There is a simple question that sits at the center of today’s financial system, and almost no one asks it directly:

Who is actually buying all of this U.S. debt?

Washington continues to run large deficits. Treasury issuance keeps climbing. And yet, beneath the surface, a new class of buyer has emerged, one that does not show up in the usual conversations about central banks, pension funds, or sovereign wealth funds.

It is not a government. It is not a bank. It is not even a traditional financial institution.

It is a piece of software.

More specifically, it is something called a stablecoin.

I’ve been closely watching the rapid rise of stablecoins because they may represent one of the most important shifts in the global monetary system and finance in decades. At their core, stablecoins are digital dollars designed to maintain a one-to-one relationship with the U.S. dollar. Their stability comes from the reserves backing them, primarily short-term U.S. Treasury bills and government debt instruments held by the companies issuing these coins. In effect, these firms purchase U.S. debt, collect the yield generated by those assets, and issue digital tokens against those reserves that can move instantly across the global financial system.

What makes this development so significant is the emerging relationship between stablecoins and U.S. sovereign debt markets. Washington gains a growing class of buyers for Treasury issuance, while stablecoin issuers generate substantial profits from the interest income tied to those holdings. At the same time, consumers and businesses around the world gain access to a digital dollar infrastructure that operates outside the traditional banking system. What may appear today as a niche corner of crypto increasingly looks like the early architecture of a new global payments network built directly on top of the U.S. dollar itself.

At its simplest, a stablecoin is a digital dollar. Not a volatile asset like Bitcoin, and not a programmable platform like Ethereum, but something far more practical. A stablecoin is designed to hold a steady value, typically one coin equal to one U.S. dollar, while moving across the internet instantly, without the friction of the traditional banking system.

Stablecoins are increasingly being used by a wide range of participants. Traders use them to move in and out of positions without touching the banking system. Businesses use them to settle payments across borders in seconds instead of days. And perhaps most importantly, millions of individuals around the world use them as a way to hold and transfer U.S. dollars in places where access to the dollar itself is limited, restricted, or unstable.

In other words, stablecoins are not just a tool for crypto insiders. They are becoming a global distribution system for the U.S. dollar.

To understand why that matters, you have to understand how they are created.

When a user wants stablecoins, they deposit dollars with an issuer, typically a private company. In return, the issuer creates new digital tokens and sends them to the user. But the critical step happens next. The issuer does not simply hold that cash idle. Instead, it invests those funds in highly liquid, low-risk assets, most commonly short-term U.S. Treasury securities.

Each new stablecoin, then, is not just a digital token. It is a claim on a pool of dollar-backed reserves, often tied directly to the U.S. government’s own debt.

This structure did not emerge overnight. The first widely adopted stablecoins appeared in the mid-2010s, with Tether launching in 2014. The motivation was straightforward. Early crypto markets were volatile and disconnected from the traditional financial system. Traders needed a stable unit of account, a way to move quickly between positions without wiring money in and out of banks. Stablecoins solved that problem.

What began as a convenience for traders has since evolved into something much larger.

Today, stablecoins sit at the intersection of technology, global finance, and public policy. They are used by hedge funds and retail traders, fintech companies and multinational firms, and increasingly by individuals in emerging markets seeking stability in an unstable monetary environment.

And while they were created to make trading easier, their most important role may be something else entirely.

They are quietly becoming one of the fastest-growing channels through which global demand for dollars is transformed into demand for U.S. government debt.

That is not a side effect. That is the story.

Let me give it to you straight.

A stablecoin is just this:

A digital version of the U.S. dollar that actually stays at $1.

That’s it.

No mystery. No hype. No magic.

The dollar’s deterioration, if it comes, is unlikely to arrive as a singular event. More likely, it will emerge gradually through a series of shifts in confidence, capital flows, and market behavior that only appear obvious in retrospect. The DXY now sits at 97.86, resting on a 15-year trendline after retreating from its 2022 highs, a technically important level that investors are watching closely even as broader markets continue to behave as though the underlying system remains intact.

Meanwhile, offshore dollar liabilities have climbed beyond $14 trillion, the highest level in recorded history. Never before has the world depended so heavily on borrowed dollars or been so exposed to the consequences of their scarcity, strength, or decline.

Source: BIS Locational Banking Statistics

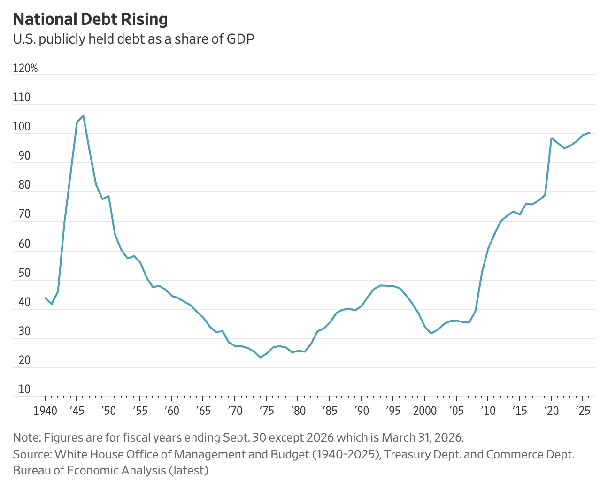

The chart below is showing something very simple but very important: the United States government is now carrying debt equal to more than the entire annual economic output of the country. The last time debt levels were this high was after World War II, but back then America had an enormous industrial boom, a younger population, rising productivity, and decades of economic growth ahead of it. Today, the backdrop is very different. The government now spends roughly $1.33 for every $1 it collects in taxes, which means the gap must continually be filled with more borrowing. At some point, the question stops being whether the debt is large and becomes whether the system can realistically grow fast enough to outrun it.

For regular people, this eventually shows up in the cost of living. Since 2020, the U.S. dollar has already lost roughly 25% of its purchasing power, meaning groceries, insurance, housing, and energy all require materially more dollars than they did just a few years ago. When debt levels become this large, policymakers are left with very few politically acceptable options: raise taxes aggressively, slash spending dramatically, or create more money to keep the system functioning. History suggests the path of least resistance is almost always the same, and that means sooner rather than later the monetary authorities will have little choice but to rev up the money printer once again.

Last Thursday morning, the U.S. Treasury quietly published a set of numbers that, taken together, amounted to something far more consequential than a routine fiscal update. Publicly held federal debt reached $31.265 trillion. Gross domestic product for the prior year came in at $31.216 trillion. The result was a debt-to-GDP ratio of 100.2%, a threshold that economists, market strategists, and policy observers immediately recognized as psychologically and historically significant.

The reaction was swift because the implication was unmistakable: the United States government now owes more than the country produces in an entire year, a condition not seen since 1946. That postwar period, however, came with an industrial boom, demographic expansion, and decades of accelerating productivity. Today’s environment looks very different, which is precisely why that seemingly technical ratio suddenly became the center of a much larger conversation about deficits, debt sustainability, and the future trajectory of the dollar itself.

Stablecoins were created to fix the problem of immediate settlement and instant liquidity.

Instead of bouncing around…

They’re engineered to sit still.

1 coin = $1

Always.

Here’s how to think about it:

Cash in your wallet → physical dollars Bank account → digital dollars (slow, controlled) Stablecoins → digital dollars that move instantly, anywhere

No waiting. No banking hours. No middlemen slowing things down.

Now here’s the part most people miss.

Stablecoins are not trying to replace the dollar.

They are the dollar.

Just… upgraded.

When you hold a stablecoin like:

Tether USD Coin

You’re not holding some experimental crypto token.

You’re holding a digital claim on real dollars sitting somewhere in the system.

And who uses these things?

Not just crypto nerds.

Traders who want speed Businesses moving money globally People in unstable countries who just want access to dollars

In other words…

Anyone who wants the stability of the dollar without the friction of the banking system

So forget the jargon.

Stablecoins are dollars that live on the internet, move instantly, and don’t change in price.

And once you understand that…

You’re ready to see why they matter a whole lot more than anyone is telling you.

Most stablecoins offer near-instant settlement compared to the traditional banking system, and that is one of the major reasons they are attracting so much attention from financial institutions, payment companies, and governments.

When you send a stablecoin such as USD Coin or Tether over blockchain networks like Ethereum, Solana, or Tron, the transaction can typically settle within seconds to a few minutes depending on the network being used. That is dramatically faster than traditional bank wires, ACH transfers, or international SWIFT payments, which can take hours or even several business days to fully clear and settle. More importantly, many stablecoin transactions settle 24 hours a day, 7 days a week, including weekends and holidays.

That speed changes a lot economically. A merchant in another country can receive dollar-based payment almost immediately. A company can move treasury funds globally without waiting for banks to open. Traders can move collateral between exchanges instantly. And stablecoin issuers themselves become major buyers of short-term U.S. Treasury debt because those reserves are what back the digital dollars circulating online.

There is an important nuance, however. The blockchain transfer itself may settle instantly, but converting stablecoins back into traditional bank deposits still depends on banking rails, regulations, compliance checks, and liquidity providers. So the crypto side can move at internet speed while the legacy banking system still moves at banking speed. That tension is one reason stablecoins are increasingly viewed as a bridge between the old financial system and a new digitally-native one.

At a mechanical level, stablecoins are less mysterious than they sound and far more consequential than they appear. A user deposits U.S. dollars with an issuer, typically a private company, and in return receives newly created digital tokens, each designed to maintain a one-to-one value with the dollar. The issuer then allocates those funds into a reserve pool, most often composed of cash and short-duration U.S. Treasury securities, effectively anchoring the digital token to the traditional financial system. The result is a financial instrument that behaves like cash but moves with the speed and flexibility of software.

What makes this structure significant is not just its simplicity, but its scale and direction of flow. Every new stablecoin minted represents incremental demand for high-quality dollar assets, and in practice, that has meant Treasuries. The system is, in effect, a conversion engine, turning global demand for digital dollars into a steady bid for U.S. government debt. It is a quiet, continuous loop, one that operates outside the traditional banking narrative but increasingly sits at the center of it.

The debate surrounding stablecoins ultimately comes down to control, trust, and monetary sovereignty. Supporters see faster payments, broader financial access, and a more efficient global dollar network. Critics worry that programmable digital money could create unprecedented levels of financial surveillance and centralized control. Both concerns are legitimate. Stablecoins can be monitored, restricted, and regulated in ways physical cash cannot. Yet despite those concerns, the broader direction appears increasingly clear: some form of digital dollar infrastructure is likely inevitable. That reality is precisely why many investors continue to view Bitcoin as an important parallel asset, not necessarily as a replacement for the dollar, but as an independent monetary alternative in a world moving rapidly toward digitized finance.

Not all stablecoins are centralized, but the overwhelming majority of the largest and most widely used stablecoins today are centralized in practice.

Centralized stablecoins are issued and controlled by companies that hold reserves, manage redemption, and can freeze or blacklist wallets if required by regulators or internal policy. Examples include Tether and USD Coin. These companies typically back their coins with U.S. Treasury bills, cash, or other short-term assets. Because there is a company in the middle, users must trust that:

- the reserves actually exist, the company remains solvent, regulators allow the system to operate, and redemptions continue functioning.

- that centralization is also why these stablecoins can usually maintain tighter dollar pegs and scale globally.

Decentralized stablecoins attempt to remove the company in the middle. Instead of relying on a corporation holding dollars in a bank account, they use smart contracts and crypto collateral to maintain stability. The best-known example is Dai. Rather than being backed directly by dollars in a bank, Dai is largely backed by overcollateralized crypto assets locked into decentralized protocols.

- But decentralization comes with tradeoffs:

- More complexity.

- Greater volatility risk.

- Dependence on crypto collateral prices.

- Potential smart contract vulnerabilities.

- Less regulatory clarity.

And here’s the important reality many people miss: there’s a spectrum. Even “decentralized” stablecoins often rely on some centralized components somewhere in the system, whether that’s governance, collateral sources, or oracle providers. Pure decentralization in finance is much harder to achieve than most early crypto enthusiasts originally imagined.

That is why many governments and institutions currently favor centralized stablecoins. They are easier to regulate, easier to audit, and easier to integrate into the existing banking and Treasury system. Meanwhile, many Bitcoin and crypto purists continue to prefer decentralized alternatives because they are specifically trying to reduce reliance on governments, banks, and corporate intermediaries.

To understand why stablecoins matter, you have to step back and look at the basic math of the U.S. fiscal system. The government spends more than it collects in taxes, creating an annual deficit, and finances that gap by issuing debt in the form of Treasury bills, notes, and bonds. Over time, those deficits accumulate into the national debt, which now requires a constant and growing pool of buyers willing to absorb new issuance. Traditionally, that demand has come from central banks, large institutions, and domestic investors, all operating within a relatively predictable framework.

What has begun to shift, however, is the composition of that demand. Foreign central banks have become less consistent buyers, and private markets must increasingly carry the load. The system still functions, but it does so on the assumption that new sources of demand will continue to emerge as issuance grows. That is the pressure point. Because at its core, the sustainability of U.S. deficits is not just a political question. It is a market question, one that hinges on a simple reality: someone, somewhere, has to keep buying the debt.

What makes stablecoins newly relevant to this conversation is the direct and mechanical link between their growth and demand for U.S. government securities. When a stablecoin issuer creates new tokens, it does so against incoming dollars, and those dollars are not left idle. They are deployed into reserve assets, most often short-term Treasuries, because they offer liquidity, safety, and yield. The consequence is straightforward but profound: every incremental dollar flowing into stablecoins becomes an incremental bid for U.S. debt.

This creates a feedback loop that is easy to overlook but increasingly difficult to ignore. As global demand for digital dollars rises, particularly in markets where access to the traditional banking system is limited, stablecoin issuance expands. And as issuance expands, so does the accumulation of Treasury holdings on issuer balance sheets. In effect, stablecoins are not just financial tools operating alongside the system. They are becoming embedded within it, quietly channeling global capital into the very instruments that finance U.S. deficits.

The growth in stablecoins is not being driven by Silicon Valley enthusiasm or speculative fervor alone. It is being pulled by a far more durable force: global demand for dollars. In many parts of the world, local currencies are volatile, access to the U.S. banking system is limited, and capital controls restrict the free movement of money. Stablecoins offer a workaround, a way to hold and transfer dollar-denominated value with nothing more than a smartphone and an internet connection. For individuals and businesses operating in these environments, they are not a novelty. They are a solution.

What emerges from this dynamic is a quiet but powerful expansion of the dollar’s reach, one that does not rely on traditional financial intermediaries. Stablecoins effectively export the U.S. currency system into regions where it would otherwise be difficult to access, creating new, decentralized channels of dollar adoption. And as that adoption grows, so too does the underlying demand for the assets backing those digital dollars. It is a form of monetary distribution that operates outside the usual policy tools yet increasingly reinforces them from the ground up.

Regulators are no longer asking whether stablecoins matter, but how to oversee them without disrupting the benefits they provide. The concerns are predictable: Are the reserves truly safe and liquid? Could a loss of confidence trigger rapid redemptions? And what happens if a system built outside traditional banking becomes systemically important to it? These are not abstract questions. They are the kinds of issues that sit squarely within the mandate of policymakers responsible for safeguarding markets.

At the same time, there is a growing recognition that stablecoins may serve a strategic function. By channeling global demand for dollars into U.S. Treasury markets, they reinforce the very foundation of the country’s financial system. That has led to a subtle but important shift in tone, from skepticism to cautious engagement, with discussions increasingly centered on how to integrate stablecoins into the regulatory framework rather than push them to the margins. In that sense, stablecoins are no longer just a private innovation. They are becoming part of the conversation about how the United States maintains its financial influence in a changing world.

If the current trajectory holds, stablecoins may evolve from a peripheral innovation into a meaningful source of demand for U.S. government debt. The logic is not complicated. As more users around the world adopt digital dollars for payments, savings, and settlement, the total supply of stablecoins expands. And because those tokens are backed by reserves that are heavily concentrated in short-term Treasuries, the growth of stablecoins translates directly into increased purchases of U.S. debt. What begins as a convenience for moving money becomes, over time, a structural component of how that money is invested.

The more provocative implication is what this means for future deficits. In a world where traditional buyers are less predictable, stablecoins could emerge as a consistent, technology-driven channel for absorbing new issuance. That does not mean they replace institutional demand, but they may increasingly complement it, particularly at the short end of the curve. In effect, the digital rails of the dollar could become part of the financing mechanism itself, linking global demand for liquidity with the ongoing needs of the U.S. Treasury in a way that is both decentralized in form and deeply connected in function.

For all their promise, stablecoins introduce a set of risks that are difficult to ignore precisely because of how tightly they are beginning to link into the broader financial system. The model depends on confidence, specifically the belief that each token is fully backed by liquid, high-quality assets. If that confidence is questioned, even briefly, the result could be rapid redemptions at scale. In that scenario, issuers would be forced to sell reserves, including U.S. Treasuries, potentially creating short-term dislocations in funding markets that are otherwise considered among the most stable in the world.

There is also the regulatory dimension, which remains unresolved. Policymakers must strike a balance between enabling innovation and imposing safeguards, but missteps in either direction carry consequences. Overregulation could push activity offshore and reduce transparency, while underregulation could allow systemic vulnerabilities to build unchecked. What makes this particularly complex is that stablecoins are no longer operating in isolation. As they become more integrated into payment systems, trading infrastructure, and Treasury markets, any disruption is less likely to remain contained, and more likely to ripple outward in ways that challenge both market stability and policy response.

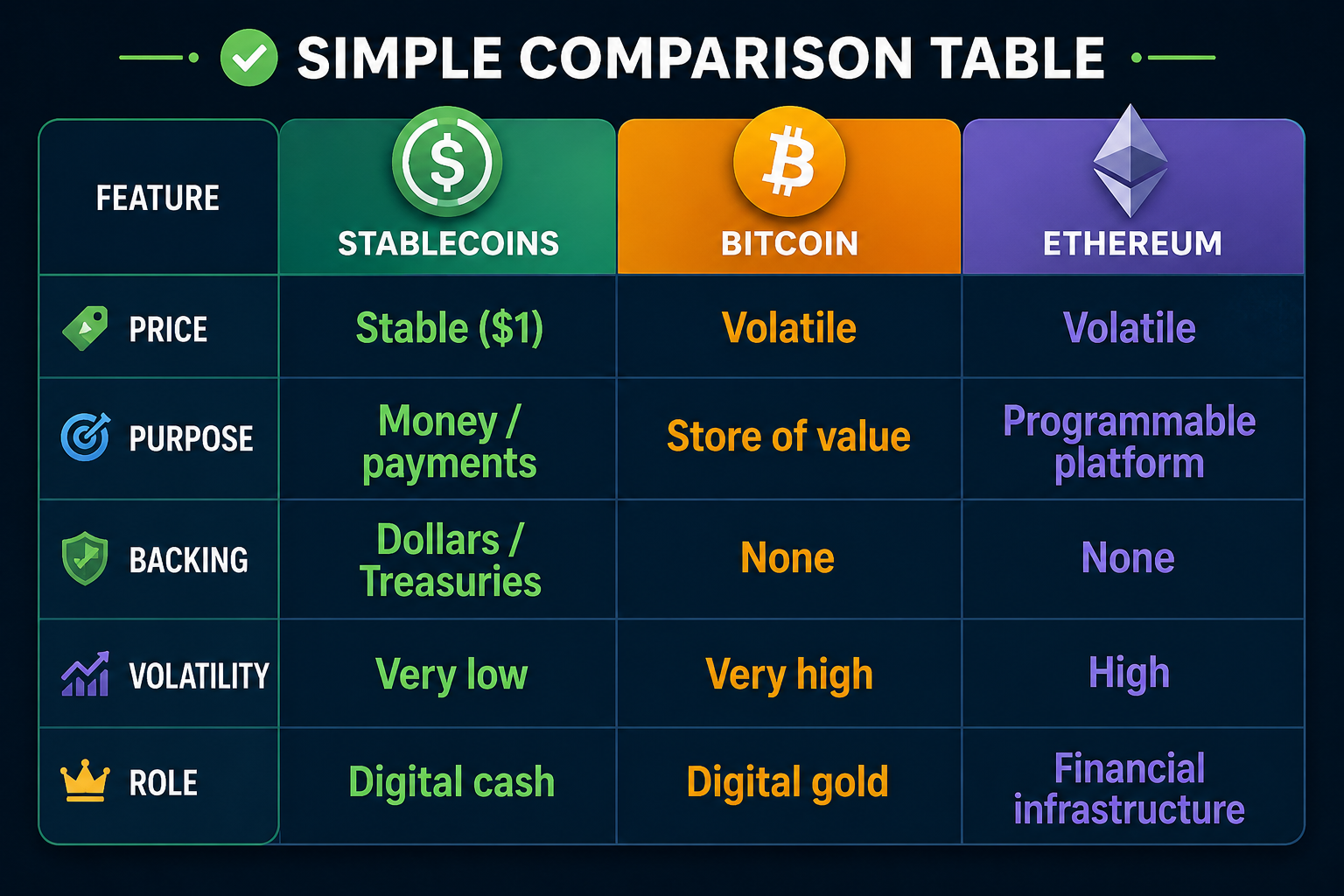

The easiest way to understand this graphic is to think of these three assets as having completely different jobs. Stablecoins are designed to act like digital cash. They stay close to $1 and are backed by dollars or U.S. Treasuries, so people use them to move money quickly around the internet. Bitcoin is different because it was built to be scarce, like digital gold, with a limited supply that cannot be endlessly printed. Ethereum is different again because it functions more like financial software infrastructure, allowing developers to build applications, contracts, and payment systems on top of it. They may all be part of the crypto world, but they solve very different problems, and understanding those differences is becoming increasingly important in modern finance.

Over the last hundred years, the world of audio evolved from long-playing vinyl records to 8-track tapes, cassettes, compact discs, and eventually digital MP3 files streamed instantly across the internet. Each transition changed not just the format, but the economics, distribution, ownership, and control of the entire industry. The same transformation is now unfolding in finance through crypto. Some projects are centralized systems where private companies manufacture digital tokens and promote their own vision of what money should be, while Bitcoin represents something fundamentally different: a decentralized monetary protocol with a fixed supply and no central authority controlling issuance. For traders and investors, understanding these distinctions is not academic. These are the architectural changes reshaping how value, trust, and capital will move through the global financial system over the coming decades.

The appeal of stablecoins is not especially ideological. It is operational. They promise to move money faster, cheaper, and with fewer constraints than the traditional banking infrastructure that has dominated global payments for decades. Transactions can settle nearly instantly rather than over several business days, transfer costs can fall from the typical $10 to $25 international wire fee to fractions of a dollar, and the system itself operates continuously, without regard for banking holidays, closing hours, or geographic borders. As long as two parties have access to digital wallets, dollar-based value can move across the world with a level of speed and accessibility that legacy financial systems were never designed to provide.

What makes the model more consequential, however, is the flexibility it introduces once money becomes fully digital and programmable. Stablecoins can be transferred, lent, pledged as collateral, or integrated into automated financial applications in ways that blur the line between payments infrastructure and capital markets infrastructure. That combination of efficiency and adaptability is precisely why stablecoins are attracting attention not only from traders and fintech firms, but increasingly from policymakers and institutions trying to understand what a digitally native dollar system could ultimately become.

For traders, the relevance of stablecoins is not theoretical. It is directional. Their growth is a signal, one that speaks to where liquidity is forming and how capital is moving beneath the surface. Watching the expansion or contraction of stablecoin supply can offer insight into broader risk appetite, funding conditions, and the health of the digital dollar ecosystem. At the same time, shifts in regulation or reserve composition can influence demand for short-term Treasuries, subtly shaping yields and liquidity in ways that may not be immediately visible on the surface.

The larger point is that this is not a headline-driven development. It is a structural one. Stablecoins sit at the intersection of global dollar demand and U.S. debt markets, and that positioning makes them worth monitoring with the same discipline applied to interest rates or capital flows. For traders focused on staying aligned with the underlying forces that move markets, the message is familiar: follow the money, even when it is moving through channels that did not exist a decade ago.

The defining word in finance over the next decade may very well be “tokenization.” At its core, tokenization simply means turning real-world assets into digital tokens that can move across blockchain networks the same way emails move across the internet. Today, when people hear the word crypto, they often think only of Bitcoin or speculation. But the larger transformation is much broader. Stocks, bonds, real estate, commodities, currencies, artwork, and even private company ownership stakes can potentially be represented digitally, traded instantly, divided into fractional ownership pieces, and transferred globally without relying on traditional financial plumbing. In many ways, finance is beginning the same transition media experienced when physical music and DVDs evolved into streaming digital files.

For traders and investors, this matters because tokenization has the potential to dramatically increase liquidity, accessibility, and speed across financial markets while simultaneously creating entirely new forms of competition and risk. Assets that were once illiquid may suddenly trade 24/7. Fractional ownership could broaden participation in markets historically limited to institutions or the wealthy. At the same time, the barriers to creating digital assets are falling rapidly, meaning the market could eventually be flooded with competing tokens, unstable projects, regulatory uncertainty, and new forms of leverage and volatility. The opportunity is enormous, but so is the complexity. Understanding tokenization is increasingly becoming less about understanding crypto and more about understanding where the architecture of modern finance itself is heading.

Markets no longer move at the speed of newspapers, television anchors, or quarterly reports. They move at the speed of algorithms, capital flows, and information traveling instantly across global digital networks. Entire trends can emerge, accelerate, and mature before the average investor fully understands what is happening. The rise of stablecoins, tokenization, and digital financial infrastructure is not a distant theory. It is happening now, quietly reshaping the way money moves, how assets trade, and where opportunity appears first.

The challenge for traders is not a lack of information. It is the overwhelming flood of it. Every day brings more headlines, more narratives, more opinions, and more noise competing for your attention. What most traders need is not another prediction. They need clarity. They need a way to identify where strength is building, where money is flowing, and where risk is quietly expanding beneath the surface. Because in modern markets, timing matters. And delayed awareness can be extraordinarily expensive.

This is precisely why traders around the world use VantagePoint AI Its predictive technology was designed to help traders cut through confusion and focus on what matters most: trend direction, market strength, and opportunity. By analyzing enormous amounts of intermarket data, VantagePoint AI helps traders recognize developing moves before they become obvious to the broader public. In markets increasingly shaped by speed, automation, and digital capital flows, having the right information a little earlier can make an extraordinary difference.

VantagePoint A.I. was built for one purpose: to help traders align themselves with the strongest trends before those trends become obvious to the crowd. It cuts through the endless clutter of headlines, opinions, and market noise to reveal where momentum is strengthening and where danger may be quietly forming. Instead of forcing traders to react emotionally to yesterday’s news, it provides a forward-looking perspective designed to help them act with greater clarity, discipline, and confidence.

If you want to better understand how professional traders are navigating this rapidly changing financial landscape, I invite you to attend a free live online AI masterclass and see VantagePoint AI in action for yourself. You will learn how traders are using artificial intelligence to identify opportunity, manage risk, and stay aligned with the strongest trends in the market before they become front-page news. In a world where financial change is accelerating, awareness is no longer optional. It is a competitive advantage.

See you at the masterclass.

It’s not magic.

It’s machine learning.

THERE IS A SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.IMPORTANT NOTICE!

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.