The Federal Reserve is the only institution in America capable of making everybody simultaneously angry, terrified, confused, and poorer while insisting it is all part of a carefully calibrated plan. It is a place where twelve people gather around a polished mahogany table, speak in sentences that sound like hostage notes written by economists, and somehow determine whether the average American can afford a mortgage, a truck payment, or eggs. Into this monetary circus walks Kevin Warsh, the new Fed Chair, at a time when inflation still stalks the economy like a raccoon that learned how to open coolers at a campground.

Warsh inherits a financial system drowning in contradictions. Wall Street wants lower interest rates yesterday. Savers want higher yields. Politicians want prosperity without pain, deficits without consequences, and economic growth without recessions. Consumers want prices to stop rising while continuing to spend money like sailors on shore leave. Meanwhile the bond market sits in the corner smoking cigarettes and muttering, “This math does not work.” It is less a monetary environment and more a family Thanksgiving dinner where everybody secretly blames everybody else for the national debt.

That is what makes Kevin Warsh such an interesting choice.

He is not arriving as a traditional ivory-tower economist armed with 900-page academic papers proving that inflation is “transitory” right before your grocery bill doubles. Warsh comes from Wall Street, Washington, and crisis management. He understands markets, politics, and perhaps most importantly, human panic. The Federal Reserve no longer resembles a calm institution adjusting dials behind the scenes. It now resembles an emergency room physician sprinting through a casino carrying a fire extinguisher. Warsh is stepping into the role at a moment when confidence in central banking may matter more than the actual interest rate itself.

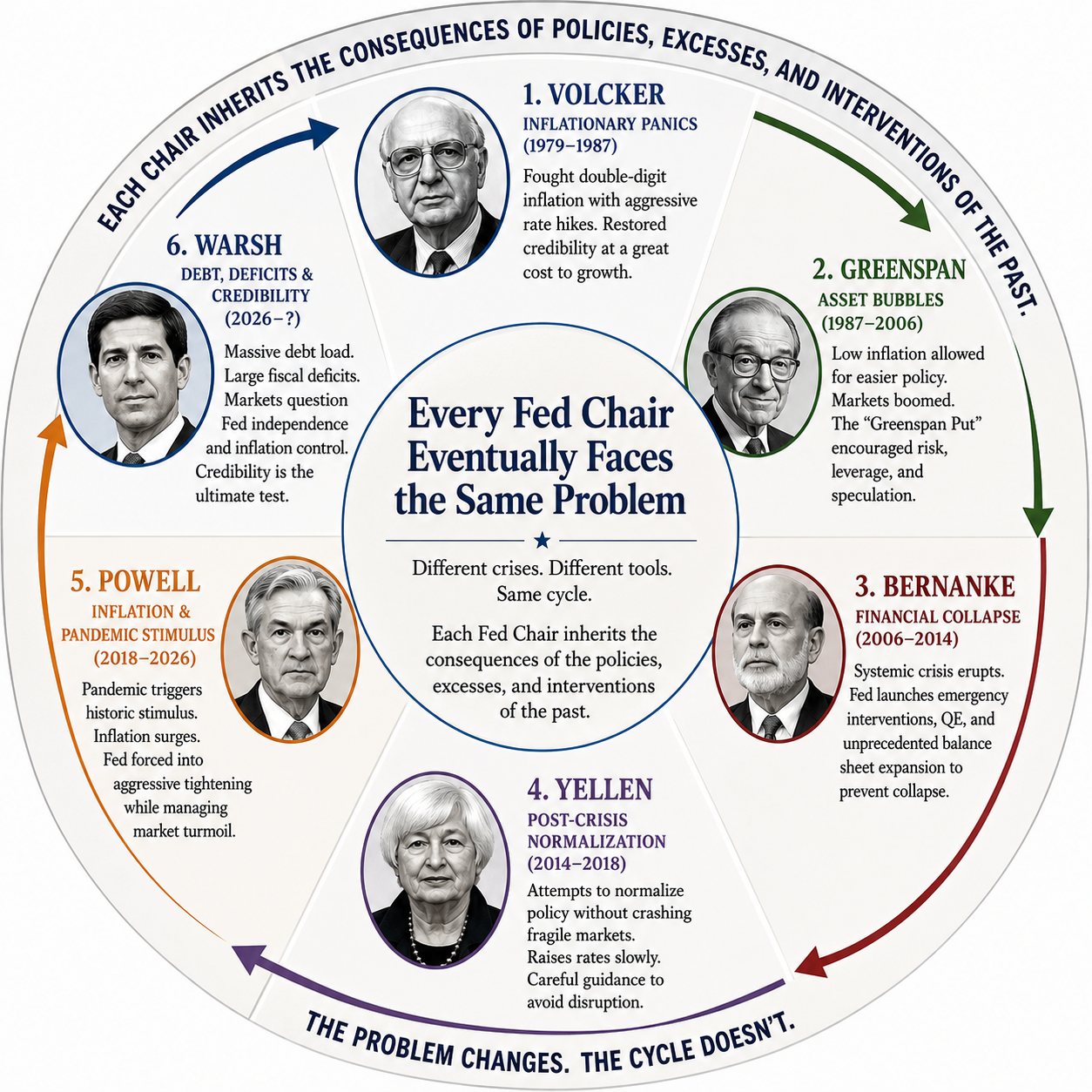

Every Fed Chair walks into the job pretending to be a pilot. He is usually the janitor arriving after the last guy’s party. The punch bowl is empty, the carpet is smoking, the guests are overleveraged, and someone from the Treasury Department is asking whether the cleanup can be financed over 30 years.

Volcker inherited inflation, which is what happens when politicians discover the printing press and economists call it “stimulus.” He walked in, looked at the mess, and did the one thing nobody in Washington likes: he made money expensive. It hurt. It worked. Naturally, later generations decided this was far too unpleasant to repeat.

Greenspan inherited Volcker’s restored credibility and converted it into a market comfort blanket. Under Greenspan, investors learned a dangerous lesson: when markets fall hard enough, the Fed might show up with rate cuts and soothing language. Thus, was born the Fed put, one of the great inventions in modern finance, right up there with derivatives, stock options, and blaming everything on “liquidity conditions.”

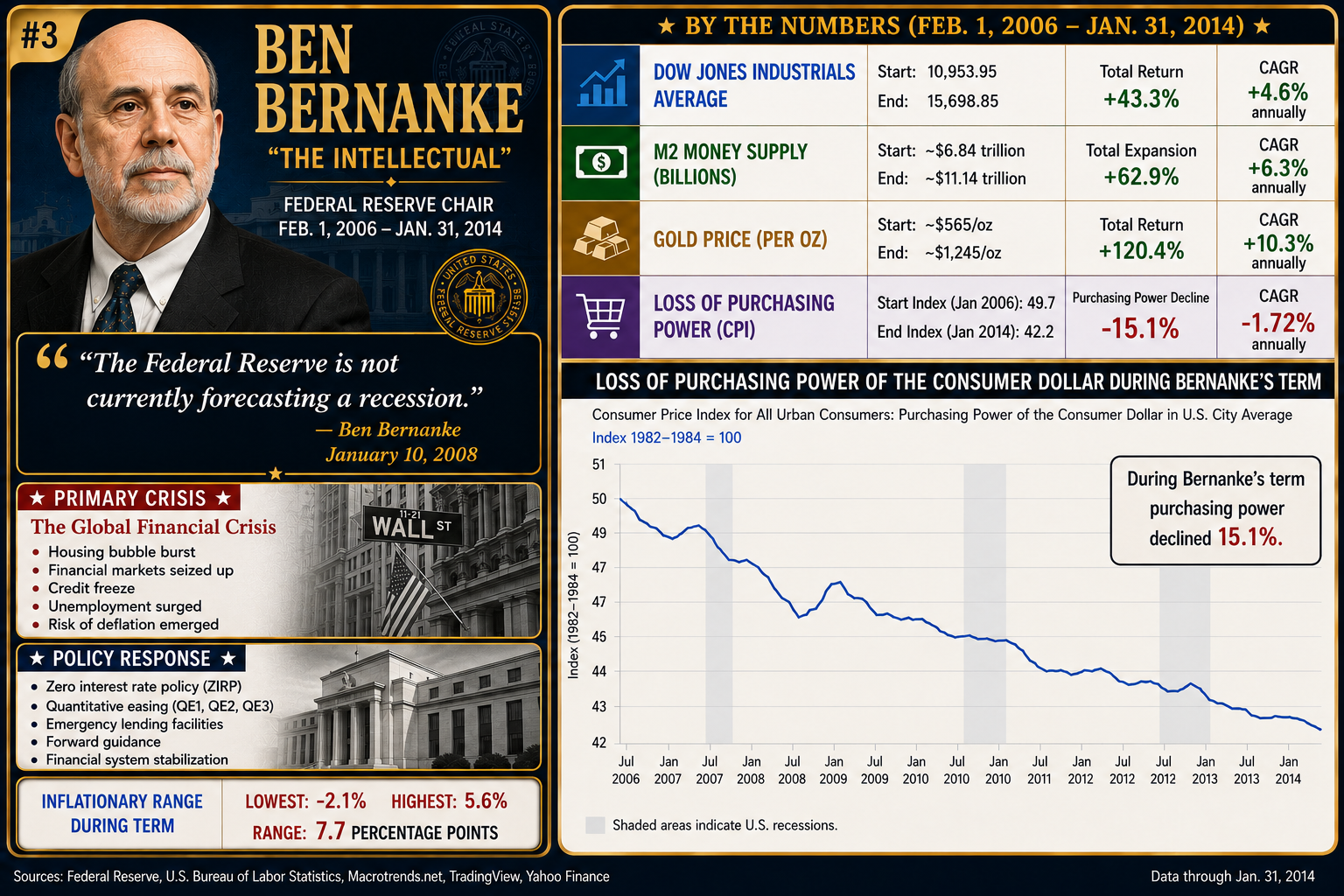

Bernanke inherited the bubble that confidence helped inflate. Housing cracked. Credit froze. Wall Street discovered that leverage is only fun on the way up. Bernanke, a scholar of the Great Depression, responded by building the emergency-policy machine: zero rates, quantitative easing, rescue facilities, and a Federal Reserve balance sheet that began to look like a government garage sale conducted with trillion-dollar checks.

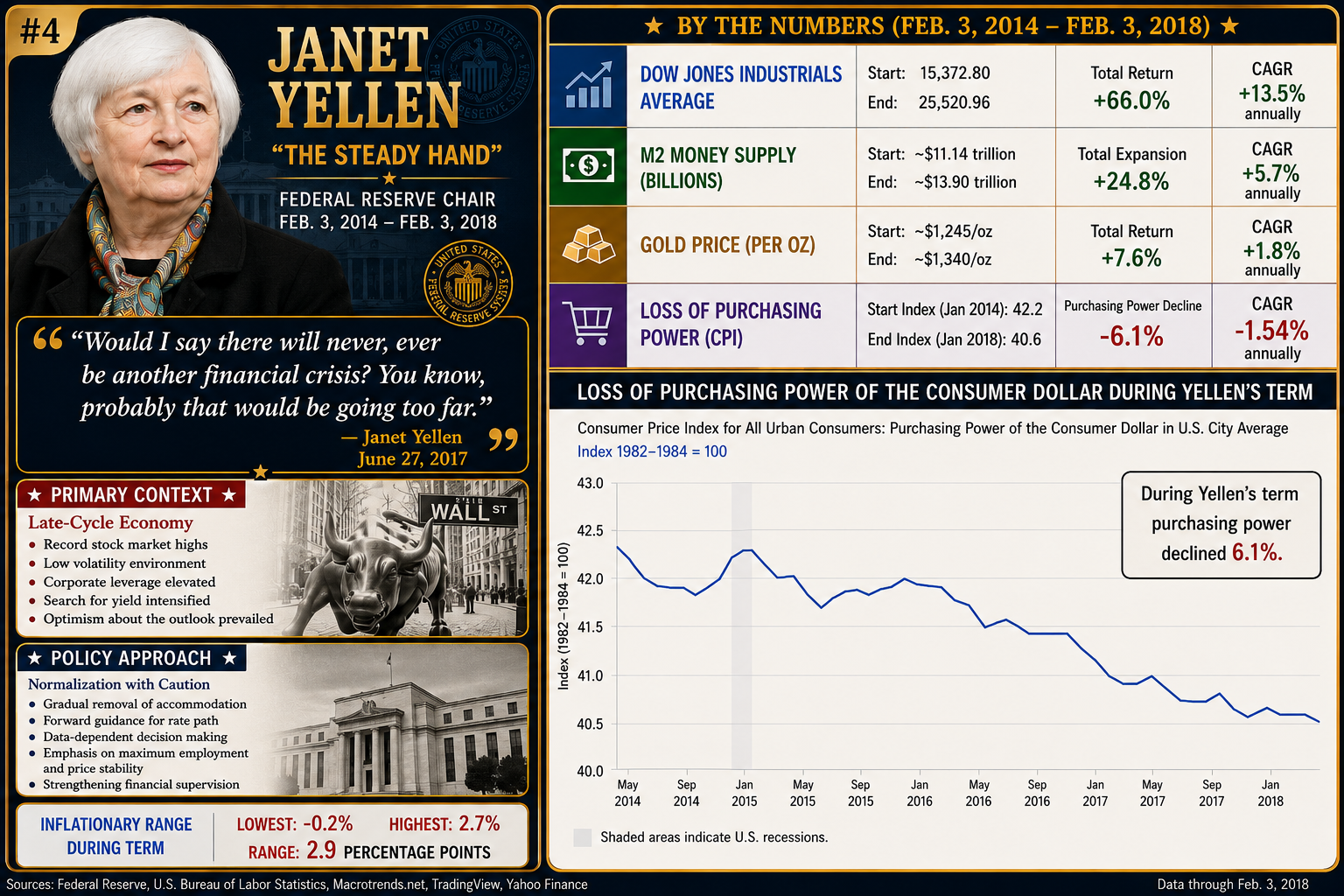

Yellen inherited that emergency machine and tried to gently turn it off without electrocuting the patient. She raised rates slowly, spoke carefully, and attempted normalization in the same way one removes a sleeping tiger from the living room: quietly, slowly, and with a deep awareness that everybody may still get mauled.

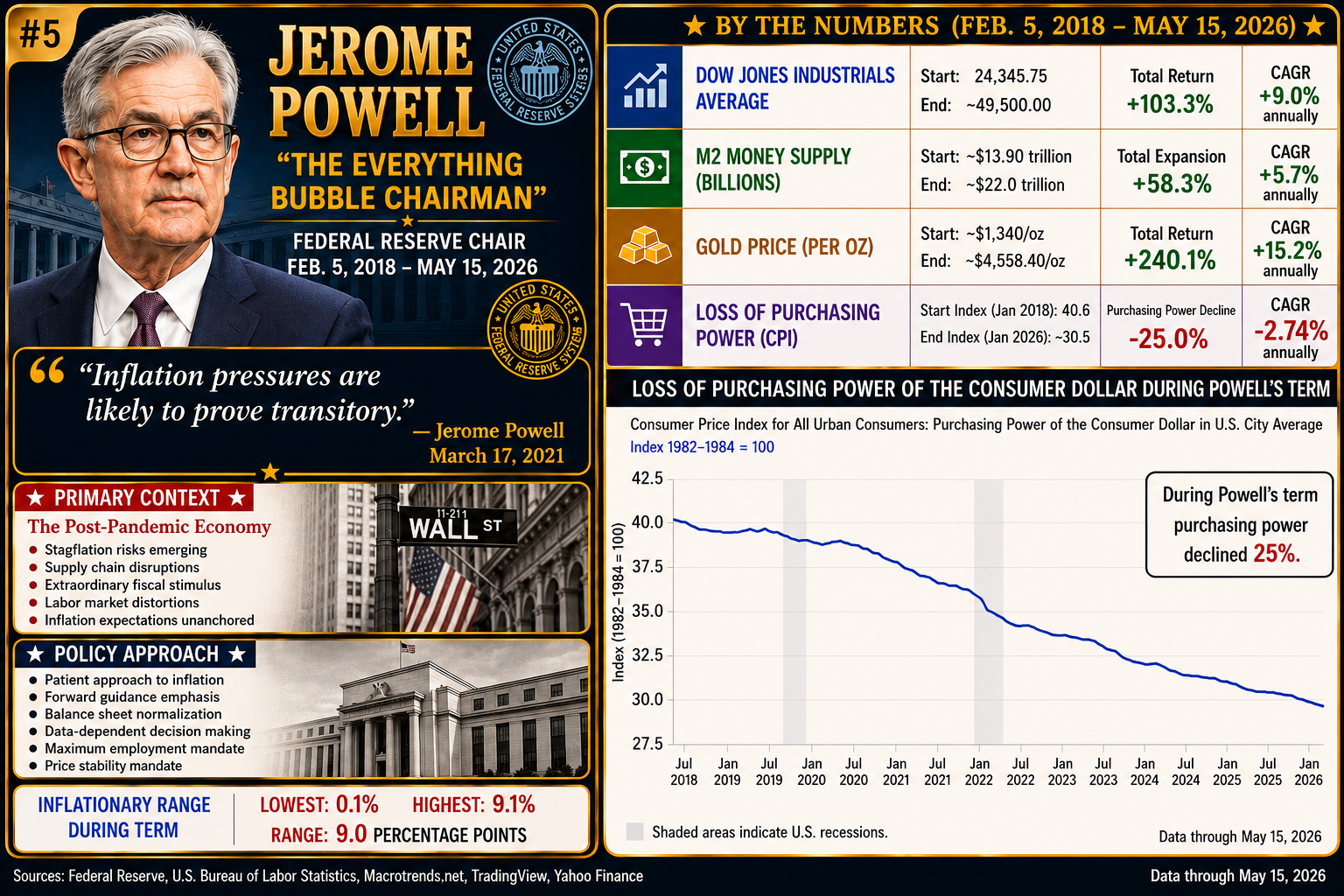

Powell inherited the whole contraption, then COVID arrived and the Fed fired the liquidity cannon. Money flooded the system. Markets levitated. Speculation became a national hobby. Then inflation showed up, wearing steel-toed boots, and Powell had to fight the very fire that years of emergency policy helped fuel.

Now Warsh inherits the entire bill. Not just inflation. Not just debt. Not just deficits. He inherits the accumulated tab for decades of easy money, market rescues, moral hazard, asset bubbles, and the comforting national delusion that every problem can be solved with lower rates and a bigger balance sheet. Every Fed Chair inherits the consequences of the last policy regime. Warsh may be the one who discovers whether America can still afford the consequences.

Wall Street says it wants capitalism.

It does not.

It wants sedation.

It wants free markets when stocks are rising. It wants discipline when someone else is taking the loss. It wants price discovery right up until price discovery discovers something ugly.

Then the language changes.

Suddenly, the market wants rate cuts. It wants liquidity. It wants balance-sheet expansion. It wants the Fed Chair to walk to the microphone, speak calmly, and tell everyone the grown-ups are back in charge.

That is the great contradiction of modern markets.

Wall Street loves capitalism until capitalism starts acting like capitalism. Then it wants rescue. It wants comfort. It wants cheap money. It wants the Federal Reserve to turn pain into policy.

And that is the world Kevin Warsh has inherited.

Kevin Warsh is not the typical Federal Reserve Chair. He did not spend his entire career buried inside academic economic models or teaching graduate students about monetary theory. His background is much more practical. Warsh built his career at the intersection of Wall Street, Washington, and global finance. That matters because the Federal Reserve today is not operating in a textbook environment. It is operating in a world where markets move instantly, debt levels are enormous, inflation pressures remain unpredictable, and confidence can disappear overnight.

Warsh grew up in Loudonville, New York, near Albany. He attended Stanford University where he studied public policy before earning a law degree from Harvard Law School. From there he moved into finance, joining Morgan Stanley where he worked on mergers, acquisitions, and corporate strategy. That experience gave him direct exposure to how businesses raise capital, how markets function, and how investor psychology influences financial decision making. Unlike many economists, Warsh understands that markets are not driven solely by equations. They are driven by fear, confidence, liquidity, and expectations.

His path eventually took him into government. Warsh served as a special assistant for economic policy in the George W. Bush administration before joining the Federal Reserve Board of Governors in 2006. That timing proved critical because only two years later the financial crisis erupted. Warsh found himself at the center of one of the most dangerous economic periods in modern history. He worked directly on crisis response, banking stability, and international coordination during a period when confidence in the entire financial system was collapsing. That experience is one of the primary reasons many observers believe he is qualified to lead the Federal Reserve today.

That distinction matters more than it may initially appear. Over the past several decades, the Federal Reserve has often been led by deeply academic economists whose careers were rooted in research, statistical modeling, and university life. Warsh’s trajectory was different almost from the beginning. After Harvard, he entered Morgan Stanley, where he worked on mergers, acquisitions, and strategic advisory work during an era when globalization and capital flows were rapidly reshaping corporate America. It gave him firsthand exposure to how markets behave under pressure, how executives think about capital allocation, and how confidence and liquidity can move entire sectors long before economic data catches up.

His move into public service accelerated under President George W. Bush, where he served as a special assistant for economic policy before joining the Federal Reserve Board in 2006. In retrospect, the timing could hardly have been more consequential. Within two years, the global financial system was unraveling. Lehman Brothers collapsed. Credit markets froze. Confidence evaporated. Warsh suddenly found himself inside the institution tasked with preventing systemic collapse. For many on Wall Street, that period remains the defining credential on his résumé. He was not merely observing crisis management from the sidelines. He was inside the room while the modern Federal Reserve was reinventing itself in real time.

There is a tendency in Washington and on Wall Street to treat each incoming Federal Reserve Chair as though a new monarch has ascended the throne, armed with fresh theories, superior judgment, and the ability to tame whatever economic chaos threatens the financial system at that particular moment. Yet history suggests something far less glamorous and considerably more uncomfortable. Every Fed Chair eventually discovers that the institution is not simply managing the economy. It is managing the accumulated consequences of prior interventions, prior excesses, and prior attempts to postpone pain. The problems change names. The underlying cycle rarely changes at all.

Paul Volcker inherited an America suffering from inflation so severe that confidence in the dollar itself was deteriorating. Prices were spiraling, oil shocks had destabilized expectations, and the public had begun to assume inflation was a permanent feature of economic life. Volcker responded with brutal interest rate hikes that ultimately restored credibility to the Federal Reserve, but not before causing immense economic pain. In many respects, Volcker’s legacy became the foundation for modern central banking itself: the belief that the Fed’s ultimate power rests not in stimulus, but in credibility. Ironically, the decades that followed would test whether markets and politicians preferred credibility once it became expensive.

Alan Greenspan entered a different environment entirely. Inflation had been subdued. Markets were globalizing. Technology was accelerating productivity and optimism. But Greenspan’s era quietly introduced another problem that would echo through the next several Fed regimes: the growing belief that the Federal Reserve would always intervene to stabilize markets when asset prices fell too far. The so-called “Greenspan Put” became less a theory than an assumption embedded into investor psychology. Cheap money, expanding leverage, and increasingly speculative behavior flourished under the confidence that the Fed would ultimately cushion systemic pain. Asset bubbles did not become accidental side effects. They increasingly became structural features of the system itself.

Ben Bernanke inherited the logical conclusion of that environment. The housing bubble collapsed. Credit markets froze. Major financial institutions stood on the brink of failure. Bernanke, a scholar of the Great Depression, responded with extraordinary emergency measures that fundamentally reshaped the Federal Reserve. Quantitative easing, massive balance sheet expansion, and aggressive liquidity programs became the new architecture of crisis management. At the time, many argued the actions were necessary to prevent financial catastrophe. They may well have been. But they also accelerated another long-term transformation: the Federal Reserve evolved from lender of last resort into the central stabilizing force behind nearly every major asset market in the world.

Janet Yellen then faced the unenviable task of attempting to normalize policy after years of emergency intervention without destabilizing the very markets those interventions had helped inflate. It was a delicate balancing act that revealed an uncomfortable truth about modern monetary policy: once markets become conditioned to extraordinary accommodation, removing it becomes politically and financially dangerous. Jerome Powell eventually confronted an even larger version of the same dilemma. The pandemic unleashed historic fiscal and monetary stimulus simultaneously. Liquidity flooded the system. Asset prices exploded higher. Inflation surged. And suddenly the Federal Reserve found itself trying to contain an inflationary cycle partially born from the very policies used to prevent economic collapse only a few years earlier.

Now Kevin Warsh steps into the same institutional drama, though perhaps at an even more fragile stage. His defining challenge may not simply be inflation or growth, but credibility itself. Debt levels are enormous. Fiscal deficits continue expanding. Treasury financing needs are immense. Markets increasingly question whether the Federal Reserve can simultaneously support government borrowing costs, contain inflation, stabilize financial markets, and preserve confidence in the dollar over the long term. That is the recurring irony of central banking. Every Fed Chair arrives promising to solve the immediate crisis of the moment. Eventually, they discover they are also inheriting the unintended consequences of every rescue operation that came before them.

America today resembles a man who has financed three boats, two vacation homes, a bass fishing addiction, and a divorce settlement entirely on a credit card, then becomes furious when the bank mentions interest rates might need to rise. The national debt has blasted past $40 trillion, which is no longer an economic statistic so much as a cry for help written in spreadsheets. And yet Washington continues spending money with the confidence of a drunken billionaire at a Monaco casino. The uncomfortable reality is that honest interest rates would reveal what much of modern finance desperately hopes nobody notices: a great many things only appear affordable because money itself has been artificially cheap for an extraordinarily long time.

That cheap money created an entire ecosystem of dependency. Politicians became addicted to deficits because borrowing seemed painless. Wall Street became addicted to liquidity because every market wobble was eventually greeted with another soothing blast of Federal Reserve intervention. Corporations borrowed aggressively. Speculators borrowed aggressively. Consumers borrowed aggressively. Meanwhile savers, retirees, and anyone foolish enough to believe thrift might still matter were rewarded with yields barely capable of purchasing a gas station sandwich. Inflation quietly became the most politically convenient tax in America because unlike actual taxation, nobody has to vote for it. Your purchasing power simply disappears while economists explain on television that this is somehow evidence of a “strong economy.”

Now comes the dangerous question Kevin Warsh and the Federal Reserve will eventually confront: what happens if interest rates are finally allowed to reflect actual risk? The answer is both obvious and terrifying. Markets want lower rates because higher rates threaten valuations, leverage, and speculation. The federal government needs lower rates because financing trillions of dollars of debt at honest borrowing costs would turn interest expense into a fiscal horror movie. But monetary credibility may require precisely the opposite. That is the central banking trap. The longer artificial rates suppress reality, the more painful reality eventually becomes. At some point the bond market begins behaving like the only sober person left at the party. And sober people have an annoying tendency to ruin everybody’s fun.

I have listened to more Federal Reserve speeches than I care to admit, and after a while the language begins to sound strangely familiar. The vocabulary changes slightly from Chair to Chair. The accents differ. The academic frameworks evolve. But the core promise rarely changes: stability, confidence, controlled inflation, sustainable growth. The Federal Reserve presents itself as the institution standing between the American economy and financial chaos. And to be fair, there are moments in history when that description is entirely justified.

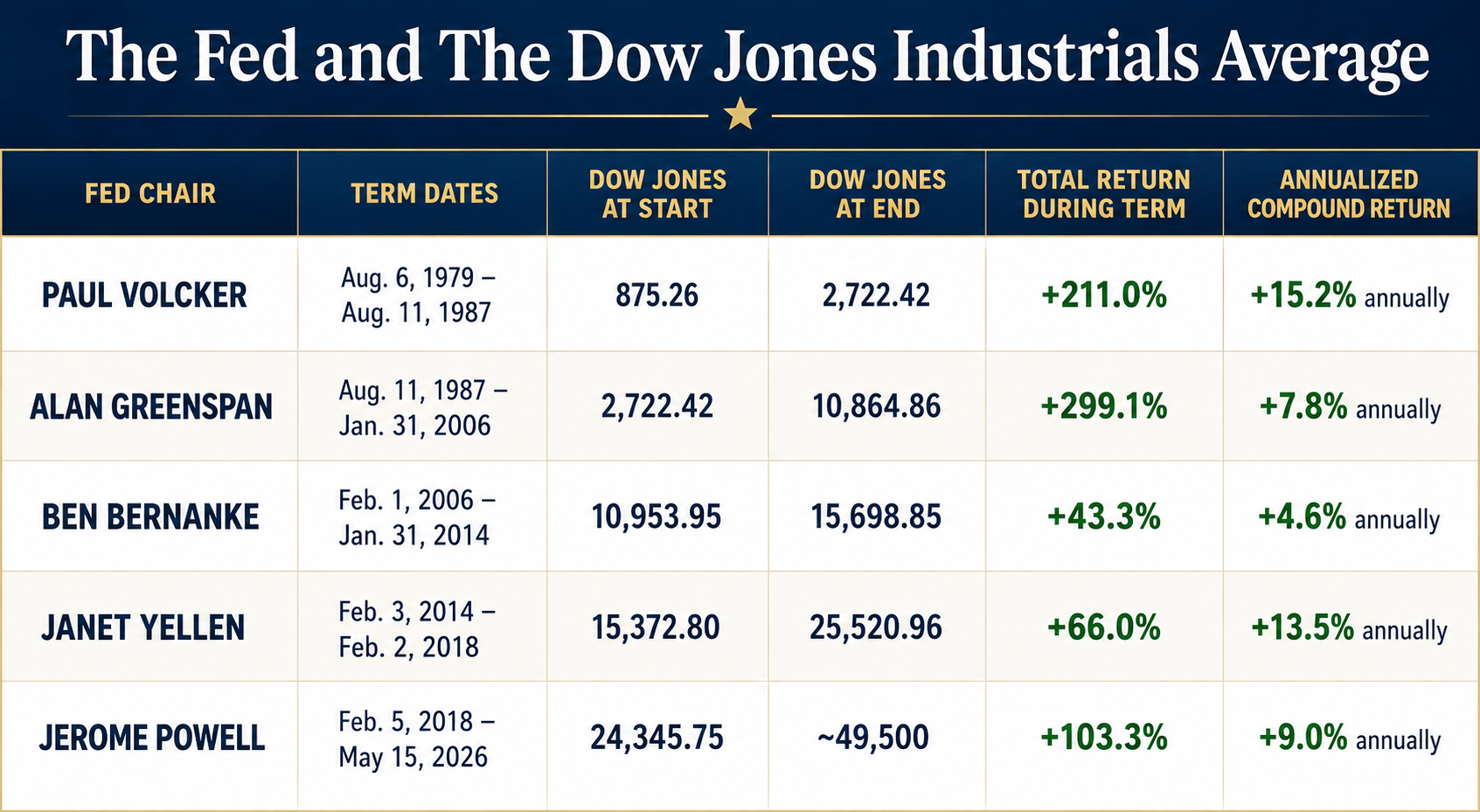

But there is another side to the story that becomes difficult to ignore once you step back and examine the data over long periods of time. While I remain deeply skeptical of the Fed, there are five metrics through which every Fed Chair can ultimately be evaluated with remarkable clarity: the performance of the DJIA, the rate of expansion of the M2 money supply, the loss of purchasing power of the U.S. dollar, the price of gold, and the range of inflation experienced during their tenure. Those five measurements tell a more revealing story than any press conference ever could.

The legendary market observer Jim Grant once made an observation that may be one of the most brutally accurate descriptions of central banking ever offered. Supporters of the Fed, he said, view the institution as the fire department. Critics view it as the arsonist. The uncomfortable reality is that both descriptions contain elements of truth. The Fed has repeatedly stepped in during periods of panic, collapse, and systemic fear. But many of the imbalances requiring rescue were themselves amplified by years of easy money, suppressed rates, expanding liquidity, and the market psychology those policies helped create.

That is the harsh truth few on Wall Street care to admit publicly. Modern financial markets increasingly depend on the very interventions they simultaneously criticize. Investors denounce inflation while celebrating liquidity. They complain about asset bubbles while rewarding policies that inflate them. They praise capitalism until markets begin behaving like actual markets, at which point they demand stabilization, intervention, and reassurance from the central bank. Over time, the relationship between Wall Street and the Federal Reserve has become less adversarial than symbiotic. And that may be the defining financial story Kevin Warsh ultimately inherits.

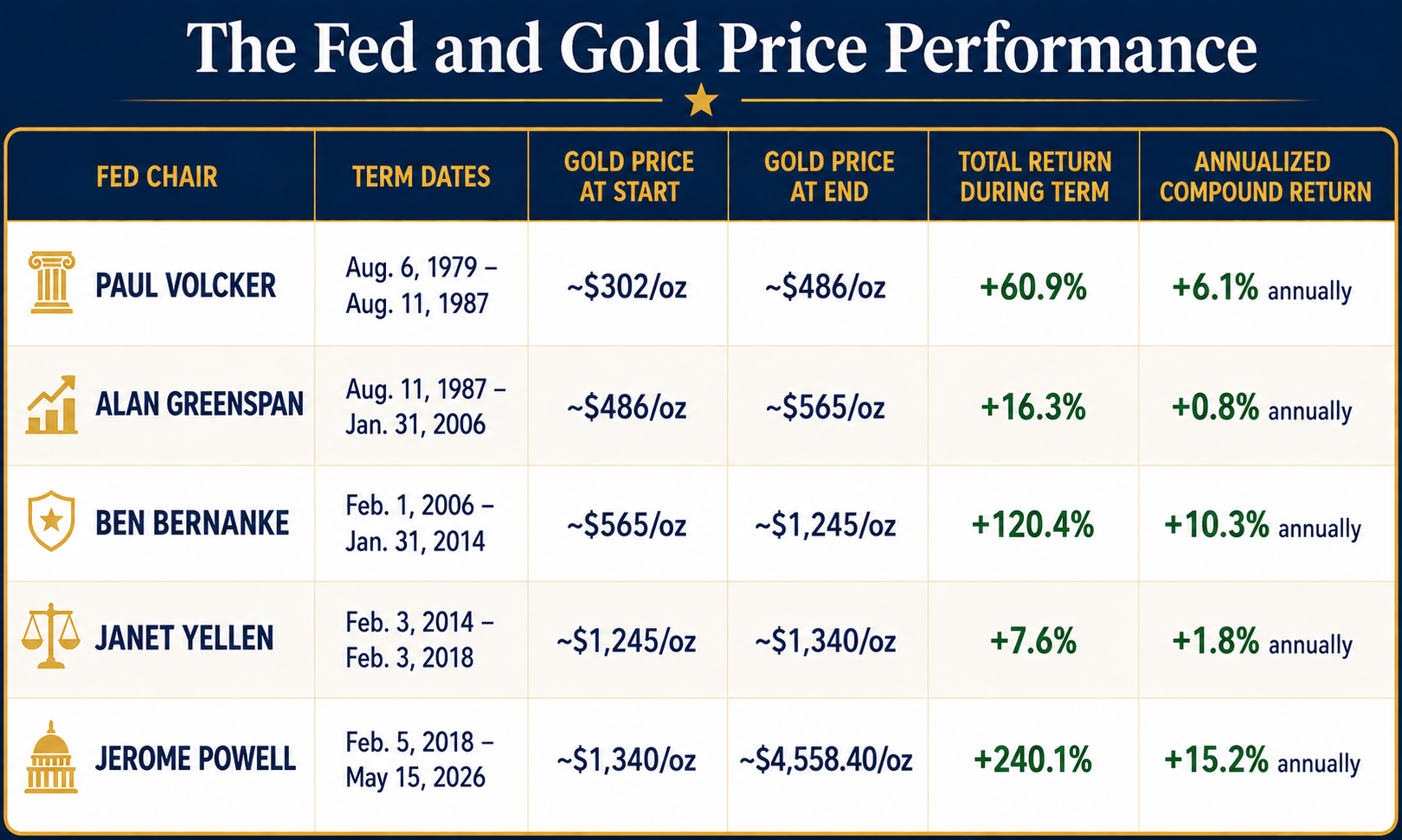

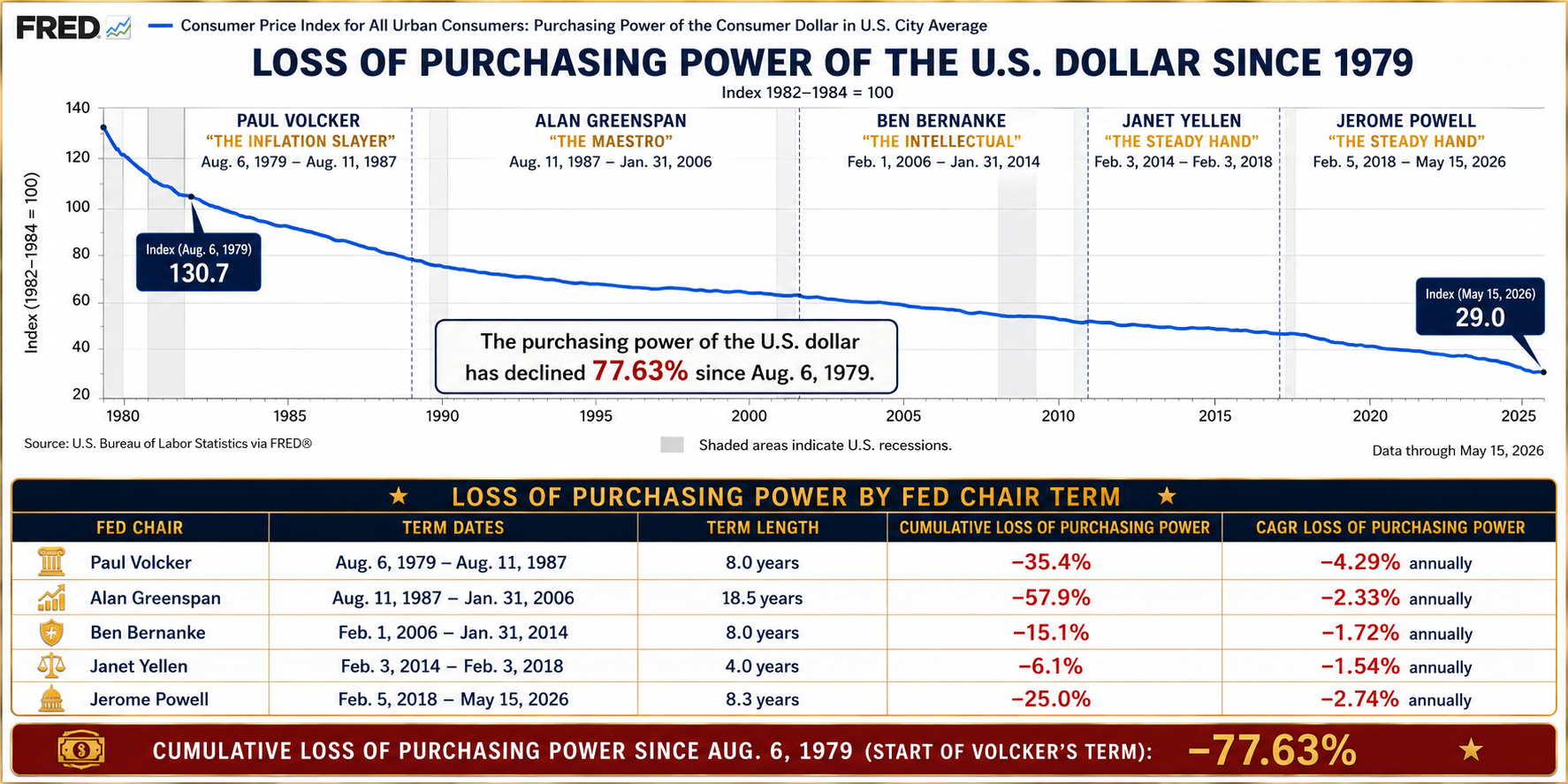

Let’s look at these metrics one at a time for each Fed Chair:

The most important insight is that every Fed Chair inherited a higher stock market than the one before them, despite completely different economic crises and policy regimes. Volcker crushed inflation, Greenspan fueled financial expansion, Bernanke normalized emergency intervention, Yellen stabilized normalization, and Powell unleashed historic liquidity, yet the market’s long-term trajectory increasingly depended on lower rates, expanding debt, and Federal Reserve support. The harsh reality is that Wall Street talks about capitalism, but over time the Dow Jones became increasingly tied to monetary intervention, liquidity expansion, and the expectation that the Fed would step in whenever markets broke badly enough.

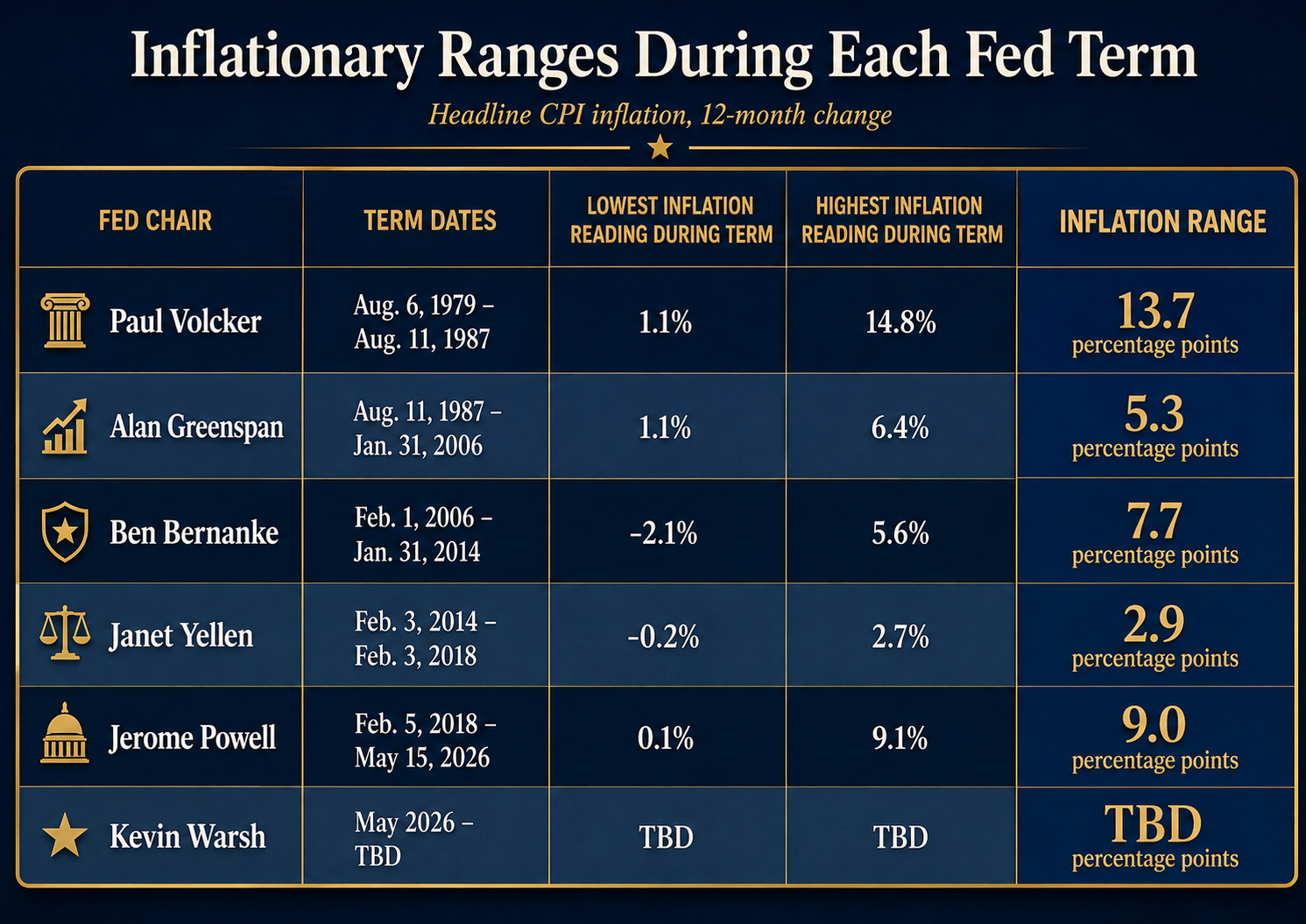

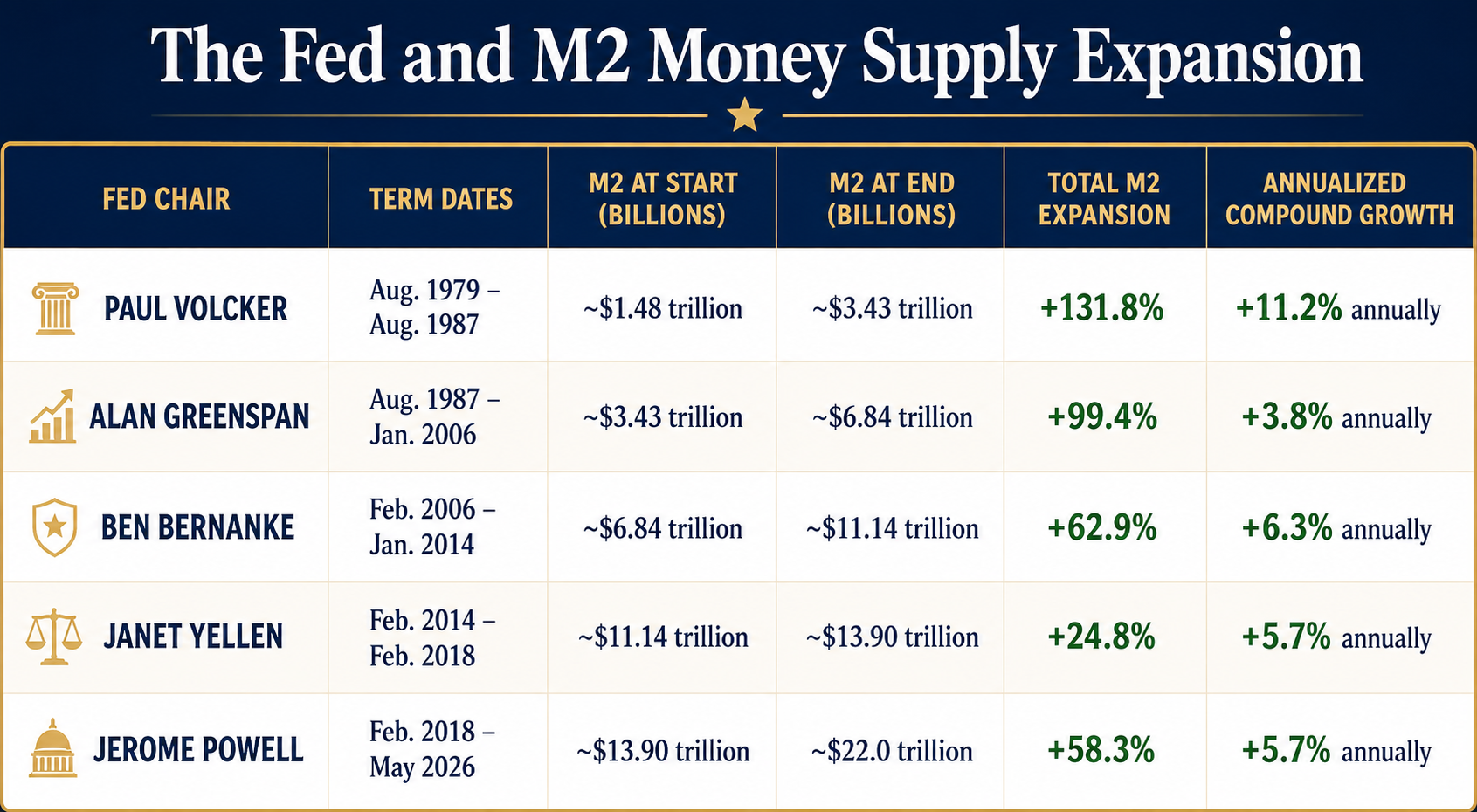

The following two graphics expose the dirty little secret of modern finance: the entire system became increasingly dependent on money creation while simultaneously pretending inflation was under control. Volcker flooded the system with money at an 11.2% annualized pace while crushing inflation through brutally high interest rates, Greenspan institutionalized the belief that the Fed would always rescue markets, Bernanke normalized emergency policy after the financial crisis, Yellen carefully preserved the illusion of normalization, and Powell detonated one of the largest liquidity expansions in American history just as inflation exploded to levels not seen in decades. The pattern is impossible to miss. Every Fed Chair inherited a system requiring more debt, more liquidity, and more intervention than the one before it, while the inflationary ranges reveal the unavoidable consequence of that dependence: sooner or later the purchasing power of the dollar pays the bill for Wall Street’s addiction to monetary sedation.

The gold table may be the most politically uncomfortable graphic of the entire group because it quietly reveals what sophisticated capital eventually does whenever confidence in monetary discipline begins to erode. Volcker’s era was dominated by inflation panic and aggressive tightening, which kept gold relatively contained, but once Greenspan normalized easier money and financial leverage, Bernanke institutionalized emergency liquidity, and Powell flooded the system with historic stimulus, gold’s performance exploded as a long-duration referendum on fiat credibility itself. The most important insight is not simply that gold rose under Powell. It is that every successive Fed regime required larger interventions, larger balance sheets, and greater monetary expansion to stabilize markets, while gold increasingly behaved like a running audit of whether investors truly believed the dollar would maintain its purchasing power over time.

There is something almost poetic about the modern Federal Reserve. Every chairperson arrives in Washington speaking the language of “stability,” “confidence,” and “protecting the consumer,” while the purchasing power of the dollar quietly gets marched out the back door like a drunk uncle at a wedding reception. The chart tells the story with brutal honesty. Since Paul Volcker took office on August 6, 1979, the U.S. dollar has lost 77.63% of its purchasing power. That works out to a compounded annual loss rate of roughly 3.17% per year over nearly 47 years. Not in one catastrophic collapse. Not with sirens and headlines. Just a slow, polite confiscation spread across decades, administered by very educated people in expensive suits assuring everyone the situation is “well contained.”

If you are keeping score at home, we see certain facts jump off the page when we look at these metrics.

- Each Fed Chair has seen higher stock market prices.

- Each Fed Chair has expanded the M2 Money Supply massively.

- Each Fed Chair has seen gold price increases.

- Each Fed Chair has seen massive currency debasement and loss of purchasing power.

So, excuse me if I am not overly optimistic about what Kevin Warsh is going to do during his reign as Fed Chair.

Kevin Warsh may become the first true Wall Street Fed Chair of the artificial intelligence era, and that distinction matters far more than many investors currently appreciate. The economy he is inheriting is not merely cyclical. It is structurally transforming in real time. Artificial intelligence is beginning to alter productivity, labor markets, capital allocation, corporate strategy, and even national security simultaneously. At the same time, the United States is attempting to finance historically large deficits while rebuilding domestic manufacturing capacity, restructuring global supply chains, and funding an increasingly digitized geopolitical competition. This is no longer the post-Cold War globalization economy that shaped much of modern central banking. It is something far more unstable, interconnected, and technologically accelerated.

Unlike Ben Bernanke, who approached the financial crisis primarily as an academic student of systemic collapse, or Jerome Powell, who managed the extraordinary overlap of pandemic stimulus and inflation shocks, Warsh arrives with the instincts of a market operator. That difference could prove enormously important. AI is not simply another technology cycle. It is creating explosive capital flows into semiconductors, infrastructure, data centers, robotics, cybersecurity, and defense technologies at a pace that increasingly resembles a monetary event as much as an innovation story. Markets are repricing entire industries around future productivity assumptions that may or may not materialize. In many ways, the Federal Reserve is entering an environment where technological optimism itself could become inflationary through speculation, leverage, and asset appreciation.

The challenge for Warsh is that the monetary system itself may be entering a transition period at precisely the same moment the federal government faces unprecedented financing pressures. Treasury issuance continues climbing. Foreign capital relationships are evolving. De-globalization and reshoring are raising structural costs across supply chains that were once optimized purely for efficiency. Meanwhile AI-driven productivity gains could simultaneously suppress labor demand in some sectors while dramatically increasing investment demand in others. This creates a deeply unusual policy environment where deflationary technology, inflationary fiscal policy, geopolitical fragmentation, and speculative capital flows may all collide at once. The next Federal Reserve Chair may not simply be managing inflation or growth. He may be managing the monetary consequences of a rapidly digitizing economic order.

As a kid, I used to collect and trade baseball cards. Everybody had their favorites. Some cards exploded in value, some looked great until the stats on the back told a very different story. So, I got to thinking… why not do the same thing with Federal Reserve Chairmen? After all, these guys have been managing the most important “trading card” in America for the last 47 years: the purchasing power of your money. And judging by the long-term statistics, owning dollars has sometimes felt like collecting a rookie card of a relief pitcher with a 9.00 ERA. Respectfully speaking, Kevin Warsh is about to inherit the same dugout, the same rulebook, and the same money printer that every Fed Chair before him eventually became best friends with. At this point, betting a new Fed Chair will suddenly protect the dollar feels a little like believing the next contestant at a hot dog eating contest is finally going to recommend salads.

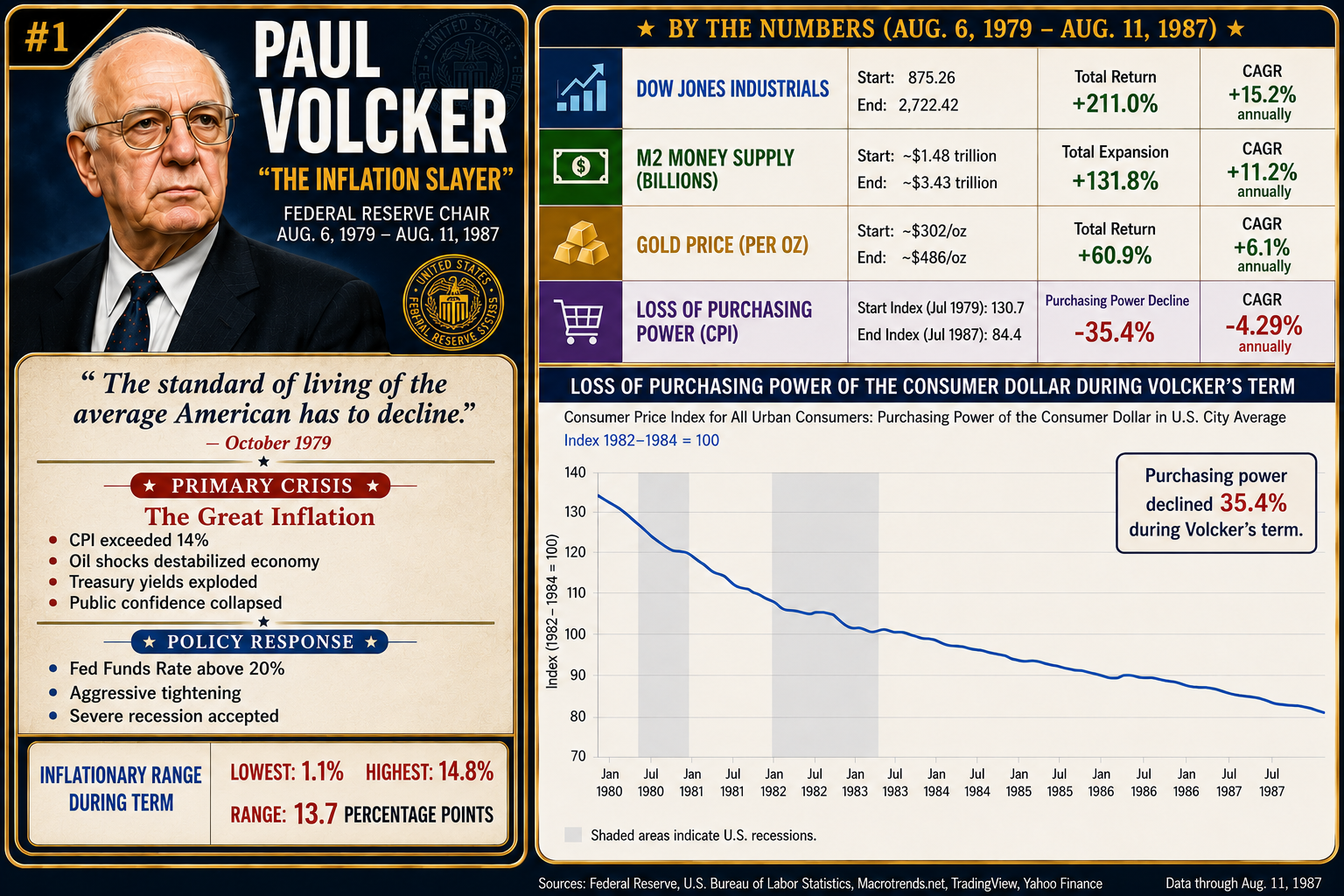

#1 Paul Volcker — “The Inflation Slayer”

Volcker walked into the Federal Reserve like a firefighter entering a burning building with a gasoline can in one hand and a flamethrower in the other. He crushed inflation with interest rates north of 20%, but even during his legendary tenure the dollar still lost 35.4% of its purchasing power, which is a reminder that “winning” at central banking often just means losing money more slowly.

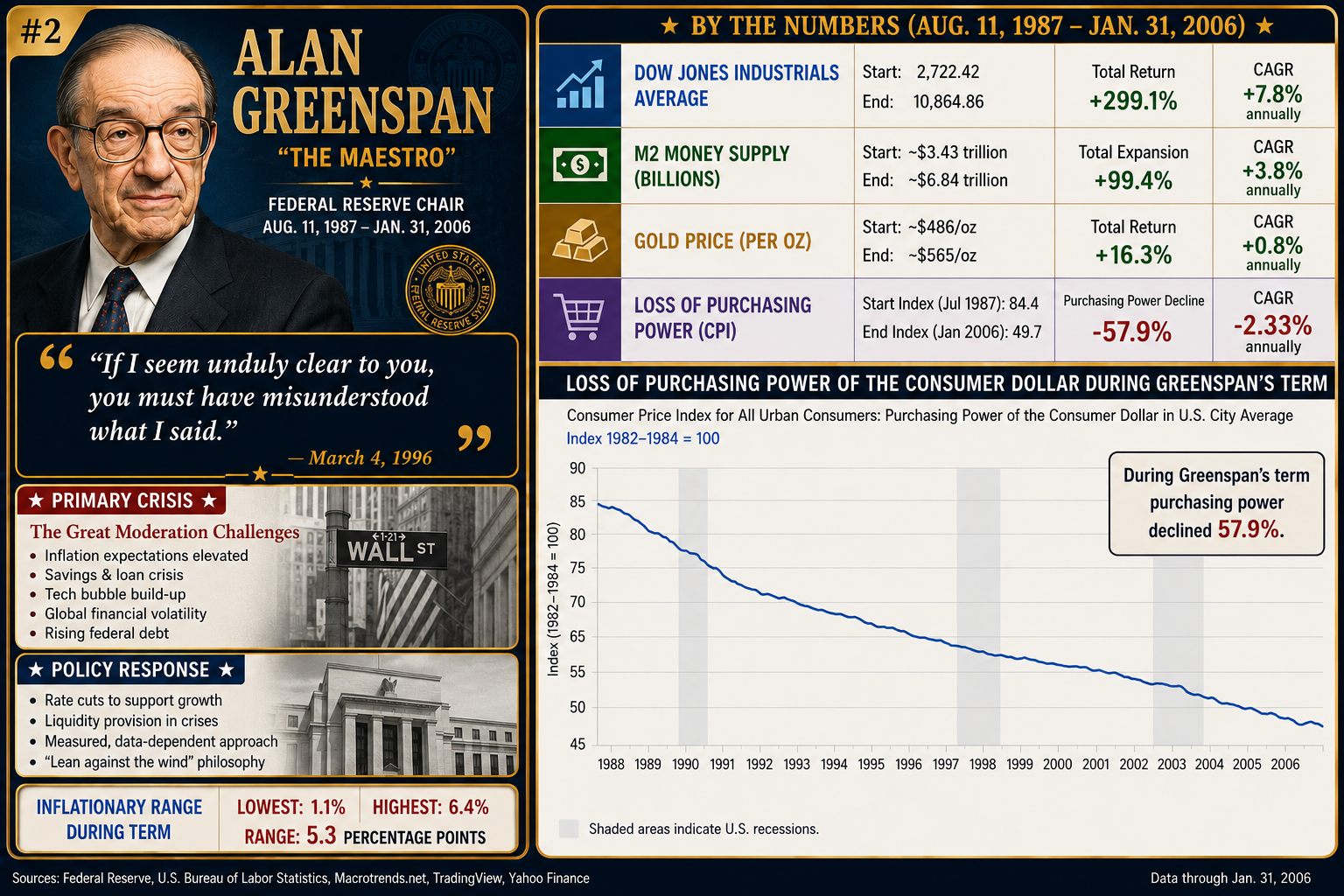

#2 Alan Greenspan — “The Maestro”

Greenspan became the rock star Fed Chair of Wall Street, the financial equivalent of a Vegas magician who kept making bubbles appear out of thin air. Stocks soared, everyone felt richer, and meanwhile the dollar quietly lost another 57.9% of its purchasing power while most Americans were too busy admiring their 401(k) statements to notice the ice cube melting in their drink.

#3 Ben Bernanke — “The Intellectual”

Bernanke inherited the financial crisis and responded the only way modern central bankers know how: print first, explain later. Quantitative easing entered the mainstream, trillions appeared like rabbits from a hat, and the dollar lost another 15.1% of its purchasing power while Wall Street got rescued faster than a celebrity stranded on a yacht.

#4 Janet Yellen — “The Steady Hand”

Yellen’s era felt calm on the surface, almost suspiciously calm, like the eye of a hurricane where everybody suddenly forgets weather exists. Stocks climbed, volatility disappeared, and yet even in one of the smoothest economic stretches in modern history the dollar still managed to lose another 6.1% of its purchasing power because apparently inflation never really sleeps… it just takes coffee breaks.

#5 Jerome Powell — “The Everything Bubble Chairman”

Powell took office just in time for a pandemic, supply chain chaos, stimulus mania, and the greatest money-printing experiment since somebody first discovered paper and ink. The result? The dollar lost another 25% of its purchasing power while Americans were repeatedly assured inflation was “transitory,” which may go down as the financial version of telling passengers on the Titanic the water in the hallway is only temporary.

If you study the last 47 years of Federal Reserve history with any intellectual honesty, it becomes very difficult to argue that Kevin Warsh is suddenly going to reverse a system built on perpetual currency debasement. I genuinely wish him enormous success because the stakes could not be higher, but as both a student of history and someone who understands incentives, I would be stunned if the next chapter looks materially different from the previous five. Warsh was not selected accidentally. He was carefully vetted by Treasury Secretary Scott Bessent and the Trump administration, and while he will undoubtedly go to great lengths to project independence, markets ultimately care less about rhetoric and far more about outcomes. And the one outcome President Trump has been crystal clear about is his desire for lower interest rates and a significantly weaker U.S. dollar to stimulate growth and competitiveness. History suggests that combination rarely arrives quietly. It usually arrives with enormous volatility, violent rotations across asset classes, and extraordinary trading opportunities for those prepared to navigate the chaos. That is precisely why traders using VantagePoint AI should be paying extremely close attention right now.

A few important observations jump off the page.

Paul Volcker inherited inflationary chaos and left behind the foundation for one of the greatest bull markets in financial history. Alan Greenspan oversaw the largest structural expansion of financial assets, leverage, and investor confidence in modern history. Ben Bernanke inherited systemic collapse and, in the process of preventing depression, normalized emergency intervention as a standard operating procedure of modern central banking. Janet Yellen attempted the delicate task of normalization without destabilizing markets that had become deeply conditioned to easy money. Jerome Powell presided over one of the most aggressive liquidity expansions ever attempted, colliding with the AI boom, pandemic stimulus, and the sharpest inflation cycle in four decades. And now Kevin Warsh has inherited the highest Dow Jones Industrial Average in history alongside the largest debt burden the United States has ever carried. In my book the odds favor a massive money print far bigger than his predecessors.

What becomes difficult to ignore is the broader historical pattern underneath these individual eras. Every Fed Chair confronted a different immediate crisis. Inflation. Asset bubbles. Banking collapse. Pandemic shutdowns. Debt expansion. Yet across nearly every regime, the long-term trajectory of markets became increasingly dependent on the same underlying forces: lower rates, larger liquidity injections, expanding Federal Reserve balance sheets, and continuously rising debt levels. The mechanisms changed. The dependence deepened.

That may be the central contradiction of modern finance. Markets still describe themselves as capitalist systems driven by risk, discipline, and price discovery. But over time, the largest market advances increasingly coincided with periods of extraordinary monetary accommodation. The line separating emergency policy from structural policy slowly blurred. Quantitative easing became normalized. Zero rates stopped looking temporary. Market participants began to assume intervention itself was part of the financial architecture.

Which is why the Warsh moment may prove so consequential. The next Fed Chair may not simply be managing inflation, unemployment, or economic growth. He may be managing the accumulated consequences of decades of intervention layered on top of one another. The question is no longer whether markets respond to liquidity. That answer is obvious. The real question is whether a financial system conditioned by years of monetary support can tolerate a world where support is no longer unlimited.

The uncomfortable truth is this: the game has changed, but most investors are still playing by rules written for a world that no longer exists. Traditional textbook investment theory was built during an era when currencies were relatively stable, interest rates behaved rationally, and central bankers still feared inflation more than recession. That world is gone. Today, currency debasement is no longer an emergency policy response. It is the policy. Quietly. Consistently. Relentlessly. And if history is any guide, the next chapter under Kevin Warsh is far more likely to continue that trend than reverse it.

For traders, this changes everything. Because when currencies weaken, volatility rises. Capital rotates faster. Trends accelerate harder. Entire sectors become leadership stories almost overnight while others collapse under the weight of changing interest rates, inflation expectations, and global capital flows. The old “buy and hope” approach becomes dangerously inadequate in an environment where markets can reprice billions of dollars in a single afternoon. You do not need more opinions. You need better tools. You need the VantagePoint AI framework designed specifically for uncertainty, speed, and trend recognition.

That is precisely where VantagePoint AI was built to excel. Its mission is remarkably simple: keep you, the trader, on the right side of the right trend at the right time. Instead of reacting after the move becomes obvious, VantagePoint AI analyzes intermarket relationships, predictive forecasting models, neural networks, and machine learning to identify where strength is building before it becomes front-page news. While most traders are trapped staring at yesterday’s indicators, VantagePoint AI is focused on tomorrow’s probabilities. In a world increasingly driven by policy shocks, currency fluctuations, and algorithmic speed, that advantage is no longer optional. It is essential.

The opportunity ahead could be extraordinary for traders prepared to adapt. But adaptation begins with education, understanding, and seeing these tools in action for yourself. That is why I strongly encourage you to attend a FREE Live Online Masterclass and discover how traders are using VantagePoint AI to navigate volatility, identify opportunity, and forecast market direction with greater confidence in one of the most uncertain financial environments of our lifetime.

See you there.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.