Nvidia’s blowout earnings ushered in exactly what seasoned traders expected: a burst of enthusiasm and an immediate collapse in implied volatility. Yet it’s this specific intersection, where excitement collides with uncertainty, that demands the most discipline.

The headline numbers tempt traders to chase, but the more important question isn’t whether Nvidia can continue climbing. It’s how to participate in the unfolding story without overpaying for exposure. In moments like this, when the market collectively exhales, the edge shifts from prediction to structure. This is where professionalism is measured: in the ability to harness the narrative without succumbing to its emotional gravity

Here’s a 52-week chart of $NVDA:

The quarter delivered several unmistakable signals: data-center revenue accelerating at a pace typically reserved for early-stage disruptors, guidance moving faster than even the most bullish projections, and demand for cloud GPUs surpassing supply a rare position of pricing leverage in any industry. These aren’t simply “good numbers”; they recalibrate the psychology of the entire A.I. ecosystem. But compelling narratives create inefficiencies, and one of the most persistent is mispriced volatility in the aftermath of euphoria. It’s in that dislocation — between the story traders want to believe and the volatility the market has just shed — that real opportunity begins.

Nvidia’s earnings beat isn’t just a headline; it’s a signal about the market’s psychology. The company’s performance confirms that the A.I. boom still has structural momentum behind it; momentum that traders ignore at their own peril. But the market, as it often does, has already priced in part of the excitement. Implied volatility has deflated, enthusiasm is inflated, and the next move requires more precision than bravado.

The rational trader now faces a fork in the road: how to lean into strength without getting crushed by the very volatility collapse that follows every monster earnings print. The answer is not hope, it’s architecture. Well-built options structures, not directional impulses. Implied volatility is a multiplier on the price of uncertainty.

Nvidia didn’t just beat earnings, it slammed a gavel down on the whole A.I.-trade and said, “Court’s in session.” Revenue’s ripping, guidance is sprinting, demand’s climbing over itself, and suddenly the market must admit the unthinkable: sometimes momentum isn’t madness, it’s math… and still a little terrifying. Which leaves options traders in that classic post-earnings no-man’s-land, trying to ride the afterburner without getting flattened by the volatility hangover that always shows up the morning after.

The market walked into Nvidia’s earnings like a guy bracing for a bar fight that never happened, implied volatility jacked up, everyone pricing in disaster, and then… nothing. No catastrophe. Just a clean upside punch that sent implied volatility sliding off a cliff while conviction quietly tightened its grip. And that’s the sweet spot most traders never recognize: when you can pocket momentum and milk the decay of overcooked volatility at the same time. But here’s the part the amateurs miss, the options structure is the whole ballgame. Not the direction, not the drama, not the prediction. Get the structure wrong and you’re roadkill. Get it right and you could play both sides of the board like a grandmaster.

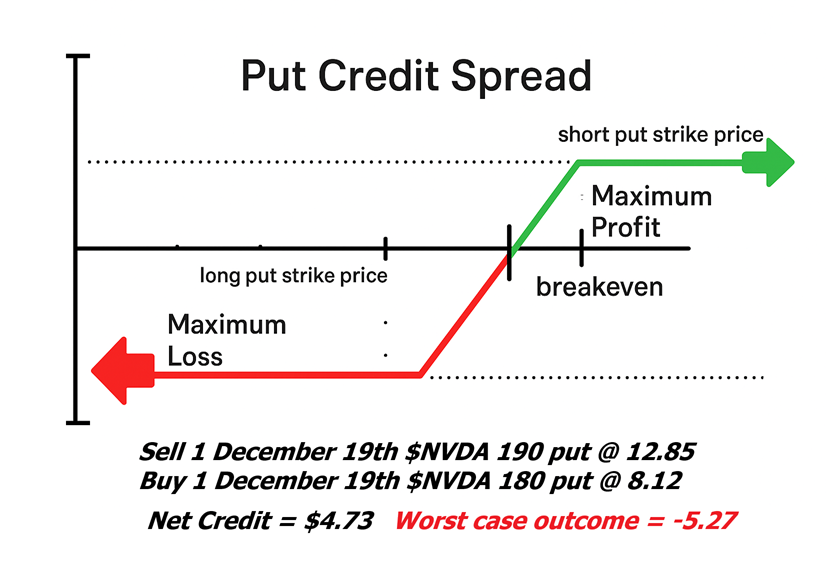

If Nvidia’s earnings underscored anything, it’s that markets often house fear and opportunity in the very same breath. In the aftermath of a major event, when the fundamental story still appears sound, one of the most grounded, almost architectural, approaches is the put credit spread. The idea is straightforward: sell a put spread while implied volatility remains elevated, capturing the premium that lingers after the uncertainty has passed. In effect, you allow the market’s residual anxiety to subsidize your strategy — turning short-term fear into usable capital. From there, allocate part of that premium into a deep out-of-the-money call several months out. The result is elegant: you effectively finance a long-dated upside wager with the remnants of post-earnings caution. Your long-term exposure becomes close to cost-neutral, a structurally funded moonshot, without venturing into reckless leverage.

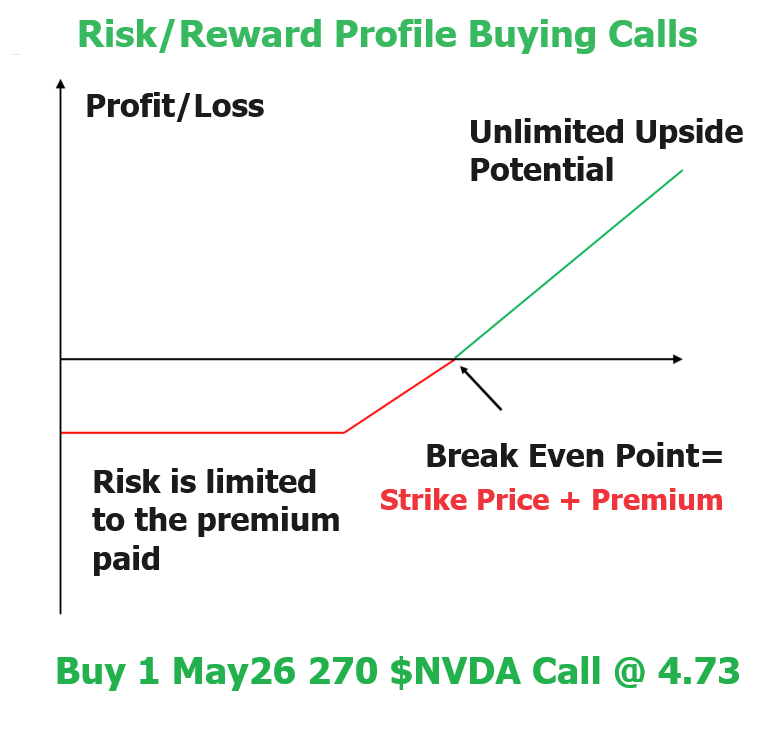

In markets as emotionally charged as Nvidia’s, the temptation is always to reach for short-dated calls and hope for a quick win. But the more disciplined approach, the one used by traders who think beyond the week, is almost the inverse. Instead of paying up for ephemeral upside, they begin by selling premium where fear is still mispriced. Elevated post-event volatility becomes a source of funding, not anxiety. The premium collected from a put credit spread effectively buys what traders need most: time. With that cushion in hand, they can step out the curve and acquire a deep out-of-the-money call several months out, transforming what might look like a speculative moonshot into a structured, asymmetric wager. It’s a way of participating in a potential multi-month melt-up without surrendering capital to theta decay. And, perhaps more importantly, it underscores the distinction that separates professionals from tourists: speculation is allowed, irresponsibility isn’t.

Here’s the beauty of this hybrid trade: Nvidia’s got the two ingredients every trader secretly prays for, volatility and momentum. The trick isn’t chasing the upside; it’s paying for it like you’ve got a functioning prefrontal cortex. So you start simple: sell a put credit spread under the levels the market already swears by, scoop up the premium, and let that cash do something useful.

Take it and buy a long-dated, way-out-there call — the kind of optionality that can turn a quiet melt-up into a personal fireworks show, all at a near-zero net cost. That’s the philosophy: the most elegant trades are the ones where the premium you earn subsidizes the premium you spend, where the market’s fear politely picks up the tab for your ambition. And in an age where everyone wants the future to be a yes-or-no coin flip, this little structure is one of the few that keeps paying even when the future refuses to cooperate.

This example is theoretical but the values, risk/reward profile and premium levels are all accurate.

Before a big news event, option premium doesn’t just “go up,” it swells like a balloon at a kid’s birthday party, and everyone’s holding their breath because they know it might pop. The market pumps in air — fear, rumors, guesses, worst-case scenarios — and that balloon stretches tighter and tighter as traders brace for whatever’s coming. That’s implied volatility: the crowd’s collective nerves priced into every contract. Nobody knows if the news will be a sparkler or a stick of dynamite, so they bid up options just to avoid being the sucker caught flat-footed. But the moment the announcement hits — good, bad, or boring — the balloon stops inflating, the tension whooshes out, and premiums deflate fast. It’s not magic. It’s just the marketplace charging top dollar for uncertainty… and dropping the price the second certainty walks in the door.

If you want the simplest, cleanest way to understand how implied volatility reacts to earnings and industry headlines, you don’t need a Ph.D. or a pricing model, you just need to look at one thing: the cost of the at-the-money straddle. That single number tells you exactly how much uncertainty the market is pricing in. When major news is pending — an earnings report, a regulatory announcement, a sector-shifting headline — traders perceive more risk, and options premiums rise accordingly. And we can see that dynamic at work right now. The December 19th $NVDA at-the-money call is trading at 8.05, while the matching at-the-money put is priced at 15.60, for a combined premium of 23.65. Divide that by Nvidia’s current price of 193.80, and you get roughly 12.2% — meaning the market is implying a double-digit move over that timeframe. Before earnings, that percentage was far lower. And typically, after earnings — once the suspense lifts and the uncertainty is resolved — that number contracts sharply. It’s a real-time window into how fear and expectation get baked into price.

Think of a put credit spread like running a tiny rental business on time itself — you’re collecting rent (the $4.73 credit) from traders who are afraid the market will misbehave before December 19. Your job? Lease out that fear while it’s expensive. When premium is high, it’s like tourist season: everyone’s paying top dollar for the same stretch of beachfront. Selling a put spread at that moment means you’re charging peak-season rates. And the deal is simple — if NVDA stays above $190, you keep the entire $4.73. That’s your max profit, your full “rental fee.” If NVDA collapses to $180 or lower, you take the hit and pay out $5.30 — the cost of being on the hook if the storm really does come. Everything between now and December 19 is just watching the clock and letting time decay work for you. The strategy is clean, bounded, and honest: you know the most you can make, you know the most you can lose, and you’re literally selling time when buyers are willing to pay the most for it.

To place this put credit spread, the trader must adopt a very specific and practical outlook on prices, not wildly bullish, not bearish, but calmly confident that NVDA will remain above $190 through December 19. This isn’t a bet on explosive upside; it’s a bet on stability. The trader believes that NVDA may wiggle, wobble, or even pull back, but it probably won’t sink below the $190 short strike, and it almost certainly won’t collapse all the way to $180, where the maximum loss occurs. This is a probability trade rather than a prediction trade, built on the mindset: “I don’t need NVDA to go up; I just need it to not go down too much.” It’s the equivalent of saying, “I’m not betting the horse will win the race — I’m betting it won’t fall off the track.” The entire trade hinges on one belief: NVDA’s price is statistically more likely to stay above the danger zone than to plunge into it. If a trader can adopt that expectation — not bullish bravado, just measured, probability-based confidence — then the credit spread makes clear strategic sense.

You’re looking at this particular put credit spread that pays you $4.73 upfront, and in the options world, that’s real money, cash in your pocket just for showing up. That’s your maximum reward: the market stays above $190, your short put expires worthless, and you walk away with every nickel of the credit. But don’t mistake this for a free lunch — the worst-case scenario is the market face-plants below $180. At that point, the spread widens to its full $10, and after subtracting your credit, you’re staring at a –$5.27 loss. Best case: easy money for being on the right side of market fear. Worst case: you pay $5.27 for betting the wrong level of support. It’s a simple trade with simple math — but like every good punch, you feel it whether you land it or take it.

When you look at just the first leg of this strategy — the put credit spread — it’s designed to win more often than not, provided your analysis on price levels is anywhere near correct. That alone allows you to consistently harvest premium in high-volatility environments. But the real brilliance of the approach isn’t in the credit spread itself; it’s in understanding that this is simply another way to harness massive volatility and turn it into usable capital. The true risk-management edge emerges when you take the premium you collected — the “rent” from selling December time — and use it to buy a deep out-of-the-money call out in May 2026 at a net cost of zero. You finance the entire calendar by letting short-term fear pay for long-term optionality. And this, as Warren Buffett would put it, speaks directly to his two most sacred rules: 1) Don’t lose money. 2) Don’t forget rule #1. This isn’t a promise of profit — nothing in trading ever is. It is, however, a fully risk-defined structure where the upside, downside, and time horizon are all cleanly marked. More importantly, the goal isn’t to nudge you into executing this on NVDA specifically. This is a portable tactic, which is usable in any market where volatility is elevated and premiums are inflated. It’s not about guessing the future — it’s about letting volatility pay for your opportunity to participate in it.

Look, the chart makes call buying look like a fantasy: limited downside, unlimited potential upside, clean diagonal line to the moon. And sure, technically that’s true. But here’s the part nobody prints on the brochure: most option buyers lose money. Not because they’re dumb. Not because they picked the wrong stock. They lose because they never understood the silent killer baked into every option contract — time decay. Theta doesn’t care about your dreams of glory. It grinds down the value of your call every single day, like a leak in the gas tank you can’t plug. So yes, buying calls comes with “unlimited profit potential,” but what good is unlimited potential if your option bleeds to death before the move ever happens? That’s where this strategy flips the script. You don’t pay for the call. You let the put credit spread do the dirty work first — harvest premium, book profit, and then use that captured credit to buy long-term opportunity way out on the calendar. Now you’re not risking with your own money. You’re letting the market’s fear finance your shot at the upside. That’s not recklessness — that’s risk management with teeth.

The idea of having limited risk and unlimited profit potential can be very risky if you don’t know what the trend or probabilities of success are! It’s no different than rolling the dice at the casino.

One of the often-overlooked realities of options trading is that you can be completely wrong in your market outlook and still avoid losing money; in some cases, you can even be wrong and still turn a profit. But these outcomes aren’t accidents; they are the product of understanding how options truly work. They emerge only when traders take the time to study the mechanics of premium, the obligations that come with selling it, and the strategic structures that transform volatility into opportunity. Options reward creativity and discipline in equal measure — but only for those willing to learn the playbook.

The headline takeaway from yesterday’s $NVDA earnings call was simple: the company is still printing money at an extraordinary pace. Nvidia generated $57 billion in revenue last quarter, up 62% from a year ago, a number so large it almost obscures the conversation around risks. Jensen Huang was quick to argue that these results prove the fears of an “A.I. asset bubble” are overstated, insisting that the demand for accelerated computing is both real and durable. And on the surface, that reassurance is compelling. Nvidia’s numbers continue to defy gravity, suggesting the company is operating in its own category entirely.

But that narrative is, by definition, one-sided. Nvidia’s success doesn’t automatically guarantee the financial health of the companies buying its products. Corporations pouring billions into A.I. infrastructure still face the responsibility of proving those investments translate into profits and that’s a story Jensen Huang cannot tell for them. This is where Wall Street’s more cautious voices are looking back to the dot-com era for context. In 2000, the refrain was “this time is different,” because the internet fundamentally changed reach, engagement, and connection. That was true and it still didn’t prevent the dot-com bust. The collapse wasn’t driven by technology failure; it was driven by companies burning cash and valuations outrunning reality. Today’s A.I. cycle may be built on more solid demand, but the underlying question remains the same: can the buyers of this technology ultimately justify what they’re spending? Until that answer becomes clearer, Nvidia’s extraordinary results tell only half the story.

I hope you’re beginning to see the quiet little trap that catches so many options traders by the ankle. On one side, you have the seductive promise of “limited risk” and “unlimited profit potential.” Sounds thrilling, doesn’t it? But without a firm grip on the trend, without knowing the probabilities, that kind of thinking is just casino logic dressed up in financial jargon. It’s rolling dice and praying for sevens.

On the other side, you have strategies that look far less glamorous… trades where the reward is capped, defined, even modest. And yet, these are the trades that could quietly win repeatedly because they stack the odds in a trader’s favor. They’re the difference between hoping for windfall miracles and engineering high-probability edges.

These are the kinds of insights we unpack — deeply, clearly, profitably — in our Free Live Trainings, where traders learn how to harness the power of artificial intelligence and finally break free from guesswork. If you’ve ever wondered how elite traders stay on the right side of the right trend at exactly the right time… this is where they learn how. A.I. becomes your sleepless, relentless trading ally — scanning markets, sniffing out patterns, crunching probabilities, and illuminating opportunities that ordinary tools never reveal.

Let me be blunt. Trading with VantagePoint A.I. is not a “game-changer.” It’s a game-winner. It replaces hope with certainty, noise with clarity, and emotion with data. In our complimentary live sessions, you’ll discover how advanced algorithms and predictive analytics can help you minimize risk, maximize reward, and approach every trade with the quiet confidence of someone who knows they have an unfair advantage. You’ll see how A.I. has already conquered Chess, Poker, and Go — because it sees patterns we don’t. Why should trading be any different?

So I’m inviting you — personally — to join us for a FREE Live Training and see what happens when cutting-edge machine intelligence becomes part of your trading toolbox. No magic tricks. No hype. Just machine learning applied with precision and purpose… and the peace of mind that comes from knowing your decisions are backed by world-class data instead of gut feelings.

Here’s the whole strategy boiled down to brass tacks: if NVDA closes at $190 or higher on December 19, I theoretically walk away with the full $4.73 credit in my pocket. No drama, no fireworks — just cash for being on the right side of fear. And that $4.73? I don’t let it sit around doing nothing. I flip it into a deep out-of-the-money call, the kind of long-shot ticket that keeps the dream of a moonshot alive without risking a dime of my own capital. In other words, I’ve turned the market’s anxiety into my opportunity. I’ve literally found an opportunity to fund my ambitions with Wall Street’s fears.

Now let’s talk about the nightmare scenario — the one where $NVDA doesn’t wobble… it face-plants. In that case, you eat the full loss on the credit spread: –$5.27. And because disaster doesn’t travel alone, that long-dated call you bought with the premium? That’s another –$4.73 down the drain. Total damage: right around $10. And before you flinch, remember this — even in the absolute worst possible outcome, your maximum risk is capped and known in advance. Ten bucks. That’s it. On a stock trading near $193, that’s barely 5% of the share price. A trader is not blowing up their account. They’re taking a defined, disciplined shot where both the upside and downside are carved in stone. This isn’t reckless. This is risk with guardrails.

Now, you might be thinking, “Where’s the catch?” Good. Healthy skepticism is the mark of a smart trader. But here’s the truth: we’re living in one of the greatest moments in market history, a moment when the so-called “little guy” can finally ride the waves in the same financial ocean where whales used to swim alone. This isn’t about chasing one lottery-sized win. It’s about finding opportunities and stacking consistent, incremental gains, the kind that quietly compounds into real wealth.

And think about this for a moment. In a market this volatile, stepping in without Artificial Intelligence, Machine Learning, and Neural Networks is like walking into a gunfight armed with a rubber band. Why handicap yourself? A.I. doesn’t just level the playing field, it tilts it. It slices through noise with surgical precision, sifts through billions of data points in seconds, and uncovers opportunities no human could spot fast enough. It’s not a fancy gadget. It’s a strategic advantage, the ace subtlety tucked up the sleeves of traders who are dead serious about winning.

This is exactly what VantagePoint’s A.I. delivers every single day: a way to reduce the ugly risks, amplify the beautiful rewards, and trade with the quiet confidence that you’re no longer “guessing” — you’re calculating. And once you see what it can do, the only question you’ll ask is: “Why didn’t I start sooner?”

Curious? Good. That curiosity has built more fortunes than fear ever has. Step forward and discover why VantagePoint has become the trusted choice for professionals who want lower risk, higher reward, and that priceless trader’s commodity: peace of mind.

Let’s be careful out there.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.