time, the same pattern appeared. Selling accelerated, liquidity disappeared, and price moved faster than anyone expected.

At the center of it all is the margin call. It does not negotiate, it enforces. When it hits, positions are liquidated not because they are wrong, but because they must be sold. Strong assets get sold alongside weak ones. Correlations move toward one. And price stops reflecting value and starts reflecting urgency. That is the moment when markets remind everyone who is really in charge. Selling creates more selling as leverage unwinds. Liquidity disappears at the exact moment it is needed. Assets unrelated to the initial problem get pulled into the process.

This is where truth is revealed. Not in calm conditions, but in constraint. The margin call strips away theory and exposes reality. And in that moment, price tells the only story that matters.

Forget the politics.

Watch the incentives.

Money doesn’t care about speeches, press conferences, or carefully worded statements. It moves to where it’s treated best. Period. If Treasuries become attractive again, capital flows in and the system stabilizes. If they don’t, the gap gets filled the only way it always does. With printed money.

And here’s the part most people miss. You won’t need a headline to tell you it’s happening. You won’t need an expert panel to explain it after the fact. The market will show you in real time.

Because in the end, every decision, every delay, every shortcut…

Shows up in one place:

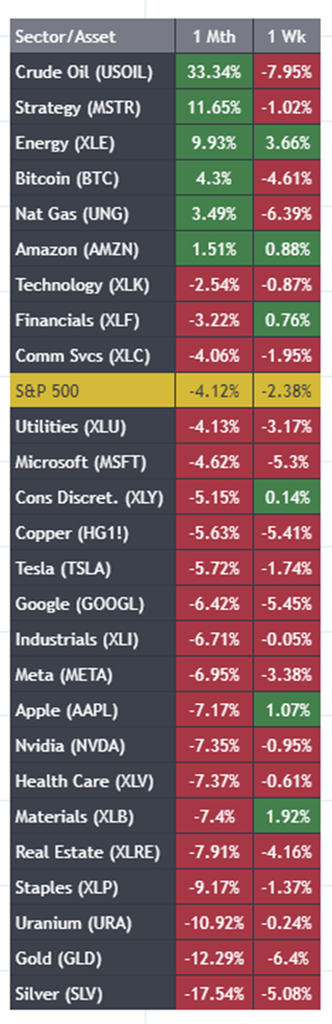

Over the last month, Crude Oil (USOIL) is up over 33%. Energy (XLE) is firmly positive. Strategy (MSTR) and Bitcoin (BTC) are holding gains. Meanwhile, the S&P 500 is down. Technology (XLK) is down. The so-called market leaders like MSFT, NVDA, GOOGL, and AAPL are all under pressure.

This is not a balanced market.

This is a divided market.

And in divided markets, confusion is expensive.

We live in an age where technology has made everything easier… faster… more accessible. But in trading, that convenience has created a new problem. You are no longer competing against individuals making decisions over coffee.

You are competing against algorithms.

Relentless. Tireless. Unemotional.

They scan thousands of markets simultaneously. They detect shifts in capital flow before they become obvious. And they act without hesitation.

This is precisely why so many traders feel out of sync. What “should” be happening no longer matters. What is happening is all that counts.

And right now, what is happening is clear:

Money is flowing into energy… and away from much of the rest of the market.

It is exactly this type of environment for which VantagePoint AI was created. It is built for markets where leadership is narrow, trends are fractured, and clarity is scarce.

The question is simple.

Are you reacting to the market…

Or are you seeing it clearly before the move unfolds?

We invite you to join a free live online masterclass: Learn How To Trade with VantagePoint AI.

You will see the AI in action. Discover how it identifies where money is actually flowing. And most importantly, you will learn how to separate facts from narratives in real time.

Because in markets like these, survival does not go to the smartest trader.

It goes to the most prepared.

And discover how to stay on the right side, of the right trend, at the right time.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.